- Specialty & Fine Chemicals

- Esterquats Market

Esterquats Market Size, Share, and Growth Forecast 2026 - 2033

Esterquats Market by Product Type (TEA-quats, MDEA & Others), by Form (Solid/Paste, Liquid), by Feedstock (Tallow-based, Vegetable-based), by Application (Fabric Care Products, Personal Care Products, Others), by Regional Analysis, 2026 - 2033

Esterquats Market Size and Trend Analysis

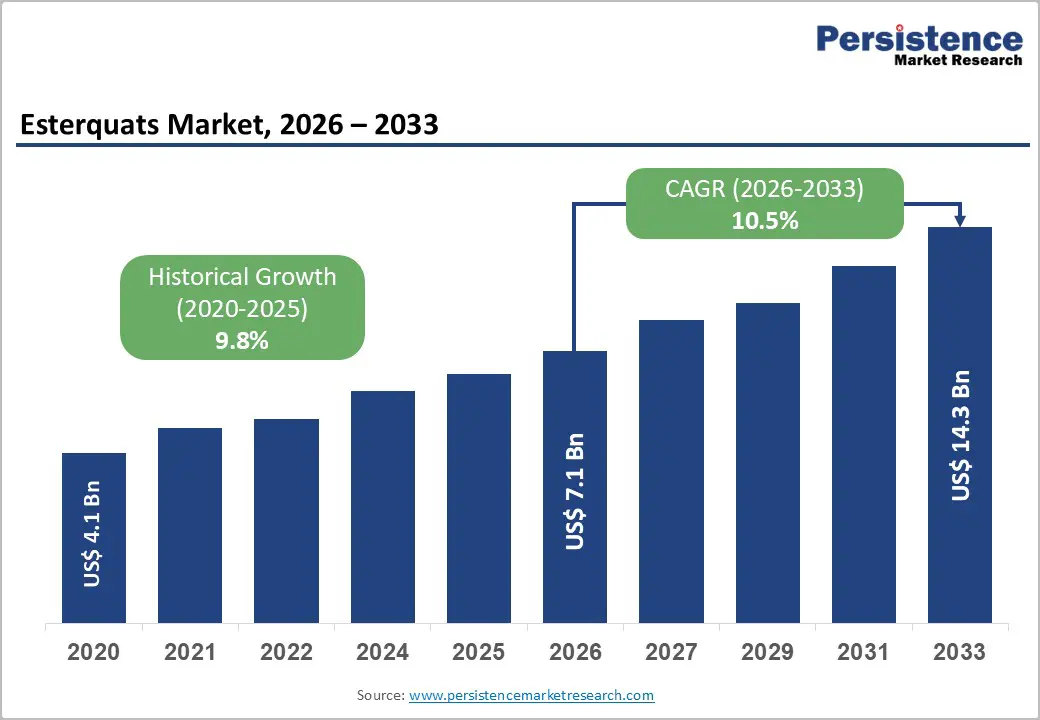

The global esterquats market is projected to reach US$ 7.1 billion in 2026 and US$ 14.3 billion by 2033, growing at a CAGR of 10.5% over the forecast period.

Market expansion is driven by rising demand for biodegradable fabric care products, the rapid growth of premium personal and hair care categories, and the expansion of manufacturing in the Asia-Pacific region, supported by increasing sustainability awareness.

Key Industry Highlights:

