- HVAC

- Glass Interposers Market

Glass Interposers Market Size, Share, and Growth Forecast, 2026 - 2033

Glass Interposers Market By Product Type (2D Glass Interposers, Thick Glass Interposers, Others), Substrate Technology (Through-Glass Vias (TGV), Glass Panel Level Packaging (PLP), Others), Packaging Architecture, End-use Industry, and Regional Analysis for 2026 - 2033

Glass Interposers Market Size and Trends Analysis

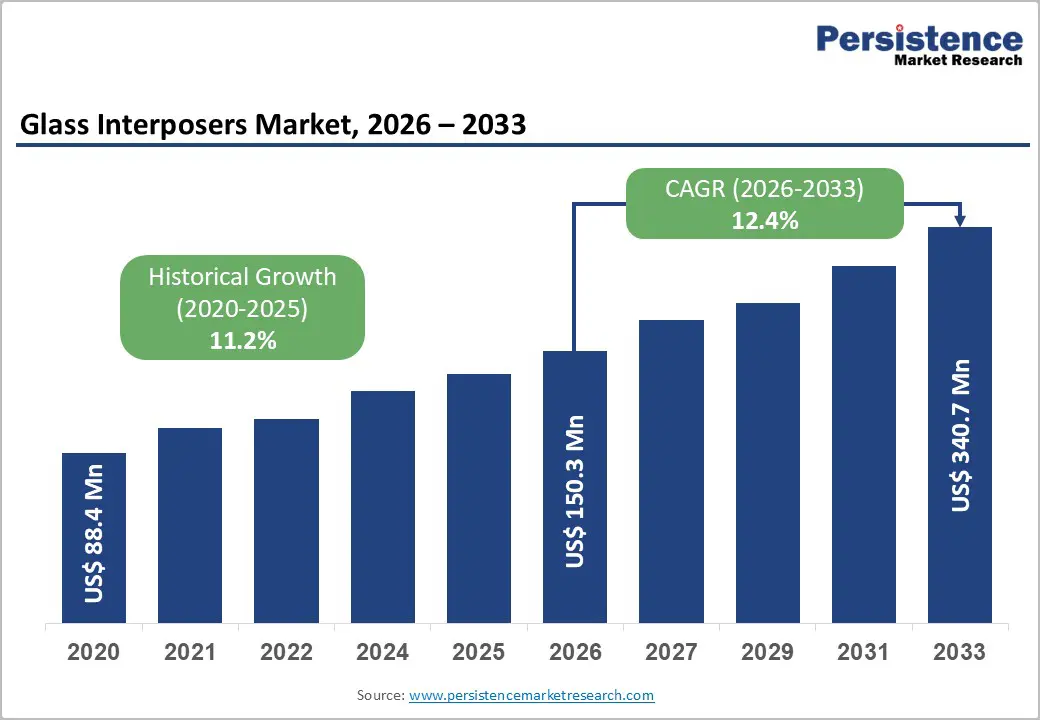

