- Sporting Goods & Equipment

- Diving Regulator Market

Diving Regulator Market Size, Share, and Growth Forecast 2026 – 2033

Diving Regulator Market by Product Type (Balanced Regulators, Unbalanced Regulators, Diaphragm Regulators, Other), Application (Recreational Diving, Professional Diving, Technical Diving, Military & Rescue, Others), Distribution Channel (Specialty Stores, Brand Stores, Online), End User (Civilian/Individual, Commercial Operators, Government/Military), and Regional Analysis for 2026–2033

Diving Regulator Market Size and Trend Analysis

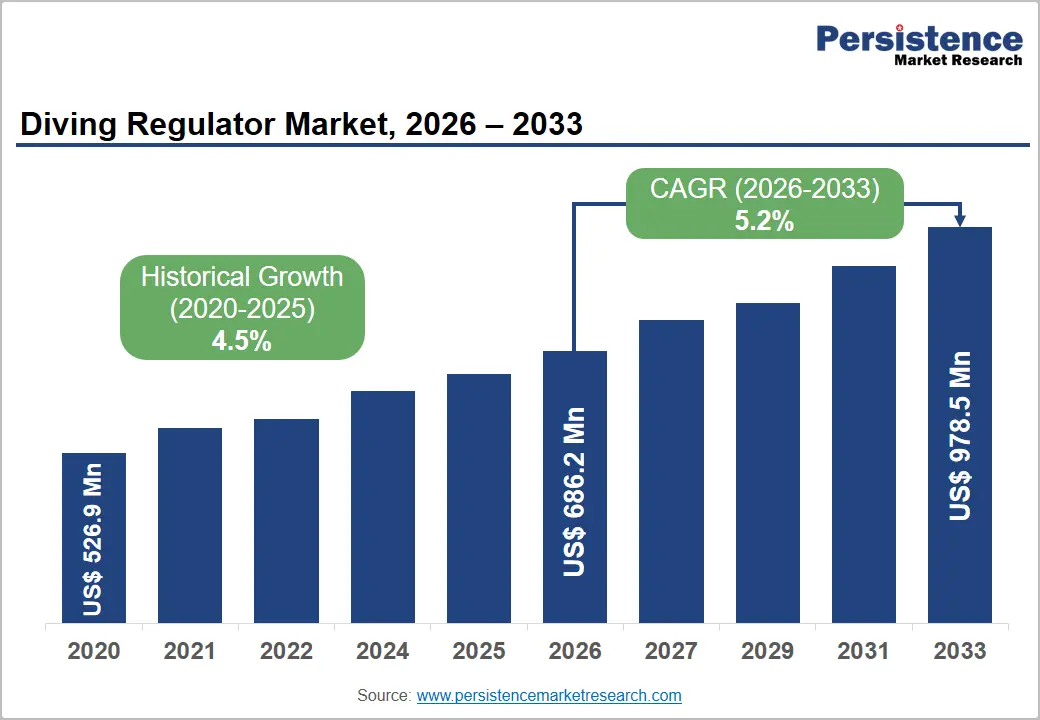

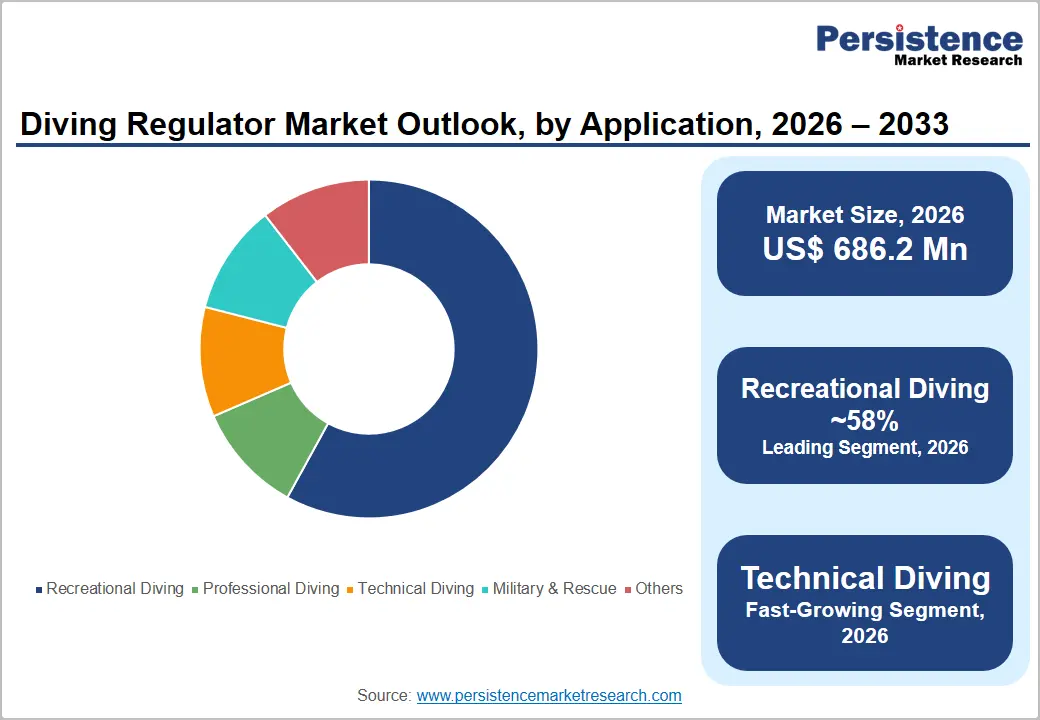

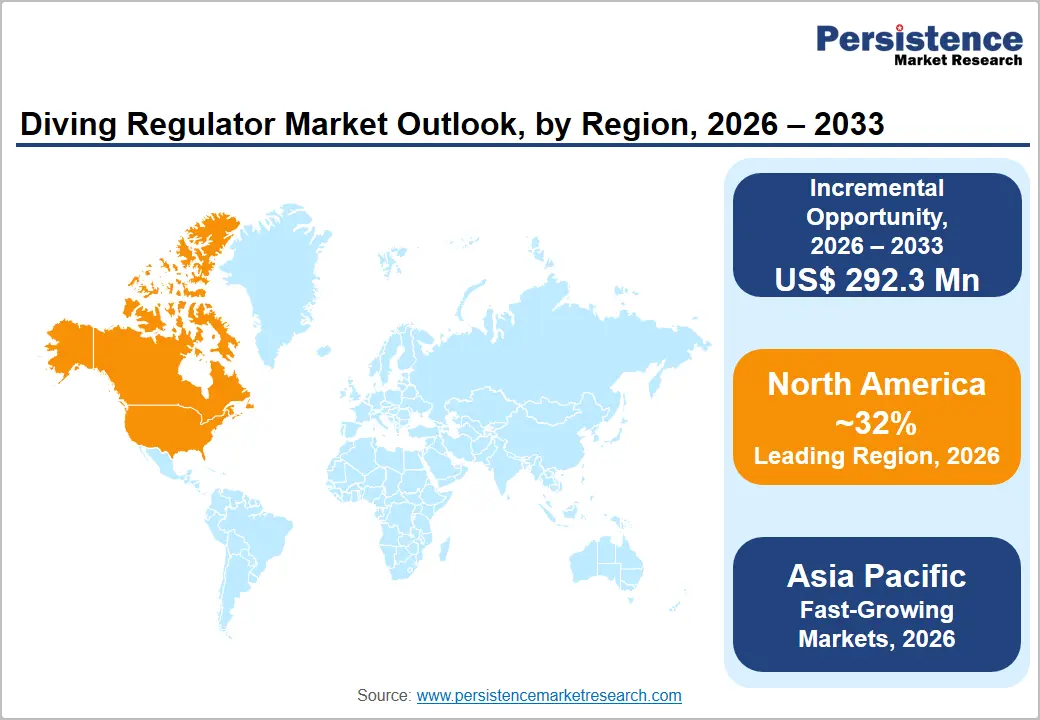

The global diving regulator market size is valued at US$ 686.2 million in 2026 and is projected to reach US$ 978.5 million, growing at a CAGR of 5.2% between 2026 and 2033. The growth in recreational and professional underwater activities is a key driver of market expansion, supported by a rising global base of certified divers and the rapid development of marine tourism in the Asia Pacific.

Additionally, the market benefits from ongoing product innovation, such as lightweight materials and environmentally sealed designs, which stimulate demand for upgrades across user segments. Participation rates among millennials and Generation Z adventure enthusiasts are increasing, bolstered by government initiatives to promote coastal and adventure tourism, particularly in emerging markets throughout Southeast Asia, the Middle East, and Latin America.