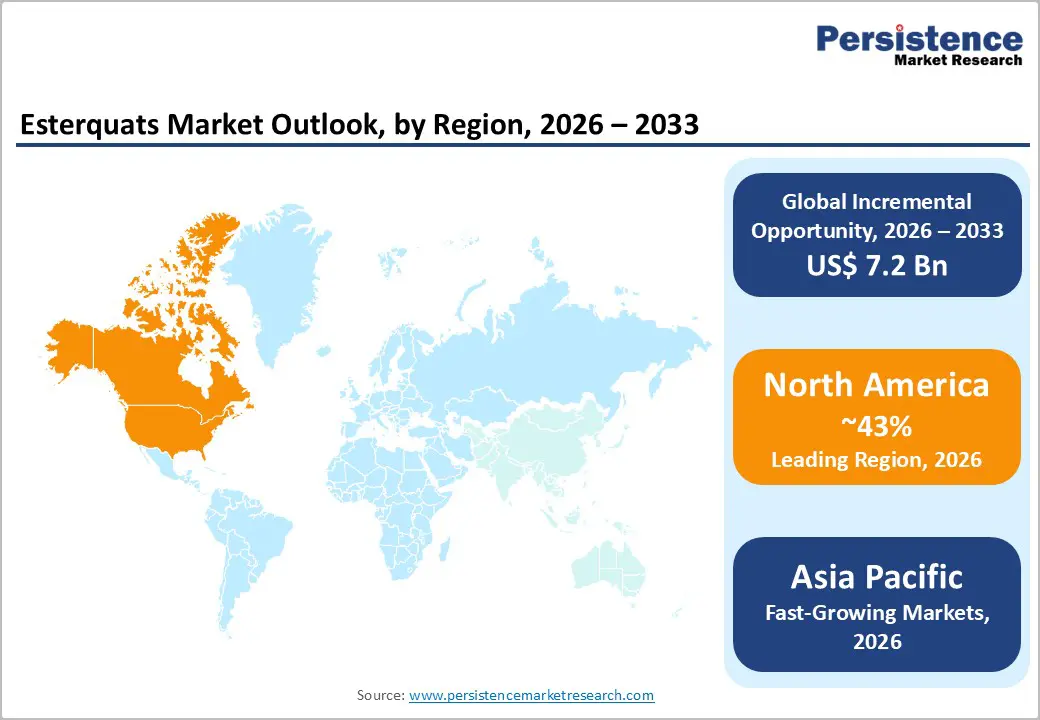

- Leading Region: North America is likely to maintain established dominance, holding 43% share, driven by mature fabric care and personal care industries, stringent environmental regulations, and substantial consumer demand for biodegradable, premium-positioned esterquat-containing household and personal care products.

- Fastest-Growing Region: Asia Pacific experiences the fastest regional growth at 12.4% CAGR in China and 11.5% CAGR in India, driven by rapid manufacturing expansion, rising consumer awareness, systematic product innovation integration, and strategic manufacturer partnerships supporting exceptional market development.

- Leading Segment: TEA-quats command 43% market share, driven by proven effectiveness, superior biodegradability, excellent skin and hair compatibility, and well-established manufacturing supporting widespread commercial adoption and customer confidence.

- Fastest Growing Segment: Liquid esterquats dominate the market form segment with superior solubility, uniform distribution in formulations, and compatibility with modern personal care and household cleaning processes, supporting premium product development and expanded application scope.

