- Electrical Equipment & Services

- Vibration Monitoring Systems Market

Vibration Monitoring Systems Market Size, Share, and Growth Forecast 2026 – 2033

Vibration Monitoring Systems Market by Product Type (Portable Devices, Non-portable Devices), Component (Proximity Probe, Accelerometer), End-use Industry (Power, Oil & Gas, Aerospace & Defense), and Regional Analysis, 2026 – 2033

Vibration Monitoring Systems Market Size and Trends Analysis

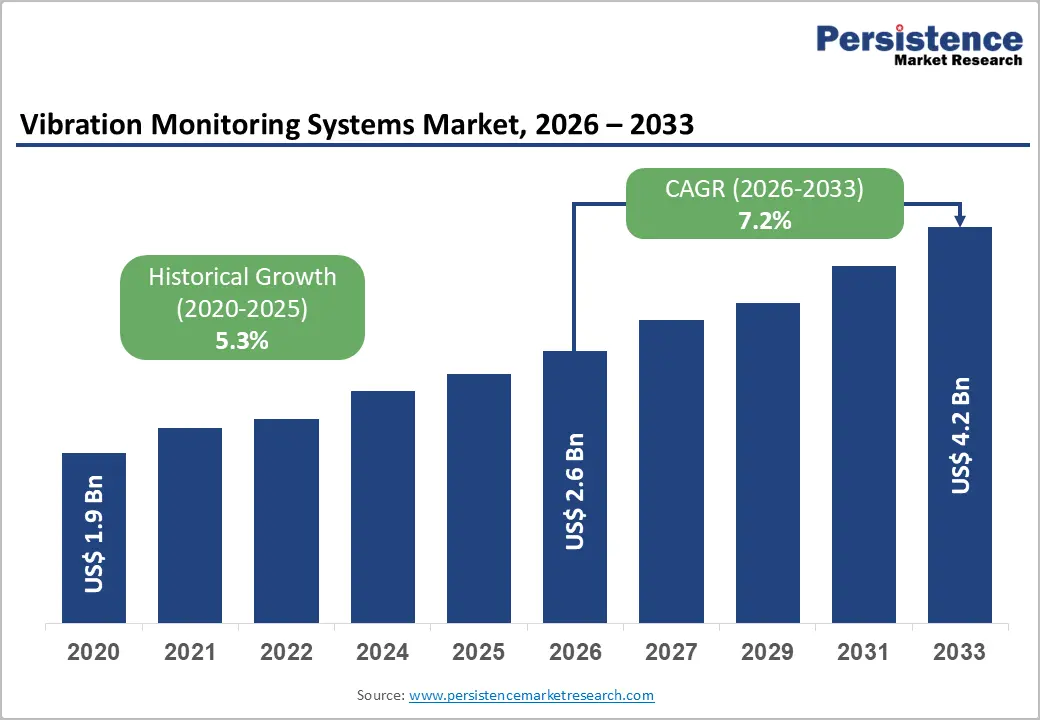

