- HVAC

- Commercial Heating Equipment Market

Commercial Heating Equipment Market Size, Share, and Growth Forecast, 2026 - 2033

Commercial Heating Equipment Market by Product Type (Heat Pumps, Furnaces, Others), Fuel Type (Electric, Natural Gas, Others), End-user, Equipment Scale, and Regional Analysis for 2026 - 2033

Commercial Heating Equipment Market Size and Trends Analysis

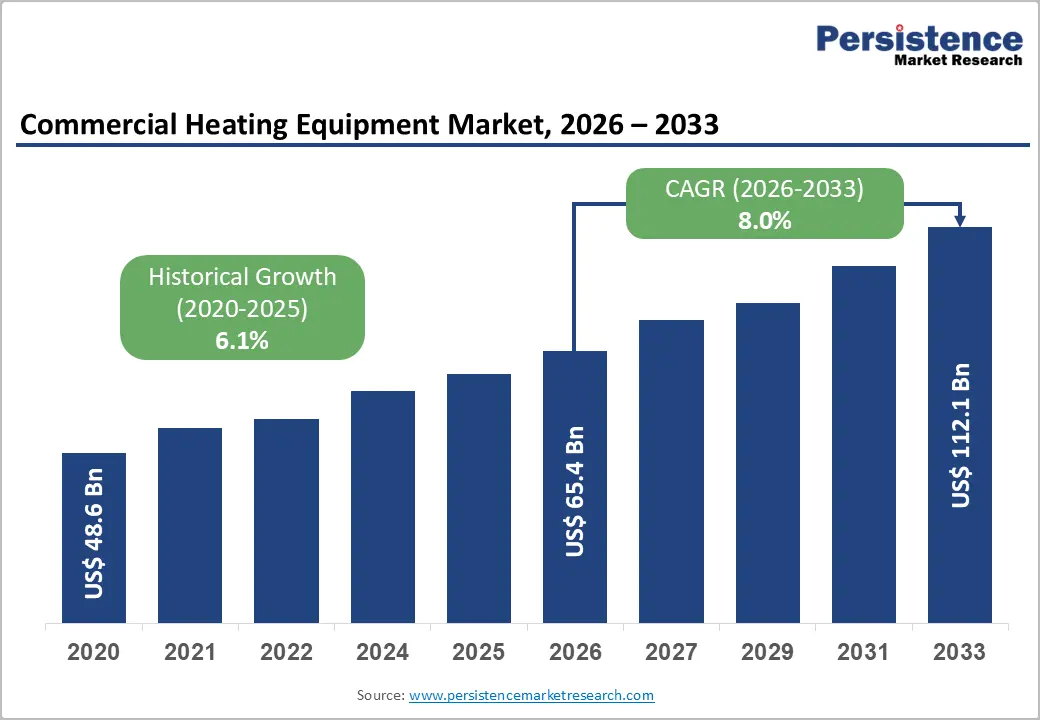

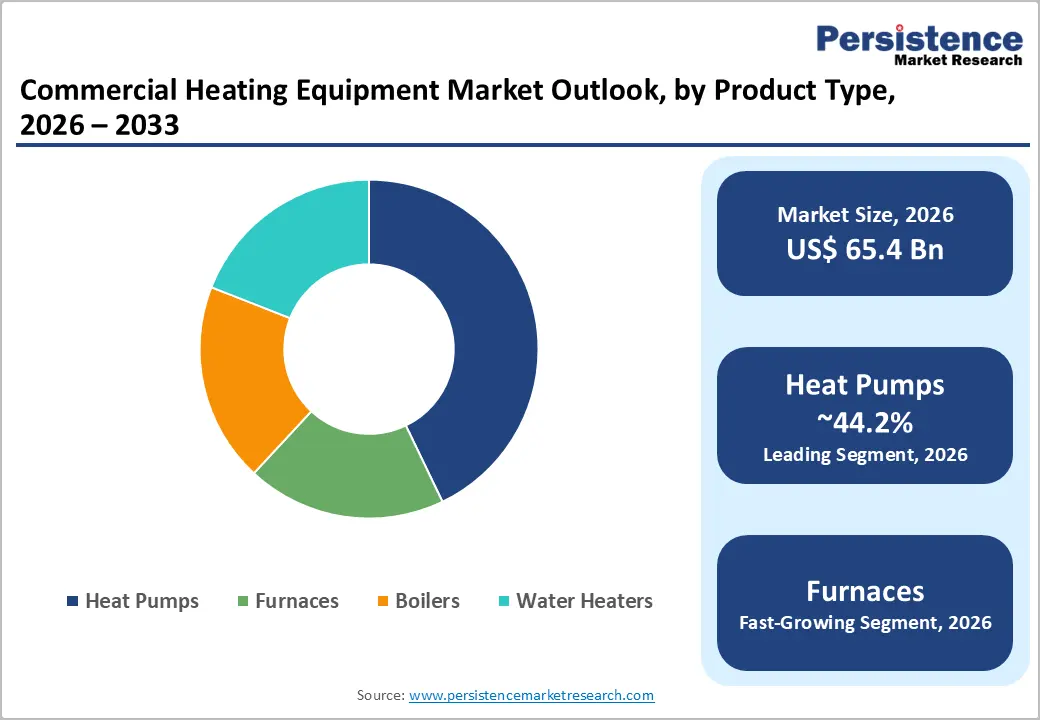

The global commercial heating equipment market size is likely to be valued at US$65.4 billion in 2026 and is expected to reach US$112.1 billion by 2033, growing at a CAGR of 8.0% between 2026 and 2033, driven by rising energy consumption in commercial buildings, strong retrofit activity, and increasing adoption of high-efficiency electric heating systems. Demand is supported by stricter energy regulations, rising energy costs, and aging infrastructure, pushing building owners to invest in cost-efficient, low-emission, and modern heating solutions.

