- Pharmaceuticals

- Erectile Dysfunction Drugs Market

Erectile Dysfunction Drugs Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Erectile Dysfunction Drugs Market by Drug (Viagra, Cialis, Staxyn/Levitra, Stendra/Spedra, Others), Distribution Channel (Hospital Pharmacy, Retail Pharmacy, Online Pharmacies), and Regional Analysis, from 2026 - 2033

Erectile Dysfunction Drugs market Share and Trends Analysis

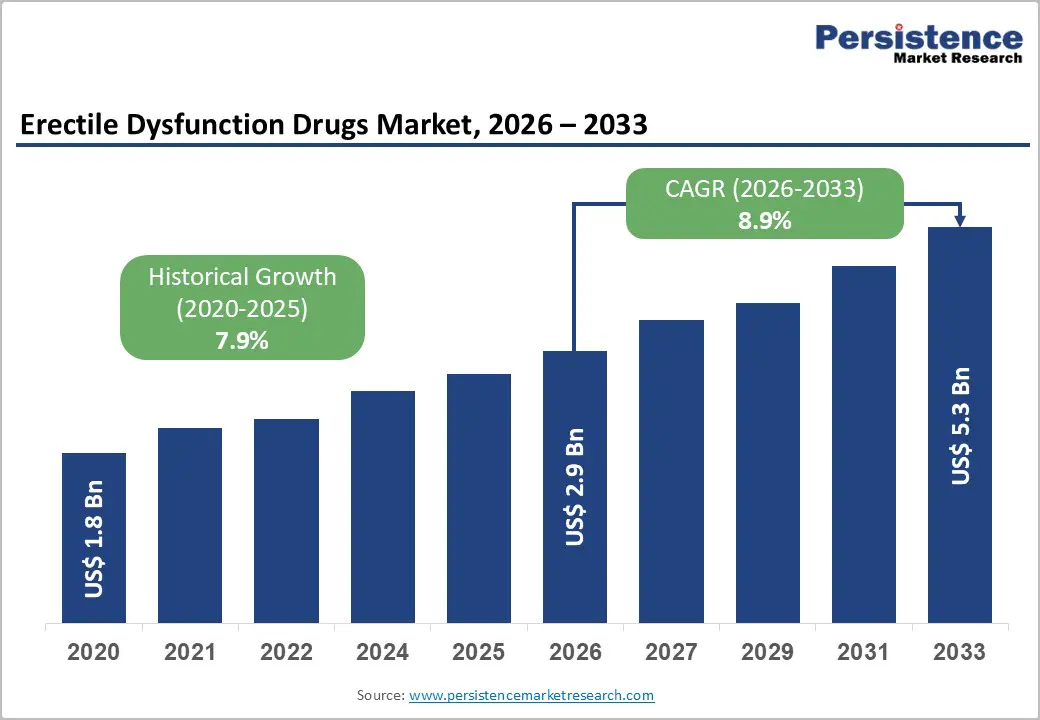

The global erectile dysfunction drugs market is estimated to grow from US$ 2.9 billion in 2026 to US$ 5.3 billion by 2033. The market is projected to record a CAGR of 8.9% during the forecast period from 2026 to 2033. Erectile dysfunction is a pathological state distinguished by the persistent incapacity to attain or sustain an erection that is adequate for engaging in sexual activity. ED is a prevalent condition that predominantly impacts males. It can be attributed to a multitude of factors, including, but not limited to, age, pre-existing health conditions (e.g., cardiovascular disease or diabetes), psychological influences, and lifestyle choices.

Pharmaceutical interventions such as sildenafil (Viagra), tadalafil (Cialis), and vardenafil (Levitra), which increase blood flow to the penile region, have significantly transformed the treatment of erectile dysfunction. These pharmaceuticals are classified as phosphodiesterase type 5 (PDE5) inhibitors, providing non-invasive and efficacious solutions for individuals experiencing difficulties with their sexual performance.

