- Biotechnology

- Fibrinogen Testing Market

Fibrinogen Testing Market Size, Trends, Share, Growth, and Regional Forecast, 2025 to 2032

Fibrinogen Testing Market by Product (Devices, Kits & Reagents, Software & Services), Test (Lab-based Tests, Point-of-Care / Rapid Tests), Indication, End-user, and Regional Analysis from 2025 to 2032

Fibrinogen Testing Market Share and Trends Analysis

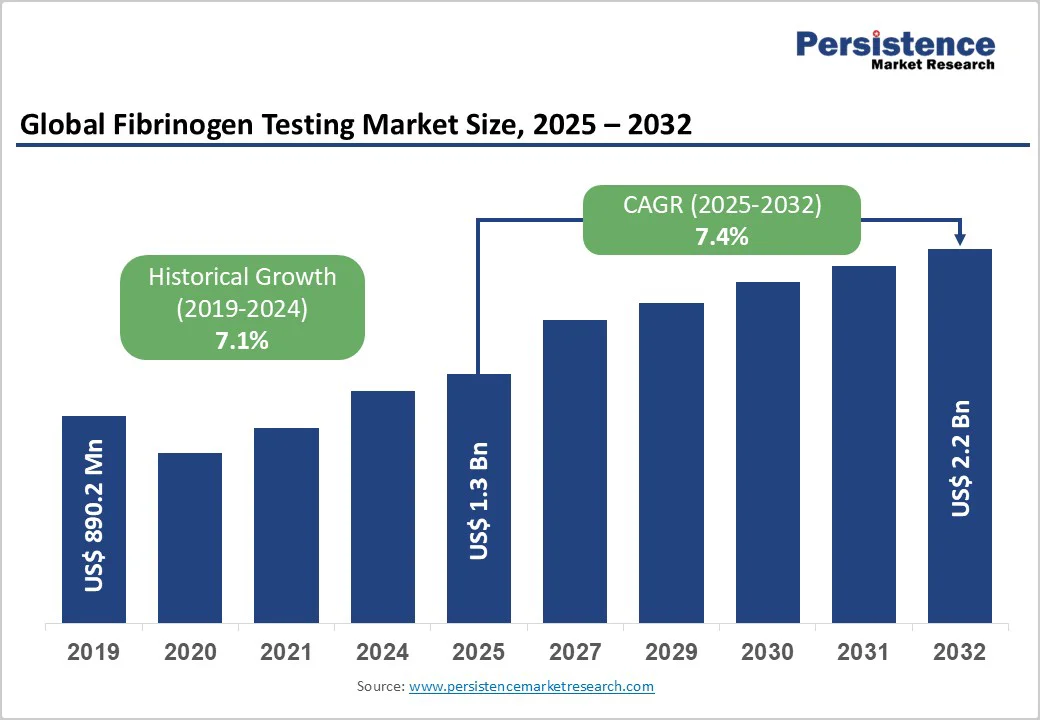

