- Specialty & Fine Chemicals

- Fixing Agent Market

Fixing Agent Market Size, Share, and Growth Forecast, 2026 – 2033

Fixing Agent Market by Product Type (Chemical Fixing Agents, Liquid Fixing Agents, Powder Fixing Agents, Granular Fixing Agents, Gel Fixing Agents), Technology (Ion Exchange, Adsorption, Coagulation, Flocculation), and Regional Analysis for 2026 – 2033

Fixing Agent Market Size and Trends Analysis

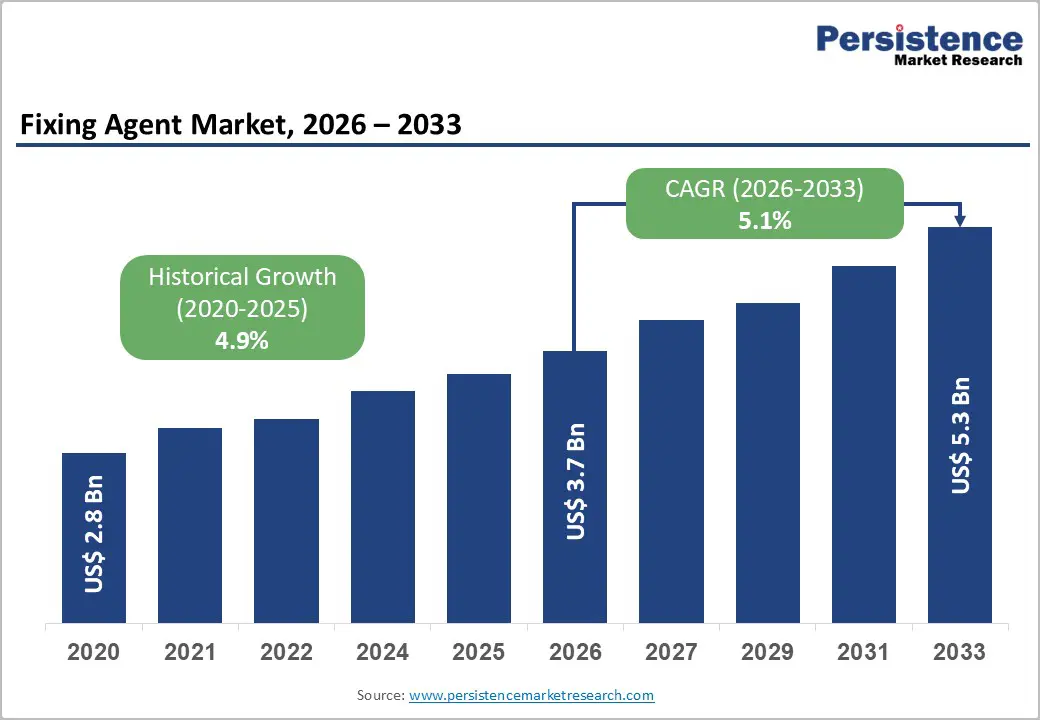

The global fixing agent market size is likely to be valued at US$3.7 billion in 2026 and is expected to reach US$5.3 billion by 2033, growing at a CAGR of 5.1% during the forecast period from 2026 to 2033, driven by expanding textile manufacturing activities, increasing quality standards for dyed and printed fabrics, and the transition toward sustainable chemical processing solutions. Fixing agents play a critical role in improving colorfastness, wash resistance, and durability of dyes across cotton, synthetic blends, and technical textiles, making them indispensable in modern textile processing.

Rapid industrialization in Asia Pacific, particularly in key textile-producing economies, continues to strengthen demand, while modernization of dyeing and finishing facilities is encouraging the adoption of advanced, low-formaldehyde and formaldehyde-free fixing formulations. In textiles, growing applications in paper processing, leather treatment, water treatment, and specialty industrial processes are broadening the market base. Regulatory pressure related to wastewater discharge, hazardous chemical reduction, and sustainable production standards is accelerating innovation in eco-friendly and biodegradable fixing chemistries.

