- Processed Food

- Cultured Buttermilk Market

Cultured Buttermilk Market Size, Share, and Growth Forecast 2026 - 2033

Cultured Buttermilk Market by Product Type (Plain Cultured Buttermilk, Flavored Cultured Buttermilk), by Form (Liquid, Powder), by Sales Channel (B2B, B2C), by Regional Analysis, 2026-2033

Cultured Buttermilk Market Share and Trends Analysis

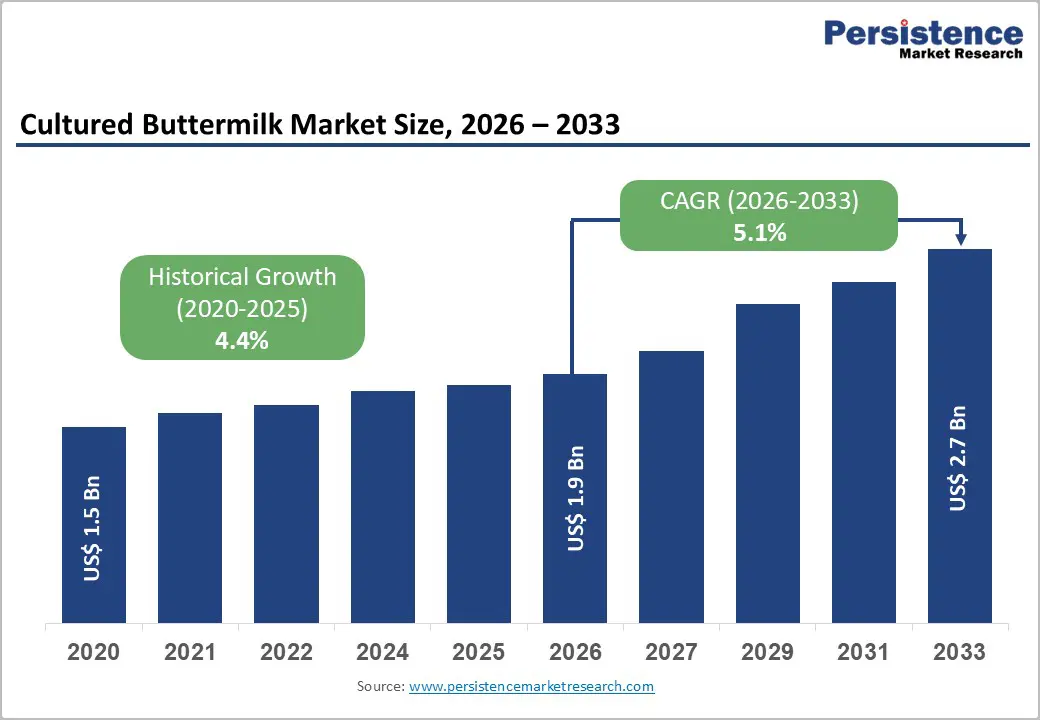

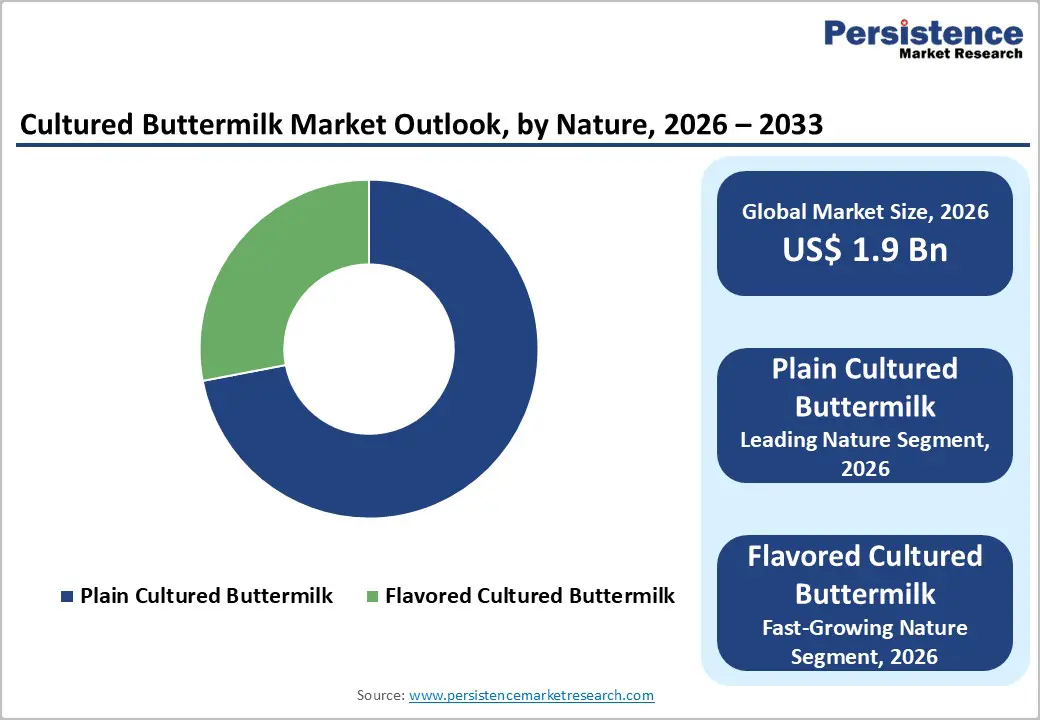

The global Cultured Buttermilk Market size is expected to be valued at US$ 1.9 billion in 2026 and projected to reach US$ 2.7 billion by 2033, growing at a CAGR of 5.1% between 2026 and 2033.

