- Hardware & Software IT Services

- Crisis, Emergency, and Incident Management Platforms Market

Crisis, Emergency, and Incident Management Platforms Market Size, Share, and Growth Forecast, 2025 - 2032

Crisis, Emergency, and Incident Management Platforms Market By Solution Type (Emergency/Mass Notification Systems, Others), End-user (Government & Defense, Healthcare & Life Sciences, Corporate/BFSI, Energy & Utilities, Others), Emergency Type, and Regional Analysis for 2025 - 2032

Crisis, Emergency, and Incident Management Platforms Market Size and Trends Analysis

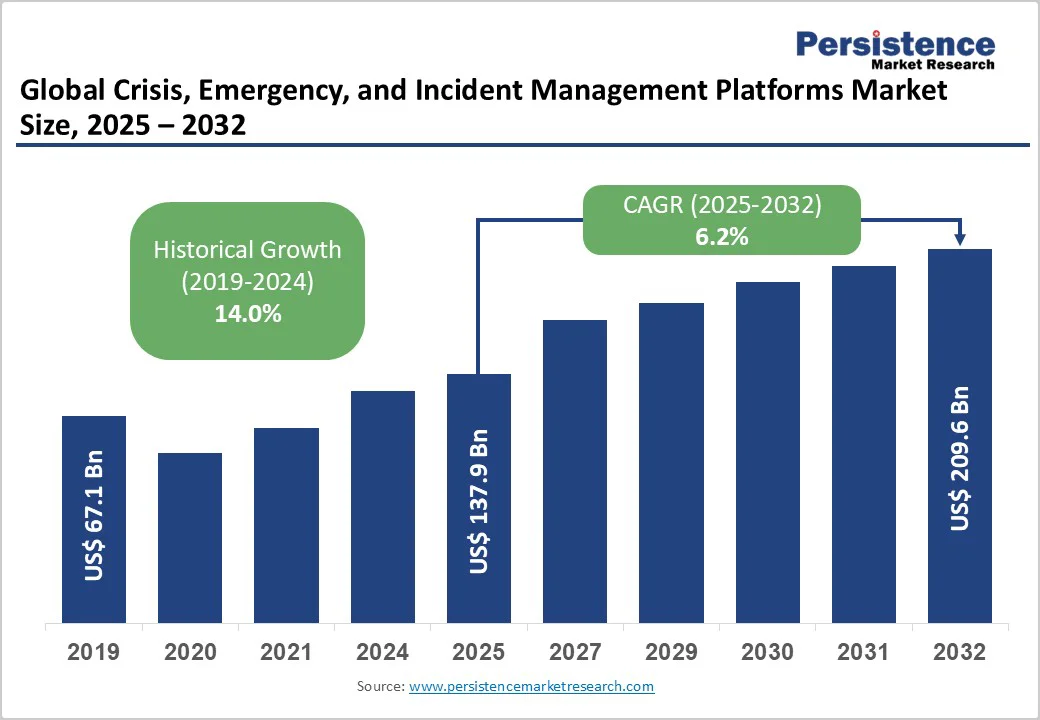

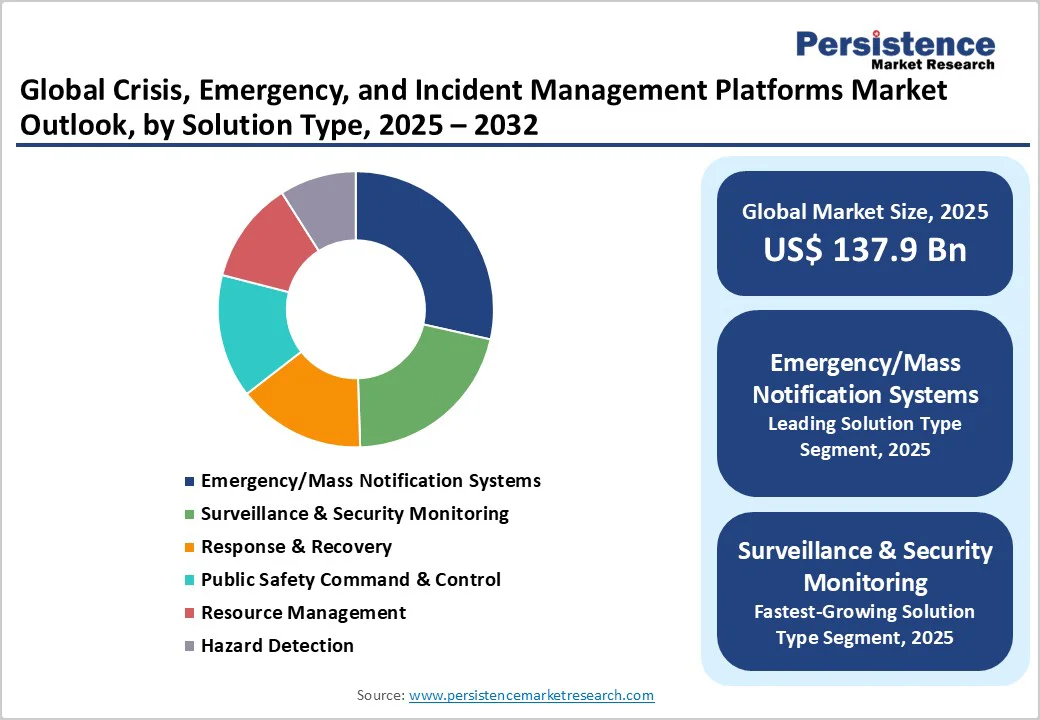

The global crisis, emergency, and incident management platforms market size is likely to be valued at US$137.9 Billion in 2025, and is estimated to reach US$209.6 Billion by 2032, growing at a CAGR of 6.2% during the forecast period 2025−2032, driven by recurrent climate-related disasters, escalating cyber-security threats, and increasingly stringent regulatory mandates surrounding public safety infrastructure. Urbanization and rising population density drive demand for scalable, data-driven incident management solutions, with AI-powered surveillance and cloud deployments reshaping the market, led by government, healthcare, and BFSI sectors.

Key Industry Highlights

- Dominant Solution Type: Emergency/mass notification systems are set to dominate with a 28.5% market share in 2025, driven by urbanization and regulatory mandates.

- Fastest-growing Solution Type: Surveillance & security monitoring platforms are forecast to grow at 8.5% CAGR during 2025–2032, reflecting an increasing demand for AI-enabled analytics and real-time situational awareness.

- Largest End-user: The government & defense vertical is expected to hold a projected 37% market share in 2025, remaining the largest end-user segment in the market.