Key Industry Highlights:

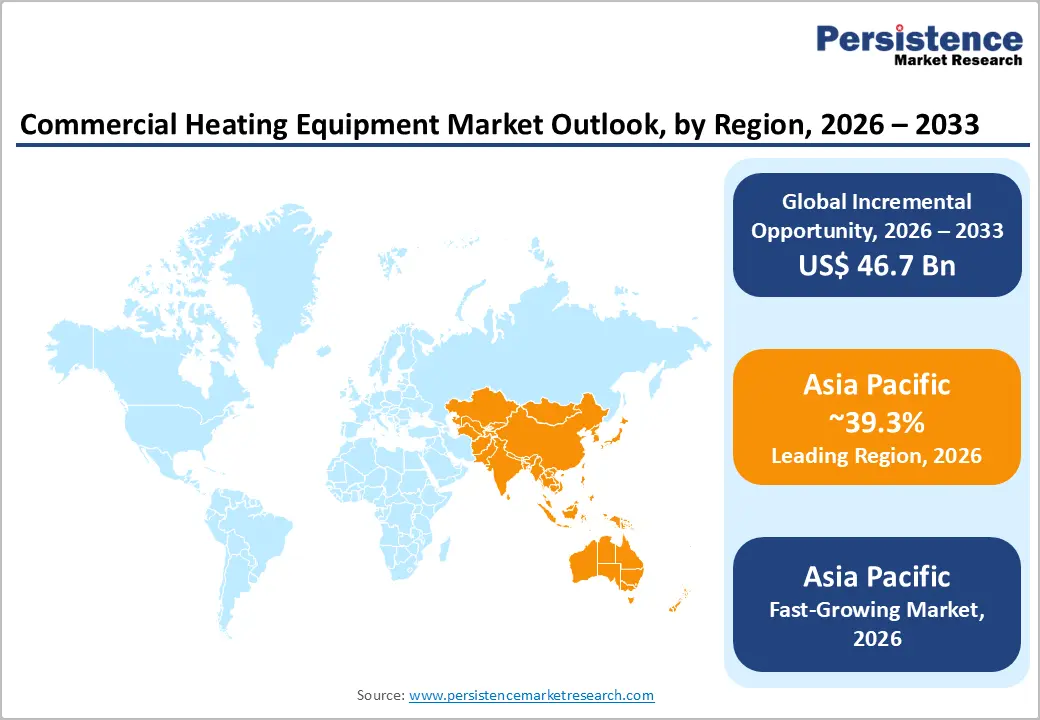

- Leading Region: Asia Pacific is projected to account for approximately 39.3% of the market share, supported by strong manufacturing capacity and rapid commercial infrastructure expansion.

- Fastest-growing Region: Asia Pacific is also expected to be the fastest-growing region, driven by urbanization, rising commercial construction, and increasing adoption of energy-efficient heating technologies across China, India, and Southeast Asia.

- Investment Plans: Significant investments are being directed toward electrification, heat pump manufacturing expansion, and smart building integration, with major companies focusing on regional production facilities and advanced low-emission technologies.