Cultured buttermilk is transitioning from a traditional dietary staple into a functional, lifestyle-aligned fermented beverage. Shifts in gut health awareness, product innovation, and regional consumption patterns are reshaping demand dynamics across global markets.

Key Industry Highlights

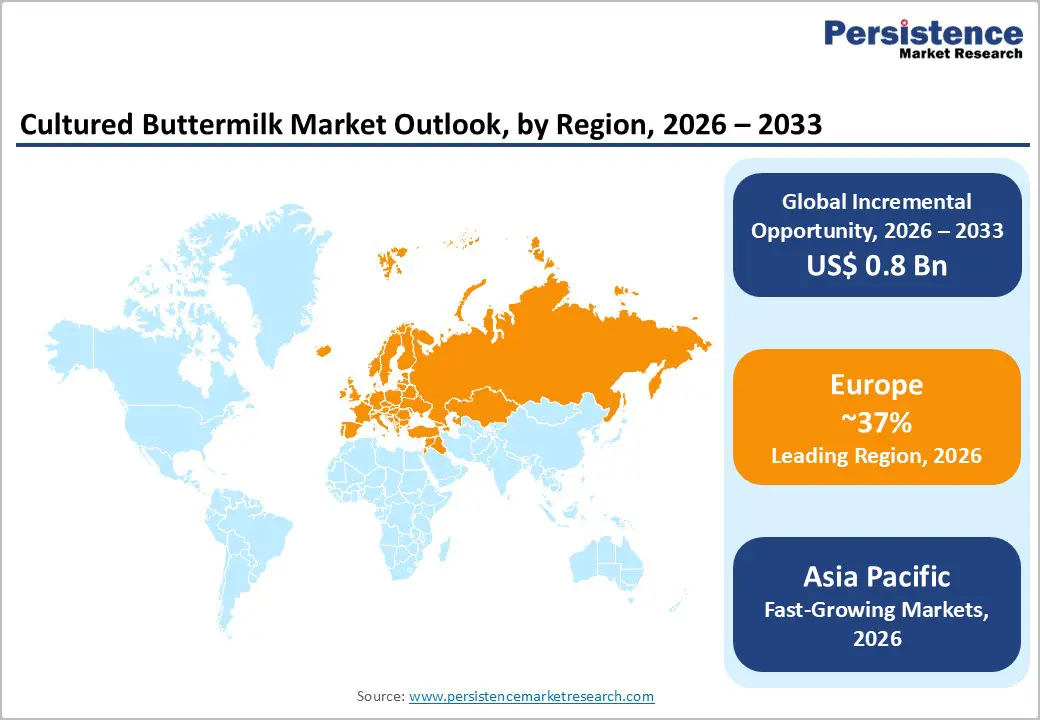

- Leading Region: Europe, holding approximately 37% market share, supported by strong dairy heritage, clean-label preferences, and widespread acceptance of fermented foods across daily diets and culinary applications.

- Fastest-Growing Region: Asia Pacific, driven by urbanization, packaged traditional beverages, expanding cold-chain infrastructure, and rising digestive health awareness in India, China, Japan, and South Korea.

