- Industrial Machinery

- Dock Levelers Market

Dock Levelers Market Size, Share, and Growth Forecast 2026 - 2033

Dock Levelers Market by Product Type (Mechanical Dock Levelers, Hydraulic Dock Levelers, Air-Powered Dock Levelers, Telescopic Lip Dock Levelers, Vertical Dock Levelers, Others), Capacity, Leveling Type, Operation, Industry, and Regional Analysis, 2026 - 2033

Dock Levelers Market Size and Trend Analysis

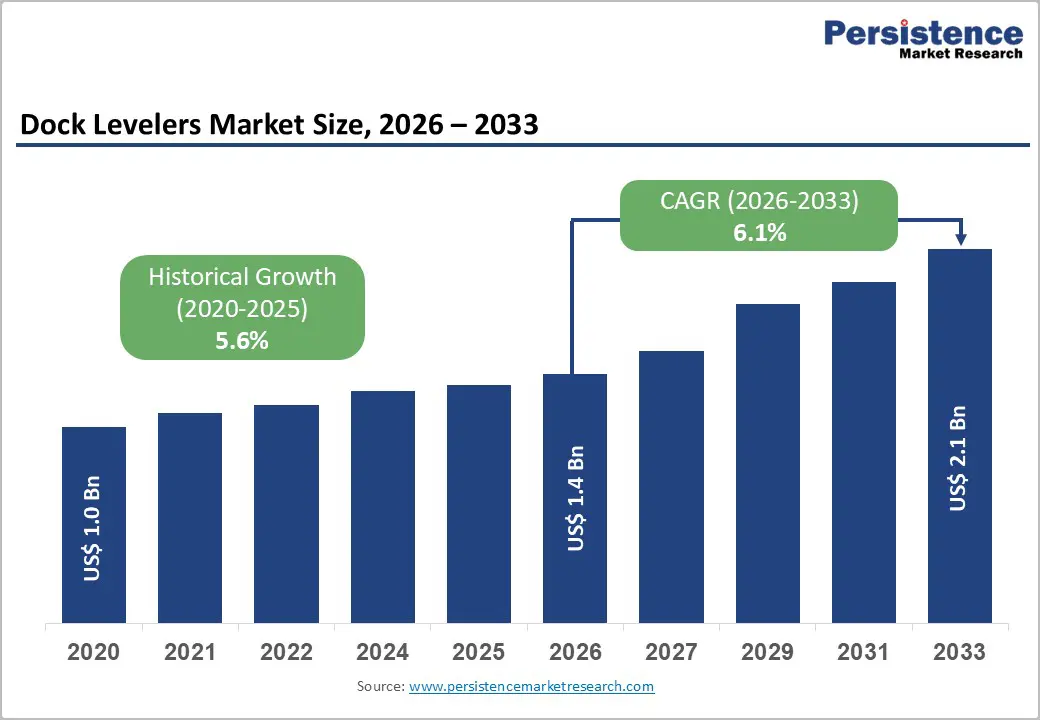

The global dock levelers market size is expected to be valued at US$ 1.4 billion in 2026 and projected to reach US$ 2.1 billion by 2033, growing at a CAGR of 6.1% between 2026 and 2033.

This growth is largely driven by the rapid expansion of e-commerce and the rising emphasis on logistics efficiency across warehouses and distribution centers. As order volumes increase, operators require reliable dock solutions to ensure smooth, fast, and safe truck-to-dock transitions.

Investments in new distribution facilities worldwide are driving demand for advanced material-handling equipment. Moreover, increasing automation in manufacturing and logistics facilities is accelerating dock leveler adoption to improve throughput, reduce labor dependency, and enhance operational safety.