Key Industry Highlights:

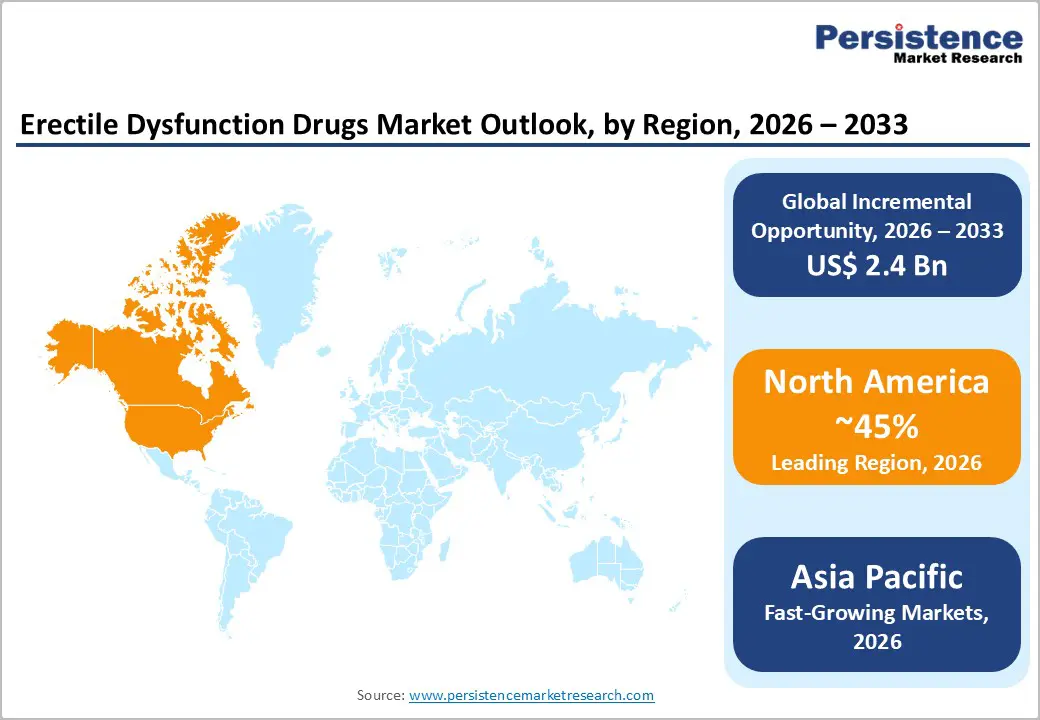

- Leading Region: North America leads the erectile dysfunction drugs market due to high disease awareness, strong brand presence, widespread telemedicine adoption, and favorable reimbursement coverage.

- Fastest Growing Region: Asia Pacific is the fastest growing region, driven by a rise in aging population, increasing lifestyle disorders, improving healthcare access, and growing treatment acceptance.