- Dominant Region: North America is anticipated to lead with an estimated 42% market share, supported by strong disaster regulations of the U.S. and technological innovation.

- Fastest-growing Regional Market: Asia Pacific is poised to be the fastest-growing regional market from 2025 to 2032 at around 7.3% CAGR, benefiting from higher investments in disaster reduction technologies, policy reforms, and aggressive Smart City investments.

- Competitive Dynamics: The market is increasingly favoring ecosystem-based approaches, with interoperability, cross-platform integration, and partnerships with cloud providers and telecom operators becoming prerequisites for competitive viability.

- March 2025: Oracle enhanced its health system operations suite with tools such as Oracle Health Patient Flow and Oracle Health Transfer Center, which enable better bed management, mass patient transfers, and evacuation planning in near real time.

| Key Insights | Details |

|---|---|

|

Crisis, Emergency, and Incident Management Platforms Market Size (2025E) |

US$137.9 Bn |

|

Market Value Forecast (2032F) |

US$209.6 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

14.0% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Convergence of Climate Resilience Planning and Smart City Integration

Urban centers globally are embracing climate resilience strategies that prioritize advanced crisis and emergency platforms as critical infrastructure, underpinned by multi-hazard early warning systems, dynamic evacuation network overlays, and real-time geospatial analytics. According to the Global Assessment Report of the UN Office for Disaster Risk Reduction (UNDRR), climate-induced disasters, including extreme heat, flooding, and hurricanes, have resulted in dramatic losses in the past decade, with direct damages in billions in 2022 alone.