Key Industry Highlights:

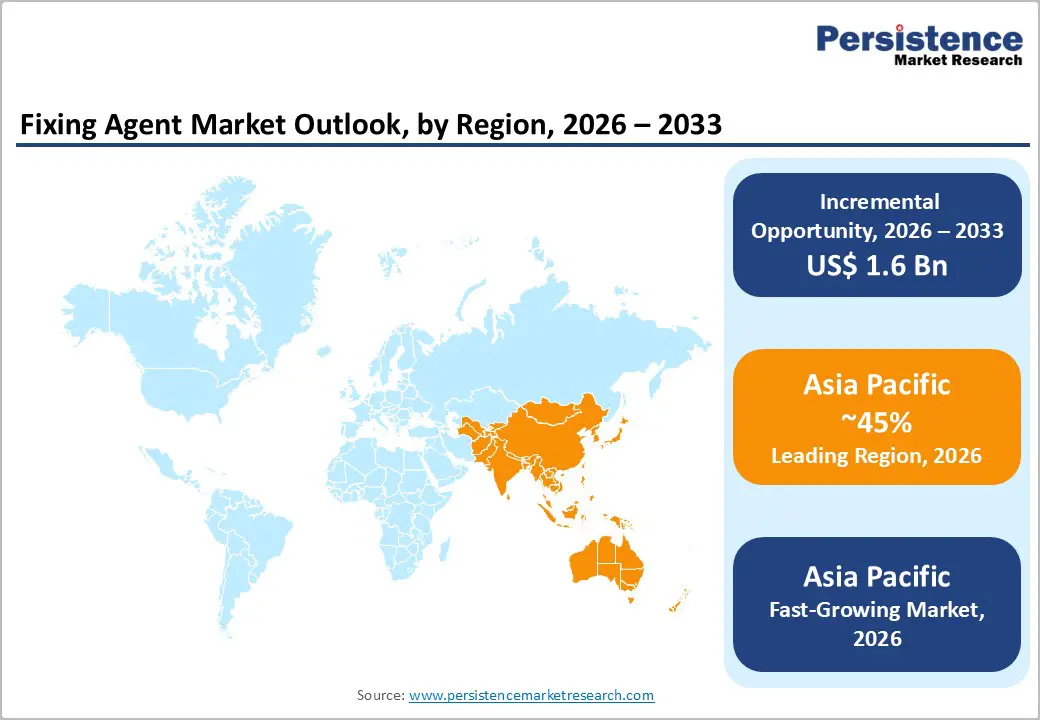

- Leading Region: Asia Pacific is anticipated to be the leading region, accounting for a market share of 45% in 2026, driven by its dominant textile manufacturing base and strong export-oriented production capacity.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region in the Fixing Agent in 2026, supported by rapid industrial expansion, increasing demand for high-performance dyed fabrics, and rising adoption of sustainable fixing technologies.