Key Industry Highlights:

- Leading Region: North America accounted for approximately 32% of the global diving regulator market share in 2026, supported by the largest active diver population, mature specialty retail infrastructure, and prominent regulator brand headquarters in the United States.

- Fastest Growing Region: Asia Pacific is the fastest-growing regional market, projected at a CAGR of 6.5%, propelled by booming marine tourism in Indonesia, Thailand, and the Philippines, rising disposable incomes, and government-backed dive tourism initiatives.

- Dominant Segment: Balanced Regulators lead the product type category with approximately 40% revenue share, favored by both recreational and professional divers for delivering consistent airflow across varying depths and tank pressure levels.

- Fast-Growing Segment: The online distribution channel is the fastest growing, driven by e-commerce adoption, expanding direct-to-consumer brand initiatives, and growing purchase confidence among experienced divers seeking competitive pricing and convenience.

- Key Opportunity: Innovation in eco-material and technologically integrated regulators, combining sustainable bioplastic and recycled-component designs with wireless digital connectivity, presents a high-value differentiation and premiumization opportunity for leading manufacturers.

DRO Analysis

Drivers - Rising Global Participation in Recreational Diving and Adventure Tourism

Recreational diving remains the dominant demand driver for the global diving regulator market. According to the Diving Equipment and Marketing Association (DEMA), there are approximately 2.5 million active scuba divers in the United States alone, with as many as 6 million active scuba divers worldwide. Simultaneously, global adventure tourism is expanding rapidly, with travelers increasingly seeking immersive underwater experiences at destinations such as Indonesia's Raja Ampat, Thailand's Similan Islands, and the Philippines' Tubbataha Reefs.

Every new certified diver represents a direct consumer of diving regulators, both for personal ownership and rental-fleet procurement by dive centers, making certification-volume trends a reliable leading indicator for market demand. Growing government investments in marine tourism infrastructure across Asia-Pacific and the Mediterranean further expand the accessible diver population.

Expanding Commercial and Professional Diving Sector

The professional and commercial diving sector is a structurally important demand segment for high-specification diving regulators. The global commercial diving services market was valued at approximately USD 1.44 billion in 2024 and is projected to grow at a CAGR of 5.7% through 2033, driven by expansion in offshore oil and gas maintenance, subsea cable installation, offshore wind-farm servicing, and underwater infrastructure inspection.

More than 3,500 offshore oil and gas platforms globally require routine underwater inspection at intervals of 6 to 12 months, generating over 18,000 scheduled diving assignments annually. The rapid growth of offshore renewable energy, with Europe alone operating or planning over 300 offshore wind farms, is creating sustained demand for specialized regulators built to withstand extreme depths and cold-water conditions. Military and rescue diving programmes further contribute to demand for high-durability, mission-critical regulator solutions.

Restraints - High Product Cost and Maintenance Burden for Entry-Level Consumers

Diving regulators are precision life-support instruments requiring stringent manufacturing standards and regular maintenance, resulting in relatively high price points that create a barrier to first-time purchaser adoption. Quality regulator systems typically range from USD 300 to USD 800 for recreational configurations, considerably for technical and professional-grade equipment. Beyond purchase price, annual servicing costs, mandated by manufacturers and safety standards such as EN 250, add to the total cost of ownership.

According to data from the Business of Diving Institute, nearly 55% of divers prefer budget gear, and 49% cite high cost barriers as a disincentive to personal ownership, instead relying on rental equipment from dive centers. This preference for rentals moderates direct consumer sales of premium regulators, particularly in price-sensitive emerging markets.

Declining Entry-Level Scuba Certification Volumes in Mature Markets

While global diver populations remain substantial, entry-level certification volumes in mature markets have trended downward. According to the Business of Diving Institute in collaboration with the Diving Equipment and Marketing Association (DEMA), open-water scuba certifications in the United States declined from 198,000 in 2001 to 128,000 in 2023, with a significant pandemic-related dip to 87,000 in 2020.

Furthermore, PADI's market share in North America fell from 55% in 2023 to 43% in 2024, accompanied by an overall contraction in market volume. A shrinking pool of new entrants in developed markets constrains baseline demand growth, placing greater reliance on emerging-market expansion and professional sector procurement to sustain overall market momentum.

