- Biotechnology

- Fermenters and Bioreactors Market

Fermenters and Bioreactors Market Size, Share, and Growth Forecast, 2026 – 2033

Fermenters and Bioreactors Market by Product Type (Bioreactors, Fermenters), Biologic Type (Antibodies, Vaccines, Cell Therapies, Other Biologics), End-User (Biopharmaceutical Companies, Contract Research Organizations (CROs), Academic & Research Institutions, Beverage Companies), and Regional Analysis for 2026-2033

Fermenters and Bioreactors Market Share and Trends Analysis

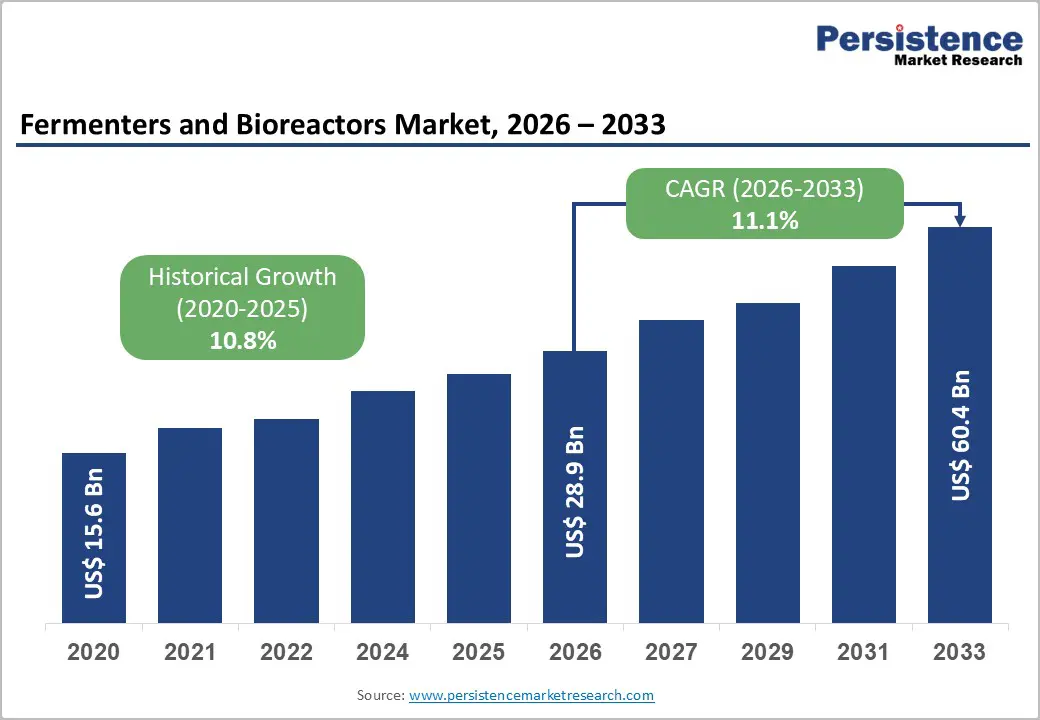

The global fermenters and bioreactors market size is likely to be valued at US$ 28.9 billion in 2026, and is projected to reach US$ 60.4 billion by 2033, growing at a CAGR of 11.1% during the forecast period 2026−2033.

Sustained biologics expansion, demographic health transitions, and manufacturing modernization are expected to drive double-digit growth across the forecast period. Aging populations and rising chronic disease incidence increase demand for monoclonal antibodies, vaccines, and cell-based therapies, directly elevating bioprocess capacity requirements. Increased clinical awareness and earlier therapeutic intervention accelerate biologic adoption across oncology, immunology, and rare disease segments, reinforcing upstream manufacturing investments. Regulatory encouragement for advanced therapies and pandemic preparedness frameworks supports localized production infrastructure development. Technological integration, including single-use systems, automation, and digital bioprocess control platforms, enhances scalability and reduces contamination risk, enabling flexible manufacturing models. Expansion of biopharmaceutical production facilities across emerging economies strengthens global supply resilience and supports capacity additions.