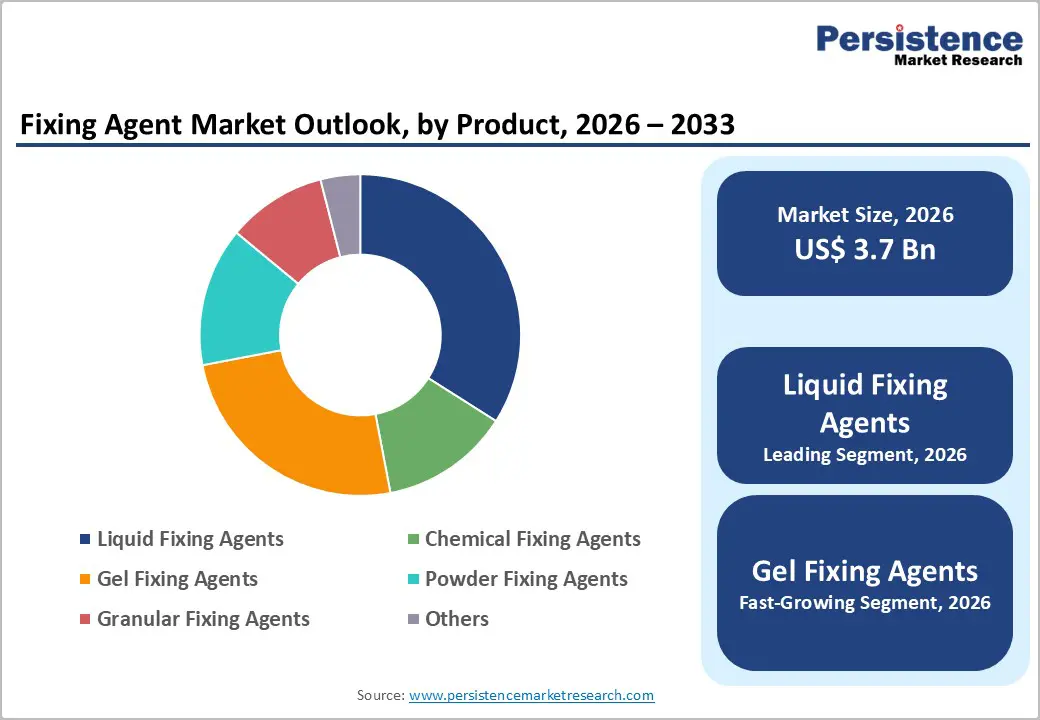

- Leading Product Type: Liquid fixing agents are projected to represent the leading product type in 2026, accounting for 55% of the revenue share, driven by their operational efficiency and compatibility with automated dyeing processes.

- Leading Technology: Ion exchange technology is anticipated to be the leading technology, accounting for over 50% of the revenue share in 2026, supported by its strong performance in improving dye fixation and wet fastness.

| Key Insights | Details |

|---|---|

| Fixing Agent Market Size (2026E) | US$3.7 Bn |

| Market Value Forecast (2033F) | US$5.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis- Shift toward Sustainable and Low-Impact Formulations

Regulatory frameworks across major textile-exporting regions are tightening restrictions on hazardous substances, formaldehyde emissions, and wastewater discharge standards. Manufacturers are reformulating products to meet eco-label certifications and international compliance benchmarks. Brands and apparel retailers are also demanding environmentally responsible dyeing auxiliaries to strengthen supply chain transparency and sustainability commitments. This shift is accelerating innovation in biodegradable, low-VOC, and formaldehyde-free fixing agents that reduce environmental burden while maintaining high colorfastness performance and processing efficiency standards.

Growing consumer awareness regarding sustainable fashion and responsible manufacturing is reinforcing demand for eco-friendly dye fixation solutions. Textile mills are adopting cleaner production technologies, including low liquor ratio dyeing and water recycling systems, which require compatible fixing chemistries. Suppliers investing in green chemistry research are gaining a competitive advantage through differentiated product portfolios. This transition is driven by regulatory compliance and supports long-term cost savings through reduced wastewater treatment, lower chemical consumption, and improved fabric durability.

Expansion of Technical Textiles and Specialty Applications

The rapid expansion of technical textiles across sectors such as automotive, medical, industrial filtration, sportswear, and protective clothing is significantly driving demand for advanced fixing agents. Technical textiles need stronger wash fastness, better chemical resistance, UV protection, and higher durability compared to regular apparel fabrics. Fixing agents enhance dye bonding strength and prevent color bleeding, ensuring long-term performance in demanding environments. As innovation in engineered fabrics accelerates, chemical auxiliaries must evolve to deliver precision application, compatibility with synthetic blends, and consistent quality in high-performance textile manufacturing systems worldwide.

Growth in digital printing, functional coatings, and performance apparel is increasing the need for specialized fixation solutions tailored to niche applications. Technical fabrics often undergo multi-stage processing, requiring fixing agents that maintain substrate integrity without compromising mechanical properties. Manufacturers are responding by developing high-efficiency chemistries optimized for polyester blends, microfiber materials, and smart textiles. As industrial and consumer markets prioritize performance-driven fabrics, the reliance on technologically advanced fixing agents continues to rise, strengthening their role beyond conventional dye houses and positioning them as critical enablers of specialty textile innovation.