Recognizing the value of predictive modeling, cities such as Singapore, Rotterdam, and Los Angeles have invested in platforms coupling AI-driven scenario simulation with GIS mapping to optimize emergency logistics and inter-agency coordination. The European Union (EU)’s 2025 regulatory harmonization mandates cross-border alerting systems and real-time resource tracking for all member states, driving platform upgrades at both municipal and national levels. Businesses embedded in the urban management value chain are leveraging these platforms for resilience benchmarking, insurance underwriting, and ESG (Environmental, Social, & Governance) risk mitigation.

Resource and Skills Gaps in Developing Economies Limit Implementation Scale

The crisis, emergency, and incident management platforms market growth is stymied due to substantial deployment barriers in emerging economies in the form of funding constraints, fragmented digital infrastructure, and acute shortages of specialized personnel. A recent survey by the Organisation for Economic Co-operation and Development (OECD) found that only a small percentage of municipalities in Southeast Asia and Sub-Saharan Africa have the financial and technical capabilities to execute advanced emergency platform rollouts.

The cost-per-capita ratio for comprehensive platform deployment is more than two times higher in these regions due to a reliance on custom integration, the absence of open data standards, and logistical challenges associated with decentralized agency networks. Poor cyber-security readiness at local-level governance bodies further compounds the restraints on the market.

Healthcare Sector Digitalization and Pandemic Preparedness

Healthcare digital transformation is creating outsized opportunities for crisis and emergency platforms, particularly those with advanced analytics, interoperability, and real-time patient logistics capabilities. The pandemic exposed severe shortfalls in incident management readiness among hospitals and health systems. As governments fund healthcare digital infrastructure upgrades, market players are capitalizing on the demand for scalable platforms supporting automated triage, secure mass notification, and hospital capacity optimization.

For example, the FY2026 budget of the U.S. Health and Human Services (HHS) outlines major changes in the way the federal government will henceforth support emergency preparedness in the healthcare system. The coming together of AI, telemedicine, and genomic monitoring is unlocking new services such as predictive outbreak alerts, automated contact tracing, and embedded geo-fencing for medical logistics, making healthcare the single most lucrative vertical for technology differentiation and margin expansion.

Category-wise Analysis

Solution Type Insights

Emergency/Mass notification systems are expected to lead with approximately 28.5% of the market revenue share in 2025. This leadership stems from stringent regulatory mandates such as the Integrated Public Alert & Warning System (IPAWS) of the U.S. Federal Emergency Management Agency (FEMA) and the EU’s Emergency Communication Code, which obligate governments and large enterprises to implement robust multi-channel communication infrastructures. These platforms deliver real-time alerts through SMS, voice, email, mobile apps, and social media, serving an indispensable role in public safety initiatives. The criticality of multichannel, scalable alerting coupled with interoperability and data security has made this segment a procurement priority for public agencies and commercial entities alike.

Surveillance & security is expected to be the fastest-growing segment with a projected CAGR of 8.5% from 2025 to 2032. This acceleration is driven by the convergence of AI-powered video analytics, sensor network integration, and IoT-enabled real-time data feeds that empower emergency responders with actionable situational awareness. Capabilities such as crowd density analysis, anomaly detection, and rapid threat assessment are reshaping operational protocols, especially in metropolitan environments and complex industrial settings.

