- HVAC

- Europe HVAC System Market

Europe HVAC System Market Size, Share, and Growth Forecast, 2026 - 2033

Europe HVAC System Market by Heating Systems (Heat Pumps (Air Source, Ground Source), Boilers (Gas, Oil), Furnaces, Electric Heating Equipment, Misc.), Cooling Systems (Air Conditioning Systems, Chillers: Air-Cooled, Water-Cooled, Misc.: cooling towers, portable coolers, fan coil units), Ventilation Systems (Air Handling Units (AHUs), Ventilation Fans, Heat Recovery Ventilators (HRV/ERV), Ductwork, Diffusers, Louvers, Exhaust Systems) Installation Type (New Construction, Retrofit and Replacement), End-user and Regional Analysis for 2026 - 2033

Europe HVAC System Market Size and Trends Analysis

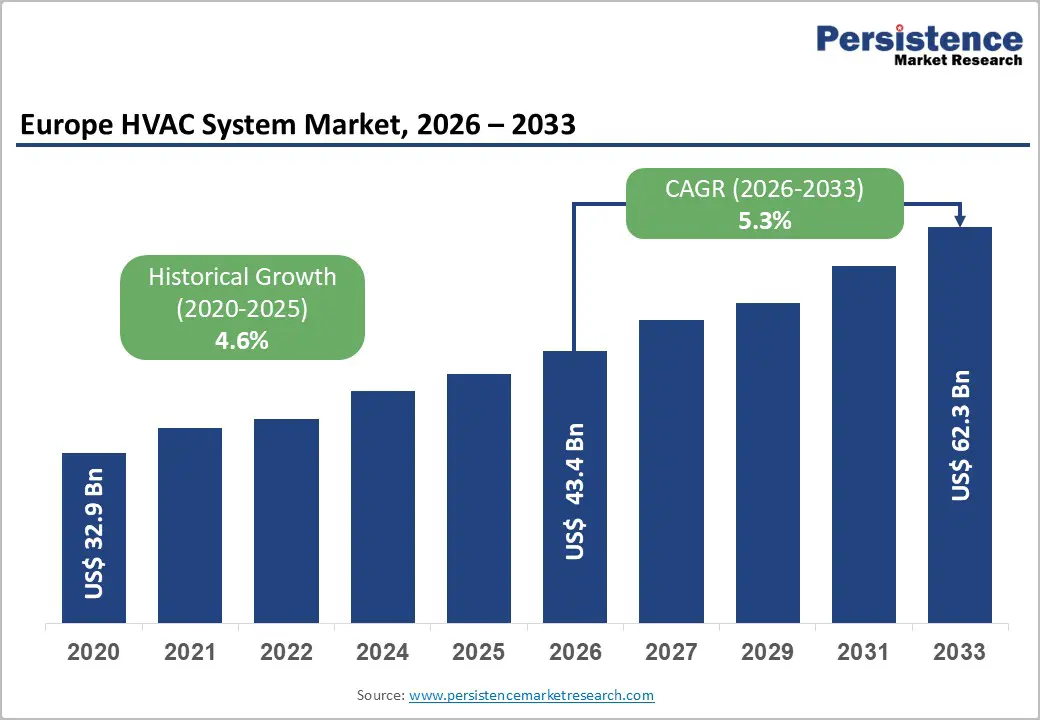

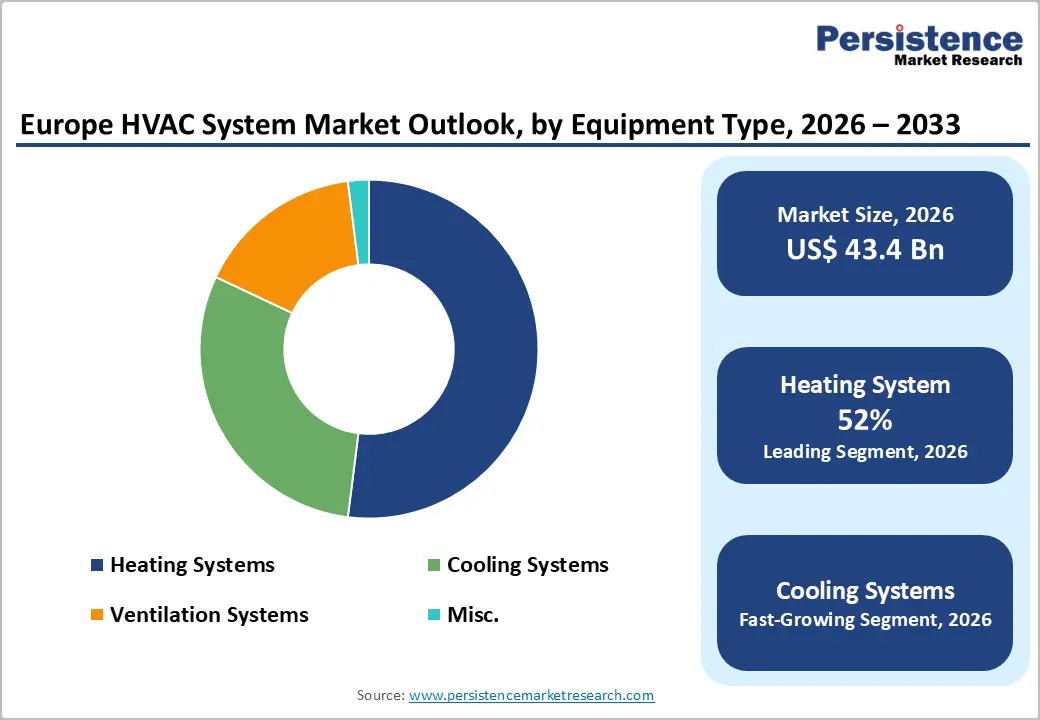

The Europe HVAC system market size is likely to be valued at US$ 43.4 Billion in 2026 and is projected to reach US$ 62.3 Billion by 2033, growing at a CAGR of 5.3% between 2026 and 2033.

