- HVAC

- Steam Trap Monitor Market

Steam Trap Monitor Market Size, Share, and Growth Forecast, 2026 - 2033

Steam Trap Monitor Market by Function (Monitoring, Diagnostics, Others), Trap Types (Mechanical Traps, Orifice Traps, Others), End-user Industry (Pharmaceutical, Oil & Gases, Others), and Regional Analysis 2026 - 2033

Steam Trap Monitor Market Size and Trends Analysis

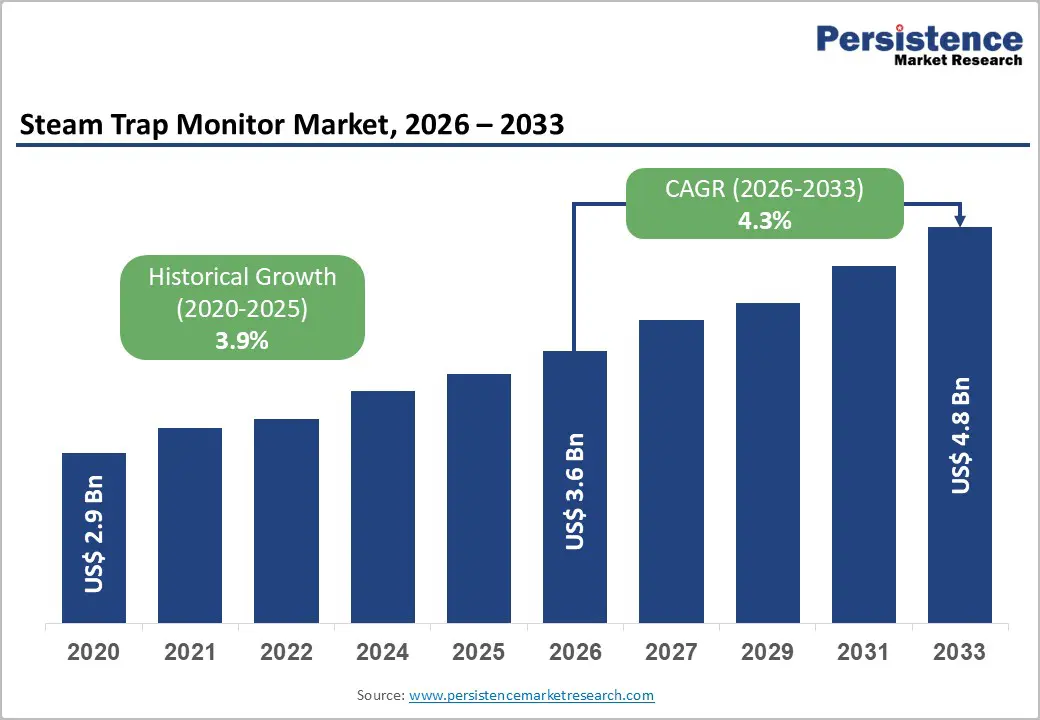

The global steam trap monitor market size is likely to be valued at US$3.6 billion in 2026 and is expected to reach US$4.8 billion by 2033, growing at a CAGR of 4.3% during the forecast period from 2026 to 2033, driven by a global industrial shift toward carbon neutrality and the widespread integration of Industrial Internet of Things (IIoT) technologies.

Industrial facilities are increasingly moving away from manual, periodic audits of trap failures toward real-time, wireless monitoring solutions that ensure continuous thermal efficiency. Furthermore, the rising cost of energy and stringent environmental mandates from bodies such as the International Energy Agency (IEA) are forcing manufacturers to adopt precision monitoring to mitigate the substantial economic losses associated with "failed-open" traps.