Barrier Analysis - Fluctuations in Raw Material Supply

Many fixing agents rely on petrochemical derivatives, specialty polymers, and amine-based intermediates that are subject to price fluctuations influenced by crude oil trends, geopolitical disruptions, and trade restrictions. Supply chain bottlenecks can lead to inconsistent availability of critical inputs, impacting production planning and cost structures for manufacturers. Smaller producers are particularly vulnerable to procurement instability, which may compress margins and limit their ability to maintain competitive pricing in price-sensitive textile markets.

Environmental regulations affecting upstream chemical manufacturing can restrict access to certain intermediates, tightening supply conditions. Transportation disruptions, currency volatility, and regional trade barriers can amplify these challenges, especially for exporters dependent on cross-border sourcing. To mitigate risks, companies are diversifying supplier bases and investing in localized production capabilities. Persistent raw material uncertainty can delay expansion projects and discourage aggressive pricing strategies. Sustained price volatility shifts customer preference toward suppliers that offer stable contracts and integrated production capabilities.

Limited Awareness and Adoption in Price-Sensitive Developing Markets

Limited awareness regarding the performance benefits of advanced fixing agents restricts adoption in certain developing textile markets. Smaller dyeing units often prioritize immediate cost savings over long-term fabric durability or environmental compliance. Traditional fixation methods or low-cost substitutes may continue to dominate in fragmented manufacturing clusters where regulatory oversight is limited. This creates uneven demand patterns across regions, slowing penetration of premium and eco-friendly fixing formulations despite their technical advantages and efficiency benefits in industrial-scale production systems.

Capital constraints and limited technical training hinder the transition toward modern dyeing auxiliaries in emerging economies. Without adequate knowledge of optimized dosing, compatibility testing, and process integration, mills may hesitate to shift from established chemistries. Educational outreach, technical service support, and demonstration trials are essential to bridge this gap. Limited awareness and uneven regulatory enforcement across regions result in moderate adoption rates in cost-sensitive markets.

Opportunity Analysis - Technological Convergence with Digital Printing and Low-Liquor-Ratio Dyeing

The convergence of fixing agent technology with digital textile printing and low-liquor-ratio dyeing systems presents a significant growth opportunity. Digital printing requires precise droplet control, rapid fixation, and minimal migration to preserve design sharpness and color vibrancy. Advanced fixing chemistries tailored for these processes enhance binding efficiency while reducing water and chemical consumption. As textile producers modernize operations to improve productivity and sustainability, demand for compatible fixation solutions increases across both fashion and industrial textile segments.

Low-liquor-ratio dyeing systems, designed to reduce water usage and effluent generation, also require highly efficient fixing agents capable of operating in concentrated environments. These technologies optimize resource utilization while maintaining consistent shade reproducibility. Suppliers that develop formulations engineered for digital and resource-efficient platforms capture premium positioning in the market. Integration with smart manufacturing systems enhances process monitoring and dosage precision, creating opportunities for performance-based chemical solutions that align with Industry transformation trends in textile production.

Digital Printing Integration and Eco-Friendly Formulations

The integration of eco-friendly fixing agents within digital printing workflows offers a compelling opportunity for sustainable innovation. As fashion cycles accelerate and customization gains popularity, digital textile printing enables short production runs with reduced waste. Environmentally responsible fixation solutions complement this model by minimizing hazardous emissions and supporting compliance with sustainability certifications. Brands seeking transparent and traceable supply chains increasingly prefer dyeing auxiliaries that align with environmental, social, and governance objectives, strengthening demand for green fixing chemistries worldwide.

Advancements in bio-based polymers and waterborne formulations are expanding the functional capabilities of eco-conscious fixing agents. These innovations reduce dependency on traditional petrochemical inputs while maintaining high-performance color retention. Collaboration between chemical suppliers, textile machinery manufacturers, and apparel brands is fostering integrated product development. Sustainability becomes a competitive differentiator rather than a regulatory obligation; eco-friendly digital printing and compatible fixing agents are poised to unlock new market segments and long-term value creation within the evolving textile chemicals landscape.