Key Industry Highlights:

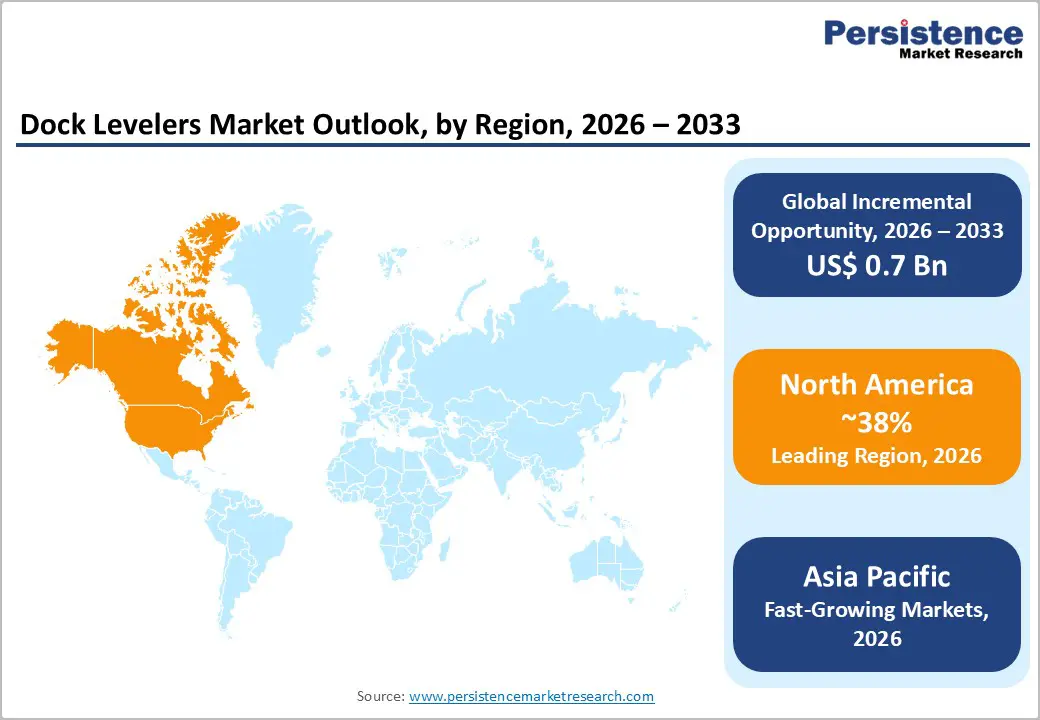

- Leading Region: North America leads the dock levelers market with a 38% share in 2025, supported by advanced logistics infrastructure and stringent OSHA safety regulations.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, driven by rapid manufacturing expansion and e-commerce growth across China and India.