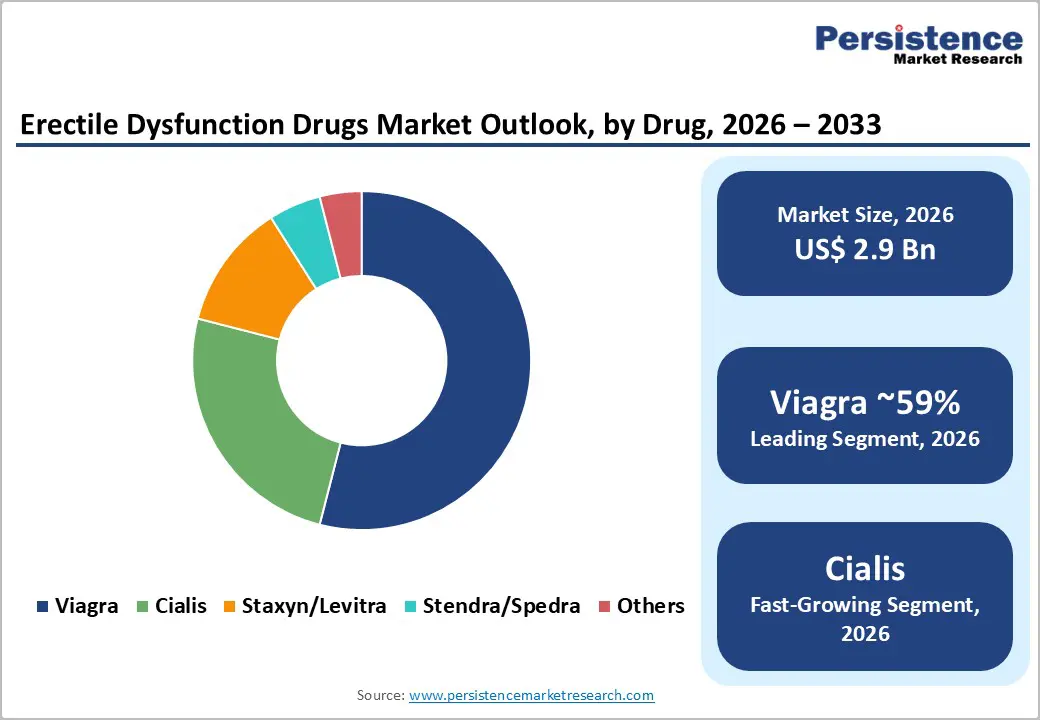

- Dominant Segment: Viagra leads the market due to strong brand recognition, early-mover advantage, extensive clinical use, and high physician and patient familiarity.

- Fastest Growing Segment: Online pharmacies are expanding rapidly, offering discreet access, virtual consultations, home delivery, and convenience, especially in North America, APAC and Europe.

| Key Insights | Details |

|---|---|

|

Erectile Dysfunction Drugs Market Size (2026E) |

US$ 2.9 Bn |

|

Market Value Forecast (2033F) |

US$ 5.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

8.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

7.9% |

Market Dynamics

Driver - Exponential Growth of the Elderly Demographic

The exponential growth of the elderly demographic serves as a critical catalyst for the worldwide ED drugs industry. The incidence of ED grows substantially in tandem with the demographic transition towards senior age groups that is occurring in societies across the globe. There are physiological changes that are intrinsic to the aging process; these include hormonal fluctuations, impaired neurological function, and deteriorating vascular health. All these factors contribute to the increased prevalence of erectile dysfunction. ED-associated risk factors include atherosclerosis, hypertension, and diabetes, all of which can develop with the aging process. The surge in demand for efficacious pharmaceutical interventions to tackle sexual health concerns associated with aging has catalyzed the expansion of the market for ED drugs.

The phenomenon of an aging population is notably conspicuous in developed nations, where progress in the medical field has prolonged the average lifespan. As an increasing percentage of the population advances to the geriatric stage, it is anticipated that the market for ED medications will continue to expand. Additionally, the increasing acceptance of sexual health discussions within society has prompted more people to seek medical attention for erectile dysfunction, thereby stimulating market demand. The adoption of ED medications is also influenced by the psychological effects of aging on sexual confidence and relationships, as more people become aware of the potential for enhanced quality of life that effective treatment can provide.

Restraints - Social Stigma Associated with Sexual Health Concerns

The worldwide market for erectile dysfunction medications is hindered by the social stigma associated with sexual health concerns. Although ED is prevalent, individuals are frequently dissuaded from seeking medical assistance or candidly discussing their condition due to social stigmas and embarrassment. Due in part to the societal perception of sexual dysfunction as a source of shame or personal failure, ED is underreported and undertreated. As a result, a considerable proportion of individuals afflicted with ED abstain from pharmaceutical interventions out of apprehension regarding criticism or a hesitancy to reveal their challenges. This stigma can impede market expansion by preventing education and awareness regarding available treatment options. It also affects individuals' propensity to seek advice from healthcare professionals, which may result in treatment being postponed or insufficient.

Rise in Prominence and Emergence of Alternative or Natural Remedies

An influential factor affecting the worldwide erectile dysfunction pharmaceutical industry is the rise in prominence and emergence of alternative or natural remedies. To address their ED concerns in a more holistic and non-pharmaceutical manner, a considerable number of individuals resort to alternative therapies, dietary supplements, and lifestyle modifications. This phenomenon presents a formidable obstacle for the pharmaceutical industry, as it redirects a fraction of prospective consumers from conventional ED medications.

The allure of natural remedies resides in their perceived safety, diminished adverse effects, and compatibility with an overarching societal transition towards wellness and organic lifestyles. Consumers may choose to supplement their diets, incorporate herbal remedies, or alter their way of life, frequently motivated by a desire for alternatives to prescription medications or apprehensions regarding the possible adverse effects linked to pharmaceutical substances.