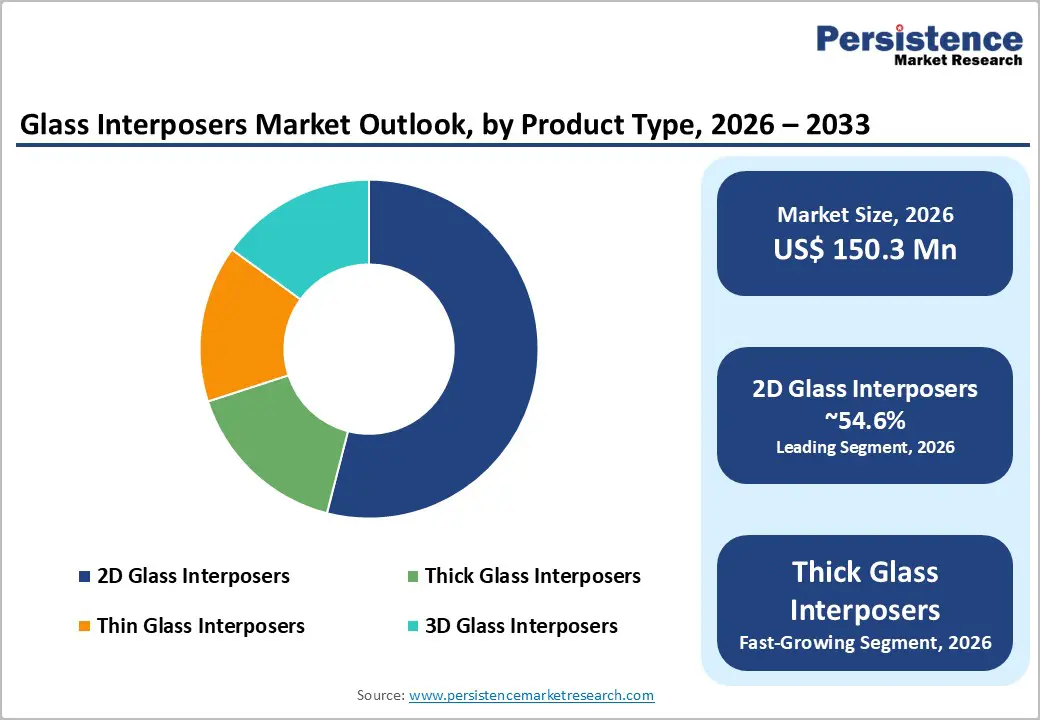

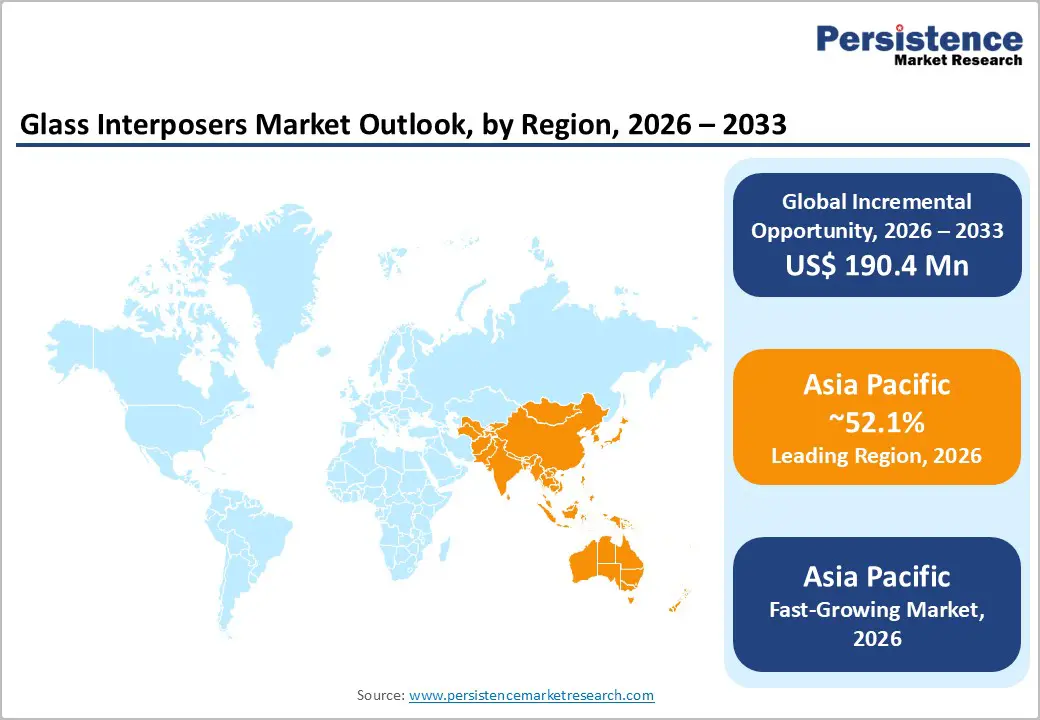

The global glass interposers market size is likely to be valued at US$150.3 million in 2026 and is expected to reach US$340.7 million by 2033, growing at a CAGR of 12.4% between 2026 and 2033, driven by the rapid transition toward chiplet-based architectures, increasing adoption of 2.5D/3D packaging, and rising demand for high-performance computing and AI-driven semiconductor designs.