Key Industry Highlights:

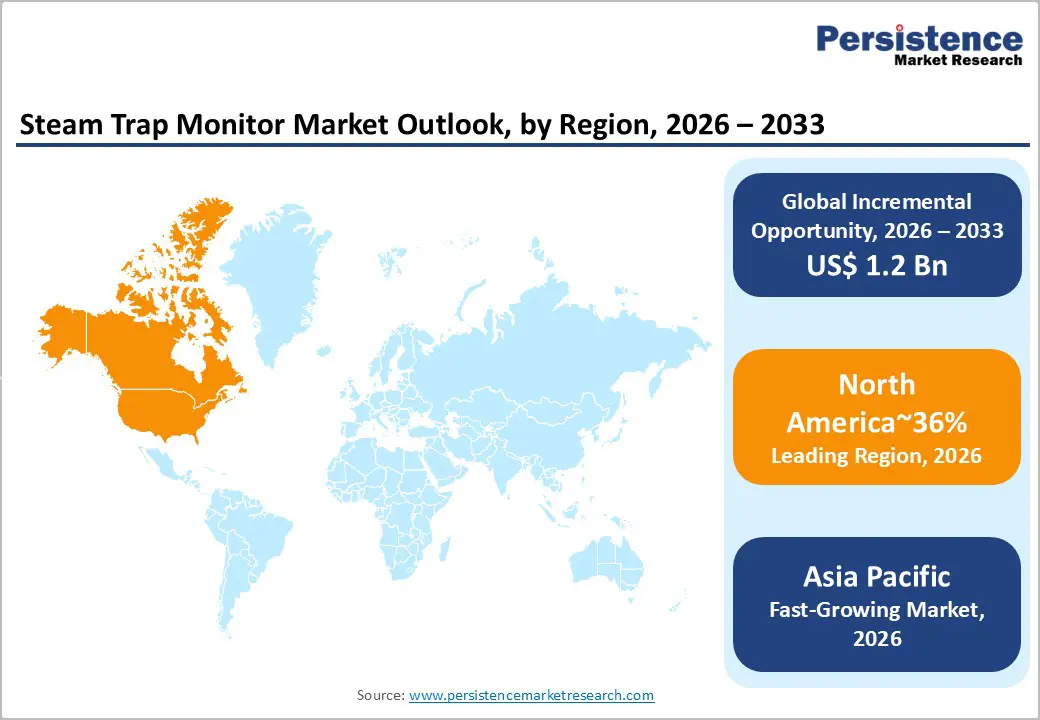

- Leading Region: North America is projected to lead due to advanced industrial infrastructure, strong automation adoption, and stringent energy efficiency regulations, accounting for approximately 36% share in 2026, supported by widespread deployment of IIoT-enabled monitoring systems and strong vendor ecosystems.

- Fastest-Growing Region: Asia Pacific is anticipated to grow fastest due to rapid industrial expansion, supportive manufacturing policies, and increasing adoption of smart factory technologies across energy-intensive industries.

- Leading Trap Type: Mechanical traps are expected to lead, accounting for approximately 46% share in 2026 through extensive industrial adoption, reliable condensate handling performance, and strong presence across refining, chemical processing, and heavy manufacturing operations.