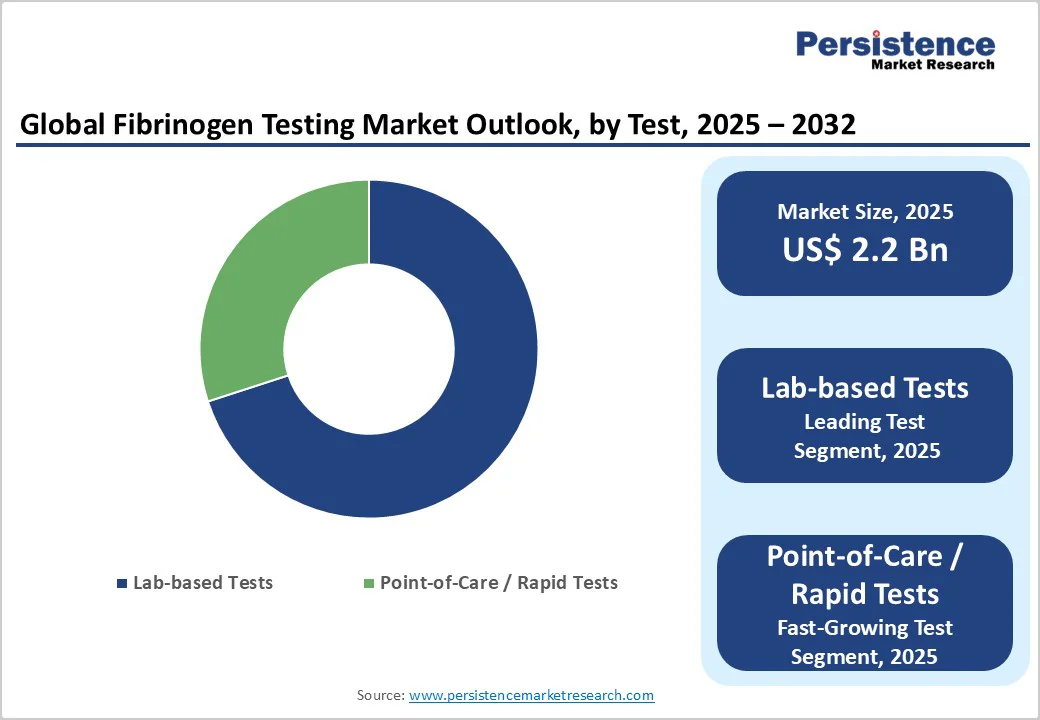

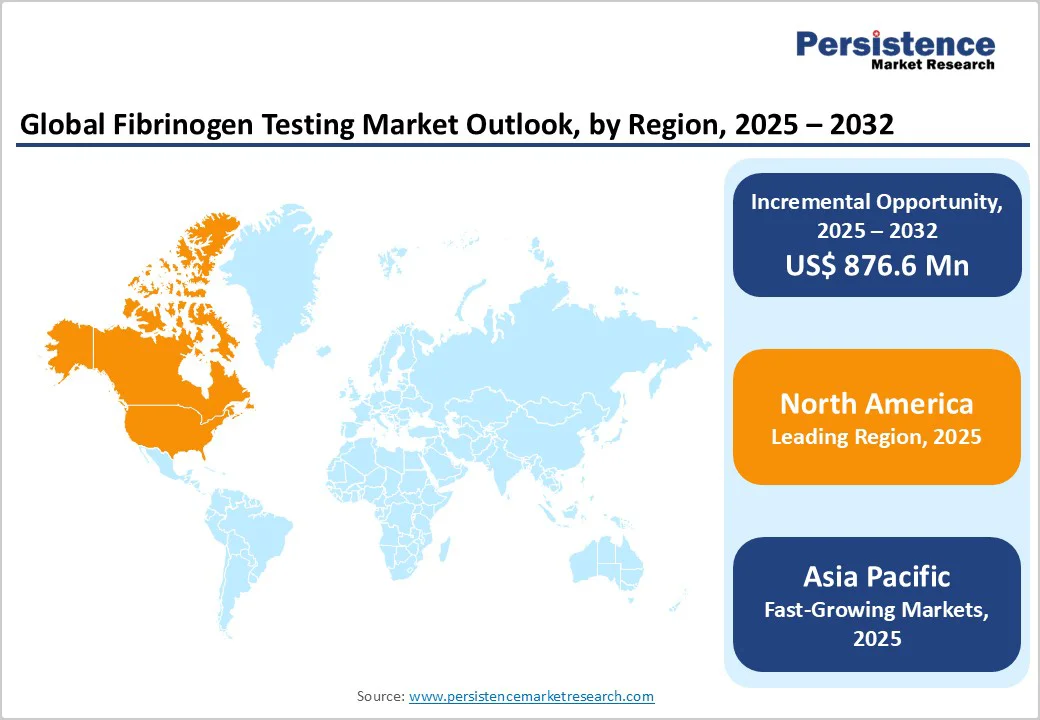

The global fibrinogen testing market size is likely to value US$ 1.3 billion in 2025 and is projected to reach US$ 2.2 billion by 2032, growing at a CAGR of 7.4% between 2025 and 2032. Fibrinogen is a vital high-molecular-weight glycoprotein in plasma that plays a central role in hemostasis and blood circulation.