Key Industry Highlights

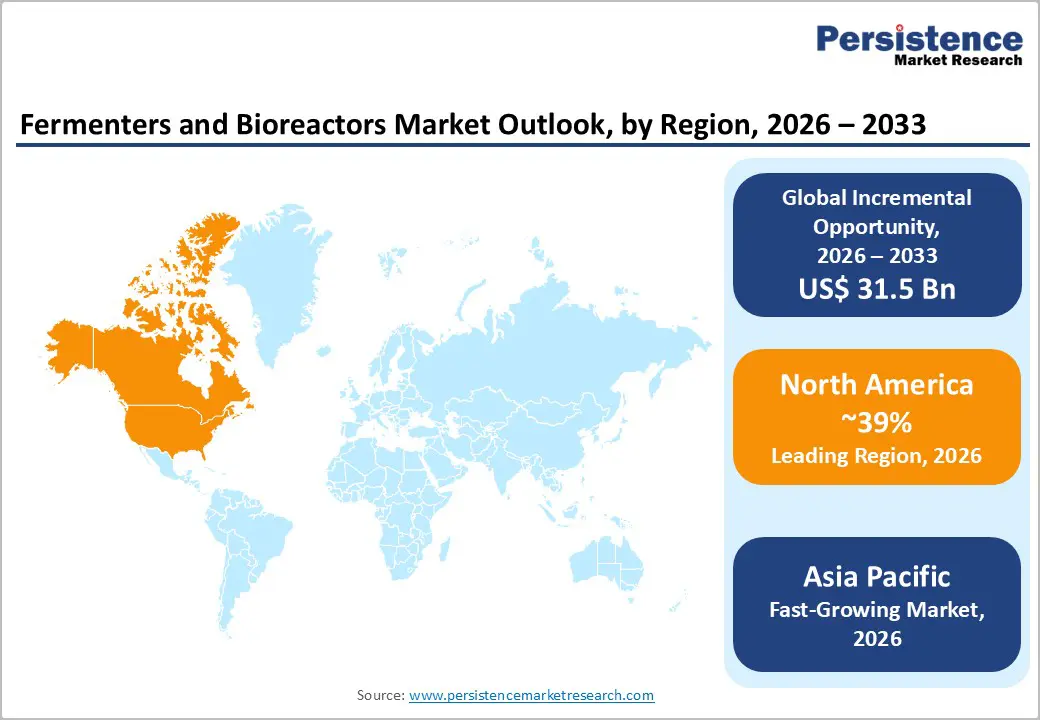

- Dominant Region: North America is expected to lead in 2026 with a share of roughly 39%, driven by strong biologics manufacturing capacity and advanced upstream technology adoption.

- Fastest-growing Market: Asia Pacific is projected to be the fastest-growing market from 2026 to 2033, supported by favorable biotechnology policies and cost efficient manufacturing models.

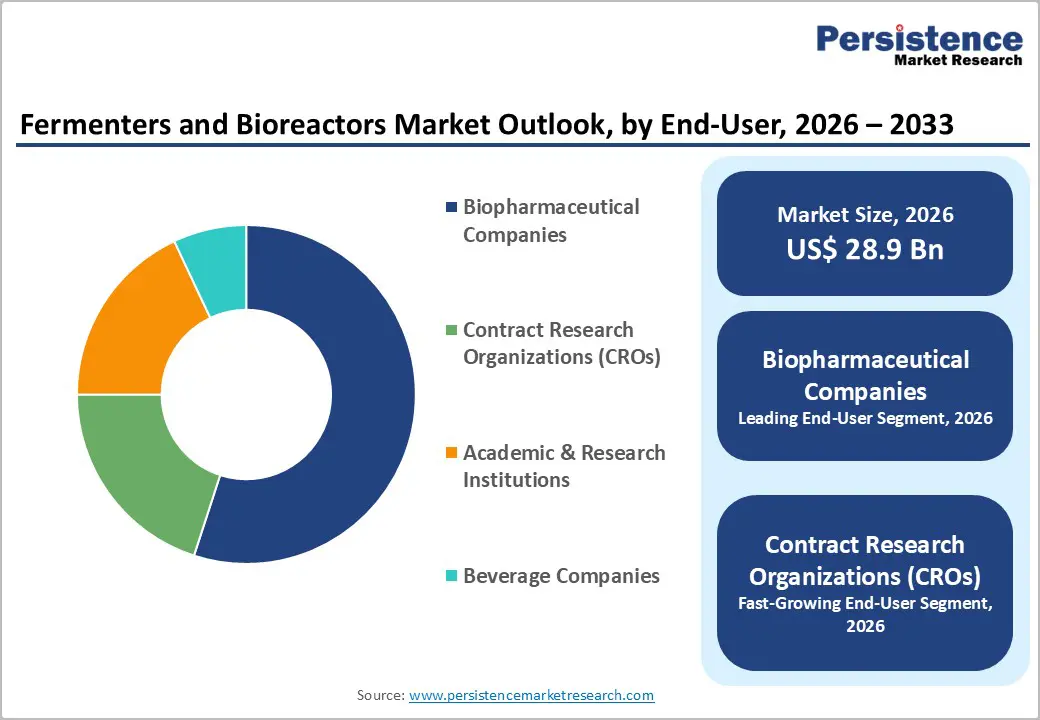

- Leading End-User: Biopharmaceutical companies are expected to hold around 55% market share in 2026, backed by large-scale biologics manufacturing and strong regulatory compliance.