Category-wise Analysis

Product Type Insights

Liquid fixing agents are expected to lead the fixing agent market, accounting for approximately 55% of revenue in 2026, driven by their operational efficiency and strong compatibility with modern textile processing systems. Their liquid form ensures uniform dispersion in dye baths, precise dosing control, and seamless integration with automated continuous dyeing lines used in large textile mills. Liquid formulations are particularly preferred in high-volume apparel manufacturing clusters where speed, reproducibility, and quality assurance are critical. For example, large cotton garment exporters in Asia widely use liquid cationic fixing agents in exhaust dyeing processes to enhance wash fastness and reduce reprocessing rates.

Gel fixing agents are likely to represent the fastest-growing segment, supported by increasing demand for controlled application and improved fixation performance in advanced textile processes. Gel-based formulations provide higher viscosity, which helps reduce dripping and uneven spread during application, particularly on dense or technical fabrics. Their structure enables better surface adherence and penetration control, making them suitable for precision-based operations such as digital textile printing and specialty fabric finishing. For example, manufacturers of performance sportswear fabrics use gel fixing agents to maintain sharp print definition while enhancing color durability on polyester blends.

Technology Insights

Ion exchange technology is projected to lead the market, capturing around 50% of the revenue share in 2026, supported by its strong effectiveness in improving dye fixation and wet fastness. This mechanism relies on electrostatic attraction between cationic fixing agents and anionic dyes, forming stable bonds on cellulosic and blended fibers. The approach is well established in conventional exhaust and pad dyeing systems, making it widely adopted in cotton and viscose processing. Its reliability, predictable performance, and compatibility with existing textile machinery contribute to its dominant position. For example, reactive dyeing of cotton fabrics commonly incorporates ion-exchange-based fixing agents to enhance wash durability and reduce color bleeding.

Adsorption based technologies are likely to be the fastest-growing technology, driven by their suitability for modern and resource-efficient textile processes. These systems function by binding dye molecules onto fiber surfaces through physical and chemical adsorption mechanisms, offering high surface affinity and controlled fixation. They are particularly effective in digital printing and low-liquor-ratio dyeing applications where precision and minimal migration are essential. For example, digital printed home textile manufacturers adopt adsorption-based fixing agents to preserve design clarity and reduce re-dyeing requirements. These technologies support formaldehyde-free formulations and contribute to lower effluent loads, aligning with environmental compliance standards.

Regional Insights

North America Fixing Agent Market Trends

North America is likely to be a significant market for fixing agents, driven by the region’s advanced textile manufacturing base and growing emphasis on sustainable dyeing solutions. This has created demand for high-performance fixing agents that deliver superior wash fastness, color retention, and compatibility with eco-friendly dyeing systems. For example, Huntsman Corporation, a major specialty chemical producer headquartered in the U.S., has been expanding its portfolio of sustainable dyeing and fixation solutions tailored to modern processing demands, reinforcing competitive dynamics in the North America fixing agent landscape.

Increasing collaboration between chemical suppliers and textile manufacturers to co-develop tailored solutions for niche fabric segments. This collaborative approach helps address technical challenges such as dye migration in blended fabrics, fixation on high-performance polymers such as nylon and polyester, and integration with automated dyeing lines. Sustainability remains a strong influence, with buyers seeking products that lower effluent loads and simplify wastewater treatment without compromising quality. Import of specialty textiles from overseas and subsequent finishing in North America is fostering demand for versatile fixing chemistries that can accommodate diverse fabric types and end-user requirements.

Europe Fixing Agent Market Trends

Europe is likely to be a significant market for fixing agents, due to strong regulatory influence, high sustainability standards, and a shift toward premium textile production. European textile manufacturers are increasingly focused on compliance with stringent environmental regulations such as REACH and wastewater discharge norms, which has driven demand for eco-friendly and low-impact fixing agents that reduce hazardous chemical use and effluent loads. For example, Archroma, a Switzerland-headquartered specialty chemicals company, has developed an extensive range of certified sustainable fixing agents under its ‘advanced denim chemistry’ portfolio, reinforcing its presence in compliance-driven European textile markets.

European textile clusters are emphasizing resource efficiency, water reuse, and chemical recycling initiatives that influence auxiliary selection, including fixing agents. Textile mills are transitioning to low-liquor-ratio dyeing technologies and improved effluent treatment systems, necessitating fixation solutions that are compatible with reduced water usage and high process automation. Sustainability becomes a core purchasing criterion for brands and manufacturers, regional fixation chemistries must balance performance with eco-credentials, driving suppliers to innovate with bio-based polymers and safer chemical alternatives.

