- Media & Entertainment

- Contextual Market

Contextual Market Size, Share, and Growth Forecast 2026 – 2033

Contextual market by solution type (cloud-based, on-premise), by services (ad campaign management services, consulting services, support services), by end use (BFSI, travel & hospitality, healthcare & life sciences, telecommunications, manufacturing, retail & consumer goods, others), by regional analysis, 2026–2033.

Contextual Market Size and Trend Analysis

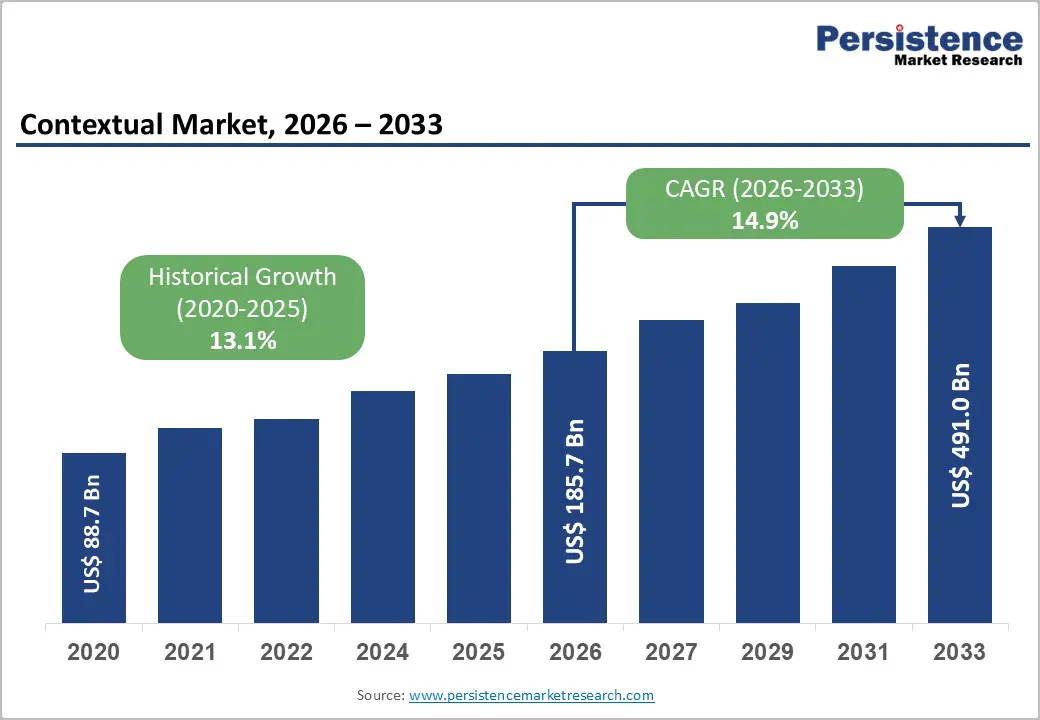

The global Contextual market size is likely to be valued at US$ 185.7 Billion in 2026 and is expected to reach US$ 491.0 Billion by 2033, growing at a CAGR of 14.9% during the forecast period from 2026 to 2033.

The accelerating growth trajectory is driven by the industry's urgent transition away from third-party cookie dependencies, increasing regulatory pressures mandating privacy-first marketing approaches, and escalating demand from enterprises seeking to deliver personalized customer experiences without compromising data privacy standards

Key Market Highlights

- North America maintains regional leadership with 38.2% global market share, driven by advanced technology infrastructure, regulatory frameworks incentivizing privacy-first marketing innovation, and concentrated presence of major Contextual platform providers including Google, Microsoft, Adobe, Oracle, and Amazon continuously enhancing platform capabilities and driving market expansion through strategic acquisitions and product development investments.

- Asia Pacific emerges as fastest-growing region expanding at 11.9% CAGR through 2032, propelled by extraordinary mobile internet penetration, rapid e-commerce digitalization, and 73% adoption rates of generative AI tools in India, establishing region as critical growth frontier where China commands 42.4% regional share while India demonstrates highest growth potential.

- Cloud-based solution deployment captures dominant segment position commanding approximately 62-65% market share, driven by scalability advantages, reduced capital requirements, automated AI model updates, and seamless integration with modern SaaS marketing stacks, reflecting organizational preference for flexible, innovation-optimized deployment models over traditional on-premise infrastructure.

- Retail & Consumer Goods segment demonstrates fastest category growth capturing 24% vertical market share, driven by critical omnichannel personalization requirements, aggressive e-commerce expansion, and measurable performance gains where contextual recommendations deliver 20-25% sales increases and significantly improved customer lifetime value metrics.

