- Metalworking & Fabrication

- Electropolishing Services Market

Electropolishing Services Market Size, Share, and Growth Forecast 2026 - 2033

Electropolishing Services Market by Product Type (Citric Acid, Nitric Acid, Sulfuric Acid, Hydrochloric Acid, Phosphoric Acid), Application (Medical and Pharmaceutical Industry, Aerospace and Defense, Others), and Regional Analysis for 2026 - 2033

Electropolishing Services Market Size and Trends Analysis

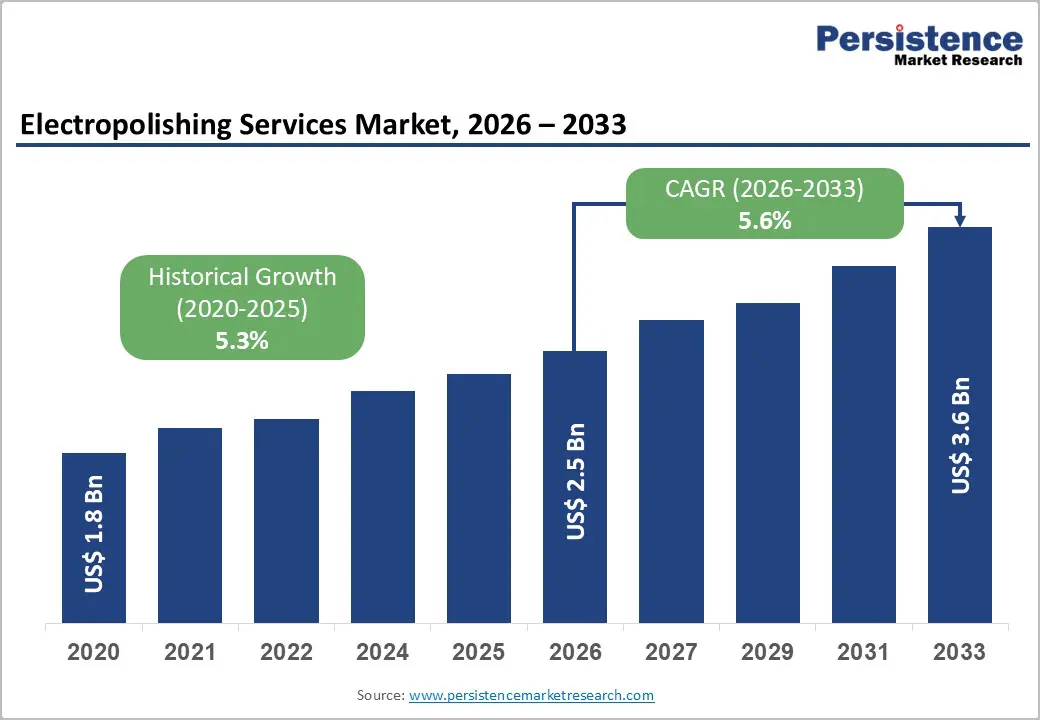

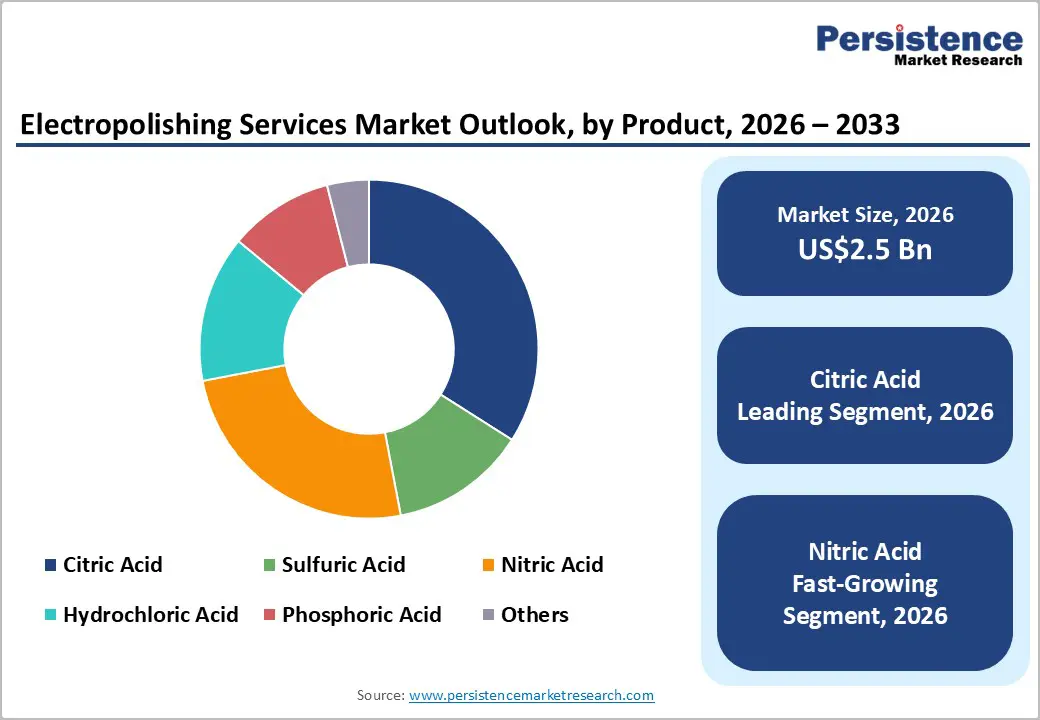

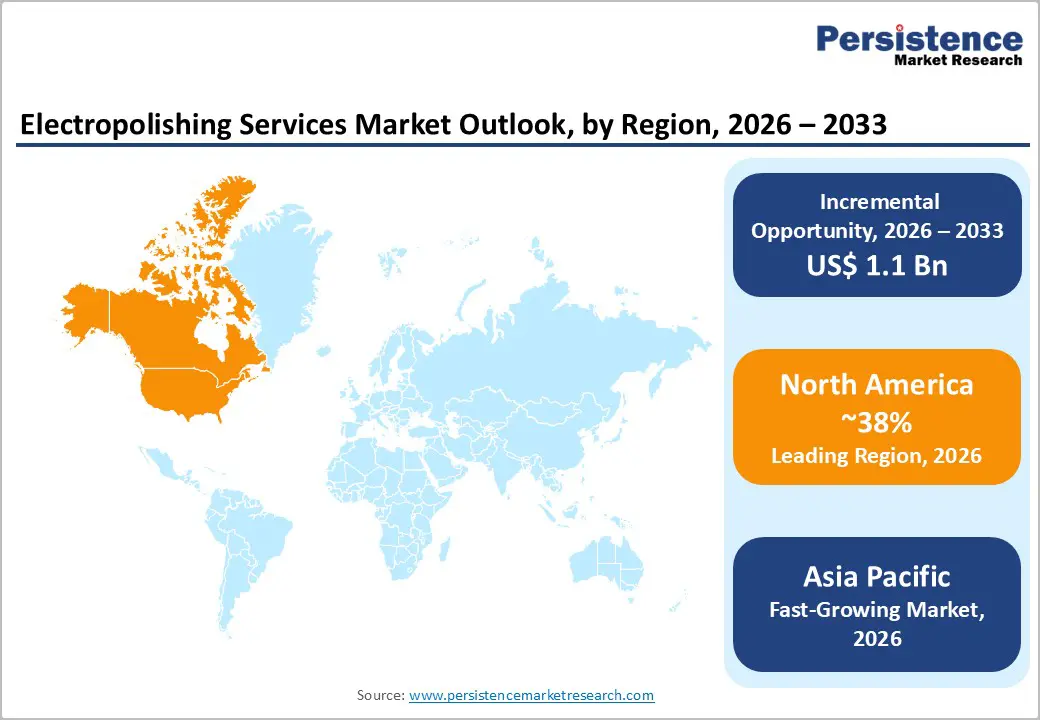

The global electropolishing services market size is likely to be valued at US$2.5 billion in 2026 and is expected to reach US$3.6 billion by 2033, growing at a CAGR of 5.6% during the forecast period from 2026 to 2033, driven by increasing demand across high-precision manufacturing sectors where surface quality, corrosion resistance, and cleanliness are critical.