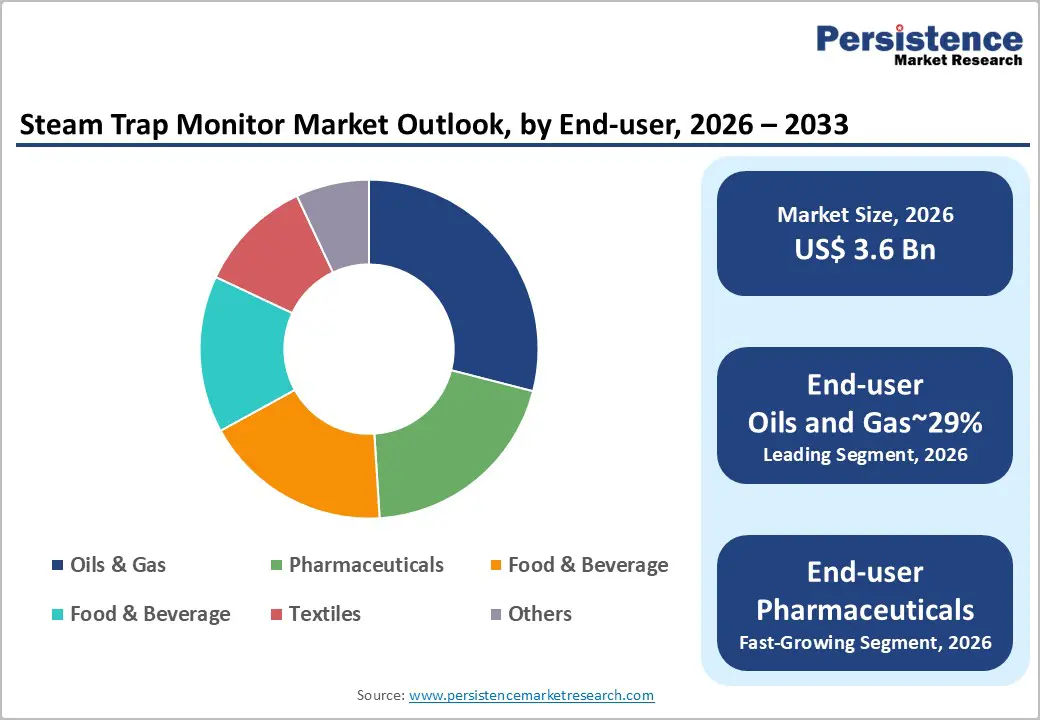

- Leading End-user: Oil & gas is projected to dominate due to its critical dependence on steam for refining, distillation, and heat tracing operations, holding approximately 29% share in 2026 across large-scale industrial utility networks.

| Key Insights | Details |

|---|---|

|

Steam Trap Monitor Market Size (2026E) |

US$3.6 Bn |

|

Market Value Forecast (2033F) |

US$4.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Escalating Industrial Energy Efficiency Regulations Accelerating Steam Trap Monitoring Adoption

Escalating industrial energy efficiency mandates are intensifying the need for continuous monitoring of steam distribution infrastructure across process industries. Steam systems represent critical energy carriers within refineries, chemical plants, and manufacturing facilities, where leakages materially erode operational efficiency and thermal balance. Unmonitored steam traps allow persistent losses that elevate fuel consumption and emissions across centralized boiler networks. Regulatory frameworks targeting decarbonization and industrial efficiency increasingly require verifiable performance monitoring across energy-intensive utility systems. Compliance mechanisms embedded within regional energy legislation emphasize measurable reductions in thermal waste and emissions intensity. These mandates elevate monitoring instrumentation from optional maintenance tools into integral components of plant energy governance structures.

Energy management certification frameworks are reinforcing the strategic importance of automated steam trap monitoring technologies across industrial utility networks. Standardized energy governance protocols require continuous data capture to verify system performance and identify efficiency deviations. Monitoring platforms generate operational intelligence that supports auditing, reporting, and regulatory verification within structured energy management programs. Integration with digital plant monitoring systems strengthens visibility across steam infrastructure while enabling predictive maintenance interventions. This transition aligns operational maintenance practices with broader corporate decarbonization and resource optimization commitments. As regulatory scrutiny intensifies, industrial operators increasingly prioritize monitoring systems that deliver auditable efficiency insights.

Industrial IoT Convergence and Predictive Analytics Enhancing Steam System Reliability

The integration of industrial internet technologies is transforming steam infrastructure monitoring across energy-intensive industrial environments. Modern steam trap monitoring platforms combine wireless sensing architectures with intelligent analytics capabilities embedded within industrial automation frameworks. Continuous acquisition of acoustic, thermal, and pressure signatures allows early identification of malfunctioning traps before operational failure occurs. These systems replace manual inspection routines with automated diagnostics that enhance operational transparency across complex steam networks. Real-time monitoring strengthens asset visibility while reducing unplanned shutdown risks within refinery, chemical, and manufacturing operations. Predictive analytics engines interpret sensor signals to forecast degradation patterns and maintenance intervention windows. This digital transformation aligns steam management practices with broader smart manufacturing strategies focused on reliability and efficiency.

Technological convergence between wireless instrumentation and predictive analytics is reshaping maintenance economics within industrial steam utilities. Advanced monitoring systems integrate with enterprise asset management platforms to create centralized operational intelligence across plant utilities. Continuous diagnostics reduce dependency on labor-intensive manual inspections traditionally required for trap condition verification. Preventing undetected failures mitigates risks such as condensate accumulation and destructive pressure fluctuations within piping networks. These operational safeguards protect high-value process equipment from mechanical stress and performance disruptions. Integration with sustainability and energy governance programs further strengthens the business case for digital monitoring infrastructure.