- Privacy-regulatory transition and third-party cookie deprecation present exceptional market opportunity, as enterprises mandatorily transition from cookie-dependent targeting to privacy-first approaches, with 90% of marketers already adjusting strategies and contextual solutions positioned as compliance-enabling technologies delivering marketing effectiveness without personal data vulnerability, creating sustained demand extending through entire forecast period.

| Key Insights | Details |

|---|---|

| Contextual Market Size (2026E) | US$ 185.7 Bn |

| Market Value Forecast (2033F) | US$ 491.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 14.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 13.1% |

Market Dynamics

Market Growth Drivers

Privacy-First Marketing Transition and Regulatory Compliance Requirements

The deprecation of third-party cookies, accelerated by regulatory frameworks including the GDPR in Europe and CCPA in the United States, has fundamentally reshapen the digital advertising landscape, making Contextual solutions increasingly indispensable for enterprises seeking sustainable competitive advantages.

Data from IAB's State of Data 2024 reveals that nearly 90% of marketers have shifted their personalization tactics and budget allocation strategies in anticipation of privacy-related changes, with only 49% of brands now considering cookies essential to their marketing strategies, down from 75% just two years prior. The EU AI Act implementations in 2025 have further accelerated adoption of Contextual platforms, as enterprises must demonstrate transparent, explainable advertising decision-making processes that contextual intelligence systems inherently provide through content-based targeting rather than personal data utilization.

Artificial Intelligence and Machine Learning Advancement in Content Analysis

Artificial intelligence and machine learning technologies have revolutionized Contextual capabilities, enabling real-time semantic analysis of content across websites, video platforms, and emerging channels such as generative AI chatbots, with deployment complexity dramatically reduced through cloud-based platforms offering pre-built AI models and natural language processing capabilities. Research shows that 75% of marketing organizations have either fully implemented artificial intelligence or are actively experimenting with AI adoption, and 80% are targeting the reduction of repetitive tasks through AI-driven automation and campaign optimization.

Microsoft Copilot integration in advertising platforms, alongside Google's Advanced Contextual targeting powered by sophisticated language models, exemplifies how AI enables advertisers to analyze millions of articles and content pieces across extended historical periods, thereby identifying and reaching consumers in hyperspecific contextual environments across multiple media formats simultaneously, yielding measurable performance improvements including 276% increases in click-through rates observed in location-based campaigns and 30% cost-per-acquisition reductions across healthcare sector implementations.

Market Restraints

Complexity of Implementation and Organizational Skill Gaps

While Contextual solutions offer substantial technical sophistication, many organizations lack internal expertise and capability to effectively implement, manage, and optimize these platforms, creating significant barriers to adoption particularly among small and mid-cap enterprises, with approximately 38% of marketing professionals indicating they do not know how to use generative AI safely and 43% reporting uncertainty about maximizing value from AI-driven tools.

Integration challenges persist across hybrid and multi-cloud environments, requiring seamless data flow among existing systems, legacy infrastructure, and emerging cloud-native contextual platforms. Successful implementations demand substantial technical resources, change management initiatives, and ongoing staff training investments that many smaller organizations cannot sustain financially or operationally.

Limited Effectiveness in Niche Markets and Emerging Digital Channels

Contextual effectiveness remains constrained in emerging digital environments such as private messaging platforms, decentralized social networks, and proprietary content ecosystems where content analysis becomes significantly more complex and sophisticated AI models encounter reduced data availability for training purposes. Additionally, certain consumer segments and industry verticals demonstrate resistance to contextual approaches, with some premium brands preferring behavioral personalization or first-party data strategies, while emerging platforms, including emerging metaverse environments, blockchain-based advertising networks, and voice-activated shopping ecosystem,s present contextual targeting challenges that existing AI models have not yet adequately addressed, limiting total addressable market expansion in these growth categories.

Market Opportunities

Expansion into Healthcare, Financial Services, and Manufacturing Verticals

Healthcare organizations and financial institutions face extraordinary pressure to modernize customer engagement strategies while maintaining HIPAA and PCI-DSS compliance requirements, creating substantial opportunities for Contextual platforms that deliver personalization without compromising sensitive patient or financial data privacy commitments. The healthcare sector demonstrates particular receptivity, with 76% of healthcare advertising campaigns using contextual approaches significantly outperforming traditional retargeting efforts while simultaneously reducing cost-per-acquisition metrics, indicating substantial opportunity for platform providers and consulting services to establish market presence in these regulated verticals.