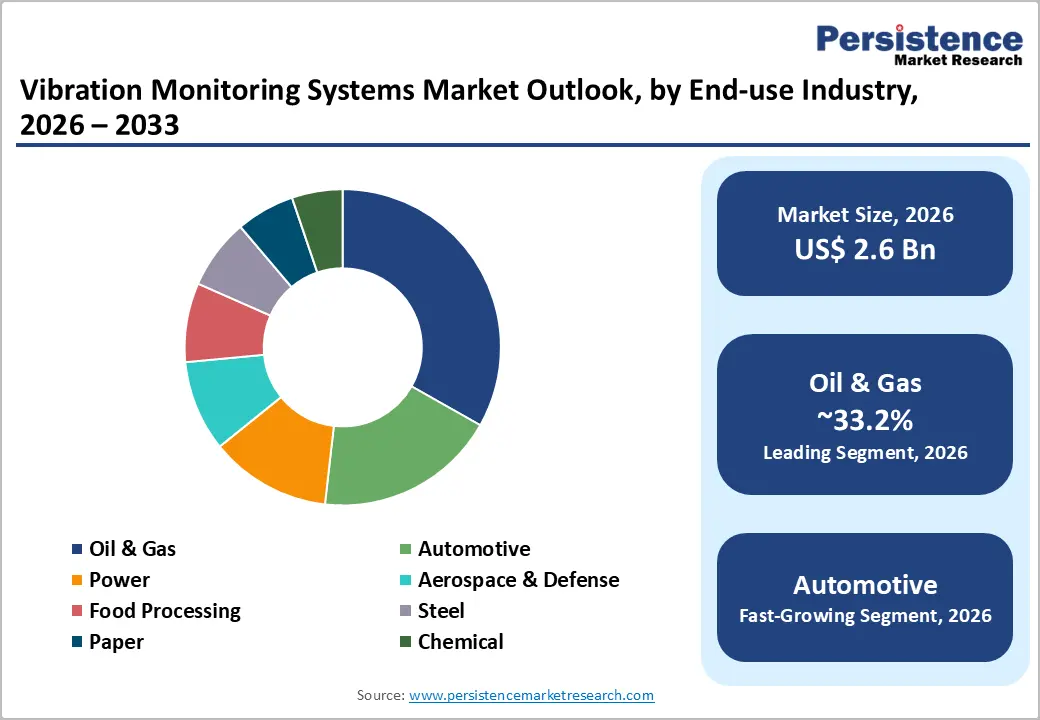

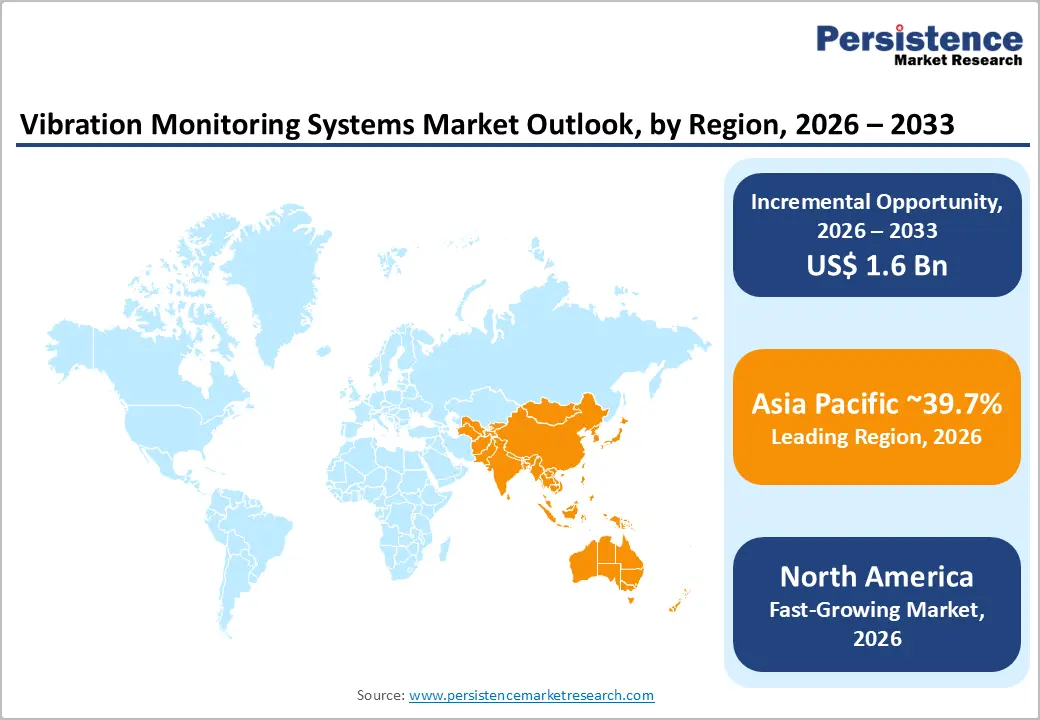

The global vibration monitoring systems market size is likely to be valued at US$2.6 billion in 2026 and is expected to reach US$4.2 billion by 2033, growing at a CAGR of 7.2% from 2026 to 2033, driven by the rising adoption of predictive maintenance across asset-intensive industries such as oil & gas, power generation, and mining, where avoiding unplanned downtime has become a strategic priority.