Barrier Analysis - Elevated Capital Investment Requirements Limiting Adoption of Steam Trap Monitoring Infrastructure

High upfront capital expenditure requirements represent a significant constraint on widespread deployment of automated steam trap monitoring systems across industrial facilities. While conventional steam traps remain relatively inexpensive components within utility infrastructure, advanced monitoring architectures require substantial investment in sensors, wireless communication modules, gateways, and centralized analytics platforms. Large facilities operating extensive steam distribution networks must deploy hundreds of monitoring nodes to achieve comprehensive system visibility. This infrastructure requirement substantially elevates procurement budgets and lengthens capital approval cycles within cost-sensitive industrial environments. Facilities operating under strict operational budgets frequently defer modernization initiatives despite recognized efficiency losses. Consequently, many plants continue relying on periodic manual inspections that provide limited operational visibility across complex steam networks.

Integration complexity further compounds capital expenditure barriers associated with digital monitoring infrastructure across established industrial utility systems. Retrofitting monitoring sensors into legacy steam networks often requires communication gateways, data management platforms, and compatibility with plant automation systems. These integration requirements increase implementation timelines while introducing additional engineering and configuration costs. Organizations must also allocate resources for system calibration, workforce training, and digital maintenance management processes. Such operational adjustments create perceived implementation risk among facilities lacking prior experience with industrial internet technologies. Budget holders, therefore, evaluate monitoring investments cautiously against competing capital priorities within plant modernization programs. These financial and operational considerations collectively restrain near-term adoption of advanced steam monitoring solutions.

Workforce Skill Gaps Constraining Effective Utilization of Advanced Monitoring Technologies

A shortage of specialized technical expertise is constraining the effective deployment and utilization of advanced steam trap monitoring systems across industrial environments. Although automated alerts and digital diagnostics simplify failure detection, interpreting complex operational datasets still requires trained technical personnel. Wireless monitoring infrastructures generate continuous acoustic and thermal signals that must be evaluated within established engineering thresholds. Industrial operators lacking experience in digital instrumentation often struggle to translate these signals into actionable maintenance decisions. This capability gap reduces operational confidence in automated monitoring platforms despite their efficiency advantages. Facilities, therefore, hesitate to expand digital monitoring infrastructure without parallel investments in workforce capability development. The absence of skilled technicians consequently slows operational integration of advanced steam diagnostics across many industrial regions.

The maintenance of wireless sensor networks and calibration of diagnostic monitoring parameters introduces additional operational complexity within plant utility management systems. Monitoring platforms rely on precise threshold configuration to distinguish normal operating signatures from early failure conditions. Improper calibration or misinterpretation of diagnostic signals can reduce monitoring accuracy and undermine system credibility among plant engineers. Organizations must therefore maintain personnel capable of managing sensor reliability, communication stability, and data validation processes. Many industrial regions face persistent shortages of technicians trained in digital instrumentation and industrial analytics. This workforce imbalance weakens the economic justification for monitoring investments within facilities lacking advanced technical capabilities.

Opportunity Analysis - Expansion of AI-Enabled Diagnostic Platforms within Industrial Steam Monitoring Systems

The expansion of artificial intelligence-driven diagnostics is creating a significant opportunity within the evolving steam trap monitoring ecosystem. Advanced monitoring platforms increasingly incorporate machine learning algorithms capable of interpreting acoustic, thermal, and pressure signatures within steam distribution networks. These analytical capabilities enable predictive detection of trap malfunctions before operational disruptions occur within energy-intensive facilities. Integration with connected industrial sensor networks strengthens real-time asset visibility across complex steam infrastructure. This transition transforms monitoring systems from passive detection tools into intelligent operational analytics platforms. Industrial operators gain earlier intervention capabilities that reduce energy losses and protect critical process equipment. As digital industrialization accelerates, AI-enabled diagnostics are emerging as a strategic layer within smart utility management architectures.

Rising regulatory scrutiny around process integrity and energy efficiency is amplifying demand for intelligent diagnostic capabilities across industrial sectors. Industries with stringent operational controls increasingly prioritize monitoring technologies capable of continuous performance verification. Pharmaceutical manufacturing environments represent a particularly significant opportunity due to strict sterilization and process validation requirements. Reliable steam system diagnostics support compliance documentation and strengthen quality assurance frameworks within regulated production facilities. Integration of monitoring analytics with plant automation and asset management software further expands operational value. These capabilities enable coordinated maintenance strategies while strengthening infrastructure reliability across utility networks.