Manufacturing and industrial supply chain organizations similarly seek contextual solutions for B2B marketing automation, technical specification matching, and supply chain partner engagement, with platforms like SAP Marketing Cloud and Oracle Eloqua specifically designed to serve enterprise manufacturing buyers who require sophisticated account-based marketing and contextual content delivery across procurement journeys.

Emerging Opportunities in AI-Powered Conversational Commerce and Chatbot Monetization

The rapid proliferation of generative AI chatbots including ChatGPT, Claude, and emerging proprietary corporate AI assistants creates unprecedented opportunities for contextual advertising integration, with the broader chatbot marketing sector projected to expand from approximately US$ 3.6 Billion in 2024 to exceeding US$ 70 Billion by 2034, representing an extraordinary growth frontier for contextual intelligence providers.

Companies like Kontext, a Czech-founded contextual advertising platform focused specifically on native ads within chatbot conversations, secured US$ 10 Million in seed funding during August 2025, demonstrating substantial venture capital recognition of this emerging opportunity where contextual ads integrated directly into conversational flows achieve high engagement without user churn because advertisements appear naturally within the conversational context rather than as disruptive interruptions, with implementations already processing tens of millions of daily impressions for brands including Amazon, Uber, and Canva.

Category-wise Insights

Solution Deployment Model Analysis

Cloud-based Contextual solutions have emerged as the dominant deployment category, capturing approximately 65% market share across enterprise organizations, driven by the demonstrable advantages of scalability, reduced capital expenditure requirements, automated software updates incorporating latest AI advancements, and seamless integration with modern SaaS marketing technology stacks. According to Gartner, worldwide end-user spending on public cloud services is projected to reach US$ 723.4 Billion in 2025, increasing 21.5% from the previous year, with marketing and advertising cloud services representing among the fastest-growing segments as organizations prioritize operational flexibility and rapid innovation cycles over traditional infrastructure ownership models.

Services Category Analysis

Ad Campaign Management Services represent the largest and fastest-growing service segment within the Contextual ecosystem, commanding approximately 55-60% market share as enterprises increasingly seek external expertise and managed service providers to execute sophisticated contextual advertising campaigns across complex, multi-channel environments. Marketing organizations globally face persistent challenges in developing internal capabilities for campaign orchestration across display networks, video platforms, mobile applications, and emerging channels simultaneously, creating sustained demand for consulting services, campaign optimization, and performance analytics offerings where external agencies leverage specialized tools, proprietary data assets, and industry best practices to deliver superior campaign performance compared to internal team capabilities.

End-Use Industry Vertical Analysis

Retail & Consumer Packaged Goods segment commands the dominant position with approximately 24% market share among all industry verticals, driven by the sector's critical need for personalized customer experiences, aggressive pursuit of omnichannel strategies integrating physical and digital touchpoints, and sophisticated analytics requirements where Contextual platforms enable retailers to analyze customer behavior in real-time and deliver contextually relevant promotions, product recommendations, and personalized offers that significantly influence immediate purchasing decisions. Organizations including Walmart utilizing AI-driven pricing strategies achieved 10% sales increases, while Sephora's implementation of contextual AI-powered beauty recommendations generated 20% sales uplift, demonstrating quantifiable business impact driving sustained technology investments in retail sector contextual solutions.