Opportunities - Accelerating Demand from Asia-Pacific's Marine Tourism Boom

Asia Pacific presents the most compelling near-term growth opportunity for diving regulator manufacturers and distributors. The region accounted for approximately 26% of global diving regulator demand in 2024 and is projected to grow at a CAGR of 6.5%. Countries including Indonesia, Thailand, the Philippines, Malaysia, and Vietnam are investing heavily in marine tourism infrastructure, dive certification programmes, and sustainable underwater tourism practices.

Asian Governments are actively promoting dive tourism through dedicated campaigns, for instance, Tourism Malaysia's 'Dive Into The Unimaginable' programme, generating a consistent pipeline of first-time and returning certified divers who require reliable equipment.

Innovation in Sustainable and Technologically Advanced Regulator Designs

Growing environmental consciousness among divers and tightening sustainability benchmarks in manufacturing present a significant innovation-led opportunity. Apeks Marine Equipment, for example, launched the Ocea regulator, the industry's first model constructed from recycled components and bioplastics, manufactured in a solar-powered facility, demonstrating that eco-design and high performance are compatible. Material innovation, including titanium alloys, composite polymers, and Physical Vapour Deposition (PVD) coatings, is enabling regulators with superior corrosion resistance, reduced weight, and extended service life.

Digital integration, including air-integrated wireless transmitters compatible with dive computers, is driving premium replacement cycles. Manufacturers that position their portfolios at the intersection of sustainability and advanced performance stand to capture share from an increasingly discerning global diver demographic, particularly as regulatory standards such as EN 250 continue to evolve.

Category-wise Analysis

Product Type Insights

The balanced regulators segment holds the dominant share of the global diving regulator market by product type, commanding approximately 40% of total market revenue. Balanced regulators, available in both diaphragm and piston configurations, deliver consistent airflow irrespective of variations in tank pressure or ambient depth, making them the preferred choice across recreational, technical, and professional diving disciplines.

The European standard EN 250 certification, which defines performance benchmarks for cold-water breathing performance, has effectively positioned balanced diaphragm regulators as the de facto specification for professional and cold-water applications. Over-balanced variants, which boost medium-pressure delivery above ambient, are gaining traction among technical divers, further reinforcing the segment's dominance. Diaphragm and piston sub-types each serve distinct diving communities, ensuring broad market penetration within the category.

Application Insights

The recreational diving segment is the leading application, accounting for approximately 58% of total market share. The Diving Equipment and Marketing Association (DEMA) reports approximately 2.5 million active scuba divers in the United States alone, with an estimated 6 million active divers worldwide, a population almost entirely served by recreational-grade regulators. The growth of adventure tourism, expansion of dive certification programmes in emerging markets, and increasing accessibility of entry-level and mid-range regulator options have broadened the addressable recreational consumer base.

Dive resort rental fleets represent a significant and recurring B2B demand channel, as operators routinely replace and upgrade equipment to ensure safety compliance. The segment's size and consistent replacement demand create a reliable revenue floor for manufacturers, while the upsell trajectory from entry-level to premium balanced regulators sustains average selling price growth over time.

Distribution Channel Insights

The specialty stores channel retains the leading share of diving regulator distribution, accounting for approximately 38% of total sales. Specialty dive retailers offer product demonstrations, expert fitting, after-sales servicing, and access to manufacturer-authorized maintenance networks, services that are critical for a safety-critical product category in which consumers are reluctant to purchase without hands-on evaluation. The Diving Equipment and Marketing Association (DEMA) actively supports specialty retail through training initiatives and certification partnerships that sustain foot traffic to specialist shops.

The online channel is fast-growing distribution mode, driven by the expansion of e-commerce platforms and growing comfort among experienced divers with direct-to-consumer purchasing. Manufacturers are increasingly investing in digital customer support tools, including virtual consultations and detailed fitting guides, to bridge the service gap inherent to online retailer sales, gradually eroding the traditional advantage of physical specialty retailers.

End-user Insights

The civilian/individual segment dominates the end-user category, capturing approximately 79% of market demand. Civilian divers, spanning recreational enthusiasts, certified hobbyists, and adventure travelers, represent the broadest and most diverse consumer base, generating both direct personal purchase demand and indirect rental-fleet procurement through dive centers and resorts.