- Fastest-growing End-User: Contract research organizations (CROs) are projected to grow the fastest between 2026 and 2033, fueled by rising outsourcing from emerging biotechnology firms and flexible capacity models.

| Report Attribute | Details |

|---|---|

|

Fermenters and Bioreactors Market Size (2026E) |

US$ 28.9 Bn |

|

Market Value Forecast (2033F) |

US$ 60.4 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

11.1% |

|

Historical Market Growth (CAGR 2020 to 2025) |

10.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Advancements in Bioprocessing Technology

Advances in bioprocessing technologies accelerate the efficiency and reliability of biological production systems by enabling continuous and flexible operations at scale. Government-sourced research highlights the emergence of single-use bioreactor systems as critical platforms in continuous manufacturing, reducing complexities associated with traditional cleaning and validation while improving operational economics. These platforms integrate real-time monitoring and control features that enhance process reproducibility and quality assurance, directly addressing regulatory expectations for consistency in biologic drug production. Single-use designs also support rapid changeovers and multi-product facilities, which are valuable in dynamic manufacturing environments where diversified therapeutic pipelines such as vaccines and biologics require adaptable production capacities.

Government strategy documents and public sector plans further reinforce the strategic importance of bioprocessing capability to national bioeconomies by prioritizing biotechnology innovation and infrastructure investment. Enhanced bioprocess technologies strengthen domestic biomanufacturing competitiveness by reducing barriers to scaling complex biological products, a priority for health security and economic resilience. The capability to reliably produce biologics and advanced therapies aligns with broader public health objectives, including supporting vaccine readiness and access to critical biologic treatments. Such alignment ensures that modern manufacturing technologies are not academic pursuits but foundational tools for meeting societal health demands.

Rising Demand from Demographic Shifts

Demographic transition across major economies is reshaping healthcare consumption patterns and production priorities. Rising life expectancy and declining fertility rates are expanding the proportion of older adults, increasing prevalence of chronic and degenerative conditions that require biologics, cell therapies, and advanced vaccines. According to the United Nations World Population Prospects 2025, the global population aged 65 years and above reached around 857 million in 2025. This structural shift intensifies demand for large-scale cell culture, microbial fermentation, and sterile processing capacity to support complex therapeutic pipelines.

Urbanization and income growth within emerging regions are reinforcing this trajectory by expanding access to diagnosis and specialty treatment. Public health authorities are strengthening immunization coverage, oncology programs, and chronic disease management frameworks, generating sustained production requirements for recombinant proteins, monoclonal antibodies, and biosimilars. Strategic national biotechnology missions in Asia and Europe prioritize domestic biologics manufacturing to secure supply resilience amid demographic pressure. Capital allocation therefore concentrates on stainless steel and single-use bioprocess platforms capable of rapid changeover and contamination control.

Operational Complexity and Skilled Workforce Constraint

The highly technical nature of bioprocessing operations increases the barrier to efficient implementation. Modern fermenters and bioreactors integrate advanced control systems, real-time monitoring platforms, sterile handling environments, and strict regulatory compliance protocols that require advanced technical competence. Training operators to manage these systems involves extended education, process validation exposure, and practical manufacturing experience, as operational decisions directly influence product yield, batch consistency, and compliance outcomes. Limited availability of experienced bioprocess engineers, automation specialists, and quality professionals creates gaps in facility readiness. This shortage constrains production scheduling, prolongs equipment commissioning timelines, and increases reliance on external technical consultants, raising operational expenditure and reducing internal capability development.

Operational complexity also influences scalability and risk exposure. Transitioning from laboratory-scale development to commercial-scale production introduces challenges related to mixing dynamics, oxygen transfer efficiency, contamination control, and process reproducibility. Each parameter requires precise calibration and continuous monitoring to prevent batch deviations and financial loss. Inadequate technical expertise limits the ability to troubleshoot deviations in real time, resulting in production interruptions and extended validation cycles. Integration of advanced automation and digital monitoring systems further intensifies skill requirements, as personnel must interpret high-volume data streams and manage process analytics platforms effectively.