Infrastructure Retrofitting Across Mature Industrial Steam Networks

The modernization of aging industrial infrastructure across established manufacturing regions presents a substantial opportunity for steam trap monitoring technologies. Numerous chemical, petrochemical, and process manufacturing facilities continue operating legacy steam distribution systems installed several decades earlier. These infrastructures often lack continuous monitoring mechanisms capable of identifying trap failures and energy losses. Retrofitting programs increasingly prioritize non-intrusive monitoring devices that can be installed without disrupting critical plant operations. Clamp-on sensor configurations allow operators to introduce digital diagnostics while preserving existing piping architectures. This retrofit pathway offers an efficient mechanism for improving steam system visibility without extensive mechanical redesign. Consequently, monitoring technologies are emerging as practical tools for upgrading legacy industrial utility networks.

Sustainability governance frameworks are further accelerating retrofit initiatives across mature industrial hubs seeking measurable energy performance improvements. Corporate environmental accountability programs require transparent documentation of emissions reduction and energy efficiency measures. Monitoring platforms provide continuous operational intelligence that supports internal sustainability reporting and regulatory compliance verification. Low-disruption installation models appeal to facilities seeking modernization without extended shutdown periods or major capital reconstruction. Retrofitting monitoring infrastructure, therefore, aligns operational efficiency objectives with environmental performance commitments. Industrial operators view such upgrades as pragmatic strategies to optimize existing steam assets while addressing decarbonization pressures.

Category-wise Analysis

Trap Type Insights

Mechanical traps are anticipated to lead, accounting for approximately 46% share in 2026, supported by their entrenched role within high-pressure industrial steam infrastructure. Their float and inverted bucket architectures reliably manage large condensate volumes across oil refining, chemical processing, and heavy manufacturing operations. Industrial facilities prioritize these configurations because they deliver stable condensate discharge and predictable performance under fluctuating thermal loads. Monitoring ecosystems are therefore most developed around mechanical units, reflecting decades of installed base and maintenance familiarity. Technology vendors, including Emerson Electric, Spirax Group, TLV Co., Ltd., and Armstrong International, integrate wireless diagnostics with mechanical trap portfolios, embedding sensors, ultrasonic detection, and predictive analytics within enterprise asset management environments.

Orifice traps are expected to be the fastest-growing segment in the Steam Trap Monitor market, driven by rising demand for low-maintenance steam management architectures across regulated industrial operations. These traps eliminate moving mechanical components, enabling stable long-term operation within high pressure and high-pressure utility steam systems. Advancements in monitoring technologies allow ultrasonic sensors and digital analytics to detect subtle changes in orifice flow signatures, addressing historical sizing limitations. Manufacturers, including Thermal Energy International, Spirax Group, TLV Co., Ltd., and Armstrong International, are introducing monitored orifice platforms integrated with wireless connectivity and predictive diagnostics. As intelligent monitoring resolves earlier performance constraints, the adoption of monitored orifice traps is accelerating across continuous process industries.

End-user Industry Insights

Oil & Gas is expected to lead, accounting for approximately 29% share in 2026, supported by its entrenched dependence on steam-driven industrial processes. Refineries and petrochemical complexes rely extensively on steam for distillation, heat tracing, process heating, and thermal energy distribution across large processing units. These operations require continuous condensate management to maintain stable temperature control and operational safety in high-pressure environments. Steam trap monitoring systems, therefore, become critical infrastructure for detecting leaks, preventing energy loss, and maintaining process reliability. Technology providers, including Emerson Electric, Spirax Group, Armstrong International, and TLV Co., Ltd., integrate wireless diagnostics and predictive analytics platforms tailored for refinery utilities. Their monitoring ecosystems connect directly with plant automation and asset management software, reinforcing enterprise-wide steam management visibility.