Electropolishing is widely adopted in industries such as medical devices, pharmaceuticals, aerospace, food processing, semiconductors, and automotive, where it ensures sterile, smooth, and durable surfaces that meet stringent regulatory standards. The medical and pharmaceutical sectors represent a significant portion of service demand, reflecting the critical need for biocompatible and hygienic surfaces, while aerospace and defense industries rely on electropolishing to enhance component longevity, fatigue resistance, and overall performance. The rise of additive manufacturing, increased semiconductor production, and the shift toward lightweight and electric vehicles are additional factors driving market adoption.

Key Industry Highlights:

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 38% in 2026, driven by the U.S.’s dominance in medical devices, aerospace, and advanced manufacturing adoption.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by industrial expansion and rising demand in medical, semiconductor, and advanced manufacturing sectors.

- Leading Product Type: Citric acid is projected to represent the leading product type in 2026, accounting for 36% of the revenue share, driven by its environmental advantages and widespread use in medical and food applications.

- Leading Application: The medical and pharmaceutical industry is anticipated to be the leading application type, accounting for over 39% of the revenue share in 2026, supported by rising demand for sterile and high-precision components in medical devices.

| Key Insights | Details |

|---|---|

|

Electropolishing Services Market Size (2026E) |

US$2.5 Bn |

|

Market Value Forecast (2033F) |

US$3.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis- Rising Demand in the Medical and Pharmaceutical Sector

Stringent requirements for sterile and biocompatible surfaces. Electropolishing ensures smooth, contaminant-free finishes on medical devices such as surgical instruments, stents, and endoscopes, reducing the risk of infection and improving patient safety. As healthcare infrastructure expands and medical device adoption rises, manufacturers increasingly rely on electropolishing to meet regulatory standards. The process also enhances corrosion resistance and extends the service life of equipment, ensuring compliance with FDA and EU hygiene regulations. This growing demand reinforces the sector’s critical influence on market growth.

Advancements in medical technologies, including minimally invasive devices and implantable components, have heightened the need for precision surface finishing. Electropolishing provides uniform passivation, improving device performance and reliability in sensitive applications. The rise of pharmaceutical exports and international healthcare standards drives manufacturers to adopt high-quality electropolishing services. The trend toward disposable medical tools and equipment emphasizes hygiene and surface smoothness, enhancing service demand.

Expansion of Aerospace and Defense Manufacturing

Aircraft and spacecraft components, often made from titanium and stainless steel, require superior surface finishes to withstand extreme environmental conditions. Electropolishing improves fatigue resistance and reduces surface defects, critical for safety and performance. Post-pandemic recovery in commercial aviation and rising defense budgets have accelerated manufacturing activities, increasing electropolishing service requirements. Stringent international standards and certifications in aerospace demand precise surface finishing, positioning electropolishing as an essential service.

Emerging aerospace technologies, including electric and hybrid aircraft, unmanned aerial vehicles, and space exploration vehicles, contribute to electropolishing adoption. Components such as turbine blades, structural frameworks, and landing gears benefit from enhanced corrosion resistance and smooth finishes. Defense programs in multiple countries emphasize durability and operational efficiency, increasing the volume of high-precision metal parts requiring polishing. Partnerships between aerospace manufacturers and electropolishing service providers facilitate the integration of advanced process controls and automated finishing techniques.