Supply Chain Volatility and Component Dependency

Operational performance across advanced bioprocessing equipment manufacturing is highly exposed to instability in global sourcing networks and concentrated supplier ecosystems. Critical components such as single-use assemblies, control sensors, specialty valves, and high-grade stainless-steel vessels are frequently produced by a limited number of qualified vendors, creating structural dependence on cross-border trade flows. Disruptions linked to geopolitical tensions, freight bottlenecks, export controls, or raw material shortages translate directly into extended procurement cycles and elevated input costs. Government data underscores the strategic importance of supply resilience; in 2025, the white house formalized action to strengthen pharmaceutical supply security through the establishment of a Strategic Active Pharmaceutical Ingredients Reserve (SAPIR), reinforcing concerns regarding concentrated international dependencies.

Component qualification requirements further intensify the restraint. Equipment systems must meet stringent regulatory, sterility, and validation standards, limiting rapid substitution of alternative suppliers. Any interruption within a single node of the supplier base can delay installation timelines, commissioning schedules, and facility expansion projects. Capital expenditure planning becomes more complex under fluctuating pricing for precision parts and biocompatible materials. Logistics uncertainty increases inventory holding costs as manufacturers maintain buffer stock to mitigate risk. Elevated working capital allocation and extended project lead times constrain scalability and reduce margin stability.

Opportunity Analysis- Emerging Market Biomanufacturing Infrastructure Development

Rapid build-out of biomanufacturing infrastructure in emerging markets represents the most compelling strategic opportunity because it directly expands production capacity for biologics, vaccines, and industrial biotechnology at a time when global demand for these products is accelerating. Governments in several emerging economies have introduced high-performance biomanufacturing platforms and bioeconomy policies intended to support commercialization, scale-up, and innovation in biotechnology manufacturing. India’s bioeconomy has grown from US$ 10 billion in 2014 to about US$ 165.7 billion by 2024, and national targets aim to further expand this base toward $300 billion by 2030 as part of a broader strategy to position the country as a global manufacturing hub. Public investment and policy frameworks mitigate foundational barriers that have historically limited manufacturing adoption, such as access to shared facilities, regulatory navigation, and high upfront capital requirements.

Emerging market infrastructure expansion also strengthens supply chain resilience and reduces dependence on imported biologics and therapeutics. By anchoring production closer to large and growing regional demand centers, manufacturing hubs improve responsiveness to public health needs, reduce lead times, and attract further foreign direct investment. This creates a virtuous cycle of talent development, technological diffusion, and domestic innovation. For equipment suppliers and technology partners, this trend unlocks sustained demand for scale-up bioprocess equipment across a broader base of users and applications.

Digital Bioprocessing and Modular Manufacturing Integration

Integration of digital bioprocessing with modular manufacturing represents a structural shift in how bioprocess assets are designed, operated, and scaled. Government policy direction in 2025 reflects this transition, with initiatives such as the BioE3 Biotechnology for Economy, Environment and Employment policy approved by the Union Cabinet of India, which emphasizes advanced manufacturing platforms, biofoundries, and digitally enabled infrastructure to strengthen biomanufacturing capabilities. Digital platforms enable real time process visibility, closed loop control, and data driven decision making across fermentation and cell culture operations. Modular manufacturing complements this capability through standardized and relocatable production units that shorten deployment timelines and support rapid capacity adjustments.

From a business perspective, this integration supports capital efficiency and operational resilience. Modular facilities allow phased investments aligned with demand evolution, reducing exposure to long construction cycles and fixed infrastructure risk. Digital bioprocessing strengthens process predictability, supports technology transfer across sites, and enables faster scale up from development to commercial production. This model also facilitates decentralized manufacturing strategies, supporting regional production, supply security, and faster response to therapeutic or industrial demand shifts. Workforce productivity improves through automation and decision support systems that reduce manual intervention and error rates.

Category-wise Analysis

Biologic Type Insights

Antibodies are likely to be the leading segment with a projected 38% of the fermenters and bioreactors market revenye share in 2026, due to sustained oncology and immunology pipeline activity and strong clinician confidence in targeted biologic therapy. Regulatory approvals from agencies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) validate therapeutic reliability and encourage broader prescription patterns across developed and emerging healthcare systems. Expanding indications in solid tumors and autoimmune disorders sustain commercial momentum. Preventive healthcare programs and early diagnostic screening frameworks increase eligible patient pools and accelerate therapy initiation timelines. Distribution through hospital procurement systems and specialty pharmacy networks enhances product accessibility and reimbursement coordination.