End-user Insights

The government & defense sector remains the largest end-user segment, estimated to hold a 37% of the crisis, emergency, and incident management platforms market revenue share in 2025. This dominance is reinforced by substantial investments in public safety infrastructure, extending from municipal response frameworks to national homeland security operations. Public sector procurement follows a predictable cadence driven by multi-year funding cycles, regulatory compliance mandates, and the necessity to modernize legacy systems with cloud-based, interoperable platforms. Agencies are increasingly adopting platforms that bolster multi-agency coordination, real-time resource tracking, and public communication during emergencies, leveraging breakthroughs in AI and geospatial intelligence.

The healthcare and life sciences segment is likely to be the fastest-growing end-user segment over the forecast horizon, fueled by heightened pandemic preparedness imperatives and digital transformation initiatives. Healthcare providers are investing in platforms capable of coordinated mass casualty management, automated patient triage, secure intra-facility communication, and supply chain monitoring. Regulatory pressures such as those emanating from HIPAA and HHS emergency preparedness programs amplify demand for compliance-aligned, resilient platforms.

Emergency Type Insights

Natural disaster management remains the largest emergency type segment, capturing an estimated 57% of the market share in 2025. The prominence of the segment is anchored in the persistent and escalating frequency of climate-driven events such as floods, wildfires, hurricanes, and earthquakes, especially in the vulnerable geographies of Asia Pacific, Coastal North America, and Southern Europe. Advanced geospatial mapping, multi-hazard early warning systems, and real-time damage assessment are pivotal technological pillars supporting this segment. Governments and large enterprises deploy specialized flood response, wildfire containment, and seismic monitoring platforms, driving sustained procurement cycles and investments in innovation.

Cyber incident management solutions are experiencing explosive growth, with a forecast CAGR of around 11.3% during 2025-2032. This surge is propelled by escalating cyber threats encompassing ransomware, data breaches, and business interruption events across sectors such as BFSI, healthcare, government, and critical infrastructure. The adoption of integrated cyber crisis management platforms facilitates automated incident detection, secure communication networks, compliance reporting, and post-incident forensic analysis. This segment’s rapid evolution reflects rising organizational prioritization of cyber resilience amid a threat landscape marked by increasing complexity and regulatory oversight.

Regional Insights

North America Crisis, Emergency, and Incident Management Platforms Market Trends

North America is poised to lead with an estimated 42% of the crisis, emergency, and incident management platforms market share in 2025, powered by high levels of government spending, regulatory rigor, and a technology innovation ecosystem concentrated in the United States and Canada. The United States stands at the helm, backed by FEMA’s regulations and dedicated federal funding for public safety and crisis technology infrastructure. The regulatory environment is characterized by progressive frameworks such as NextGen 911, Cybersecurity Infrastructure Security Agency (CISA) mandates, and HIPAA emergency response standards, ensuring evolving requirements for interoperability, data privacy, and resilience.

The regional competitive landscape, moderately consolidated, features global leaders specializing in AI-driven analytics and cloud-based platforms, including Motorola Solutions and Honeywell, complemented by agile mid-tier firms driving innovation in mobile alerting and IoT integration.

Europe Crisis, Emergency, and Incident Management Platforms Market Trends

Europe is likely to command about 28% of the market share in 2025, sustained by regulatory harmonization and strategic funding programs across leading economies such as Germany, the U.K., France, and Spain. The regional market is driven by the EU’s Emergency Communications Code, which mandates real-time interoperable alerting systems across member states, GDPR-aligned data governance, and increased interoperability requirements facilitating cross-border coordination.

Germany’s leadership is anchored in multi-hazard resilience investments and progressive adoption of AI-enabled crisis coordination platforms, while the U.K.’s National Health Service (NHS) incorporates cloud-based patient notification and logistics management into broader healthcare reform efforts. France and Spain’s investments in wildfire and flood early warning systems reflect broader EU resilience strategies tied to climate change mitigation funding.

Competition is characterized by a balanced set of multinational technology vendors and regional integrators adept at local compliance and sustainable innovation, particularly in the domains of energy grid resilience and urban safety. Policy-driven procurement coupled with ESG-focused investment signals a durable market for scalable, privacy-aware platform deployments. Collaborative EU-wide procurement frameworks and investment partnerships with entities such as the European Investment Bank (EIB) can further facilitate platform modernization, optimizing cost structures and accelerating the adoption curve.