Barrier Analysis - Rapid Technological Obsolescence

As new surface finishing techniques, such as laser polishing, plasma treatments, and additive manufacturing post-processing, gain traction, traditional electropolishing processes may face obsolescence. Companies must continuously invest in upgraded equipment, automation, and chemical formulations to remain competitive. Failure to adopt emerging technologies can lead to loss of market share, especially in high-precision sectors such as aerospace and medical devices. Rapid innovation cycles require skilled labor and continuous training, adding to operational challenges and potentially slowing adoption among smaller service providers who cannot afford frequent technology upgrades.

The fast pace of technological change also pressures service providers to maintain compatibility with new materials and complex component designs. Additive manufacturing introduces irregular geometries that may be difficult to electropolish without specialized setups. This accelerates the risk of outdated infrastructure and reduces profitability for firms not investing in modernization. Clients may demand faster turnaround times and higher precision, requiring continuous process innovation. Smaller regional players may struggle to meet these evolving expectations, leading to market consolidation.

Supply Chain Constraints for Electrolytes

Critical chemicals such as citric, nitric, sulfuric, hydrochloric, and phosphoric acids require consistent quality and availability to maintain process efficiency and finish quality. Disruptions, regulatory restrictions, or raw material shortages can delay production schedules for electropolishing service providers. Transportation and storage requirements for hazardous chemicals increase operational complexity. Industries such as medical devices, aerospace, and semiconductor manufacturing depend on timely service delivery, making supply chain reliability crucial.

Fluctuations in chemical prices or import restrictions in key producing countries exacerbate supply chain challenges, particularly for high-purity acids needed for sensitive applications. Service providers may face difficulty in scaling operations or meeting urgent orders when electrolyte supply is constrained. Environmental regulations on chemical handling and disposal increase logistical hurdles, affecting small and medium providers disproportionately. Companies must develop strategic procurement practices, including multiple sourcing, inventory buffers, and local partnerships, to mitigate these risks.

Opportunity Analysis - Emergence of Sustainable and Green Electropolishing Solutions

Traditional electropolishing processes often involve hazardous chemicals and generate waste, prompting manufacturers to adopt eco-friendly alternatives. Citric acid-based formulations and low-impact electrolytes reduce environmental risks while maintaining surface quality, aligning with sustainability standards. Regulatory bodies in North America, Europe, and Asia increasingly encourage greener manufacturing processes, creating incentives for companies to implement environmentally responsible electropolishing methods.

Investment in research and development of green electropolishing technologies allows providers to offer safer, compliant, and more cost-effective solutions. Energy-efficient and recyclable electrolyte systems reduce operational costs and waste disposal burdens. Industries such as food processing, pharmaceuticals, and medical devices, which prioritize hygiene and environmental compliance, are early adopters of sustainable methods. Market differentiation through eco-friendly services enhances competitive advantage, particularly in regions with stringent environmental regulations.

Sustainability and Low-Emission Technology Adoption

Precision surface finishing is critical for semiconductor wafers, electronic components, and high-performance metal casings, ensuring smooth surfaces, corrosion resistance, and reliable functionality. Rising demand for consumer electronics, data centers, and advanced chips drives production expansion in regions such as China, Japan, South Korea, and India. As device miniaturization and complex geometries increase, electropolishing becomes essential for achieving uniform finishes on intricate parts. Semiconductor fabs and electronics manufacturers rely on specialized electropolishing services to maintain high quality and meet stringent process standards, presenting a growing market segment.

Advancements in electronic devices, EV components, and 5G infrastructure elevate the demand for high-precision surface finishing. Electropolishing improves yield rates, reduces defects, and ensures performance reliability in sensitive electronic assemblies. Service providers can leverage this opportunity by offering tailored solutions for different materials such as stainless steel, copper, and aluminum. Strategic partnerships with semiconductor manufacturers and EMS providers enable consistent service delivery, scalability, and technical support. With semiconductor production projected to continue expanding, the electropolishing market benefits from increased volumes, recurring contracts, and technology-driven growth, positioning the sector as a key avenue for long-term market development.