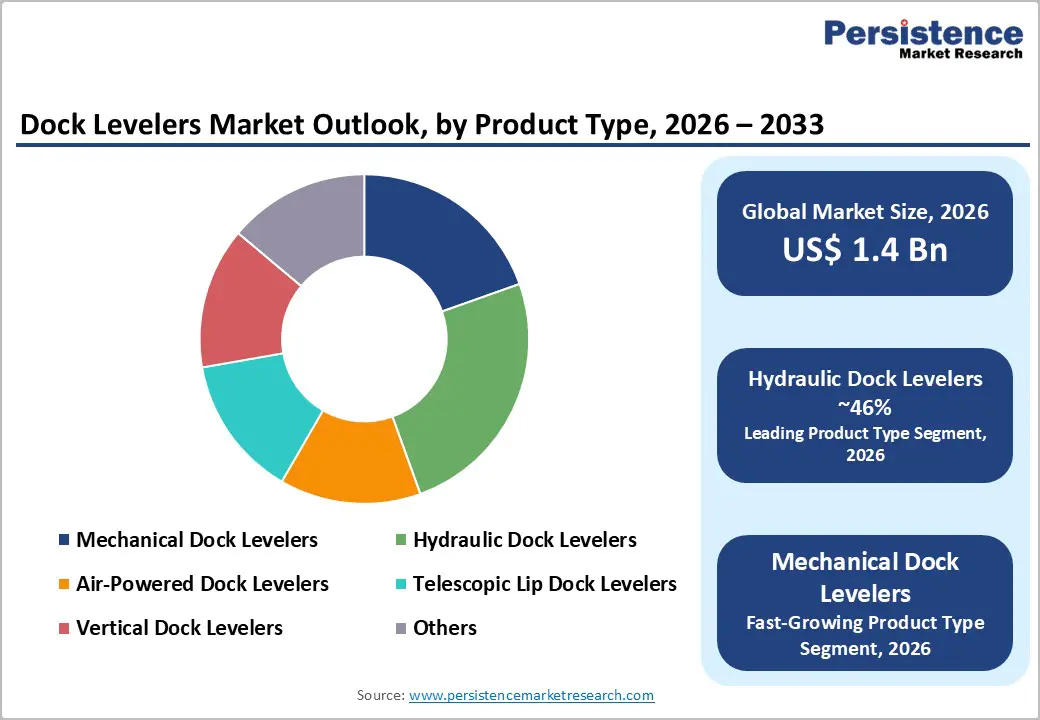

- Leading Product Category: Hydraulic dock levelers dominate the market with a 46% share in 2025, owing to their high load capacity, smooth operation, and reliability in high-throughput warehouses.

- Fastest-Growing Operation Category: Automatic and semi-automatic dock levelers are gaining traction as warehouses adopt automation to reduce labor dependency and improve operational efficiency.

- Key Opportunity Segment: Cold chain logistics presents a major opportunity, with rising demand for insulated and durable dock levelers to support expanding temperature-controlled storage and distribution networks.

| Key Insights | Details |

|---|---|

| Dock Levelers Size (2026E) | US$ 1.4 billion |

| Market Value Forecast (2033F) | US$ 2.1 billion |

| Projected Growth CAGR (2026 - 2033) | 6.1% |

| Historical Market Growth (2020 - 2025) | 5.6% |

Market Dynamics

Drivers - Rapid Expansion of E-commerce and Global Logistics Networks

The rapid growth of e-commerce has significantly increased the need for efficient loading and unloading solutions across warehouses and fulfillment centers. Rising online retail activity has driven substantial investments in new distribution centers worldwide, where dock levelers enable smooth height transitions between docks and trucks. These systems reduce loading times, support high shipment volumes, and help logistics operators meet fast delivery expectations.

As order fulfillment speeds become a competitive priority, dock levelers play a critical role in minimizing bottlenecks and operational delays. Their ability to improve turnaround times and reduce manual handling directly enhances productivity and cost efficiency. This makes dock levelers an essential infrastructure component for logistics providers managing high-throughput operations and increasingly complex supply chains.

Increasing Warehouse Automation and Strengthening Safety Regulations

Growing adoption of warehouse automation is accelerating demand for dock levelers that integrate seamlessly with forklifts, conveyors, and automated material handling systems. Automated docks improve workflow consistency, reduce reliance on manual labor, and enable greater operational scalability. This trend is especially important as the logistics and manufacturing sectors face labor shortages and rising expectations for efficiency.

In parallel, stricter workplace safety regulations are encouraging the use of advanced dock equipment. Regulatory bodies emphasize safe loading dock operations to reduce workplace accidents and equipment damage. Dock levelers equipped with safety features help reduce injury risk, minimize downtime, and ensure regulatory compliance, reinforcing their adoption across modern warehouses and industrial facilities.

Restraint - High Initial Investment Requirements and Ongoing Maintenance Complexity

High upfront investment remains a key restraint for the dock levelers market, particularly for small and mid-sized facilities. Advanced hydraulic and automated dock levelers involve significant capital expenditure, making adoption challenging for budget-constrained operators. Beyond installation costs, regular maintenance requirements increase total ownership costs, especially in high-traffic environments where component wear is frequent.

Maintenance challenges further limit adoption, as neglected inspections can lead to unexpected downtime and operational disruptions. Components such as springs, hydraulic systems, and safety mechanisms require periodic servicing to ensure reliable performance. These costs and maintenance burdens often delay retrofitting decisions, slowing penetration across older warehouses and smaller logistics facilities.

Complex and Stringent Regulatory Compliance Requirements

Strict regulatory frameworks governing dock safety and environmental standards create additional barriers to market growth. Compliance with occupational safety regulations requires certified installations, documentation, and periodic audits, which can extend project timelines and increase implementation costs. These requirements are particularly demanding for facilities upgrading existing infrastructure rather than installing new docks.

The risk of penalties for non-compliance further discourages rapid adoption, especially in regions with evolving or inconsistent regulations. Operators may delay investments due to uncertainty around regulatory interpretations and enforcement. In emerging markets, limited regulatory clarity and higher compliance complexity continue to restrain market expansion and modernization efforts.