Pharmaceuticals are expected to be the fastest-growing segment, driven by the sector’s stringent requirements for sterile steam and validated thermal processes. Pharmaceutical production relies heavily on controlled steam environments for sterilization, clean steam generation, and temperature-regulated manufacturing workflows. Manufacturers are rapidly transitioning toward automated monitoring platforms capable of real-time diagnostics and high-frequency condition tracking. Technology suppliers such as Spirax Group, Emerson Electric, Armstrong International, TLV Co., Ltd., and Forbes Marshall are introducing specialized monitoring systems designed for sterile manufacturing environments. Integration with digital plant systems enables continuous verification of steam performance parameters during critical operations.

Regional Insights

North America Steam Trap Monitor Market Trends

North America is expected to remain the leading regional market, approximating 36% share in 2026, supported by deep industrial infrastructure and advanced automation ecosystems. The region’s positioning is reinforced by the concentration of global technology vendors specializing in industrial monitoring platforms and integrated asset management systems. High penetration of refinery, petrochemical, and process manufacturing facilities is anticipated to sustain structural demand for continuous steam system diagnostics. Industrial operators increasingly prioritize predictive monitoring architectures that combine wireless sensors, cloud analytics, and enterprise asset management software to maintain operational reliability. Emerson Electric, Honeywell International, Armstrong International, and Spirax Group are positioned to reinforce regional dominance through expanded digital monitoring ecosystems and IIoT-enabled diagnostics. Growing integration of digital twins, cybersecurity-focused wireless networks, and cloud-based energy management platforms is expected to deepen enterprise adoption.

The U.S. is expected to function as the central anchor shaping North America’s market trajectory, driven by the scale of its refinery, chemical processing, and industrial manufacturing base. Industrial corridors across Texas and Louisiana are projected to sustain large-scale modernization programs targeting aging steam infrastructure and energy efficiency optimization. Federal manufacturing modernization initiatives and industrial decarbonization frameworks are anticipated to strengthen the adoption of intelligent monitoring systems capable of supporting emissions reporting and operational transparency. This shift toward service-oriented digital monitoring architectures is positioned to expand lifecycle value while strengthening long-term vendor integration within enterprise steam management operations across North American industrial facilities.

Asia Pacific Steam Trap Monitor Market Trends

Asia Pacific is expected to register the fastest growth trajectory, supported by accelerating industrialization and large-scale manufacturing expansion across emerging economies. The region’s market momentum is anticipated to be shaped by rapid capacity additions in chemical processing, power generation, and refining industries requiring efficient steam management infrastructure. Industrial facilities across major manufacturing corridors are increasingly integrating wireless monitoring platforms and predictive diagnostics to reduce steam losses and optimize plant energy utilization. Global and regional vendors, including Emerson Electric, Spirax Group, Forbes Marshall, and TLV Co., Ltd., are expected to intensify investment in localized manufacturing, training ecosystems, and digital monitoring platforms tailored for dense industrial installations. Rising adoption of Industry-driven automation frameworks and AI-enabled maintenance analytics is projected to deepen enterprise demand.

China is expected to function as the principal anchor shaping Asia Pacific’s market trajectory, supported by the scale of its chemical, power generation, and heavy manufacturing sectors. Industrial modernization programs are anticipated to prioritize energy efficiency optimization and digital plant infrastructure within large-scale processing facilities. National initiatives promoting industrial digitization and low-emission manufacturing are projected to accelerate the deployment of connected monitoring systems capable of providing continuous steam performance diagnostics. Industrial solution providers in China are increasingly aligning their regional strategies around localized production hubs, advanced wireless monitoring technologies, and integrated asset performance platforms. This alignment between manufacturing expansion, industrial policy, and technology adoption is expected to position China as the primary engine sustaining Asia Pacific’s high-growth trajectory within the global steam monitoring ecosystem.

Europe Steam Trap Monitor Market Trends

Europe is expected to remain a mature and structurally stable regional market, shaped by stringent sustainability frameworks and a highly optimized industrial base. The region’s market dynamics are anticipated to emphasize efficiency upgrades, lifecycle optimization, and digital monitoring enhancements rather than large-scale infrastructure expansion. High industrial energy costs across European manufacturing clusters are expected to reinforce enterprise demand for continuous steam monitoring solutions capable of minimizing thermal losses. Leading vendors, including Spirax Group, Emerson, Gestra AG, and ARI-Armaturen, are positioned to strengthen adoption through advanced monitoring platforms integrating acoustic diagnostics, private cloud analytics, and predictive maintenance capabilities. This replacement-driven demand environment is likely to sustain Europe’s position as a technologically sophisticated but structurally stable market within the global steam monitoring ecosystem.