The market's momentum is anchored by the EU's binding decarbonisation mandates compelling mandatory retrofits and heating electrification, the rapid commercialization of heat pump technology across residential and commercial segments, and the accelerating shift to smart, IoT-enabled climate control systems. In 2023, space and water heating alone accounted for 77.6% of final energy consumed by European households, underscoring the scale of the sector's transformation requirement. Regulatory frameworks, including the Renewable Energy Directive (EU/2023/2413) and the Energy Performance of Buildings Directive (EPBD) 2024 recast are catalyzing sustained procurement across both new construction and retrofit channels.

Key Industry Highlights

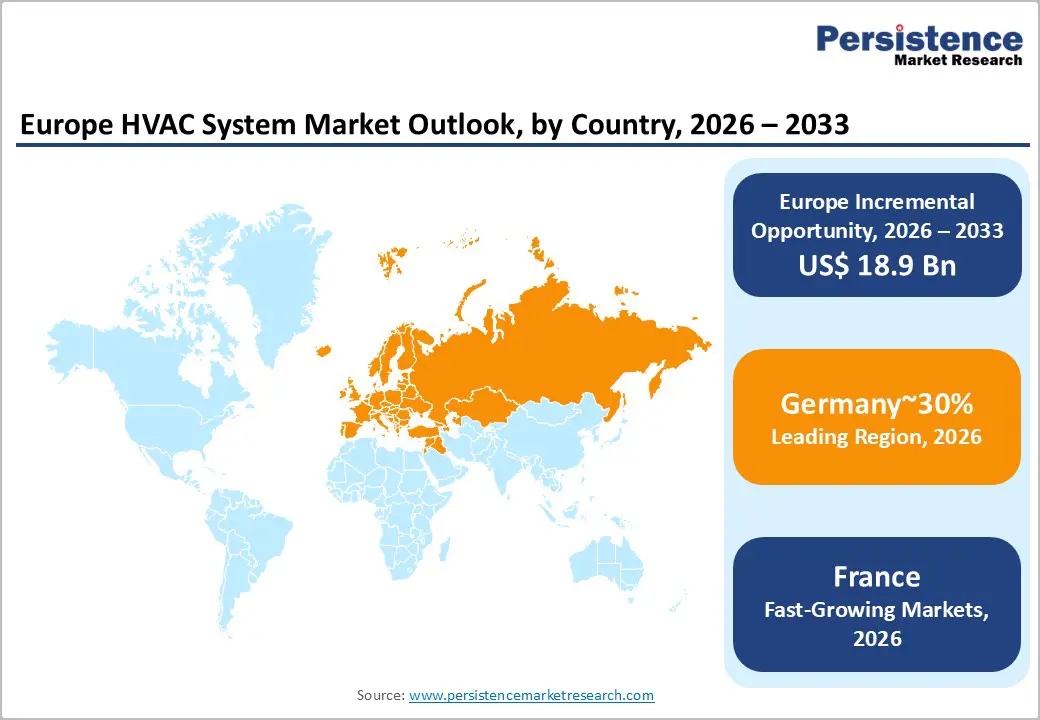

- Heating Systems: Heating systems dominate the Europe HVAC market with approximately 52% share in 2026, driven by high heating demand in Germany, France, Italy, and Poland, supported by EU decarbonisation mandates and the REPowerEU heat pump deployment targets.