The need for substrates with lower signal loss, improved thermal stability, and superior dimensional control is accelerating the shift toward glass interposers. Expansion in electric vehicles, 5G infrastructure, and data-intensive applications continues to reinforce long-term demand.

Key Industry Highlights:

- Leading Region: Asia Pacific is projected to account for approximately 52.1% of the market share, supported by strong semiconductor manufacturing infrastructure and the presence of major foundries and packaging providers such as Taiwan Semiconductor Manufacturing Company and Samsung Electronics.

- Fastest-growing Region: Asia Pacific is also the fastest-growing region, driven by rapid expansion in consumer electronics, increasing EV adoption, and large-scale investments in semiconductor packaging across countries such as China, India, and South Korea.

- Investment Plans: Significant investments are being made in advanced packaging and glass substrate technologies, particularly in the U.S. under the CHIPS and Science Act, alongside capacity expansions and technology developments by companies such as Intel Corporation and Applied Materials.

- Dominant Product Type: 2D Glass Interposers are anticipated to hold approximately 54.6% market share, due to their cost efficiency, established manufacturing processes, and widespread use in consumer electronics and computing applications.

- Leading Substrate Technology: Through-Glass Vias (TGV) is estimated to account for approximately 61.3% market share, driven by its ability to deliver high interconnect density, superior signal integrity, and compatibility with advanced semiconductor packaging requirements.

| Key Insights | Details |

|---|---|

| Glass Interposers Market Size (2026E) | US$150.3 Mn |

| Market Value Forecast (2033F) | US$340.7 Mn |

| Projected Growth (CAGR 2026 to 2033) | 12.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 11.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Adoption of AI, HPC, and Chiplet-Based Architectures

The increasing complexity of semiconductor design is driving demand for advanced packaging solutions that enable higher interconnect density and improved performance. AI and high-performance computing (HPC) applications require faster data transfer, lower latency, and efficient power management, all of which depend on advanced interposer technologies. Glass interposers provide superior dimensional stability and lower electrical loss compared to organic substrates, making them well-suited for next-generation chiplet architectures. The shift toward heterogeneous integration, where multiple chips are combined into a single package, further strengthens demand. As semiconductor manufacturers scale beyond traditional Moore’s Law limits, glass interposers are emerging as a critical enabler of performance-driven packaging innovation.

Growth in Electric Vehicles (EVs) and Advanced Driver-Assistance Systems (ADAS)

The rapid expansion of the EV market and increasing integration of ADAS features are significantly increasing semiconductor content per vehicle. Modern vehicles rely on high-speed communication systems, radar sensors, and centralized computing platforms that require advanced packaging solutions with high reliability and thermal performance. Glass interposers offer improved signal integrity and resistance to thermal expansion, making them suitable for automotive electronics operating under demanding conditions. As global EV adoption accelerates and regulatory frameworks support electrification, demand for advanced semiconductor packaging in automotive applications is expected to rise, creating sustained growth opportunities for glass interposers.

Expansion Of 5G Networks and High-Frequency Communication Systems

The global rollout of 5G infrastructure is increasing demand for high-frequency, low-loss materials in semiconductor packaging. Glass interposers provide excellent dielectric properties, enabling efficient signal transmission at high frequencies. This makes them ideal for RF modules, telecommunications equipment, and data center applications. As network traffic continues to grow and data consumption intensifies, telecom operators and equipment manufacturers are investing in advanced packaging technologies to enhance performance and energy efficiency. The integration of optical and electrical interconnects in next-generation systems further strengthens the case for glass-based substrates, positioning them as a key material in future communication technologies.