Asia Pacific Crisis, Emergency, and Incident Management Platforms Market Trends

Asia Pacific is the fastest-growing regional market for crisis, emergency, and incident management platforms, poised to expand at a CAGR of 7.3% between 2025 and 2032. This growth is energized by a convergence of factors, including rapid urbanization in China, India, and ASEAN nations, government-led Smart City investments, and increasing digital literacy rates facilitating technology penetration.

China has been aggressively deploying national emergency management platforms integrating real-time hazard detection with AI-based predictive response capabilities, while India is fast-tracking infrastructure rehabilitation through the National Disaster Management Guidelines and investments in flood and seismic alert systems.

Regulatory reforms tailored to local vulnerabilities and cross-border cooperation initiatives are catalyzing platform growth. Markets in this region increasingly favor cloud-based, mobile-first solutions implemented through public-private partnerships. Competitive advantage accrues to providers able to navigate fragmented policy environments and deliver cost-effective, scalable platforms adaptable to multi-jurisdictional governance.

Competitive Landscape

The global crisis, emergency, and incident management platforms market structure is moderately consolidated, with an estimated 58% of revenue controlled by the top 10 companies as of 2025. Leading vendors, including Motorola Solutions, Honeywell, IBM, and Hexagon AB, have distinguished themselves through extensive product portfolios encompassing cloud-based platforms, AI-powered analytics, communications infrastructure, and managed services.

The market also features several nimble, niche specialists focusing on cybersecurity incident response, healthcare emergency coordination, or geospatial intelligence, fostering moderate fragmentation within vertical and geographic sub-segments. Growth strategies prominently include mergers and acquisitions, technology alliances, and regional expansions, designed to capture specialized capability gaps, accelerate innovation cycles, and deepen penetration in emerging markets.

Key Industry Developments

- In October 2025, the UAE’s NCEMA launched the Emergency and Crisis Atlas at Gitex Global, a digital platform with 40+ AI-powered GIS applications, offering predictive modeling, risk forecasting, and interactive maps to enhance national preparedness and optimize crisis response operations.

- In July 2025, UNDP and China International Development Cooperation Agency, launched TIAEWS SYC to boost disaster preparedness. Focusing on real-time data alerts, governance, and community outreach, it promotes predictive, data-driven disaster management, enhancing resilience in small island states.

- In June 2025, India launched three disaster management platforms: ICR-ER, NDEM Lite 2.0, and the Assam Flood Hazard Zonation Atlas. These tools enhance response speed and coordination, provide real-time satellite data, and support flood mitigation, resilient agriculture, and disaster planning nationwide.

Companies Covered in Crisis, Emergency, and Incident Management Platforms Market

- Motorola Solutions, Inc.

- Honeywell International Inc.

- IBM Corporation

- Siemens AG

- Hexagon AB

- Everbridge, Inc.

- ESRI (Environmental Systems Research Institute, Inc.)

- Johnson Controls International Plc

- Eaton Corporation Plc

- NEC Corporation

- Intergraph Corporation

- Alert Technologies Corporation

- Atos SE

- BlackBerry Limited

- Collins Aerospace

Frequently Asked Questions

The crisis, emergency, and incident management platforms market is projected to reach US$137.9 Billion in 2025.

Recurrent climate-related disasters, escalating cyber-security threats, and increasingly stringent regulatory mandates surrounding public safety infrastructure are driving the market.

The crisis, emergency, and incident management platforms market is poised to witness a CAGR of 6.2% from 2025 to 2032.

Increasing public and private sector investments in scalable, data-driven incident management solutions and widening deployment of cloud-based and AI-integrated surveillance systems are the key market opportunities.

Motorola Solutions, Inc., Honeywell International Inc., and IBM Corporation are some of the key players.