The U.S. Sports and Fitness Industry Association (SFIA) data confirms the substantial size of this civilian diver population in North America alone. Unlike military or commercial operators who procure in bulk according to institutional specifications and long replacement cycles, civilian divers purchase based on personal preference, budget, and brand loyalty, creating a fragmented but high-volume demand pattern.

Regional Insights

North America Diving Regulator Market Trends & Analysis

North America is the leading region in the global diving regulator market, accounting for approximately 32% of total revenue in 2026. The region benefits from a mature and well-established scuba diving ecosystem, including a large diver population, developed coastal tourism infrastructure, and a strong presence of major equipment manufacturers.

U.S. Diving Regulator Market Size

The U.S. accounts for the largest country-level share within North America, representing approximately US$ 165 Mn in 2026, supported by approximately 2.5 million active scuba divers and a dense network of specialty dive retailers. The U.S. Bureau of Economic Analysis (BEA) recorded outdoor recreation value-added of approximately USD 374 billion in 2020, of which scuba diving is a contributing sub-segment. Demand is increasingly driven by upgrades and replacement among existing divers rather than new entrant growth.

Europe Diving Regulator Market Trends, Drivers, & Insights

Europe is the second-largest regional market for diving regulators, accounting for approximately 28% of global revenue. The region's strength derives from a rich maritime heritage, a vibrant recreational diving culture centred on the Mediterranean, the North Sea, and the Atlantic, and the highest regulatory oversight standards in the world, particularly the EN 250 cold-water performance standard, which governs regulator certification across European Union member states.

Germany Diving Regulator Market Size

Germany represents approximately US$ 42 Mn in 2026, underpinned by strong industrial and technical diving demand linked to North Sea energy operations and robust recreational culture. The professional and military diving sectors, including offshore oil and gas in the North Sea and offshore wind installation, are significant purchasers of high-performance regulators.

U.K. Diving Regulator Market Size

The United Kingdom is likely to account for approximately US$ 38 Mn in 2026, supported by home-grown premium brands and a strong cold-water recreational community. The region is also the epicenter of sustainability-driven product innovation, with brands such as Apeks (U.K.) leading the development of eco-material regulators.

France Diving Regulator Market Size

France is poised for approximately US$ 30 Mn in 2026, driven by Mediterranean resort diving and a heritage of strong industry representation through manufacturers such as Beuchat International. The U.S.-led global tariff environment of 2025, while primarily affecting trans-Atlantic goods flows, has also increased cost uncertainty for European brands exporting to the U.S. market.

Asia Pacific Diving Regulator Market Drivers & Analysis

Asia Pacific is the fast-growing market for global diving regulator market, accounting for approximately 26% of revenue in 2026 and projected to expand at a CAGR of 6.5% through 2033. Rapid economic development, rising disposable incomes, and the emergence of world-class marine tourism destinations are transforming the region into a primary growth engine. Indonesia, the Philippines, Thailand, Malaysia, and Australia collectively attract millions of international and domestic divers annually, supported by rich coral reef ecosystems, accessible dive certification infrastructure, and government-backed tourism promotion.

China Diving Regulator Market Size

China is estimated at approximately US$ 58 Mn in 2026, representing the largest single country market in the region, driven by rapidly growing recreational participation and substantial commercial offshore activity. Commercial and offshore diving demand is also growing sharply, tied to energy infrastructure development in the South China Sea and offshore wind projects in China, Japan, and South Korea.

India Diving Regulator Market Size

India is estimated at approximately US$ 14 Mn in 2026, an emerging market supported by growing adventure tourism in Andaman, Lakshadweep, and Goa. Rapid economic development, rising disposable incomes, and the emergence of world-class marine tourism destinations are transforming the region into a primary growth engine.

Japan Diving Regulator Market Size

Japan is estimated at approximately US$ 22 Mn in 2026, underpinned by a mature recreational diver base and domestic brands such as TUSA (Tabata Co., Ltd.). The region's manufacturers, particularly in China and Taiwan, are simultaneously improving their quality positioning, increasing both domestic consumption and export competitiveness.

Competitive Landscape

The global diving regulator market is moderately consolidated, with a small number of dominant multinational brands, primarily Aqua Lung International, SCUBAPRO, Mares, and Apeks, holding the majority of global revenue, while a larger cohort of regional and niche players competes in specialized price bands or technical segments. Emerging business model trends include modular regulator systems with interchangeable parts, direct-to-consumer e-commerce expansion, and subscription-based servicing programmes offered through authorized dealer networks.