- Heat Pumps Fastest-Growing Segment: Heat pumps (air and ground source) represent the fastest-growing equipment type, accounting for 23% of the market, fueled by regulatory incentives, phase-out of gas boilers, and sustainability-focused retrofits and new construction projects.

- Growth Indicator: Ventilation systems, including AHUs, HRVs, and ERVs, are accelerating in adoption due to heightened indoor air quality awareness, mandatory EU ventilation standards, and integration of demand-controlled ventilation in commercial and institutional buildings.

- Leading Installation Type: Retrofit and replacement installations hold approximately 57% of market share, reflecting Europe’s ageing building stock and the compliance-driven upgrade cycle under the EPBD and national building energy regulations.

- Fastest-Growing Installation Type: New construction HVAC projects are expanding rapidly in Central and Eastern Europe, particularly in Hungary, Poland, and Czechia, driven by EU Green Deal and Fit-for-55 mandates requiring zero-emission buildings from 2030 onwards.

- Competitive Landscape: Market concentration is high, with key players Daikin, Carrier, Vaillant, Johnson Controls, Bosch, and Viessmann leveraging energy-efficient, low-GWP refrigerants, integrated heat pump systems, and smart IoT-enabled HVAC solutions to capture market share.

| Key Insights | Details |

|---|---|

| HVAC System Market Size (2026E); | US$ 43.4 Bn |

| Market Value Forecast (2033F) | US$ 62.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.6% |

Market Dynamics

Drivers - EU Regulatory Mandates and Binding Decarbonisation Targets Reshaping Demand

Europe HVAC System Market is being structurally redirected by an unprecedented regulatory framework aimed at eliminating fossil fuel dependence in building heating and cooling. The Renewable Energy Directive (EU/2023/2413) mandates EU member states to increase the annual share of renewables in heating and cooling by at least 0.8% per year from 2021 to 2025, and by 1.1% per year from 2026 to 2030. In 2023, only 26.2% of energy used in heating and cooling came from renewable sources, while approximately two-thirds of fossil gas consumed in the EU was directed toward buildings and industry heating highlighting a profound compliance gap that must be closed.

Germany's Building Energy Act (GEG) mandates that all new heating installations from 2025 onwards must derive at least 65% of heating energy from renewables, creating immediate and durable demand for electric heat pumps and advanced HVAC systems. The EU Heating and Cooling Strategy, planned for publication in Q2 2026, will further guide decarbonisation and system integration priorities, directly shaping procurement patterns and capital allocation across the European building stock.

The 2024 Recast Energy Performance of Buildings Directive Unlocking Retrofit and New-Build Procurement

The 2024 recast of the Energy Performance of Buildings Directive (EPBD) places HVAC professionals at the core of Europe's building decarbonisation journey, mandating that all new constructions must be zero-emission by 2030 and that existing buildings undergo regular energy performance upgrades. This directive directly drives procurement of high-efficiency heating, ventilation, and air conditioning systems in both the retrofit and new construction segments. Modern HVAC equipment replacements can reduce energy consumption by 20 to 40% per installation through equipment upgrades and demand-controlled systems.

The EU ETS2 carbon pricing mechanism, scheduled to introduce carbon costs for building heating from 2027, will further accelerate the economics of transition from fossil fuel boilers to heat pump and hybrid systems. With the total number of HVAC units in Europe scheduled to surpass 157 million by the end of 2024, and an EUR 56 billion bloc-wide heat pump incentive package deployed in 2024, the EPBD is transforming from a compliance requirement into the Europe HVAC System Market's most powerful demand accelerant.

Indoor Air Quality Awareness and Smart HVAC Technology Adoption

Post-pandemic, awareness of indoor air quality (IAQ) has emerged as a material demand driver for advanced ventilation and HVAC solutions across Europe, particularly in densely populated urban centres and public buildings. Technologies including HEPA filtration, UV-C disinfection systems, demand-controlled ventilation (DCV), and CO2 monitoring sensors are increasingly specified in commercial and institutional projects. HVAC systems now represent up to 40% of total electricity consumption in commercial buildings during peak summer months, creating a compelling business case for efficiency-led system replacement.