- Dominant Product Type: Heat pumps lead, anticipated to hold over 44.2% market share, driven by superior energy efficiency and strong alignment with global decarbonization goals.

- Leading Fuel Type: Electric systems are estimated to dominate with a 60.7% market share, reflecting the accelerating transition toward electrification and sustainable commercial heating solutions.

DRO Analysis

Driver - Electrification and Efficiency Regulations Accelerating Equipment Replacement

A key growth driver is the global shift toward the electrification of heating systems and stricter energy efficiency standards. Governments across North America and Europe are implementing regulatory frameworks that encourage or mandate the transition away from fossil fuel-based heating. Heat pumps, which deliver significantly higher efficiency compared to conventional gas boilers, are central to these policies.

In the U.S., updated efficiency standards for large commercial HVAC systems are pushing manufacturers and building owners toward advanced technologies. In Europe, long-term carbon-neutrality targets are driving the adoption of electric heating systems. These regulatory changes are transforming procurement strategies, with decision-making increasingly based on lifecycle cost, emissions exposure, and compliance readiness, rather than upfront capital expenditure. This shift is accelerating replacement demand across commercial building portfolios.

High Energy Consumption in Commercial Buildings Driving Retrofit Demand

Commercial buildings represent a substantial share of global energy consumption, making heating systems a major contributor to operating expenses. Older buildings, particularly in office, retail, healthcare, and hospitality segments, often rely on outdated and inefficient heating infrastructure. This creates a significant retrofit opportunity. Government-backed initiatives promoting energy-efficient upgrades are further strengthening this trend.

Programs aimed at accelerating the adoption of advanced heating technologies are encouraging building owners to invest in modern systems. The economic impact is significant, as improved heating efficiency can substantially reduce utility costs. As a result, retrofit projects are increasingly viewed as strategic investments to improve operating margins, rather than discretionary upgrades, which supports consistent demand growth.

Restraint - High Upfront Costs and Installation Complexity Limiting Adoption

Despite strong long-term benefits, the adoption of advanced commercial heating systems is constrained by high initial investment costs and complex installations. Retrofitting existing buildings often requires structural modifications, system integration, and temporary operational disruptions, all of which increase project costs and timelines. The availability of skilled installers and technical expertise also remains limited in several regions, leading to longer project cycles and higher labor costs.

In addition, fluctuations in energy prices and financing conditions can impact the economic attractiveness of new installations. These factors contribute to delayed capital expenditure decisions and extended payback periods, particularly among small and mid-sized commercial property owners. As a result, while demand fundamentals remain strong, execution challenges continue to moderate the pace of market expansion.

Opportunity - Expansion of High-Performance and Cold-Climate Heat Pump Technologies

Technological advancements in cold-climate and high-temperature heat pumps are creating a new wave of opportunities in the commercial heating market. These systems are designed to operate efficiently in extreme weather conditions and meet the heating requirements of large commercial spaces, making them suitable for a wider range of applications.

Manufacturers are investing in the development of next-generation rooftop heat pump systems that can be deployed in existing buildings with minimal disruption. This is particularly relevant for offices, retail spaces, educational institutions, and municipal buildings. As these technologies become more cost-effective and widely available, they are expected to unlock a significant portion of the retrofit market, driving long-term growth.

Integration of Smart Controls and Low-Emission Technologies

The integration of low-global-warming-potential refrigerants, smart building controls, and energy management systems is expanding the value proposition of commercial heating equipment. Modern systems are increasingly equipped with digital monitoring and automation capabilities, enabling real-time optimization of energy usage. These advancements allow building operators to achieve substantial reductions in both operating costs and carbon emissions.

The shift toward connected and intelligent heating systems is also creating opportunities for service-based business models, including predictive maintenance and performance optimization. This evolution is transforming the market from a product-centric model to a solution-oriented ecosystem, increasing overall market value and customer retention.

Category-wise Analysis

Product Type Insights

Heat pumps represent the leading product segment, anticipated to account for over 44.2% of the market share during the forecast period. Their dominance is driven by superior energy efficiency, the ability to provide both heating and cooling, and strong alignment with global decarbonization goals. Heat pumps are increasingly being adopted across commercial buildings such as office complexes, retail chains, and institutional facilities due to their compatibility with renewable energy sources and lower lifecycle operating costs.