Key Industry Highlights

- Leading Product Type: Portable vibration monitoring devices, approximately 61.7% share in 2026, owing to their high flexibility in on-site inspections.

- Dominant End-use Industry: The oil and gas industry, nearly 33.2% in 2026, as operations involve high-value rotating equipment in remote environments.

- Exhibition Participation: In April 2026, TDK's Tronics Microsystems showcased its MEMS-based vibration and predictive maintenance solutions at Hannover Messe 2026. Tronics highlighted how its high-performance MEMS sensors are transforming Condition-Based Monitoring (CbM) and predictive maintenance at the landmark event in Germany.

- Leading Region: Asia Pacific, with about 39.7% share in 2026, owing to expanding manufacturing bases in China and India.

- Fast-growing Region: North America, backed by early adoption of advanced technologies such as AI-supported predictive maintenance.

DRO Analysis

Driver - Increasing Pressure to Cut Downtime and Optimize Maintenance Spend

Unplanned equipment failures have become one of the most expensive operational risks in the industry. A 2024 report by Oxford Economics estimated that downtime costs Global 2000 companies around US$400 billion annually, equivalent to nearly 9% of their profits. The 2024 CrowdStrike outage also reportedly caused an estimated US$5.4 billion in losses for Fortune 500 companies due to disruptions across airlines, healthcare systems, banks, and manufacturing operations.

Vibration monitoring directly addresses this by identifying developing faults, including bearing wear, misalignment, and looseness, long before they cause failure. According to the U.S. Department of Energy, predictive maintenance enabled by vibration monitoring can reduce equipment outages by 35 to 45% and equipment failures by 70 to 75% compared to fully reactive maintenance, alongside a 25 to 30% reduction in maintenance costs. This hard return on investment is pushing uptake across power generation, oil and gas, and heavy manufacturing, where the cost of downtime is simply too high to absorb.

Safety Mandates and Compliance Obligations in Hazard-Prone Industries

In industries where equipment failure can translate directly into environmental disasters or worker fatalities, compliance with safety standards is a non-negotiable driver of investment in vibration monitoring. Standards such as ISO 10816 and ISO 13373 establish internationally recognized thresholds and procedures for evaluating machine vibration in rotating equipment, giving regulators and plant operators a common framework for determining when machinery transitions from acceptable to dangerous states. In the oil and gas industry, for example, compliance with these regulations often requires the integration of unique monitoring technologies to track equipment performance accurately.

Organizations must invest in downhole vibration monitoring systems to meet these requirements. In 2025, with strict OSHA enforcement and rising legal liabilities, companies that fail to adapt to AI-supported risk assessment and real-time monitoring requirements face catastrophic fines, lawsuits, and operational shutdowns. This regulatory pressure is proving acute in GCC countries, where ongoing oil and gas projects are boosting the launch of predictive monitoring technologies.

Restraint - Skills Gap in Vibration Data Interpretation

One of the most persistent obstacles to the broad adoption of vibration monitoring is not the technology itself, but the shortage of individuals who can make sense of the data it generates. Effective vibration analysis demands expertise across multiple disciplines, which typically requires years of hands-on experience and formal certification under frameworks such as ISO 18436. Around 34% of industrial end-users cite a lack of trained personnel as a barrier to effective system utilization and maintenance. Also, more than 39% identify the volume and complexity of vibration data as a significant hurdle, mainly when it comes to transforming raw sensor data into actionable insights.