Opportunity - Rising Adoption of Telemedicine and Online Healthcare Platforms

An opportunistic factor propelling the expansion of the worldwide erectile dysfunction drugs market is the rising adoption of telemedicine and online healthcare platforms. The accessibility of medical services has been fundamentally transformed by the digital transformation of healthcare, presenting a distinctive opportunity for the ED pharmaceuticals market to broaden its scope. Telemedicine platforms provide individuals with a discreet and convenient means of consulting healthcare personnel regarding sexual health issues, such as ED. By eliminating the stigma associated with visiting a physical clinic, this virtual approach promotes greater accessibility to assistance and facilitates frank discussions regarding medical conditions.

The proliferation of telemedicine also enables the delivery of emergency department medications to patients' residences and streamlines prescription procedures. By partnering with healthcare providers, online pharmacies have the potential to improve the accessibility of ED medications, especially for those who encounter difficulties or unease when attempting to acquire prescriptions via conventional means. The growing utilization of telemedicine services for emergency department management can be attributed to the tech-savvy generation's preference for the convenience and speed of online consultations and medication delivery. By incorporating technology into healthcare at this opportune moment, not only are the practical aspects of emergency department (ED) treatment addressed, but also evolving consumer demands for personalized and on-demand healthcare solutions are met.

Category-wise Analysis

By Drug Insights

Viagra (sildenafil) continues to lead the erectile dysfunction drugs market, accounting for an estimated 54% share in 2025, despite the widespread availability of generics. Its dominance is supported by strong brand recall, early market entry, and extensive clinical use across diverse patient populations. Sildenafil is widely referenced as a first-line phosphodiesterase type-5 inhibitor in clinical practice, reinforcing physician and patient confidence. High familiarity has sustained large prescription volumes, including branded and generic formulations. In addition, strategic lifecycle management has expanded the molecule’s visibility beyond erectile dysfunction, notably through its use in pulmonary arterial hypertension under alternate branding. Targeted promotional strategies and long-standing safety data continue to differentiate sildenafil from competing molecules such as tadalafil, vardenafil, and avanafil. These factors collectively support sildenafil’s sustained leadership and reinforce its position as a benchmark therapy within the erectile dysfunction treatment landscape.

By Distribution Channel Insights

Retail pharmacies and community drugstores remain the dominant distribution channels for erectile dysfunction medications, driven by their extensive physical presence and direct patient interaction. Many patients receive ED prescriptions following consultations with primary care physicians or specialists and prefer filling them at local pharmacies due to convenience, trust, and immediate access. Pharmacists play an important role by providing counseling, facilitating generic substitution, and offering affordability programs that encourage long-term adherence. The availability of private consultation areas in pharmacies further helps reduce stigma and supports patient confidence. However, online pharmacies and telehealth-linked prescription services are gaining momentum, particularly in developed markets. These platforms offer discreet access, virtual consultations, and home delivery, appealing to younger and digitally engaged consumers. While retail pharmacies currently lead in volume, the rapid expansion of digital fulfillment channels is gradually reshaping the distribution landscape.

Region-wise Insights

North America Erectile Dysfunction Drugs Market Trends

It is projected that North America will hold the largest market share in the worldwide erectile dysfunction drugs industry. The prevalence of erectile dysfunction, the existence of a robust healthcare infrastructure, and the pervasive recognition and acceptance of ED as a treatable condition all contribute to this pre-eminence. The area is characterized by a substantial proportion of elderly inhabitants and a relatively high prevalence of lifestyle-related health complications, including diabetes and cardiovascular diseases. These factors contribute significantly to the high demand for ED medications.

Moreover, the pharmaceutical sector in North America is highly developed, with prominent companies actively participating in research and development to guarantee a consistent flow of groundbreaking treatments for erectile dysfunction. Additionally, the market is propelled by the cultural receptivity in North America towards discussing and pursuing treatment for sexual health concerns, which contributes to its dominant position in terms of market share.

Europe Erectile Dysfunction Drugs Market Trends

Europe represents a mature yet evolving erectile dysfunction drugs market, with significant demand across Germany, the U.K., France, Spain, and the Nordic countries. Aging population, high burden of cardiovascular and metabolic disease, and robust primary care networks contribute to a sizable, treated population. Many European health systems integrate ED management into broader chronic disease programs, recognizing its association with quality of life and cardiovascular risk, which supports sustained prescribing of PDE5 inhibitors through public and private reimbursement schemes.