Large manufacturers are actively expanding their commercial heat pump portfolios. For instance, Carrier Global Corporation has introduced advanced rooftop heat pump systems for large commercial buildings, while Daikin Industries Ltd. continues to scale its VRV (Variable Refrigerant Volume) heat pump solutions for commercial applications. Similarly, Trane Technologies is focusing on electrified rooftop units designed for retrofit projects. Their ability to replace multiple legacy systems with a single integrated solution makes heat pumps highly attractive, especially as regulatory pressures intensify, ensuring continued market leadership.

Furnaces are projected to be the fastest-growing segment, driven by efficiency upgrades and replacement demand in markets undergoing gradual electrification. A significant portion of existing commercial infrastructure still relies on combustion-based heating systems, creating consistent demand for high-efficiency furnace replacements.

Advanced furnace technologies now incorporate improved heat exchangers, modulating burners, and hybrid integration, offering better energy efficiency and lower emissions than older systems.

For example, Lennox International and Rheem Manufacturing Company have developed high-efficiency commercial furnace systems designed for large-scale applications. Growth is particularly strong in regions such as North America, where natural gas infrastructure is well established. This segment benefits from a phased transition strategy, where building owners prioritize incremental efficiency improvements before fully shifting to electrified systems.

Fuel Type Insights

Electric heating systems are projected to dominate the market, maintaining a leading share of approximately 60.7% throughout the forecast period. This leadership reflects the accelerating global shift toward electrification and sustainability. Electric systems are widely adopted due to their seamless compatibility with heat pumps, integration with smart building controls, and alignment with environmental regulations.

Technological advancements in electric heating solutions, including intelligent energy management systems and grid-responsive controls, further strengthen their adoption. Companies such as Mitsubishi Electric Corporation and Panasonic Corporation are developing advanced electric heating and heat pump systems tailored for commercial applications. These systems reduce direct carbon emissions and enable buildings to transition to renewable energy, reinforcing their long-term market dominance.

Natural gas is expected to be the fastest-growing fuel type in transition markets, with a steady growth trajectory driven by replacement demand and the availability of infrastructure. Its cost competitiveness and widespread distribution networks make it a preferred short- to medium-term solution for many commercial building operators.

For example, A. O. Smith Corporation and Viessmann Group continue to offer advanced gas-fired boilers and hybrid heating systems that improve efficiency while reducing emissions. These solutions are particularly relevant in regions where immediate electrification is constrained by grid capacity or cost considerations. Natural gas is expected to play a transitional role, with demand largely driven by replacement cycles and gradual integration of hybrid systems that combine gas and electric technologies.

Regional Insights

North America Commercial Heating Equipment Market Trends - Retrofit-Driven Demand and Shift toward Electrified High-Efficiency HVAC

North America is a mature yet innovation-driven market, with the U.S. leading in terms of demand and technological advancement. The region benefits from a large installed base of commercial buildings, many of which require system upgrades or replacements. This has created a strong pipeline for retrofit-driven demand, particularly across office buildings, retail chains, and institutional facilities.

Regulatory frameworks play a critical role in shaping market dynamics. Updated efficiency standards for commercial HVAC systems are pushing manufacturers toward high-performance products, while emissions regulations are encouraging the transition to cleaner technologies. This shift is clearly reflected in recent industry developments. For instance, Carrier Global Corporation introduced its next-generation WeatherMaster rooftop units using lower global warming potential refrigerants, aligning with regulatory requirements and accelerating the adoption of sustainable systems.

Trane Technologies has also expanded its electrification-focused product portfolio, targeting retrofit projects across U.S. commercial buildings. These developments are reinforcing a transition toward high-efficiency, electrified heating solutions.

The presence of major industry players strengthens the region’s competitive landscape, fostering continuous innovation and product development. Johnson Controls International has actively deployed smart building solutions, integrating heating systems with digital controls to improve energy efficiency and lifecycle performance. However, adoption rates vary depending on energy prices, financing conditions, and the availability of skilled labor. Despite these challenges, ongoing investments in electrification and building modernization ensure that North America remains a key market for advanced commercial heating solutions.

Europe Commercial Heating Equipment Market Trends - Policy-Driven Heat Pump Adoption and Commercial Heating Decarbonization

Europe is characterized by strong regulatory support for energy efficiency and decarbonization, making it one of the most policy-driven markets globally. Policies aimed at reducing carbon emissions are accelerating the adoption of electric heating systems, particularly heat pumps. Countries, such as Germany, France, the U.K., and Spain, are leading this transition, supported by subsidies, carbon pricing mechanisms, and building efficiency mandates.