The problem is compounding as experienced technicians retire in large numbers. As these individuals exit the workforce, organizations face a knowledge gap. New technicians may be technically capable, but often lack the years of exposure required to confidently diagnose complex machinery issues. The shortage of qualified technicians can slow down the adoption of these services, especially in industries where swift technological changes outpace workforce training efforts.

Opportunity - On-Device Processing to Propel Intelligence Closer to the Machine

A key opportunity is emerging around edge-native vibration monitoring, where AI inference runs directly on the sensor node rather than being routed to a distant cloud platform. This architecture matters as vibration faults in rotating machinery can escalate in milliseconds. A manufacturing facility in Zhejiang Province, for instance, demonstrated this by deploying edge processors to analyze equipment vibration patterns, cutting machinery downtime by 37% through instant fault detection.

Research published in 2025 shows that lightweight embedded platforms combined with high-resolution Integrated Electronics Piezo-Electric (IEPE) sensors can now enable local data acquisition, processing, and classification of mechanical conditions. With the deployment of machine learning models directly at the edge, it has become possible to reduce latency and eliminate the requirement for cloud-based computation. This approach also benefits small operations and remote assets where bandwidth is limited, enabling high-precision condition monitoring without heavy infrastructure investment.

Wireless Connectivity Protocols to Provide Access to Previously Unmonitorable Assets

The widespread adoption of low-power wireless protocols such as Bluetooth Low Energy and LoRaWAN is fundamentally changing which assets can be practically monitored for vibration. Traditionally, continuous monitoring was limited to the most critical machines where the cost and complexity of wired installations were justified. Wireless systems remove that constraint. In 2025, LoRaWAN-enabled factories deploying real-time vibration and temperature monitoring of critical machinery have cut operational costs by 27% in automotive and energy sectors, with downtime reductions exceeding 30%.

Companies such as TE Connectivity have developed sensors that combine both Bluetooth Low Energy for short-range high-frequency readouts and LoRaWAN for long-range coverage in a single compact device. These hence support FFT bandwidths of up to 10 kHz, drastically outperforming standard MEMS-based alternatives. This dual-protocol approach lets reliability teams extend monitoring to previously neglected assets across sprawling plant floors or geographically dispersed sites, without redesigning network infrastructure.

Category-wise Analysis

Product Type Insights

Portable vibration monitoring devices are anticipated to dominate with approximately 61.7% of the market share in 2026. These devices appeal to a wide range of industries as they provide diagnostic capability without requiring permanent installation. Technicians can carry a single handheld analyzer across a facility, collecting vibration snapshots from dozens of machines along a pre-defined inspection route. This makes them a practical starting point for plants that are new to predictive maintenance, as they involve little upfront infrastructure cost.

Non-portable vibration monitoring devices are estimated to be the fastest-growing segment in the forecast period. These are permanently installed on critical assets and collect data continuously, making them essential where even short lapses in monitoring can result in catastrophic failures. Continuous data streams allow trending of spectral signatures and early identification of transient events that route-based measurements miss. Battery-powered wireless nodes are now sustaining three or more years of battery life, making them a cost-effective solution.

End-use Industry Insights

The oil and gas industry is predicted to dominate with nearly 33.2% of the share in 2026. The industry operates extremely critical rotating assets such as compressors, turbines, pumps, and offshore platforms. Hence, even a minor mechanical failure can lead to catastrophic safety incidents. Companies deploy permanently installed systems integrated with predictive maintenance platforms to ensure uninterrupted production and regulatory compliance. Studies show that integrating vibration, process, and lifetime-stress data cuts unplanned downtime on critical machines by double-digit percentages.