Category-wise Analysis

Product Type Insights

Citric acid is expected to lead the electropolishing services market, accounting for approximately 36% of revenue in 2026, driven by its environmentally friendly profile and effectiveness across medical and food applications. For example, medical device manufacturers use citric acid to polish stainless steel surgical instruments, ensuring smooth, sterile surfaces that reduce contamination risks. Its compatibility with hygiene-focused industries makes it an ideal choice for equipment and processing surfaces in pharmaceutical plants, where maintaining sterility is critical.

Nitric acid is likely to represent the fastest-growing segment, supported by its strong oxidizing properties and ability to produce superior finishes for aerospace and automotive components. For example, aerospace manufacturers use nitric acid-based electropolishing to refine titanium turbine blades, reducing surface defects and enhancing fatigue resistance. Its application in EV battery casings also increases demand, as precise finishing improves corrosion resistance and conductivity. The growth is supported by rising defense and aerospace budgets, which drive the need for high-precision, durable components that meet stringent performance standards.

Application Insights

The medical and pharmaceutical industry is projected to lead the market, capturing around 39% of the revenue share in 2026, supported by the need for sterile and biocompatible surfaces. Electropolishing is critical for components such as surgical instruments, stents, and endoscopes, ensuring smooth finishes that prevent contamination and enhance device longevity. For example, stainless steel endoscopes undergo electropolishing with citric acid to maintain a polished, sterile surface, reducing bacterial adhesion. The segment benefits from the rapid expansion of healthcare infrastructure, stringent FDA and EU hygiene regulations, and growing medical device exports.

Aerospace and defense is likely to be the fastest-growing application, driven by initiatives focused on lightweighting, durability, and corrosion resistance. For example, titanium aircraft components, such as structural supports and engine parts, are electropolished to reduce surface roughness, improving fatigue resistance and extending service life. The growth is fueled by increasing commercial and defense aviation activity, including satellite launches and spacecraft manufacturing, as well as regulatory mandates from the Federal Aviation Administration (FAA) and the European Union Aviation Safety Agency (EASA) for corrosion prevention. The rise of private aerospace companies investing in advanced materials and lightweight components increases the need for high-quality electropolishing services.

Regional Insights

North America Electropolishing Services Market Trends

North America is anticipated to be the leading region, accounting for a market share of 38% in 2026, driven by rapid technological adoption and strong demand from regulated industries, particularly medical devices and aerospace. Service providers are increasingly investing in automation, digital process controls, and advanced chemical formulations to improve precision, reduce cycle times, and meet stringent quality standards. For example, Harrison Electropolishing L.P. has expanded its precision finishing capabilities to serve complex stainless steel and titanium medical components, reinforcing its leadership in high-value contracts.

Another key trend in North America’s electropolishing market is the growing integration of services into broader surface-engineering solutions, supported by strategic investments and industry partnerships. Aerospace and defense manufacturers are elevating electropolishing from a standalone finishing step to a core part of their supply chain quality assurance, especially for components where fatigue resistance and surface smoothness directly impact performance and safety. In the automotive segment, light-weighting initiatives and the rise of electric vehicles are creating new opportunities for electropolishing on aluminum and high-strength steel parts.

Europe Electropolishing Services Market Trends

Europe is likely to be a significant market for electropolishing services in 2026, due to a mature industrial base, stringent environmental and quality regulations, and strong demand from automotive, aerospace, and pharmaceutical sectors. European manufacturers increasingly adopt eco-friendly electropolishing techniques to comply with regulatory frameworks such as the EU’s REACH and Circular Economy Action Plan, pushing service providers toward sustainable chemical formulations and closed-loop waste management systems. For example, Poligrat GmbH, a European electropolishing specialist, has expanded its service offerings to include sustainable, nitric-acid-free processes tailored to EU environmental priorities.