Regional Insights

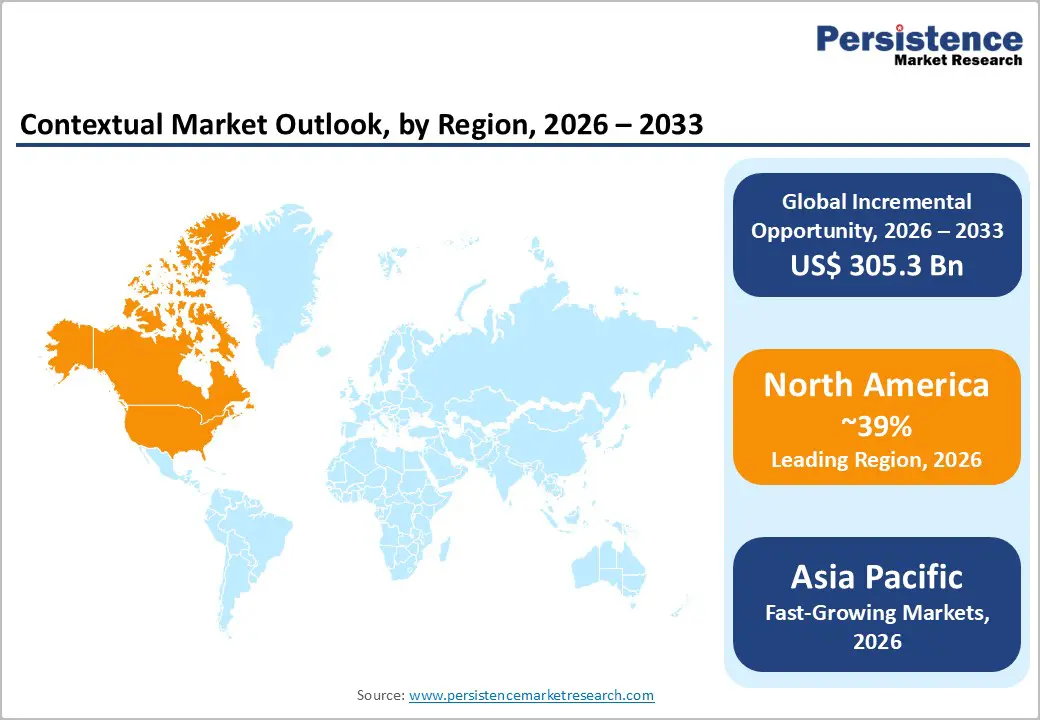

North America Contextual Trends

North America maintains dominant global market leadership, commanding approximately 38.2% market share in regional revenue. This leadership position reflects North America's advanced technological infrastructure, concentrated presence of pioneering technology companies including Google, Microsoft, Adobe, Oracle, and Amazon actively developing and commercializing contextual intelligence platforms, mature regulatory frameworks facilitating privacy-first marketing innovation, and substantial enterprise spending on digital transformation initiatives.

The region's sophisticated ecosystem combines major cloud infrastructure providers including AWS, Microsoft Azure, and Google Cloud offering serverless computing and real-time data processing capabilities essential for sub-millisecond contextual ad decisioning, with enterprise marketing teams demonstrating exceptional receptivity to emerging privacy-first marketing technologies and experimental approaches to contextual targeting that generate early competitive advantages.

Europe Contextual Trends

Europe represents the second-largest regional market for Contextual solutions, driven by exceptionally stringent regulatory environments mandating privacy-first marketing approaches. The region's regulatory complexity spans multiple frameworks including EU AI Act implementation requiring transparent, explainable algorithmic decision-making in advertising contexts, Digital Markets Act targeting anti-competitive practices in digital advertising, and evolving GDPR Reform 2025 initiatives explicitly recognizing small mid-cap enterprises as distinct regulatory entities requiring tailored compliance approaches, thereby creating differentiated market opportunities for contextual solutions serving organizations across varied enterprise size classifications.

Key European markets including Germany, United Kingdom, France, and Spain demonstrate distinctive adoption patterns reflecting regional regulatory stringency and industry verticalization, with Germany's advanced manufacturing and industrial export emphasis driving particular Contextual adoption in B2B and supply chain marketing contexts, while France and Spain emphasize AI transparency and consumer protection considerations informing platform selection and deployment strategies. The region's emphasis on regulatory harmonization, sustainable data practices, and ethical AI development creates market differentiation where contextual platforms emphasizing explainability, transparency in algorithmic decision-making, and minimal personal data utilization establish particular competitive advantages compared to behavior-tracking alternatives generating regulatory resistance and organizational risk exposure across European markets.

Asia Pacific Contextual Trends

Asia Pacific represents the fastest-growing regional market, with the regional contextual advertising market valued at approximately US$ 54 Billion, expanding through 11.9% CAGR during 2025-2032, driven by extraordinary mobile internet penetration, rapid digitalization of consumer commerce, and concentration of global e-commerce growth within region as China, India, and Southeast Asian countries experience unprecedented digital transformation accelerating at rates substantially exceeding Western markets.

China specifically commands 42.4% share of Asia-Pacific programmatic and contextual advertising, leveraging sophisticated super-app ecosystems including WeChat and Alipay unifying social commerce, payments, and content consumption, combined with rapid 5G infrastructure deployment expanding high-quality ad inventory and enabling sophisticated real-time bidding and contextual decisioning across emerging platforms not yet matured in Western markets.

Competitive Landscape

Market Structure Analysis

The Contextual solutions market exhibits moderately consolidated competitive dynamics, with large technology infrastructure companies including Google, Microsoft, Oracle, Adobe, SAP, and Amazon controlling substantial market share through integrated platforms combining advertising networks, customer data platforms, marketing automation, and analytics capabilities, while specialized contextual intelligence providers including GumGum, Seedtag, Taboola, Outbrain, Criteo, and emerging companies like Kontext compete through superior contextual analysis capabilities, specialized vertical solutions, or emerging channel expertise.