Asia Pacific Fixing Agent Market Trends

The Asia Pacific region is anticipated to be the leading region, accounting for a market share of 45% in 2026, driven by expansive textile manufacturing hubs, strong export-oriented apparel industries, and rising consumption of dyed fabrics domestically and internationally. The region’s competitive cost advantages, integrated supply chains, and policy support for textile modernization also encourage the adoption of advanced fixing chemistries. For example, Fineotex Chemical Limited, a major India-based specialty chemical manufacturer, has expanded its portfolio of formaldehyde-free fixing agents designed for modern textile processing, reinforcing its position in Asia Pacific markets focused on quality and environmental compliance.

The rising demand from technical and value-added textile segments, including performance apparel, home furnishings, and industrial fabrics. These applications require high-performance fixation to ensure wash durability, abrasion resistance, and stable dye retention under rigorous use conditions. As manufacturers adopt advanced fabric blends and functional finishes, the need for specialized fixing agents that work effectively across diverse substrates is increasing. Regional players are collaborating closely with mills to optimize formulation performance for specific machinery and process conditions.

Competitive Landscape

The global fixing agent market exhibits a moderately fragmented structure, driven by the presence of numerous regional and multinational chemical manufacturers offering a wide range of fixation solutions for textile, paper, leather, and specialty applications. This fragmentation reflects varied customer needs across different end-use segments and geographic markets, with suppliers focusing on niche product capabilities such as eco-friendly formulations, formaldehyde-free chemistries, and solutions optimized for digital printing and low-liquor dyeing systems.

With key leaders including Fineotex Chemical Limited, CHT Group, Huntsman Corporation, and Archroma, the competitive landscape reflects a mix of established chemical giants and agile specialty producers. These players compete through product innovation, strategic partnerships, localized manufacturing footprints, and value-added technical service support tailored to customer process requirements. Investments in sustainable and compliance-aligned chemistries, along with targeted marketing in high-growth regions such as Asia Pacific and Latin America, help firms differentiate offerings.

Key Industry Developments:

- In February 2026, Techtextil announced a dedicated Textile Chemicals & Dyes segment at its 2026 trade fair, bringing together over 30 innovators, including Archroma, CHT Group, Sarex Chemicals, and others, to showcase the latest textile chemical solutions, including fixing agents, dyes, and finishing systems. This marks a major industry push toward collaboration and accelerated innovation in textile chemistry.

- In June 2025, Rudolf Group introduced HYDROCOL® NFN 01, a next-generation formaldehyde-free fixing agent for polyamide dyeing that eliminates phenol, bisphenol, and formaldehyde from the chemical process chain. This product is optimized to reduce environmental impact, improve wash fastness, and maintain high performance in exhaust and padding applications, reflecting industry pressure for safer, cleaner textile chemicals.

Companies Covered in Fixing Agent Market

- BASF SE

- Huntsman Corporation

- Archroma

- DyStar Group

- Kiri Industries Ltd.

- Sumitomo Chemical Co., Ltd.

- Zhejiang Longsheng Group Co., Ltd.

- Sarex Chemicals

- Jay Chemical Industries Limited

- Avocet Dye & Chemical Co. Ltd.

- Bozzetto Group

- Tanatex Chemicals

- Matex International Limited

- Fineotex Chemical Limited

- Zhejiang Runtu Co., Ltd.

Frequently Asked Questions

The global fixing agent market is projected to reach US$3.7 billion in 2026.

The fixing agent market is driven by rising demand for enhanced colorfastness and durable dye fixation in expanding textile and technical fabric production.

The fixing agent market is expected to grow at a CAGR of 5.1% from 2026 to 2033.

Key market opportunities lie in the development of eco-friendly, formaldehyde-free formulations and integration with digital printing and low-liquor-ratio dyeing technologies.

BASF SE, Huntsman Corporation, Archroma, DyStar Group, Kiri Industries Ltd., and Sumitomo Chemical Co., Ltd. are the leading players.