Germany is expected to function as the primary anchor shaping Europe’s market trajectory, supported by its dense concentration of chemical manufacturing clusters and energy-intensive industrial operations. Industrial corridors along the Rhine region are projected to continue prioritizing modernization programs targeting aging steam infrastructure and operational efficiency optimization. European regulatory frameworks governing emissions reduction and energy auditing are anticipated to strengthen the integration of automated monitoring technologies within plant utility systems. This alignment between industrial policy, vendor innovation strategies, and enterprise energy management initiatives is expected to reinforce Germany’s central role in sustaining Europe’s mature yet technologically progressive steam trap monitoring landscape.

Competitive Landscape

The global steam trap monitor market is moderately consolidated, with leadership concentrated among global engineering and industrial automation suppliers such as Spirax-Sarco Engineering, Emerson Electric, Armstrong International, TLV International, and Watts Water Technologies, while a wide base of regional sensor manufacturers and engineering firms supports the broader ecosystem. These leading companies shape the competitive landscape through their established thermal engineering expertise, extensive installed equipment base, and integration of monitoring technologies within broader plant automation and energy management platforms.

The influence of major vendors extends beyond hardware supply, as they increasingly control system-level steam management strategies within energy-intensive industrial facilities. Their competitive positioning is defined by a combination of proprietary acoustic monitoring technologies, integrated asset management software, and lifecycle service capabilities tailored for complex industrial environments. Regional engineering firms continue to serve localized industrial markets, particularly across Asia, where specialized installation expertise and cost-efficient monitoring solutions sustain a fragmented supplier base alongside the global leaders.

Key Industry Developments:

- In January 2026, Armstrong International announced the 2026 expansion of its Herstal facility as a "sustainable factory." This facility will serve as a global test bench for high-temperature heat pumps and advanced steam diagnostic technologies.

- In January 2025, Armstrong International completed the acquisition of HygroTemp (Netherlands) to expand thermal solutions. The integration of HygroTemp’s sensing technologies directly enhances Armstrong's smart steam trap monitoring portfolio.

Companies Covered in Steam Trap Monitor Market

- Spirax-Sarco Engineering plc

- Emerson Electric Co.

- Armstrong International Inc.

- TLV Co. Ltd.

- Honeywell International Inc.

- Forbes Marshall Pvt. Ltd.

- Thermax Ltd.

- Gestra AG

- Flowserve Corp.

- Siemens AG

- Parker Hannifin Corp.

- Watts Water Technologies, Inc.

- Yokogawa Electric Corp.

- Valmet Corp.

- Pentair plc

- UE Systems Inc.

Frequently Asked Questions

The global steam trap monitor market is projected to be valued at US$3.6 billion in 2026 and is expected to reach US$4.8 billion by 2033, supported by increasing industrial emphasis on energy efficiency, emissions monitoring, and the integration of digital diagnostics within steam utility infrastructure.

Industrial energy efficiency mandates increasingly require continuous verification of thermal performance within process infrastructure. Steam trap monitoring systems provide real-time diagnostics that identify leaks, condensate accumulation, and failed-open traps that can significantly elevate fuel consumption and emissions. As regulatory frameworks emphasize measurable reductions in thermal losses, automated monitoring technologies are becoming integral components of industrial energy governance and compliance reporting systems.

The steam trap monitor market is forecast to grow at a CAGR of 4.3% from 2026 to 2033, reflecting steady adoption across energy-intensive industries as companies transition from manual inspection programs to automated wireless monitoring and predictive maintenance architectures.

North America is the leading regional market, accounting for approximately 36% share, supported by a large installed base of refinery, chemical processing, and manufacturing infrastructure. Strong adoption of industrial automation platforms, predictive maintenance systems, and IIoT-enabled monitoring technologies further reinforces the region’s leadership in advanced steam management solutions.

The market is moderately consolidated, with key players including Spirax-Sarco Engineering, Emerson Electric, Armstrong International, TLV Co., Ltd., and Watts Water Technologies. These companies compete through integrated steam management solutions, predictive monitoring technologies, and long-standing engineering expertise in industrial thermal systems.