Upon vascular injury, thrombin converts fibrinogen into fibrin, forming a stable clot to stop bleeding and repair tissue. Accurate measurement of fibrinogen levels is critical for assessing thrombotic and bleeding disorders, as low levels can trigger excessive coagulation, leading to thrombosis, heart attack, or stroke, while elevated levels are often linked to cardiovascular disease or inflammation.

Key Industry Highlights:

- Leading Region: North America is leading due to the high prevalence of cardiovascular and thrombotic disorders, extensive hospital networks, and established laboratory testing practices that support routine and specialized fibrinogen measurement.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region because of expanding clinical laboratory networks and increasing awareness of coagulation disorders.

- Leading Product: Kits and reagents are the leading product as they offer reliable performance and are widely used in diagnostic laboratories.

- Leading Test: Lab-based tests are the leading test due to standardized protocols, high accuracy, and extensive clinical experience.

- Fastest-Growing Test: Point-of-care tests are the fastest-growing test because they provide rapid results and improve accessibility in decentralized healthcare settings.

- Leading Indication: Inherited fibrinogen disorders are the leading indication owing to early diagnosis requirements and the need for precise patient monitoring.

- Expansion of clinical laboratories and diagnostic networks is enhancing accessibility of fibrinogen testing globally.

| Key Insights | Details |

|---|---|

| Global Fibrinogen Testing Market Size (2025E) | US$ 1.3 billion |

| Market Value Forecast (2032F) | US$ 2.2 billion |

| Projected Growth (CAGR 2025 to 2032) | 7.4% |

| Historical Market Growth (CAGR 2019 to 2024) | 7.1% |

Market Dynamics

Driver - Rising Burden of Chronic and Coagulation Disorders Boosts Fibrinogen Testing Demand

The growing global prevalence of diabetes and coagulation-related disorders is a key driver for the fibrinogen testing market. As of 2024, over 589 million adults worldwide live with diabetes, and many remain undiagnosed, increasing the need for regular blood monitoring (International Diabetes Federation (IDF) Diabetes Atlas (2025)).

Additionally, rising incidences of deep vein thrombosis, pulmonary embolism, and liver disease conditions, which are directly influencing clotting factors, are fueling routine coagulation profiling in clinical practice. Fibrinogen testing has therefore become essential for early detection and management of hypercoagulable states.

The adoption of automated coagulation analyzers and rapid reagents supports higher testing throughput and efficiency in diagnostic laboratories. Combined with expanding private and hospital-based laboratory networks, these epidemiological trends and technological improvements are strengthening the demand for fibrinogen testing as an essential component of patient management for thrombotic and coagulation-related conditions.

Restraints - High Equipment Costs and Limited Awareness Hinder Global Fibrinogen Testing Expansion

The global fibrinogen testing market faces significant barriers due to the high cost of advanced diagnostic equipment and limited awareness, particularly in developing regions. Advanced fibrinogen testing equipment can range from approximately $60 to $200 per test, making it financially challenging for smaller healthcare facilities and laboratories to adopt these technologies. This financial constraint limits the accessibility of fibrinogen testing, especially in low-resource settings.

Moreover, a lack of awareness about bleeding disorders and the importance of fibrinogen testing further impedes market growth. In many developing countries, there is insufficient knowledge about coagulation disorders, leading to underdiagnosis and undertreatment. This knowledge gap results in missed opportunities for early intervention and effective management of conditions related to abnormal fibrinogen levels.

These factors collectively contribute to the restrained growth of the global fibrinogen testing market, highlighting the need for increased education, awareness, and investment in affordable diagnostic solutions to enhance accessibility and early detection in underserved regions.

Opportunity - Expansion of Point-of-Care Fibrinogen Testing Devices Enhances Accessibility

The global fibrinogen testing market is witnessing rapid growth, driven by increasing awareness of coagulation disorders and the demand for faster, more accessible diagnostics. Advances in point-of-care (POC) technologies are enabling quicker and more reliable fibrinogen measurements, improving clinical decision-making and patient management across hospitals and remote healthcare settings.

A notable development in this space is the introduction of the qLabs® FIB by Diagnostica Stago. This novel POC device allows for the rapid measurement of functional fibrinogen levels from a single drop of citrated whole blood, providing lab-comparable results within 1 to 10 minutes. The device is particularly beneficial in critical care settings, such as obstetrics, where timely detection of declining fibrinogen levels can inform immediate therapeutic interventions.