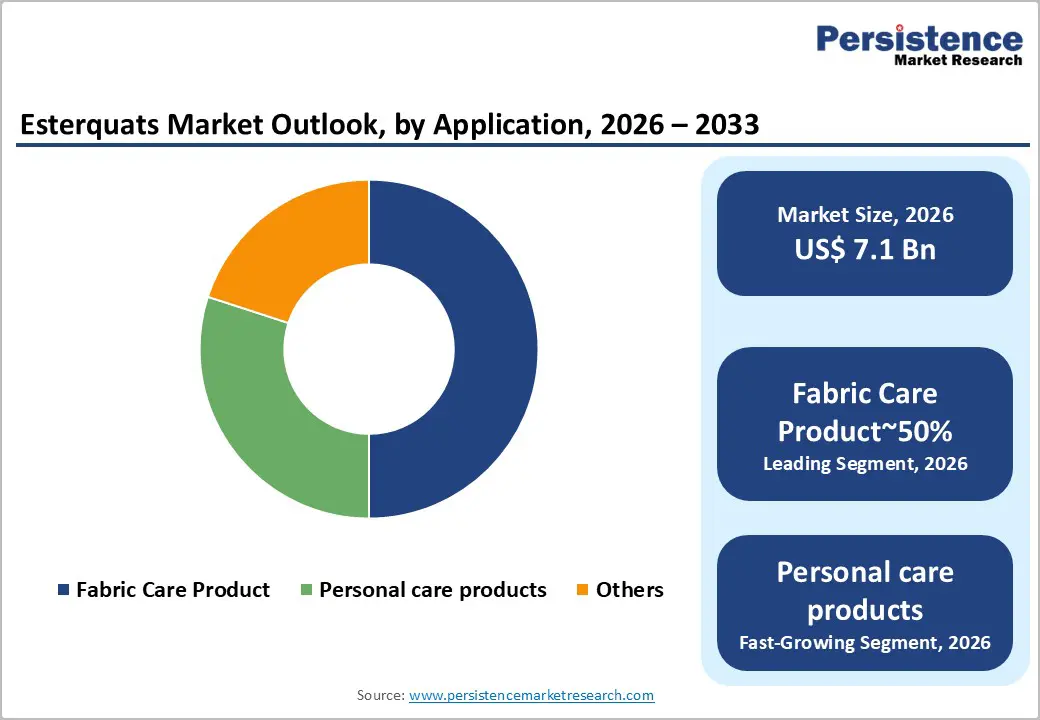

- Key opportunity: Personal care applications, including hair conditioners, treatment masks, serums, and sophisticated body care products, represent the fastest-growing market segment, driven by rapid category expansion and consumer demand for multi-functional conditioning solutions.

| Key Insights | Details |

|---|---|

| Esterquats Market Size (2026E) | US$ 7.1 Billion |

| Market Value Forecast (2033F) | US$ 14.3 Billion |

| Projected Growth CAGR (2026 - 2033) | 10.5% |

| Historical Market Growth (2020 - 2025) | 9.8% |

Market Dynamics

Drivers - Rising Demand for Sustainable and Biodegradable Fabric Care Formulations

The global shift toward environmental sustainability is strongly influencing the fabric care industry, driving manufacturers to replace traditional quaternary ammonium compounds with more eco-friendly esterquats. Increasing regulatory pressure and growing consumer awareness around environmental safety are accelerating this transition. Regulations such as the European Union Detergents Regulation (648/2004) require all surfactants used in detergent products to meet strict aerobic biodegradability standards, which clearly favor esterquats due to their superior environmental performance.

Compared to older surfactants like DHTDMAC, esterquats offer lower aquatic toxicity, faster biodegradation, and improved safety profiles, making them more suitable for long-term regulatory compliance. As a result, esterquats have become the preferred choice in North America and Europe for fabric softener formulations. Leading consumer goods companies are increasingly launching plant-based and concentrated products using esterquats to strengthen eco-friendly brand positioning. For example, Procter & Gamble introduced plant-based Downy fabric softeners in October 2023, reflecting strong market alignment with sustainability-driven consumer demand.

Rapid Expansion of Hair Care and Personal Care Product Categories Driving Esterquat Consumption

The fast-growing hair care and personal care industries are becoming major drivers of esterquat demand, supported by changing lifestyles and rising expectations for premium, multifunctional products. Consumers increasingly prefer advanced formulations such as conditioning masks, deep repair treatments, leave-in conditioners, serums, and styling creams that deliver visible results while remaining gentle on hair and skin. Esterquats are widely used in these products due to their lightweight texture, non-greasy feel, strong conditioning performance, and excellent compatibility with modern formulations. These benefits allow brands to position products at premium price points while meeting performance expectations.

Younger consumers, in particular, are drawn to products that combine hydration, protection, and styling benefits in a single solution. In addition, shampoo formulations are evolving from basic cleansing products toward nourishing and moisturizing variants, further increasing the use of conditioning ingredients. This trend is significantly expanding esterquat usage across both rinse-off and leave-in personal care applications.