- Fastest-Growing Form Segment: Powdered Buttermilk, fueled by demand from food processors seeking shelf-stable, transport-efficient dairy ingredients for bakery, snacks, sauces, and seasoning blends.

- Market Drivers: Rising consumer focus on gut health and probiotics is elevating cultured buttermilk as a natural, food-based digestive solution aligned with clean eating and everyday wellness routines.

- Opportunities: Development of flavored and fortified cultured buttermilk variants targeting youth and lifestyle consumers, supported by functional claims, modern packaging, and differentiated taste profiles.

- Key Developments: In November 2024, MilkyMist, a leading dairy innovator from South India, partnered with SIG and AnaBio Technologies to launch the world’s first long-life probiotic buttermilk in aseptic carton packaging.

| Key Insights | Details |

|---|---|

| Global Cultured Buttermilk Market Size (2026E) | US$ 1.9 Bn |

| Market Value Forecast (2033F) | US$ 2.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.4% |

Market Dynamics

Driver – Rising consumer focus on gut health and probiotics increases demand for cultured buttermilk

Curiosity around digestive wellness has moved from niche nutrition circles into everyday food decisions, positioning cultured buttermilk as a familiar yet functional solution. Consumers increasingly connect fermented dairy with microbial balance, digestive comfort, and everyday immunity support, elevating cultured buttermilk beyond a traditional refreshment into a purpose-driven beverage. Its naturally occurring cultures appeal to shoppers seeking food-based gut solutions rather than clinical supplements, strengthening relevance across age groups.

This shift is reinforced by growing skepticism toward heavily processed wellness products, pushing demand toward foods with inherent fermentation benefits. Cultured buttermilk fits seamlessly into daily diets, offering hydration, digestibility, and perceived metabolic balance. As gut health messaging becomes mainstream, brands benefit from a product that already aligns with digestive credibility, minimal processing expectations, and habitual consumption patterns, sustaining demand growth without requiring radical consumer behavior change.

Restraints – Competition from plant-based probiotic beverages

A wave of fermented plant-based drinks is reshaping how consumers perceive probiotic intake, creating competitive pressure for cultured buttermilk. Beverages made from oats, soy, coconut, and rice are gaining shelf visibility, promoted as dairy-free, digestive-friendly options for modern lifestyles. Their alignment with vegan, lactose-sensitive, and sustainability-focused audiences diverts attention from traditional dairy formats.

Marketing narratives around light digestion, ethical sourcing, and novelty flavors amplify this shift, especially among younger demographics. Cultured buttermilk faces the challenge of remaining relevant when plant-based alternatives frame themselves as progressive wellness choices. While functionality overlaps, perception favors innovation and dietary flexibility. Without refreshed positioning, dairy-based fermented drinks risk being viewed as conventional, limiting appeal in segments where experimentation and dietary identity strongly influence purchasing decisions.

Opportunity – Development of flavored and fortified cultured buttermilk variants targeting youth and lifestyle consumers

Flavor-led innovation is unlocking a new consumption layer for cultured buttermilk, particularly among youth and lifestyle-driven consumers. Younger buyers expect taste variety, visual appeal, and functional benefits in everyday beverages, creating space for fruit-infused, spiced, and savory formulations. These variants reposition cultured buttermilk from a meal companion into a standalone refreshment suited for active routines.

Fortification further strengthens differentiation, enabling protein, electrolyte, or micronutrient enhancement aligned with fitness, hydration, and recovery trends. For startups, this lowers entry barriers by allowing niche positioning without scale dependency. Established players gain portfolio depth while protecting core volumes. When combined with modern packaging and lifestyle branding, flavored and fortified cultured buttermilk evolves into a versatile functional drink, bridging tradition with contemporary wellness expectations and expanding consumption beyond regional familiarity.

Category-wise Analysis

Product Type Analysis

Plain Cultured Buttermilk holds approx. 72% market share as of 2025, reflecting its entrenched role in daily consumption and food preparation. Its dominance stems from versatility, cultural familiarity, and trust built over generations. Consumers associate plain variants with authenticity, digestive comfort, and minimal intervention, reinforcing repeat purchases across households and foodservice channels.

Unflavored profiles also provide functional reliability in cooking, baking, and marinades, strengthening institutional demand. Price accessibility compared to flavored alternatives supports volume leadership in cost-sensitive markets. From a production standpoint, plain cultured buttermilk offers consistency, lower formulation complexity, and easier regulatory alignment. These structural advantages maintain its leadership despite innovation elsewhere, ensuring plain variants remain the commercial backbone of the global cultured buttermilk category.