The automotive industry is expected to remain in the second position in 2026. The fast-growing adoption of Electric Vehicles (EVs) is creating a new and urgent demand. In an EV, there is no combustion engine noise to mask other sounds. Hence, high-frequency tonal noise from electric motors, inverter switching, and gear meshing becomes more audible to passengers. The surging popularity of EVs brings new Noise, Vibration, and Harshness (NVH) challenges, as the lack of internal combustion engine noise makes drivetrain noise more prominent. The key to managing NVH in EV powertrains is understanding the noise from electric motors, inverters, and gear systems. This has led to a surge in end-of-line vibration testing at EV manufacturing plants, where every vehicle must be checked before delivery.

Regional Insights

Asia Pacific Vibration Monitoring Systems Market Trends

In 2026, Asia Pacific is predicted to lead with a share of nearly 39.7%, as it hosts the world's largest and fastest-growing manufacturing base. China, Japan, India, and South Korea together account for an enormous installed base of rotating machinery in automotive, steel, chemicals, and energy. China and Japan both score above 63% on technology readiness indices, providing the infrastructure required for IIoT-enabled monitoring deployments. The market is also expected to grow steadily, backed by ongoing industrialization, increased demand for predictive maintenance, and the integration of AI and IoT.

Japan Vibration Monitoring Systems Market Trends

Japan’s market growth is driven by aging industrial infrastructure, increasing demand for precision manufacturing, and the government’s focus on Society 5.0 initiatives. Industries such as manufacturing, automotive, and energy are increasingly adopting predictive maintenance solutions, as real-time vibration monitoring helps enhance operational efficiency, minimize downtime, and extend equipment lifespan.

Japan's semiconductor and electronics industries are particularly sensitive. Even microscopic vibrations can cause defects in precision fabrication environments. The country’s 2025 semiconductor roadmap calls for the broad adoption of MEMS-based measurement devices in assembly lines. Japan also faces a demographic challenge. A large share of its experienced maintenance workforce is aging, pushing companies toward automated vibration monitoring to compensate.

China Vibration Monitoring Systems Market Trends

China’s growth is being augmented by top-down industrial policy and substantial investment. The Made in China 2025 initiative, which targeted intelligent manufacturing as a core pillar, was assessed as largely achieving its goals by 2024. China's AI+ Action initiative, launched in 2024, explicitly identifies AI+ Manufacturing as a key priority, aiming to harness large language models, machine vision, predictive maintenance systems, and intelligent control technologies to boost efficiency, quality, and resilience in industrial operations.

In August 2025, the State Council issued its ‘Opinions on Deepening the Implementation of the 'AI+' Initiative,’ extending these efforts. Shanghai's Implementation Plan for AI+Manufacturing, released in August 2025, set a target to integrate AI solutions across 3,000 manufacturing enterprises by 2027. China's 2024 policy blueprint called for the broad adoption of MEMS-based measurement devices in assembly lines, with subsidized smart-factory rollouts creating a fast-growing demand pocket in the market.

North America Vibration Monitoring Systems Market Trends

North America is a leader in smart factories and digital transformation. Modern plants connect motors, pumps, turbines, and conveyors to centralized cloud platforms where sensors continuously transmit vibrations, temperatures, and operational data. The region benefits from early adoption of IIoT technologies. The U.S. Department of Energy has reported that predictive maintenance, including vibration monitoring, can reduce industrial downtime by up to 45%. It is giving companies a clear financial incentive to invest. The presence of leading vendors such as Emerson, Honeywell, Rockwell Automation, and GE, who both develop and consume these solutions in the region, further strengthens market growth.

U.S. Vibration Monitoring Systems Market Trends

The U.S. is the single largest national market for vibration monitoring. Smart factories across the country are embedding vibration sensors and analytics in automated systems, with AI-backed monitoring and digital twin technology accelerating the digital transformation of industrial maintenance. Oil and gas remains the most prominent domestic end-user segment, with Permian Basin, Gulf of Mexico, and North Sea-linked operations all deploying permanent vibration surveillance on critical rotating equipment.