Opportunity - Rising Adoption of Automation-Integrated and Smart Dock Levelers

Ongoing automation across warehouses and distribution centers presents strong growth opportunities for dock levelers designed to integrate with automated material handling systems. Levelers compatible with robotics, conveyors, and AI-driven platforms support faster, safer, and more consistent dock operations. Smart features such as sensors and condition monitoring enable predictive maintenance, helping operators reduce unexpected downtime and optimize asset utilization.

As fulfillment centers scale operations to handle higher order volumes, automation-ready dock levelers allow facilities to reduce labor dependency while improving throughput. These solutions are particularly attractive to large e-commerce operators seeking efficiency gains, creating opportunities for manufacturers to expand offerings in advanced and fully automated dock leveler segments.

Expansion of Cold Chain Logistics and Demand for Sustainable Solutions

Rapid growth in cold chain logistics is creating significant opportunities for specialized dock levelers designed for temperature-sensitive environments. Food and pharmaceutical supply chains increasingly rely on insulated and weather-resistant dock equipment to maintain product integrity during loading and unloading. This trend is driving demand for durable dock levelers that operate reliably in controlled environments.

At the same time, sustainability initiatives are influencing purchasing decisions across logistics and industrial sectors. Energy-efficient dock levelers, including air-powered and low-emission models, align with corporate sustainability goals. Manufacturers offering environmentally optimized solutions are well-positioned to capture demand from eco-conscious operators and regulated industries.

Category-wise Analysis

Product Type Insights

Hydraulic dock levelers dominate the product type segment, accounting for 46% market share in 2025, driven by their high lifting capacity, smooth operation, and reliability in high-throughput environments. These systems are widely used in large warehouses and distribution centers, where they efficiently handle heavy and variable loads while reducing manual handling and improving operational consistency.

Mechanical dock levelers are expected to witness faster growth as cost-conscious facilities seek reliable yet economical solutions. Their simple design, ease of installation, and lower maintenance requirements make them attractive for small and mid-sized warehouses, especially in emerging markets and retrofit projects where budget constraints influence equipment selection.

Capacity Insights

The 10 to 40 tons capacity segment leads with a 50% share in 2025, as it offers an optimal balance between load-handling capability and cost efficiency. This capacity range suits most logistics and manufacturing applications, accommodating standard freight loads and truck types commonly used across distribution networks.

Higher-capacity dock levelers are emerging as the fastest-growing segment, driven by increasing freight volumes and the use of heavier vehicles in industrial logistics. Growth is supported by the expansion of large-scale distribution hubs and manufacturing facilities, which require robust equipment to efficiently manage oversized and bulk shipments.

Leveling Type Insights

Top-of-dock (TOD) dock levelers hold a dominant 55% share in 2025, favored for their stable pit-style installation and seamless integration into newly constructed warehouses. Their design ensures smooth load transitions and reduced vibration, supporting safety compliance and high-frequency dock operations in busy distribution centers.

Edge-of-dock levelers are gaining traction as the fastest-growing leveling type due to their space-saving design and ease of installation. They are increasingly being adopted in retrofit projects and facilities with limited dock depth, offering a practical solution to upgrade existing loading infrastructure without major construction.

Operation Insights

Conventional dock levelers account for 57% share in 2025, driven by their simple operation, proven reliability, and minimal training requirements. These systems are widely preferred in environments with high workforce turnover, where ease of use and consistent performance help maintain uninterrupted loading operations.

Automatic and semi-automatic dock levelers are the fastest-growing segment of operations as facilities move toward automation and efficiency optimization. Their ability to reduce manual effort, enhance safety, and integrate with modern warehouse systems is driving adoption across advanced logistics and manufacturing operations.

Industry Insights

Warehousing and logistics lead the Industry segment, accounting for 45% market share in 2025, supported by rapid expansion of e-commerce and third-party logistics operations. High daily loading and unloading cycles in distribution centers require durable and reliable dock levelers to maintain fast turnaround times, operational efficiency, and worker safety across large-scale facilities.