The growing adoption of automation and digital quality control systems is significantly improving precision, consistency, and production efficiency. As advanced manufacturing initiatives expand across the region, electropolishing service providers are implementing real-time process monitoring, automated electrolyte bath management, and integrated quality assurance systems to ensure consistent and repeatable results, particularly for complex geometries and high-value components. These capabilities are especially critical in industries such as aerospace, semiconductor equipment, and luxury goods, where surface finish quality directly affects performance, reliability, and overall market competitiveness.

Asia Pacific Electropolishing Services Market Trends

The Asia Pacific region is likely to be the fastest-growing region in the electropolishing services market in 2026, driven by robust industrial growth and the rising demand for high-quality surface finishing across key sectors such as semiconductors, automotive, medical devices, and electronics. For example, Shenzhen Sinorise Technology Co., Ltd. has established itself as a reliable electropolishing service provider in China, offering precision surface finishing solutions that cater to complex metal parts used in electronics and industrial applications, reflecting the region’s growing capability and specialized offerings.

The increased adoption of technological innovations and tailored service offerings to meet the evolving requirements of complex metal components. Service providers are adopting advanced process control systems, automated bath monitoring, and digital quality assurance tools to deliver consistent, high-precision finishes, supporting sectors such as aerospace and medical equipment manufacturing. Local providers are also focusing on sustainable practices by improving electrolyte management and waste treatment processes to comply with tightening environmental regulations across the region.

Competitive Landscape

The global electropolishing services market exhibits a moderately fragmented structure, driven by a mix of established multinational providers and agile regional specialists that cater to diverse end-user industries such as medical devices, aerospace, automotive, and semiconductors. Players differentiate through technological investment, broad service portfolios, automation, and sustainability initiatives to meet stringent surface finish and regulatory standards.

With key leaders including SIFCO ASC, Able Electropolishing, KEPCO Inc., Harrison Electropolishing L.P., and Advanced Surface Technologies, the competitive environment balances incumbents with localized service providers that offer tailored solutions for high-precision applications. These players compete through continuous innovation in process technology, expanded capacity, value-added finishing services, and compliance with quality standards demanded by highly regulated industries.

Key Industry Developments:

- In August 2025, Able Electropolishing expanded its service capabilities by upgrading inspection systems with advanced digital microscopy and 3D surface profiling technology. The new equipment enables higher precision, improved surface analysis, and better quality control for complex components used in critical industries such as medical devices, aerospace, and semiconductor manufacturing. This enhancement supports stringent regulatory compliance, including FDA and ISO standards, and reinforces the company’s focus on traceability, corrosion resistance, and surface integrity.

- In February 2025, MD&M West 2025 took place in Anaheim, California, highlighting advancements in medical device manufacturing and electropolishing services. Able Electropolishing showcased its precision electropolishing and passivation solutions, designed to deliver ultra-clean, defect-free, and pathogen-resistant surfaces for surgical instruments and implants. These services enhance corrosion resistance, reliability, and compliance with stringent industry standards, including ISO 9001:2015 and ISO 13485:2016 certifications.

Companies Covered in Electropolishing Services Market

- Advanced Electropolishing Technologies

- AMF Technologies, Inc.

- Anopol

- Celco Inc.

- Delstar Metal Finishing, Inc.

- Harrison Electropolishing L.P

- Irving Polishing & Manufacturing, Inc.

- Kepco Inc

- Precision Electropolishing Services

- White Mountain Process

Frequently Asked Questions

The global electropolishing services market is projected to reach US$2.5 billion in 2026.

The electropolishing services market is driven by rising demand for high-precision, corrosion-resistant, and sterile surface finishes across medical, aerospace, automotive, and semiconductor industries.

The electropolishing services market is expected to grow at a CAGR of 5.6% from 2026 to 2033.

Key market opportunities lie in the growing adoption of sustainable electropolishing solutions and the expansion of high-precision applications in medical devices, aerospace, EV batteries, and semiconductor manufacturing.

Advanced Electropolishing Technologies, AMF Technologies, Inc., Anopol, Celco Inc, and Delstar Metal Finishing, Inc are the leading players.