Europe Vibration Monitoring Systems Market Trends

Europe’s market benefits from a blend of mature industrial regulation and a superior shift toward renewable energy. Various countries in the region enforce strict workplace safety and equipment reliability requirements, which push industries to continuously monitor machine health rather than relying on periodic inspections. This helps companies comply with legal safety obligations and also reduces insurance risks and operational liability. The EU's regulatory framework demands that high-risk industrial operations maintain documented condition monitoring programs.

Germany Vibration Monitoring Systems Market Trends

Germany is Europe's most prominent industrial economy and the home of the Industry 4.0 concept, which originated from the country's own manufacturing modernization strategy. This creates an unusually strong alignment between national industrial policy and vibration monitoring adoption. Germany's automotive and manufacturing sectors are key consumers of industrial sensors, particularly those related to pressure, proximity, and motion detection.

U.K. Vibration Monitoring Systems Market Trends

Market growth in the U.K. is attributed to its offshore wind expansion. The country now hosts 46 fully commissioned offshore wind farms, 2,820 turbines, and 42 substations, with 11.4 GW of capacity now under construction. Each of these turbines requires continuous gearbox and drivetrain vibration monitoring to meet operational and insurance requirements. The government has also set a target of 50 GW of offshore wind capacity by 2030, supported by Contracts for Difference mechanisms.

Competitive Landscape

The global vibration monitoring systems market is moderately consolidated. Companies such as SKF, Emerson Electric, Honeywell, Baker Hughes, and Schaeffler collectively account for a notable portion of global revenues, especially in the oil and gas, power generation, mining, and heavy manufacturing sectors. Competition is no longer centered only on vibration sensors or analyzers. Vendors are now differentiating themselves through AI-based predictive maintenance software, wireless monitoring capabilities, cloud connectivity, and edge analytics.

Another key competitive shift is the rise of subscription-based ‘Monitoring-as-a-Service’ models. Instead of selling only hardware, vendors are delivering continuous remote diagnostics, cloud dashboards, and AI-generated maintenance alerts under long-term contracts. This trend is becoming specifically important in sectors such as mining, marine, and utilities, where operators prefer outsourced condition monitoring over maintaining large in-house reliability teams.

Key Industry Developments:

- In June 2025, Honeywell completed its $2.16 billion acquisition of Sundyne. Sundyne brought approximately 1,000 skilled employees and significant aftermarket revenue to Honeywell. The combined solution, unified under the Honeywell Forge platform, was positioned to provide an extensible, full-spectrum approach to predictive maintenance and asset reliability in the energy sector.

- In February 2025, Regal Rexnord Corporation launched the next generation of its Perceptiv Intelligent Reliability and Maintenance Solution. The updated platform introduced a new Universal Gateway and corresponding wireless vibration and temperature sensor, with the Universal Gateway providing wired and wireless connectivity to several current and future sensor types.

- In January 2025, GE Vernova improved its Remote Monitoring and Diagnostics (M&D) services for steam power plant assets. The service provides 24/7 support through automatic and expert-assisted analysis of operational data, enabling proactive maintenance interventions for steam turbines, generators, and boiler equipment.

Companies Covered in Vibration Monitoring Systems Market

- Emerson Electric Co.

- General Electric (GE)

- Bently Nevada

- Honeywell International Inc.

- SKF Group

- Rockwell Automation Inc.

- Siemens AG

- National Instruments Corporation

- Meggitt PLC

- Schaeffler Group

- Fluke Corporation

Frequently Asked Questions

The global vibration monitoring systems market is projected to be valued at US$2.6 billion in 2026.

The vibration monitoring systems market is expected to reach US$4.2 billion by 2033.

Key market trends include the shift toward wireless monitoring systems and the rise of subscription-based condition monitoring services.

The oil and gas segment is estimated to be the leading end-use industry with a share of about 33.2% in 2026, owing to strict safety and regulatory requirements.

The vibration monitoring systems market is expected to grow at a CAGR of 7.2% from 2026 to 2033.

Emerson Electric Co., General Electric (GE), Bently Nevada, Honeywell International Inc., and SKF Group are a few key market players.