Manufacturing is emerging as the fastest-growing end-use segment as factories modernize material-handling processes. Rising automation, just-in-time production models, and increased outbound logistics are driving demand for efficient dock solutions. Manufacturers are adopting advanced dock levelers to improve throughput, reduce manual handling, and support seamless integration with automated warehouse and production systems.

Regional Insights

North America Dock Levelers Market Trends

North America leads the global dock levelers market with a 38% share in 2025, supported by a well-established logistics and warehousing infrastructure, particularly in the United States. High adoption across distribution centers, retail fulfillment hubs, and manufacturing facilities drives consistent demand for advanced dock equipment with high durability and safety standards.

The region continues to benefit from strict occupational safety regulations that mandate secure dock operations. Innovation is another key strength, with increasing integration of automated and smart dock levelers into modern warehouses. Replacement demand and retrofitting of aging facilities further sustain market leadership across North America.

Europe Dock Levelers Market Trends

Europe represents a mature and stable dock levelers market, driven by strong industrial activity in countries such as Germany, the U.K., and France. Harmonized European Union regulations emphasize workplace safety and energy efficiency, encouraging the adoption of compliant and technologically advanced dock solutions across logistics and industrial facilities.

The market is projected to grow at a CAGR of around 6.5% during the forecast period, supported by gradual warehouse modernization and industrial upgrades. Retrofitting existing docks with energy-efficient and low-emission models remain a key growth avenue, particularly in Western and Southern European countries.

Asia Pacific Dock Levelers Market Trends

Asia Pacific holds a significant share of the market, accounting for approximately 36% in 2025, driven by rapid industrialization and expanding logistics networks. China’s large-scale manufacturing base and India’s fast-growing e-commerce sector are major contributors to regional demand for dock levelers across warehouses and industrial facilities.

The region continues to witness strong momentum from new warehouse construction and foreign investments in logistics infrastructure. Cost-effective manufacturing, rising automation adoption, and expansion of organized retail and cold chain facilities are accelerating dock leveler deployment across emerging Asian economies.

Competitive Landscape

The dock levelers market is moderately consolidated, with leading manufacturers collectively accounting for over a quarter of total revenue. Competitive positioning is largely driven by continuous innovation, particularly in automation-integrated dock levelers that enhance efficiency, safety, and throughput. Investments in research and development also focus on improving durability, energy efficiency, and compatibility with modern warehouse systems.

Despite the presence of strong global players, the market remains fragmented at the regional level, with numerous local manufacturers catering to cost-sensitive demand. Global strategies increasingly emphasize partnerships, technology collaborations, and modular product designs to address diverse customer needs while supporting upgrades in automated and sustainable dock infrastructure.

Key Developments:

- In November 2025, Rite-Hite launched a replacement dock leveler designed to minimize operational downtime, enabling faster installation without major construction or pit modification. The solution targets retrofit projects, helping warehouses maintain productivity while upgrading aging dock infrastructure efficiently.

- In 2024, Blue Giant enhanced its mechanical dock levelers with reinforced J-beam supports, improving compatibility with air-ride trailers. This development increases stability during loading operations, reduces trailer movement, and enhances safety and performance in high-cycle logistics and distribution environments.

Companies Covered in Dock Levelers Market

- ASSA ABLOY Group

- Rite-Hite Holding Corporation

- Blue Giant Equipment Corporation

- Pentalift Equipment Corporation

- Kelley (4Front Engineered Solutions)

- NORDOCK Inc.

- Stertil Dock Products

- Loading Systems International B.V.

- McGuire (Systems, LLC)

- Poweramp (Systems, LLC)

- Beacon Industries, Inc.

- Hörmann Group

- PROMStahl GmbH

- Armo S.p.A.

- Butzbach GmbH

Frequently Asked Questions

The global dock levelers market is projected to reach US$ 1.4 billion in 2026, supported by expanding logistics and warehousing infrastructure.

E-commerce expansion boosts demand, increasing warehouse efficiency needs by 30-40% in distribution centers.

North America leads with a 38% share in 2025, driven by mature logistics networks and stringent workplace safety regulations.

Integration of automation and smart technologies presents a major opportunity, as automated dock operations help reduce labor dependency and improve efficiency.

Key players include Essentra plc, Blue Giant, Rite-Hite, Nordock, and Hormann.