Barrier Analysis - Manufacturing Complexity and Yield Challenges

Glass interposer fabrication involves highly precise processes, including through-glass via (TGV) formation, thin-film deposition, and advanced lithography. These processes require specialized equipment and stringent quality control, which increases the risk of yield loss during production. Issues such as warpage, micro-cracks, and handling difficulties can impact manufacturing efficiency and raise costs. The need for advanced inspection and metrology systems further complicates production, limiting scalability in the short term. These technical barriers slow down the transition from pilot-scale development to high-volume manufacturing.

High Capital Investment and Limited Supply Chain Maturity

The glass interposers market requires significant capital investment in processing equipment, materials, and infrastructure. Compared to traditional substrates, the ecosystem for glass-based packaging is still developing, with fewer established suppliers and limited standardized processes. This creates supply chain constraints and longer lead times for production scaling. Companies must invest heavily in R&D and facility upgrades to achieve competitive yields and cost efficiency. These factors can delay commercialization and restrict market growth, particularly for smaller players with limited financial resources.

Opportunity Analysis - Adoption of Panel-Level Packaging (PLP) for Cost Efficiency

Panel-level packaging represents a significant opportunity for reducing manufacturing costs and improving throughput. By transitioning from wafer-based processing to larger panel formats, manufacturers can increase production efficiency and lower per-unit costs. Glass substrates are well-suited for panel-level processing due to their dimensional stability and uniformity. As demand for larger and more complex semiconductor packages grows, PLP is expected to gain traction, enabling scalable production of glass interposers. This shift will play a critical role in making glass-based packaging commercially viable across a broader range of applications.

Integration of Co-Packaged Optics and Hybrid Bonding Technologies

The increasing need for high-bandwidth data transfer in AI and data center applications is driving interest in co-packaged optics (CPO) and hybrid bonding. Glass interposers offer the precision and material properties required to support these advanced integration techniques. Their ability to combine optical and electrical interconnects within a single substrate makes them highly attractive for next-generation computing systems. As data center architectures evolve and demand for energy-efficient solutions grows, glass interposers are expected to play a central role in enabling these innovations.

Expansion into Automotive and Industrial Electronics

While consumer electronics currently dominate demand, the automotive and industrial sectors present significant growth opportunities. The increasing use of sensors, connectivity modules, and power electronics in vehicles and industrial systems requires advanced packaging solutions with high reliability and durability. Glass interposers provide the necessary performance characteristics, including thermal stability and resistance to environmental stress. As these sectors continue to adopt advanced semiconductor technologies, the addressable market for glass interposers is expected to expand beyond traditional applications.

Category-wise Analysis

Product Type Insights

2D glass interposers are anticipated to hold approximately 54.6% of the market share in 2026, maintaining their position as the dominant product type. Their leadership is driven by widespread adoption in consumer electronics and the availability of relatively mature manufacturing processes that reduce production complexity compared to advanced 3D structures. These interposers are widely used in applications requiring planar connectivity and moderate integration density, such as smartphones, tablets, and wearable devices.

For instance, application processors and memory modules in premium smartphones often rely on 2.5D configurations built on 2D interposers to balance performance and cost. Their compatibility with existing semiconductor packaging technologies and cost efficiency make them the preferred choice for high-volume production. The segment continues to benefit from steady demand across computing devices, including laptops and gaming systems, where performance improvements are required without significant cost escalation.

Thick glass interposers are anticipated to be the fastest-growing segment, driven by increasing demand for mechanically robust substrates capable of supporting larger package sizes and higher component density. These interposers provide enhanced structural stability, reduced warpage, and improved handling during panel-level processing, making them highly suitable for high-performance computing (HPC) and data center applications.

For example, large AI accelerators and server processors require substrates that can maintain dimensional integrity under thermal and mechanical stress, which thick glass interposers can effectively deliver. As semiconductor packages continue to expand in size and complexity, the need for durable substrates becomes more critical. Thin glass interposers remain relevant for compact, space-constrained designs such as mobile devices, while 3D glass interposers are gaining traction in advanced integration scenarios, including stacked memory and chiplet-based architectures, where maximum interconnect density and performance are required.