Key Developments:

- March 2026: Argo Defence Group completed the acquisition of Poseidon Diving Group for SEK 56 million, strengthening its portfolio in advanced diving and underwater systems. The acquisition expands capabilities in diving and breathing technologies used by military, professional, and specialized underwater applications, supporting innovation and growth within the diving equipment market.

- March 2026: Hollis announced a voluntary recall of certain 200LX Second Stage regulators after reports indicated internal components could separate or fracture, potentially causing regulator malfunction. The recall affects units sold between 2017 and 2025 and includes a retrofit program with redesigned components to strengthen safety and product reliability in diving equipment systems.

- May 2025: Aqualung announced the launch of Aquasense, a smart connected diving regulator designed to enhance diver safety and performance. The system integrates wireless communication, respiratory monitoring, and real-time dive insights through the Pulsa dive computer and mobile app, supporting improved underwater awareness and post-dive analytics.

Global Diving Regulator Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 526.9 Mn |

|

Current Market Value (2026) |

US$ 686.2 Mn |

|

Projected Market Value (2033) |

US$ 978.5 Mn |

|

CAGR (2026–2033) |

5.2% |

|

Leading Region |

North America, ~32% |

|

Dominant Segment |

Balanced Regulators, ~40% |

|

Top-ranking Segment |

Recreational Diving, ~58% |

|

Incremental Opportunity |

US$ 292.3 Mn |

Companies Covered in Diving Regulator Market

- Aqua Lung International

- SCUBAPRO (Johnson Outdoors)

- Mares (HEAD Sport GmbH)

- Apeks Marine Equipment

- Cressi Sub S.p.A.

- Atomic Aquatics

- Oceanic

- Sherwood Scuba

- Poseidon Diving Systems

- TUSA (Tabata Co., Ltd.)

- Beuchat International

- Zeagle Systems

- Seac SubHollis

- Dive Rite

- H2Odyssey

- IST Sports

- Saekodive

- Genesis Scuba

- Halcyon Dive Systems

Frequently Asked Questions

The global Diving Regulator Market is valued at US$ 686.2 Mn in 2026 and is projected to reach US$ 978.5 Mn by 2033, growing at a CAGR of 5.2% over the forecast period. Growth is underpinned by rising recreational diving participation worldwide, expanding commercial underwater sectors, and sustained product innovation across material science and digital integration.

The key demand drivers include the rising global participation of certified scuba divers, estimated at 6 million active divers worldwide per DEMA, the rapid expansion of marine and adventure tourism, particularly in the Asia Pacific, and the growing commercial diving sector linked to offshore energy infrastructure, subsea cable installation, and offshore wind-farm maintenance. Technological advancements in regulator materials and design also stimulate demand for replacements and upgrades.

Balanced Regulators are the leading product type segment, accounting for approximately 40% of total market revenue. Their dominance is driven by superior breathing performance across varying depths and tank pressures, broad applicability across recreational, technical, and professional diving contexts, and their compliance with the EN 250 cold-water certification standard widely mandated in European and professional diving markets.

North America is the leading region with approximately 32% of global market share in 2026, driven by the largest active diver population, a mature specialty retail and servicing infrastructure, and the headquarters presence of major global brands. Asia Pacific is the fastest-growing region, projected at a CAGR of 6.5% through 2033.

The key opportunity lies at the intersection of sustainability and digital innovation. Manufacturers that develop regulators combining eco-friendly materials with wireless digital air-integration technology compatible with modern dive computers stand to capture premium market segments. The Asia Pacific marine tourism boom, with countries such as Indonesia, Thailand, and the Philippines driving rapid dive-based expansion, also represents a significant addressable market for both mid-range and premium regulator solutions.

The leading companies include Aqua Lung International, SCUBAPRO, Mares, Apeks Marine Equipment, Cressi Sub S.p.A., Atomic Aquatics, Oceanic, Sherwood Scuba, Poseidon Diving Systems, TUSA, Beuchat International, Zeagle Systems, Seac Sub, Hollis, and Dive Rite. The June 2025 acquisition of Aqua Lung Group by HEAD Group has created the largest multi-brand portfolio.