Additionally, a study published in 2024 evaluated the accuracy of FibCare, a novel point-of-care testing device for rapid fibrinogen level assessment, demonstrating its potential for prompt clinical decision-making.

The adoption of such POC devices is expanding access to fibrinogen testing, especially in remote or resource-limited settings. Thereby, contribute to improved patient outcomes by enabling timely and appropriate treatment decisions. The integration of advanced POC fibrinogen testing devices presents a significant opportunity to enhance diagnostic capabilities, improve patient care, and drive market growth in the coming years.

Category-wise Analysis

By Product: Kits & Reagents Leads Due to Proven Reliability and Widespread Laboratory Use

Kits & reagents are expected to maintain the leading share of 57.4% in 2025. Their dominance is driven by reliable performance, compatibility with both automated and manual analyzers, and widespread adoption across hospitals and diagnostic laboratories.

These products provide reproducible results for routine and specialized fibrinogen testing, supporting both clinical decision-making and research applications. The longstanding experience of laboratories with these kits, along with ease of use and standardization, reinforces their continued preference in the global market.

By Test: Established Protocols and High Clinical Confidence Make Lab-based Tests a Dominant Category

Lab-based fibrinogen tests are projected to remain the leading segment, holding about one-third revenue share of the global market in 2025. Their prevalence is attributed to standardized protocols, higher accuracy, and extensive clinical experience in complex cases.

While point-of-care tests are growing due to portability and quick results, lab-based tests continue to dominate hospital and reference laboratory workflows, especially for critical patients and detailed coagulation profiling. These tests support precise diagnosis, monitoring, and treatment guidance in both inherited and acquired fibrinogen disorders.

By Indication: Inherited Fibrinogen Disorders Leading to Early Diagnosis and Treatment Importance

Inherited fibrinogen disorders are projected to dominate with a 31.1% value share in 2025. Their prominence stems from the necessity for early diagnosis, genetic screening, and continuous monitoring to prevent bleeding complications.

High clinical awareness and long-term management protocols make this segment significant, as accurate fibrinogen measurement informs replacement therapy and guides patient care. Hospitals and diagnostic centers increasingly prioritize testing for these disorders to support individualized treatment strategies, reduce morbidity, and improve long-term outcomes for patients with congenital fibrinogen deficiencies.

Regional Insights

North America Fibrinogen Testing Market Trends

North America continues to dominate the fibrinogen testing market with expected value share of 42.8% in 2025, driven by rising incidences of coagulation disorders, trauma, cardiovascular diseases, and surgical interventions requiring hemostasis monitoring. The region benefits from well-established diagnostic infrastructure, strong reimbursement frameworks, and early adoption of advanced coagulation analyzers.

Growing awareness of fibrinogen’s prognostic role during COVID-19, where elevated fibrinogen levels were linked to disease severity, further increased its routine clinical use across hospitals and ICUs. In 2023, U.S. healthcare spending reached nearly USD 4.9 trillion (about 17.6% of GDP), indicating robust investment in laboratory automation and rapid diagnostic technologies.

The introduction of automated Clauss-based systems, high-sensitivity immunologic assays, and portable point-of-care devices for bedside fibrinogen measurement is expanding accessibility and turnaround speed. Moreover, ongoing research into fibrinogen concentrates and biomarker-based precision medicine reinforces North America’s leadership in diagnostic innovation and clinical applications of fibrinogen testing.

Europe Fibrinogen Testing Market Trends

Europe represents a key region in the global market, projected to hold approximately 31.1% of the global market share by 2025. Europe’s fibrinogen testing market is advancing rapidly, shaped by evolving clinical guidelines, growing awareness of coagulation disorders, and greater laboratory standardization.

The European Medicines Agency’s (EMA) Scientific Guideline on Core Summary of Product Characteristics for Human Fibrinogen Products underscores the importance of accurate fibrinogen quantification for managing congenital and acquired deficiencies, prompting alignment of diagnostic protocols across member states.