Substrate Technology Insights

Through-Glass Vias (TGV) are anticipated to account for approximately 61.3% of the market share, making them the leading substrate technology. TGV technology enables vertical electrical connections through glass substrates, delivering high interconnect density, low signal loss, and excellent electrical performance. These characteristics make TGV particularly suitable for high-frequency and high-speed applications such as RF modules, AI processors, and high-bandwidth memory (HBM) integration. For example, advanced GPU and AI chip packaging increasingly relies on TGV-enabled interposers to facilitate efficient communication between logic and memory components. The widespread adoption of TGV is also supported by its compatibility with existing semiconductor fabrication processes and its ability to meet the stringent performance requirements of next-generation electronic devices.

Glass Panel Level Packaging (PLP) is anticipated to be the fastest-growing substrate technology, driven by the need for scalable, high-throughput, and cost-efficient manufacturing solutions. PLP enables the use of larger substrate formats compared to traditional wafer-based processing, significantly improving production efficiency and reducing cost per unit. This approach is particularly advantageous for large-area packages used in data centers, networking equipment, and automotive electronics. For instance, panel-level processing is increasingly being explored for manufacturing large interposers used in AI accelerators and advanced driver-assistance systems. Redistribution layer (RDL)-first/last approaches and hybrid TGV-RDL technologies continue to play a critical role in bridging traditional and advanced packaging methods. These hybrid solutions provide design flexibility, allowing manufacturers to optimize performance, routing density, and cost while transitioning toward fully scalable glass-based packaging technologies.

Regional Insights

North America Glass Interposers Market Trends-Semiconductor R&D Leadership & Next-Gen Glass Substrate Innovation

North America plays a critical role in the glass interposers market, driven by strong investments in semiconductor innovation and advanced packaging technologies. The U.S. leads the region, supported by government initiatives aimed at strengthening domestic semiconductor manufacturing capabilities, particularly under the CHIPS and Science Act. Significant funding programs are accelerating research and development in advanced substrates, including glass interposers, with organizations such as Applied Materials and Intel Corporation actively advancing glass substrate technologies. Intel’s ongoing research into glass core substrates for next-generation packaging highlights the region’s push toward higher-density, larger-format interconnect solutions. The region’s well-established ecosystem of semiconductor companies, research institutions, and equipment manufacturers continues to foster continuous innovation and early-stage commercialization.

The demand for high-performance computing, artificial intelligence, and data center infrastructure is a major growth driver in North America. Companies such as Corning Incorporated are developing precision glass solutions tailored for advanced packaging, while Amkor Technology is expanding its advanced packaging capabilities to support heterogeneous integration. The rise of hyperscale data centers operated by major cloud providers is further increasing demand for high-bandwidth, low-loss interconnect solutions. These developments reinforce North America’s position as a global innovation hub. However, challenges related to scaling production and achieving cost efficiency remain, particularly as companies transition from pilot-scale glass interposer production to high-volume manufacturing.

Europe Glass Interposers Market Trends-Precision Engineering & Automotive-Driven Advanced Packaging Development

Europe is characterized by its strong focus on materials science, precision engineering, and industrial manufacturing. Countries such as Germany, the U.K., France, and Spain are at the forefront of research and development in advanced packaging technologies. The region benefits from a robust network of research institutions and technology companies specializing in glass materials and semiconductor processing. For example, SCHOTT AG continues to expand its glass-based substrate portfolio for semiconductor applications, focusing on high-density interconnect solutions. Similarly, RENA Technologies GmbH has commissioned advanced processing facilities for large-format glass substrates, supporting the industrialization of through-glass via (TGV) technologies.