Recent developments highlight how manufacturers are aligning with these regulatory trends. Daikin Industries Ltd. has significantly expanded its European heat pump production capacity to meet rising demand, particularly for commercial and district heating applications. Similarly, Viessmann Group has strengthened its portfolio of hybrid and electric heating solutions tailored for European commercial buildings, enabling smoother transitions from gas-based systems. These investments directly support regional decarbonization goals while improving access to technology.

The region’s market is heavily influenced by government incentives, energy pricing, and infrastructure readiness. While growth remains strong, short-term fluctuations have been observed due to economic conditions and policy adjustments, including variations in subsidy structures and energy costs. High installation costs and workforce constraints also present challenges. However, Europe continues to serve as a critical innovation hub, particularly in district heating integration and low-emission technologies. Ongoing investments by both governments and private players are expected to sustain long-term growth and technology advancement.

Asia Pacific Commercial Heating Equipment Market Trends - Large-Scale HVAC Manufacturing and Rapid Urban Infrastructure Expansion

Asia Pacific is the largest and fastest-growing regional market, accounting for approximately 39.3% of the global share. Rapid urbanization, expanding commercial infrastructure, and strong manufacturing capabilities are the key drivers of growth. The region’s scale and cost advantages make it central to both production and consumption of commercial heating equipment.

China dominates both the manufacturing and deployment sectors. Companies such as Midea Group have expanded large-scale production of commercial HVAC and heat pump systems, enabling cost-effective supply across domestic and export markets. At the same time, Daikin Industries Ltd. continues to invest in regional manufacturing and R&D, strengthening its presence in China and Southeast Asia. These developments are enhancing regional supply chains while making advanced heating technologies more accessible.

Japan remains a leader in advanced and energy-efficient heating solutions, with companies like Mitsubishi Electric Corporation focusing on high-performance commercial heat pump and VRF systems. In India and Southeast Asia, rising commercial construction activity and infrastructure development are driving demand for scalable and cost-efficient heating solutions. Increasing adoption of smart and energy-efficient systems in urban commercial spaces is further accelerating market growth.

The region’s strong manufacturing base, combined with increasing investments in commercial real estate and infrastructure, is positioning Asia Pacific as a global hub for heating equipment innovation and production. As a result, it is expected to maintain its leadership position throughout the forecast period.

Competitive Landscape

The global commercial heating equipment market is moderately fragmented, with a mix of global manufacturers and regional players. Leading companies compete across multiple product categories, including heat pumps, boilers, and integrated HVAC systems. Competition is driven by product innovation, energy efficiency, and service capabilities. Companies with comprehensive portfolios and strong distribution networks are better positioned to capture market share. The market structure encourages continuous innovation while maintaining competitive pricing dynamics.

Key players are focusing on electrification, sustainability, digital integration, and geographic expansion. Emphasis is placed on developing energy-efficient products, adopting environmentally friendly refrigerants, and offering integrated solutions that combine equipment with digital services and lifecycle support.

Key Industry Developments:

- In November 2025, Johnson Controls International showcased next-generation HVAC systems, including high-efficiency chillers and advanced building automation platforms, at HVACR World 2025, emphasizing integrated solutions that reduce energy consumption and enable smart building operations.

Companies Covered in Commercial Heating Equipment Market

- Carrier Global Corporation

- Trane Technologies

- Johnson Controls International

- Daikin Industries Ltd.

- Lennox International

- Mitsubishi Electric Corporation

- Panasonic Corporation

- Viessmann Group

- Midea Group

- Rheem Manufacturing Company

- O. Smith Corporation

- Modine Manufacturing Company

- Bosch Thermotechnology

- Vaillant Group

- Ariston Holding N.V.

- Fujitsu General Limited

Frequently Asked Questions

The global commercial heating equipment market is valued at US$65.4 billion in 2026.

The commercial heating equipment market is projected to reach US$112.1 billion by 2033.

Key trends include the rapid adoption of heat pumps, increasing shift toward electric-based heating systems, integration of smart building technologies, and growing investments in low-emission and energy-efficient solutions. Retrofit demand across aging commercial infrastructure is also a major trend shaping the market.

Heat pumps are the leading segment, anticipated to account for over 44.2% of the market share, due to their high efficiency and ability to provide both heating and cooling.

The commercial heating equipment market is expected to grow at a CAGR of 8.0% between 2026 and 2033.

Major players include Carrier Global Corporation, Trane Technologies, Daikin Industries Ltd., Johnson Controls International, and Mitsubishi Electric Corporation.