Increasing recognition of fibrinogen’s prognostic role in bleeding, sepsis, and respiratory failure, highlighted in several studies published in the European Journals, has elevated testing demand in emergency and intensive-care settings. European laboratories, such as those following Laboklin’s coagulation panel standards, are adopting automated and high-sensitivity assays to ensure precision and reproducibility.

Furthermore, initiatives by clinical societies such as the European Federation of Internal Medicine and educational resources from Medthority are strengthening physician training in interpreting fibrinogen levels for complex bleeding and inflammatory conditions. Collectively, these clinical, regulatory, and educational drivers are positioning Europe as a leader in standardized, evidence-based fibrinogen testing and integrated coagulation diagnostics.

Asia Pacific Fibrinogen Testing Market Trends

Asia Pacific fibrinogen testing market is experiencing rapid expansion, projected to grow at a CAGR of around 9.2% during the forecast period. Rising cases of trauma, obstetric bleeding, liver disease, and disseminated intravascular coagulation (DIC) are driving diagnostic demand across developing economies.

The region’s growing healthcare investments-especially in China, India, Japan, and Southeast Asia-are fostering large-scale establishment of clinical laboratories and diagnostic networks to improve access to coagulation testing.

In August 2025, Malaysia-based Reszon Diagnostics, in collaboration with BioSynex, received approval from Indonesia’s Ministry of Health for the LabPad® Evolution Point-of-Care (PoC) device, along with Ksmart® and Tsmart® consumables. This initiative aims to expand decentralized coagulation testing across hospitals, community health centers (Puskesmas), and GP clinics.

Similar efforts to scale rapid testing infrastructure are underway in India and China through national diagnostic modernization and Make-in-India initiatives. Advancements in automated analyzers, portable PoC systems, and regional manufacturing partnerships are collectively enhancing the affordability, accessibility, and standardization of fibrinogen testing across the Asia Pacific region.

Competitive Landscape

The global fibrinogen testing market is highly competitive with the presence of several big players. The major players in the fibrinogen testing market are focusing on expanding their product offerings to increase revenue and market share.

Key Industry Developments:

- In January 2025, the exclusive distribution agreement between Roche and Sigma-Aldrich was renewed and extended until the end of 2029, continuing to cover products related to biochemical reagents.

- In December 2023, Thermo Fisher Scientific Inc., signed an exclusive distribution agreement with Aesku.Group to market, sell, and support their portfolio of FDA-Cleared IFA products, automated instruments, and software in the United States.

- In March 2023, Werfen acquired Immucor, Inc., a leading U.S.-based company in the in vitro diagnostics sector, expanding its portfolio in Transfusion and Transplant product lines including specialized diagnostic solutions for hospitals and clinical laboratories.

Companies Covered in Fibrinogen Testing Market

- F. Hoffmann-La Roche Ltd

- McKesson Medical-Surgical Inc.

- Siemens Healthineers

- Elabscience

- AFG Scientific

- Abcam Limited

- Thermo Fisher Scientific Inc.

- Helena Laboratories

- Labcorp

- Reszon Diagnostics International Sdn. Bhd.

- Shenzhen Micropoint Biotechnologies Co., Ltd.

- Stago

- Biosynex SA

- ICL, Inc.

- DIALAB

- Innovative Research

- CLOUD-CLONE CORP.(CCC)

- Instrumentation Laboratory Company

- Wuhan Fine Biotech Co., Ltd.

- r² Diagnostics

- Tulip Diagnostics (P) Ltd

- Diazyme Laboratories

- ARUP Laboratories

- Versiti

Frequently Asked Questions

The global fibrinogen market is projected to be valued at US$ 1.3 billion in 2025.

Increasing clinical use of fibrinogen as a biomarker for surgical bleeding risk, trauma management, and cardiovascular disease prognosis drive the global market.

The global fibrinogen market is poised to witness a CAGR of 7.4% between 2025 and 2032.

Expansion of point-of-care diagnostics and development of high-sensitivity fibrinogen assays for rapid, decentralized testing offer lucrative opportunities.

Major players in the global are F. Hoffmann-La Roche Ltd., McKesson Medical-Surgical Inc., Siemens Healthineers, Elabscience, Abcam Limited and others.