Cell therapies are poised to witness the fastest growth between 2026 and 2033, powered by increasing investment in regenerative medicine and personalized oncology treatment. Clinical validation across hematologic malignancies and select rare genetic disorders strengthens physician confidence and treatment adoption in tertiary care centers. Expansion of clinical trial pipelines and translational research collaborations accelerates commercialization pathways. Greater awareness among patients and advocacy groups improves acceptance of advanced therapy medicinal products. Digital engagement channels support education, referral networks, and enrollment efficiency in specialized treatment programs.

End-User Insights

Biopharmaceutical companies are slated to hold a dominant position, with an anticipated 55% of the revenue share in 2026, driven by extensive commercial manufacturing operations and established regulatory compliance infrastructure. Large scale production facilities support sustained output of monoclonal antibodies, recombinant proteins, and advanced biologics across multiple therapeutic areas. Strong clinical credibility and long standing provider referral networks reinforce prescribing confidence and volume stability. Vertical integration strategies support tighter control over quality, supply continuity, and cost management, encouraging in house capacity expansion. Digitalization of production environments improves process consistency, deviation management, and real time performance oversight.

CROs are forecasted to be the fastest-growing end-user segment through 2033, boosted by outsourcing trends among emerging biotechnology firms seeking cost-efficient development pathways. Early stage innovators increasingly rely on external partners to reduce fixed infrastructure investment and accelerate development timelines. Technology enabled service models enhance project transparency, data sharing, and regulatory documentation efficiency. Flexible capacity frameworks allow rapid onboarding of diverse programs across discovery, clinical, and pilot scale phases. Adoption of modular bioreactor configurations supports multi-client scheduling and quick process changeovers.

Regional Insights

North America Fermenters and Bioreactors Market Trends

North America is expected to dominate with an estimated 39% of the fermenters and bioreactors market share in 2026, reflecting concentration of large scale biologics manufacturing assets and sustained investment in advanced upstream processing platforms. Leadership is driven by high commercial output of monoclonal antibodies, recombinant proteins, vaccines, and emerging cell and gene therapies that rely on precision controlled fermentation and cell culture systems. A strong presence of integrated biopharmaceutical manufacturers and contract development and manufacturing organizations supports continuous capacity expansion and equipment modernization. Advanced regulatory science capabilities and mature quality frameworks encourage early adoption of intensified bioprocessing, single use reactors, and hybrid production architectures.

Structural and financial advantages further reinforce market leadership. Access to deep capital pools enables rapid funding of greenfield facilities and large scale retrofitting of existing plants with automation, digital monitoring, and modular production units. A highly specialized bioprocess engineering workforce supports deployment of continuous manufacturing, perfusion culture, and high cell density operations that require advanced reactor design and control. Strategic public health preparedness programs sustain baseline biologics and vaccine production volumes, stabilizing long term equipment utilization.

Europe Fermenters and Bioreactors Market Trends

Europe maintains a significant position supported by coordinated regulatory standards under the EMA and cross-border research collaboration programs, enabling efficient development, scale up, and commercialization of biologics and advanced therapies. Harmonized regulatory pathways reduce complexity for multi country manufacturing operations and encourage early investment in compliant upstream processing infrastructure. Strong public funding mechanisms for biotechnology, vaccine preparedness, and advanced therapy medicinal products sustain long term demand for fermenters and bioreactors across clinical and commercial stages. A well-established biosimilar ecosystem drives continuous utilization of large scale cell culture systems, while industrial biotechnology initiatives expand fermentation demand for sustainable chemicals, enzymes, and bio based materials.

Market structure is characterized by high specialization and technology depth. Leadership in continuous bioprocessing, perfusion culture, and precision fermentation supports manufacturing of complex biologics and next generation vaccines. Strong collaboration between academic institutions, public research bodies, and private enterprises accelerates translation of innovation into scalable manufacturing workflows. Digital batch records, advanced process analytical technologies, and automation frameworks enhance quality oversight and operational efficiency under stringent compliance requirements. Aging production infrastructure across several countries creates steady replacement demand, while transition toward flexible multi product facilities increases adoption of modular and single use bioreactor configurations.