The automotive industry is a key driver of demand in Europe, with increasing adoption of electric vehicles and advanced driver-assistance systems. Companies such as Infineon Technologies are expanding their automotive semiconductor portfolios, which indirectly drives demand for advanced packaging solutions, including glass interposers. Regulatory frameworks such as the European Green Deal and strict emissions targets are accelerating electrification, increasing the need for reliable, high-performance semiconductor packaging. Europe’s emphasis on high-quality manufacturing and technological innovation positions it as a significant contributor to the global glass interposers market. The region’s role remains more focused on technology development and high-value manufacturing rather than large-scale production, which is more concentrated in Asia Pacific.

Asia Pacific Glass Interposers Market Trends-Foundry Dominance & High-Volume Glass Interposer Manufacturing Growth

Asia Pacific is expected to be the largest and fastest-growing region in the glass interposers market, holding approximately 52.1% of the market share in 2026. The region’s dominance is driven by its extensive semiconductor manufacturing infrastructure, including foundries, packaging facilities, and electronics assembly operations. Countries such as China, Japan, South Korea, Taiwan, and India play a crucial role in the global supply chain. Leading companies such as Taiwan Semiconductor Manufacturing Company continue to expand advanced packaging technologies such as CoWoS, which rely on interposer-based architectures. At the same time, AGC Inc. and Nippon Electric Glass are investing in TGV-enabled glass substrates to support next-generation semiconductor packaging.

The rapid growth of consumer electronics, increasing adoption of electric vehicles, and expansion of 5G networks are key drivers in the region. Samsung Electronics and SK hynix are advancing high-bandwidth memory (HBM) technologies, which depend on advanced interposer solutions for efficient performance. In China, government-backed semiconductor initiatives are accelerating domestic packaging capabilities, while India is emerging as a new hub for electronics manufacturing through policy incentives. Asia Pacific benefits from cost advantages, a highly skilled workforce, and strong government support for semiconductor manufacturing. Continuous investments in advanced packaging infrastructure and rapid adoption of new technologies ensure that the region will maintain its leadership position in the glass interposers market.

Competitive Landscape

The global glass interposers market is moderately fragmented, with competition spanning materials suppliers, semiconductor manufacturers, and equipment providers. While no single company dominates the market, a group of leading players holds a significant share due to their technological expertise and strong industry presence. The competitive landscape is shaped by continuous innovation, strategic partnerships, and investments in advanced packaging technologies.

Market leaders focus on technological innovation, process optimization, and strategic collaborations. Key strategies include investment in panel-level packaging, development of high-performance materials, and expansion into emerging applications such as AI, automotive electronics, and data centers.

Key Industry Developments:

- In September 2025, Intel Corporation reaffirmed its glass substrate roadmap and initiated plans for a pilot production line, focusing on preparing the supply chain for commercialization before 2030. The development highlights Intel’s continued commitment to glass-based advanced packaging for AI and high-performance computing applications.

Companies Covered in Glass Interposers Market

- Corning Incorporated

- AGC Inc.

- SCHOTT AG

- Samtec Inc.

- Plan Optik AG

- 3D Glass Solutions, Inc.

- Allvia, Inc.

- LPKF Laser & Electronics AG

- Nippon Electric Glass Co., Ltd.

- HOYA Corporation

- Dai Nippon Printing Co., Ltd.

- RENA Technologies GmbH

- Tecnisco Ltd.

- Kiso Micro Co., Ltd.

- NSG Group

- SUSS MicroTec SE

Frequently Asked Questions

The glass interposers market is estimated to be valued at US$150.3 million in 2026.

The market is projected to reach US$340.7 million by 2033.

Key trends include the growing adoption of chiplet-based architectures, increasing demand for 2.5D and 3D packaging, rising integration of AI and high-performance computing (HPC), and the shift toward panel-level packaging (PLP) for cost efficiency and scalability.

2D glass interposers are the leading segment, accounting for approximately 54.6% of the market share, driven by their cost-effectiveness and widespread use in consumer electronics and computing devices.

The glass interposers market is expected to grow at a CAGR of 12.4% from 2026 to 2033.

Some of the major players include Intel Corporation, Taiwan Semiconductor Manufacturing Company, Corning Incorporated, AGC Inc., and SCHOTT AG.