Regulatory harmonization under the European Medicines Agency (EMA) has facilitated approval of multiple generic sildenafil and tadalafil formulations and more recently of innovative options such as topical MED3000-based products marketed as Eroxon in several countries. In markets like the U.K., reclassification of certain sildenafil strengths to pharmacy medicines has allowed sale without a traditional prescription, improving access while maintaining pharmacist oversight. These policy shifts, combined with high internet penetration and growing acceptance of online pharmacies, are reshaping distribution patterns and broadening patient access across the region.

Asia and Pacific Erectile Dysfunction Drugs Market Trends

The South Asia, and the Pacific region is anticipated to witness the most rapid expansion of the worldwide market for erectile dysfunction medications. Several factors contribute to this expansion, including a swiftly growing population, heightened public consciousness regarding sexual health, and advancements in healthcare infrastructure. An increased emphasis on healthcare and well-being accompanies the economic progress of these nations, resulting in a heightened awareness and concern regarding conditions such as erectile dysfunction.

Changing sociocultural norms and the region's sizable and heterogeneous population both contribute to the increasing demand for ED medications. Moreover, progress in telemedicine and online healthcare platforms is facilitating access to information and treatment for sexual health issues for individuals residing in South Asia, and the Pacific, thereby propelling the expansion of the market. South Asia and the Pacific is currently trending ahead of the global market in terms of growth rate, owing to two key factors: the region's comparatively untapped market potential and the rising propensity of individuals to address and treat ED.

Competitive Landscape

The global erectile dysfunction pharmaceutical market is characterized by the strong presence of established players that adopt multiple strategies to preserve and strengthen their competitive positions. Continuous investment in research and development remains a core focus, enabling companies to refine existing therapies and improve efficacy, safety, and patient compliance. Well-known brands have undergone formulation enhancements over time to address side effects and expand patient suitability. These improvements support lifecycle management strategies and help companies retain existing users while expanding into new patient segments and geographies.

Brand strength and strategic commercialization play a critical role in shaping the competitive landscape. Leading companies leverage high brand recall to build consumer trust and loyalty through consistent messaging around safety and clinical effectiveness. Extensive marketing efforts, including direct-to-consumer campaigns, contribute to increased awareness and reduced stigma associated with erectile dysfunction. In parallel, partnerships with telemedicine platforms, online pharmacies, and healthcare providers have become increasingly important. These collaborations enhance product accessibility, support digital prescribing, and align with the growing preference for discreet, technology-enabled healthcare solutions.

Key Industry Developments:

- In September 2025, Boots launched its own-brand Sildenafil Orodispersible Film 50 mg, developed with Swiss pharmaceutical company IBSA, designed to dissolve quickly on the tongue for erectile dysfunction treatment.

- In September 2024, Haleon announced the launch of Eroxon®, the first and only FDA-cleared over-the-counter gel for erectile dysfunction, available for preorder in the U.S. without a prescription.

- In May 2024, Petros Pharmaceuticals partnered with Lemonaid Health to offer all STENDRA strengths via telehealth, expanding nationwide access, boosting brand awareness, and supporting potential OTC transition.

- In January 2024, Hims & Hers partnered with Hartford HealthCare, enabling referrals to in-person care, expanding reach across 14 U.S. states and Washington, D.C., and supporting personalized treatments.

Companies Covered in Erectile Dysfunction Drugs Market

- Pfizer, Inc.

- Dong-A ST Co., Ltd.

- Eli Lilly and Company

- Bayer AG

- Vivus, Inc.

- Teva Pharmaceutical Industries Ltd.

- SK Chemicals

- Meda Pharmaceuticals, Inc.

- Futura Medical plc

- Hims & Hers Health, Inc.

- Petros Pharmaceuticals, Inc.

- Others

Frequently Asked Questions

The global erectile dysfunction drugs market is projected to be valued at US$ 2.9 Bn in 2026.

Rising aging male population, cardiovascular comorbidities, lifestyle disorders, growing awareness, improved diagnosis rates, and expanding treatment acceptance.

The global erectile dysfunction drugs market is expected to witness a CAGR of 8.9% between 2026 and 2033.

Growth of telemedicine platforms, online pharmacies, novel formulations, emerging economies, affordable generics, discreet delivery, and personalized therapy options.

North America is the leading region in the global erectile dysfunction drugs market.