Restraints - High Production Costs and Complex Manufacturing Requirements

Despite strong demand, esterquat adoption is constrained by high production costs and technically complex manufacturing processes. The production of esterquats requires advanced chemical synthesis, including fatty acid esterification followed by quaternization reactions, which demand specialized equipment and skilled technical expertise. These requirements increase capital investment and limit participation from smaller manufacturers. Historically, tallow-based feedstocks have dominated the market due to their ideal carbon chain length and strong softening performance.

However, tallow supply is subject to volatility in livestock production and agricultural pricing, leading to rising raw material costs. This cost pressure affects overall product pricing and reduces affordability in price-sensitive markets, particularly in emerging economies. Additionally, limited feedstock flexibility restricts manufacturers’ ability to quickly adjust production during demand fluctuations. As a result, while esterquats offer strong performance and sustainability benefits, cost and manufacturing complexity remain key barriers to broader market penetration.

Regulatory Complexity and Evolving Environmental Standards Creating Compliance Uncertainty

The esterquats market also faces challenges related to increasingly complex and evolving regulatory frameworks. Global regulations governing chemical safety, biodegradability, and environmental impact continue to tighten, increasing compliance costs for manufacturers. In Europe, REACH regulations require extensive chemical registration, toxicological testing, and safety documentation for esterquats, extending product development timelines and raising operational expenses.

In addition, growing regulatory focus on identifying persistent, bioaccumulative, and toxic (PBT) substances creates uncertainty around the long-term acceptance of certain feedstocks and manufacturing routes. Companies may be required to reformulate products or redesign production processes to remain compliant with future standards. This uncertainty can delay investment decisions and increase financial risk for both manufacturers and end-use formulators. While regulations support sustainability goals, the pace of regulatory change adds complexity and compliance burden across the esterquats value chain.

Opportunities - Bio-based and Sustainable Feedstock Development Supporting Premium Market Positioning

Rising consumer preference for natural and environmentally responsible products is creating strong opportunities for bio-based esterquat development. Manufacturers are increasingly investing in sustainable alternatives to traditional tallow-based feedstocks to enhance brand credibility and premium positioning. Vegetable oil-based esterquats, particularly those derived from palm oil and palm kernel oil, offer performance levels comparable to tallow-based variants while supporting renewable sourcing claims. These bio-based options align well with eco-conscious consumer expectations and sustainability-focused marketing strategies.

Leading chemical companies are actively supporting this transition; for instance, BASF introduced a bio-based esterquat for fabric softener applications in 2021, highlighting industry commitment to greener solutions. Palm-based esterquats also demonstrate excellent biodegradability and conditioning efficiency, enabling their use in both fabric care and personal care products. Manufacturers offering certified sustainable sourcing and traceable raw materials can achieve competitive differentiation and capture higher-margin segments in premium household and personal care markets.

Regional Manufacturing Hub Expansion and Asia Pacific Market Growth Supporting Capacity Development

The rapid expansion of manufacturing infrastructure across Asia Pacific is creating significant growth opportunities for the esterquats market. Countries such as China, India, and several Southeast Asian nations are emerging as key production and consumption hubs due to strong industrial capabilities, expanding consumer markets, and improving supply chain networks. Asia Pacific currently dominates global esterquat production, supported by cost-effective manufacturing and readily available raw materials.

China is witnessing strong market growth with an estimated CAGR of 12.4%, driven by large-scale detergent and textile care production. India is also experiencing robust expansion at around 11.5% CAGR, supported by urbanization, rising disposable incomes, and increased awareness of premium household and personal care products. Strategic collaborations between global ingredient suppliers and regional manufacturers are accelerating technology transfer and formulation adoption. These partnerships are strengthening local capacity development while supporting long-term regional market expansion.

Category-wise Analysis

Product Type Insights

TEA-quats (Triethanolamine Ester Quaternary Ammonium Compounds) hold an estimated 43% market share in 2025, reflecting their strong commercial acceptance and proven performance across applications. Their chemical structure provides high cationic activity, resulting in excellent softening and conditioning efficiency in both fabric care and personal care products. TEA-quats are also recognized for their superior biodegradability and mildness, making them suitable for environmentally compliant formulations.