Form Analysis

Powdered buttermilk is projected to grow at a CAGR of 8.4% during the forecast period, driven by demand for shelf-stable dairy ingredients. Food manufacturers value its extended usability, transport efficiency, and functional consistency in bakery, snacks, sauces, and seasoning blends. The format aligns with industrial needs where liquid handling poses logistical and spoilage risks.

Rising interest in convenient dairy solutions further accelerates adoption across institutional kitchens and export-oriented supply chains. Powdered forms reduce cold storage dependence while maintaining characteristic tang and emulsification properties. For producers, this unlocks new application markets beyond beverage consumption, expanding revenue streams. As food processing intensifies globally, powdered buttermilk benefits from scalability, formulation flexibility, and compatibility with dry mix innovations.

Region-wise Insights

Europe Cultured Buttermilk Market Trends and Insights

Europe holds approximately 37% market share in the global Cultured Buttermilk Market, anchored by deep-rooted dairy consumption habits. Germany emphasizes clean-label fermented drinks, while France integrates cultured buttermilk into culinary applications and premium dairy offerings. The UK market focuses on gut-friendly positioning tied to everyday wellness routines.

Southern Europe shows regional adaptation. Spain blends traditional dairy refreshment with modern convenience packaging, while Italy explores artisanal fermentation and regional sourcing narratives. Across Europe, sustainability influences packaging shifts toward recyclable bottles and reduced food waste strategies. Retailers support private-label expansion, increasing accessibility. These trends reinforce Europe’s leadership by balancing heritage dairy practices with evolving health, environmental, and lifestyle expectations across diverse consumer segments.

Asia Pacific Cultured Buttermilk Market Trends and Insights

Asia Pacific Cultured Buttermilk Market is expected to grow at a CAGR of 8.7%, fueled by dietary modernization and urban consumption patterns. India drives volume through traditional spiced buttermilk adapted into packaged formats. China shows rising curiosity toward fermented dairy as digestive awareness grows among urban consumers.

Japan emphasizes precision fermentation and portion-controlled servings linked to digestive harmony, while South Korea integrates cultured dairy into functional beverage routines. Across the region, manufacturers focus on affordability, localized flavors, and ambient-stable innovations. Expanding cold chains and organized retail accelerate penetration. Unlike Western markets, growth here blends tradition with modernization, positioning cultured buttermilk as both familiar and aspirational across evolving dietary landscapes.

Market Competitive Landscape

The global Cultured Buttermilk Market remains moderately fragmented, with strong regional players alongside multinational dairy groups. Leading companies invest in flavor innovation, digestive positioning, and differentiated packaging to strengthen shelf presence. Certifications linked to quality, safety, and sourcing reinforce brand trust across regulated markets.

Competition increasingly centers on product innovation, sustainability commitments, and targeted marketing. Companies introduce region-specific flavors while upgrading packaging to improve recyclability and shelf life. Strategic sales partnerships with retailers, foodservice operators, and institutional buyers expand reach. Compliance with evolving government regulations shapes formulation and labeling strategies. Success depends on balancing tradition with innovation, allowing brands to defend core volumes while capturing emerging lifestyle-driven demand.

Key Developments:

In November 2024, MilkyMist, a leading dairy innovator from South India, partnered with SIG and AnaBio Technologies to launch the world’s first long-life probiotic buttermilk in aseptic carton packaging, enabling ambient storage while preserving probiotic efficacy and expanding access beyond cold-chain–dependent markets.

Companies Covered in Cultured Buttermilk Market

- Danone

- Saputo Inc.

- Lactalis Group

- Yili Group

- Mengniu Dairy

- Alta Dena Dairy

- Agri-Mark Inc.

- California Dairies, Inc.

- Maola

- Others

Frequently Asked Questions

The global Cultured Buttermilk market is expected to reach around US$ 1.9 billion in 2026.

Rising consumer focus on gut health and probiotics increases demand for cultured buttermilk is key demand driver in the Cultured Buttermilk market.

Europe leads the Cultured Buttermilk market with about 37% share in 2025.

Development of flavored and fortified cultured buttermilk variants targeting youth and lifestyle consumers is the key opportunity for key players in the market.

Key players include Danone, Saputo Inc., Lactalis Group, Yili Group, Mengniu Dairy, and others