Major technology platforms are executing explicit expansion strategies emphasizing contextual targeting capabilities within existing marketing technology portfolios, with Oracle strengthening contextual intelligence through Grapeshot acquisition, Google advancing Advanced Contextual features and AI Overviews integration, and Microsoft expanding Copilot capabilities within Microsoft Advertising platform, thereby leveraging existing customer relationships, data assets, and distribution infrastructure to capture contextual market share.

Key Market Developments

- August 2025: Kontext, a Czech-founded contextual advertising platform specializing in native ad insertion within generative AI chatbot conversations, completed US$ 10 Million seed round led by M13 with participation from Torch Capital, Credo Ventures, and Parable VC, positioning itself as a pioneering player in emerging chatbot monetization market where contextual ads appear naturally within conversational flows without disrupting user experience, already processing tens of millions of daily impressions for major brands including Amazon, Uber, and Canva.

- June 2025: Microsoft Advertising substantially expanded Copilot capabilities across campaign management dashboards, enabling advertisers to auto-generate creative variations, optimize targeting, and receive performance recommendations through conversational AI interface, with Daily active users growing significantly from November 2024 through May 2025 and user satisfaction rising 2% monthly throughout 2025, demonstrating strong market adoption of AI-augmented advertising platform features.

- November 2024: Peec AI, a London-based startup focused on "answer engine optimization" helping brands optimize performance within AI-powered search contexts including Perplexity and ChatGPT Search, secured US$ 21 Million Series A funding led by Lightspeed Venture Partners with participation from Seedcamp and firstminute capital, addressing critical business need for marketing professionals to optimize performance within emerging AI search environments representing fundamental shift in consumer search behaviors and advertising opportunities.

Companies Covered in Contextual Market

- Oracle Corporation

- SAP

- Microsoft Corporation

- Adobe Inc.

- Pelatro

- Intersec

- Flybits Inc.

- Comviva

- IBM

- Amazon

Frequently Asked Questions

The global Contextual market is projected to reach US$ 185.7 Billion in 2026 and is expected to expand to US$ 491.0 Billion by 2033, representing a robust 14.9% CAGR throughout the forecast period, with growth accelerating as organizations transition from third-party cookie dependencies toward privacy-first, regulatory-compliant marketing approaches increasingly enabled by advanced artificial intelligence and machine learning technologies.

Primary demand drivers include mandatory regulatory compliance with GDPR, CCPA, and emerging EU AI Act requirements that restrict personal data utilization in marketing contexts, creating business imperatives to adopt privacy-first strategies where contextual targeting delivers personalization without personal data reliance, alongside demonstrable performance advantages where contextual ads generate 50% higher click-through rates compared to non-contextual alternatives and integrate artificial intelligence capabilities enabling sophisticated real-time content analysis and hyper-targeted audience matching.

Retail & Consumer Packaged Goods commands the largest industry vertical with approximately 24% market share, driven by critical omnichannel personalization requirements, aggressive e-commerce expansion, and measurable performance gains where contextual recommendations deliver 25% sales increases, improved customer engagement, and enhanced customer lifetime value metrics, making Contextual solutions strategically essential for competitive positioning in saturated retail markets.

North America maintains dominant global market leadership with 38.2% market share, driven by advanced technological infrastructure, presence of major Contextual platform innovators including Google, Microsoft, Adobe, Oracle, and Amazon, mature regulatory frameworks facilitating privacy-first marketing innovation, sophisticated enterprise customer bases, and substantial digital transformation investment budgets establishing the region as the primary market for contextual solution adoption and continued technology advancement

Emerging opportunities include the rapidly expanding AI-powered chatbot advertising market, where contextual advertising solutions integrate native ads within conversational flows, combined with healthcare and BFSI vertical expansion where Contextual enables personalization while maintaining HIPAA and PCI-DSS compliance requirements, and Asia Pacific regional growth driven by extraordinary mobile penetration and e-commerce digitalization in India and Southeast Asia.

Major market leaders include technology infrastructure companies Google, Microsoft, Oracle, Adobe, SAP, and Amazon who control substantial market share through integrated platforms combining advertising networks and customer data capabilities, while specialized contextual intelligence providers including GumGum, Seedtag, Taboola, Outbrain, and emerging innovators like Kontext compete through superior contextual analysis capabilities and specialized vertical or channel expertise, establishing diverse competitive strategies within moderately consolidated market structures.