Well-established manufacturing processes and long-standing application history have built strong confidence among formulators and brand owners. These factors support widespread adoption across mass-market and premium product categories. The MDEA and other esterquat variants segment accounts for the remaining 57% market share, offering greater formulation flexibility. These alternatives allow manufacturers to tailor performance characteristics, improve feedstock compatibility, and meet varying regulatory requirements, supporting customized solutions across diverse end-use industries.

Form Insights

Liquid esterquats represent the dominant form segment due to their high compatibility with modern fabric softeners and personal care formulations. Their excellent water solubility enables uniform dispersion, accurate dosing, and consistent performance in liquid detergents, conditioners, and rinse-cycle applications. Liquid forms are particularly well-suited for concentrated fabric softeners and premium hair care products, where stability and ease of formulation are critical.

Their ability to deposit effectively on fabrics and hair surfaces enhances conditioning efficiency and consumer-perceived performance. Solid and paste esterquats account for approximately 25% of market share and are mainly used in specialized applications. These include dryer sheets and heat-activated fabric conditioning systems, where thermal energy helps release esterquat molecules during drying cycles. While smaller in volume, this segment remains important for specific regional and application-driven requirements.

Feedstock Insights

Tallow-based esterquats continue to dominate the market with approximately 68% share, supported by their optimal carbon chain length ranging from C12 to C22 fatty acids. This structure delivers superior softening and conditioning performance, particularly in fabric care applications. Despite growing sustainability concerns, tallow-based variants remain widely used due to consistent performance, established supply chains, and formulation familiarity.

However, vegetable oil-based esterquats are steadily gaining traction and currently account for around 32% of the market. Feedstocks such as palm oil and palm kernel oil offer comparable conditioning efficiency while enabling improved sustainability positioning. These alternatives support reduced environmental impact and align with corporate sustainability commitments. As brands increasingly promote eco-friendly and renewable sourcing claims, vegetable-based esterquats are expected to gain stronger adoption, especially in premium and environmentally conscious product categories.

Application Insights

Fabric care remains the largest application segment, accounting for approximately 50% of total esterquat demand. Esterquats are extensively used in liquid fabric softeners, dryer sheets, and concentrated conditioning products, where their superior softness, antistatic properties, and biodegradability deliver strong performance advantages over traditional surfactants. Their ability to enhance fabric feel while meeting environmental standards supports continued dominance in this segment.

Personal care represents the fastest-growing application area, with estimated growth of 14% CAGR. Rising demand for premium hair conditioners, treatment masks, shampoos, and specialty body care products is driving this expansion. Esterquats provide lightweight conditioning without greasy residue, making them ideal for modern personal care formulations. This dual demand across household and personal care applications ensures sustained long-term market growth.

Regional Insights

North America Esterquats Market Trends

North America remains a key market for esterquats, supported by mature fabric care and personal care industries and strong consumer preference for sustainable products. The region has largely transitioned away from DHTDMAC-based softeners toward esterquat-based formulations due to improved biodegradability and lower aquatic toxicity. Regulatory emphasis on environmental protection and chemical safety further supports this shift. In the United States, manufacturers increasingly focus on premium, concentrated, and plant-based fabric softeners to strengthen product differentiation.

The growing popularity of eco-labeled and high-performance household products continues to drive esterquat demand. In personal care, expanding categories such as conditioning treatments, hair masks, and styling products are boosting usage. Affluent consumer demographics and high awareness of ingredient safety support ongoing adoption, positioning North America as a stable and innovation-driven esterquats market.

Europe Esterquats Market Trends

Europe represents one of the most advanced and regulation-driven esterquats markets globally. Stringent environmental standards, particularly the EU Detergents Regulation (648/2004), strongly favor biodegradable surfactants, accelerating the replacement of legacy compounds. Countries such as Germany, the United Kingdom, France, and Spain maintain highly developed fabric care and personal care industries with strong focus on sustainability and premium product design. European consumers actively prioritize environmentally responsible products, encouraging manufacturers to invest in green formulation technologies.