Asia Pacific Fermenters and Bioreactors Market Trends

Asia Pacific is forecasted to be the fastest-growing market for fermenters and bioreactors between 2026 and 2033, propelled by accelerated biologics manufacturing expansion, supportive biotechnology policies, and rising investment in localized production infrastructure. Large scale capacity additions across China, India, South Korea, Singapore, and select Southeast Asian economies are reshaping global upstream manufacturing distribution. National biotechnology roadmaps prioritize domestic vaccine, biosimilar, and cell therapy production, stimulating procurement of advanced fermentation and cell culture systems. Cost efficient construction models and faster facility commissioning timelines attract multinational biopharmaceutical companies seeking diversified manufacturing footprints. Expansion of contract development and manufacturing organizations strengthens technology transfer pipelines and increases demand for scalable pilot and commercial reactors.

Structural transformation of manufacturing ecosystems reinforces this growth outlook. Adoption of modular facilities and single use bioreactor platforms aligns with demand for rapid scale up and multi product flexibility. Workforce development programs and academic industry collaboration enhance availability of skilled bioprocess engineers and automation specialists, supporting operational efficiency. Regulatory modernization initiatives improve approval timelines and harmonize quality standards with global benchmarks, strengthening export readiness. Increasing focus on biosimilar affordability strategies expands production volumes, sustaining long term utilization of fermentation assets. Digital integration across production sites improves monitoring, batch consistency, and predictive maintenance, enhancing return on capital deployment.

Competitive Landscape

The global fermenters and bioreactors market structure demonstrates moderate consolidation with multinational corporations holding significant global share alongside specialized regional manufacturers. Leading players leverage broad product portfolios spanning laboratory, pilot, and commercial scale systems, enabling engagement across the full bioprocess development lifecycle. Global service and support networks strengthen long term customer relationships through installation, validation, maintenance, and process optimization services. Competitive strength is reinforced by sustained investment in automation, digital bioprocess control, and data integration capabilities that address rising demand for process consistency and regulatory compliance. System scalability remains a core differentiator, with suppliers focusing on flexible platforms that support seamless transition from research to commercial production.

Key participants such as Sartorius, Applikon Biotechnology, Shanghai Bailun Biological Technology, Merck, Solaris Biotech, and Cytiva shape competitive dynamics through targeted innovation and strategic positioning. Sartorius and Merck emphasize integrated upstream solutions combined with consumables and digital tools, strengthening recurring revenue streams. Cytiva and Applikon Biotechnology focus on modular and customizable bioreactor platforms that support intensified and single use processing models. Solaris Biotech differentiates through engineering flexibility and tailored solutions for specialized fermentation applications. Shanghai Bailun Biological Technology strengthens competitiveness through cost optimized systems aligned with regional manufacturing expansion.

Key Industry Developments

- In December 2025, Tetra Pak Processing Equipment SIA acquired Bioreactors.net, a Latvia-based bioreactor system designer and manufacturer, to accelerate development of advanced fermentation solutions for precision and biomass-derived New Food production.

- In December 2025, Sunflower Therapeutics completed the installation of multiple Daisy Petal™ perfusion bioreactor systems at Serum Institute of India’s GMP facility, enhancing high-yield protein production capacity for vaccine manufacture.

- In June 2025, Aragen announced it will start Good Manufacturing Practice (GMP) biologics production at its Bangalore facility in late July, featuring intensified fed batch platforms and flexible single-use bioreactors to support scalable contract manufacturing operations.

Companies Covered in Fermenters and Bioreactors Market

- Sartorius

- Applikon Biotechnology

- Shanghai Bailun Biological Technology

- Merck

- Solaris Biotech

- Cytiva

- Solida Biotech

- Parr Instrument Company

- Eppendorf

- Bionet

- Ollital Technology

Frequently Asked Questions

The global fermenters and bioreactors market is projected to reach US$ 28.9 billion in 2026.

Increasing production of biologics, vaccines, biosimilars, and cell based therapies, along with the need for scalable, automated, and regulatory compliant bioprocessing systems, is driving the market.

The market is poised to witness a CAGR of 11.1% from 2026 to 2033.

Key market opportunities include digital bioprocess integration, modular manufacturing expansion, single use system adoption, and capacity build out in emerging biopharmaceutical production hubs.

Some of the key market players include Sartorius, Applikon Biotechnology, Shanghai Bailun Biological Technology, Merck, Solaris Biotech, Cytiva, Solida Biotech, Parr Instrument Company, Eppendorf, Bionet, and Ollital Technology.