Northern European countries play a leading role in environmental research and innovation, supporting continuous improvement in esterquat performance and sustainability credentials. Harmonized regulations across EU member states also simplify regional distribution and supply chain integration. These factors collectively support consistent esterquat demand and reinforce Europe’s position as a key market for sustainable surfactant solutions.

Asia Pacific Esterquats Market Trends

Asia Pacific is the largest and fastest-growing regional market for esterquats, supported by strong manufacturing expansion and rapidly rising consumer demand. The region benefits from large-scale production facilities, competitive manufacturing costs, and growing household and personal care industries. China leads the market with approximately 12.4% CAGR growth, driven by extensive detergent manufacturing, textile care operations, and increasing use of advanced surfactants.

India is also emerging as a high-growth market with around 11.5% CAGR, supported by urbanization, rising disposable incomes, and increasing awareness of premium care products. Strategic collaborations between global ingredient suppliers and regional manufacturers are accelerating esterquat adoption. The expansion of e-commerce and direct-to-consumer platforms is further improving product accessibility, enabling faster market penetration beyond traditional retail channels across Asia Pacific.

Competitive Landscape

The global esterquats market shows moderate consolidation, with a mix of multinational leaders and strong regional manufacturers. Tier 1 companies such as BASF SE, Evonik Industries, Stepan Company, and Kao Corporation collectively account for approximately 50-60% of global market share. Their leadership is supported by advanced manufacturing capabilities, broad product portfolios, and continuous investment in research and development. Tier 2 and regional players, including Akzo Nobel, Clariant, Italmatch Chemicals, and several Asia Pacific manufacturers, contribute around 25-30% market share.

These companies focus on regional strength, customized solutions, and cost-competitive production. Competitive differentiation increasingly centers on sustainability credentials, bio-based feedstocks, regulatory compliance, and performance documentation. Ongoing investment in renewable raw materials and next-generation formulations is shaping long-term competition and supporting the market’s transition toward environmentally responsible growth.

Key Developments:

- In November 2024: Evonik Industries AG launched an advanced bio-based esterquat platform using plant-derived feedstocks with improved biodegradability. The innovation supports premium hair care formulations, helping brands meet rising consumer demand for natural, sustainable, and high-performance conditioning ingredients.

- In August 2024: Stepan Company expanded its esterquat manufacturing facilities in the Asia Pacific region to support rapidly increasing demand from personal care and household care manufacturers. The expansion strengthens regional supply chains and enables faster adoption of advanced conditioning technologies.

- In May 2024: Kao Corporation introduced a high-performance, vegetable oil-based esterquat formulation offering conditioning results comparable to tallow-based products. This innovation enables manufacturers to adopt renewable feedstocks while maintaining product performance and strengthening sustainability-focused brand positioning.

Companies Covered in Esterquats Market

- BASF SE

- Evonik Industries AG

- Stepan Company

- Kao Corporation

- Akzo Nobel N.V.

- Clariant AG

- Italmatch Chemicals S.p.A.

- ABITEC Corporation

- Hangzhou FandaChem Co. Ltd.

- Dongnam Chemical Industries Co. Ltd.

- Langh Tech Oy Ab

- Seppic

- Innospec Inc.

- Floerger GmbH

Frequently Asked Questions

The global esterquats market is expected to reach US$ 14.3 billion by 2033, growing at 10.5% CAGR driven by sustainability-focused fabric and personal care demand.

Market growth is driven by sustainable fabric care adoption, rapid expansion of premium hair and personal care products, and strong Asia Pacific manufacturing growth.

TEA-quats lead the market with around 43% share, supported by strong conditioning performance, biodegradability, and wide industry acceptance.

Asia Pacific leads the global esterquats market due to high production capacity and strong growth in China and India.

Major opportunities include bio-based feedstock development and rapid manufacturing expansion across Asia Pacific markets.

The market is led by BASF, Evonik, Stepan, Kao Corporation, and Akzo Nobel, supported by strong sustainability-driven innovation.