The proliferation of IoT-enabled smart HVAC systems particularly in commercial hubs, hospitals, schools, and luxury residential developments accelerated markedly in 2024, with adoption expected to intensify in 2025 as property developers pursue smart building certifications such as BREEAM, LEED, and WELL standards. This convergence of IAQ standards and digital building management is creating a distinct, high-value procurement sub-segment within the broader Europe HVAC System Market, particularly across Western Europe where building energy intelligence is embedded in procurement mandates.

Market Restraining Factors

Qualified Installer Shortage Constraining Market Execution

Despite strong regulatory and consumer demand, the Europe HVAC System Market faces a critical bottleneck in skilled workforce availability. The scale-up of installer training programmes is identified as a significant enabler, with installer shortages noted particularly in Germany, the Netherlands, and the United Kingdom. The EU target of 10 million new heat pump installations by 2027 under REPowerEU places intense pressure on a workforce that is structurally insufficient to absorb this demand, creating implementation delays and increasing installation costs that dampen overall market throughput. Without coordinated national workforce investment, regulatory targets risk outpacing physical delivery capacity.

High Upfront Capital Costs and Subsidy Dependency

The transition from conventional fossil fuel systems to advanced heat pump and hybrid HVAC solutions involves substantially higher upfront capital expenditure for both households and commercial operators. While government subsidies including Germany's BEG programme and France's MaPrimeRénov scheme partially offset costs, reduced or restructurally amended incentive programmes in several markets contributed to a 23% decline in European heat pump sales in 2024. Price sensitivity among residential consumers and SME building owners creates significant market vulnerability whenever subsidy frameworks are modified or delayed, slowing the pace of market conversion from fossil fuel to low-carbon HVAC equipment.

Opportunities - Heat Pump Acceleration Under REPowerEU and National Subsidy Frameworks

The European heat pump segment represents the highest-priority commercial opportunity within the Europe HVAC System Market, supported by aligned political will, regulatory obligation, and consumer demand. The European Heat Pump Association (EHPA) reported that 980,000 heat pumps were sold in the first half of 2025, representing a 9% recovery after a 23% decline in 2024, signalling market normalization and renewed growth momentum.

The EU's REPowerEU plan targets 50 to 60 million heat pump units in operation by 2030, creating a structural multi-year procurement pipeline for manufacturers, installers, and component suppliers. Norway and Finland already demonstrate the long-term potential, with 632 and 524 heat pumps installed per 1,000 households respectively as of 2025. Companies that invest in scalable production capacity as demonstrated by Vaillant Group's commissioning of a 300,000-unit annual capacity heat pump mega-factory in Senica, Slovakia in March 2023, doubling its European production capacity to over 500,000 units per year are positioned to capture outsized market share as demand re-accelerates across Western and Central Europe.

Smart Building Integration and IoT-Enabled HVAC Systems in Commercial Real Estate

The convergence of smart building infrastructure and high-performance HVAC technology creates a well-defined and commercially significant opportunity for solution providers in the Europe HVAC System Market. Commercial building owners and institutional operators are under growing pressure to meet BREEAM and LEED performance standards, mandatory energy audits, and operational cost reduction targets simultaneously all of which are efficiently addressed through IoT-integrated, data-driven HVAC management platforms.

Daikin Europe's Smart Control System (SCS), launched for hydronic HVAC plants in January 2025 and covering chillers, heat pumps, air handling units, and fan coils, illustrates the commercial value of integrated control architectures that optimize energy efficiency, system performance, and occupant comfort in real time.

Trane's containerised Battery Energy Storage System (BESS) rental solution, launched across Europe in February 2026, offering 230 kWh battery capacity and 50 kW output, enables customers to enhance energy resilience and decarbonisation in off-grid and peak-demand scenarios. Companies capable of offering turnkey, digitally managed HVAC ecosystems combining equipment, controls, and energy management services stand to command premium pricing and long-term service revenue in the fast-growing commercial and light-industrial segments across Europe.

Category-wise Analysis

Equipment Type Insights

Heating Systems command the leading position in the Europe HVAC System Market's Equipment Type segmentation, accounting for 52% of total market share in 2026. This dominant positioning reflects Europe's structural orientation toward heating-intensive climates and the scale of the ongoing fossil-to-electric transition in building heat supply. Within the Heating Systems segment, Heat Pumps (Air Source and Ground Source) alone hold a 23% share of the overall market a significant sub-segment concentration driven by EU policy incentives, REPowerEU commitments, and the phase-out trajectory for gas boilers across key markets.

In 2024, heat pumps accounted for 28% of the European heating systems market, according to the European Heat Pump Association (EHPA), down from a peak of 31.6% in 2023 but still over 6 percentage points higher than in 2021, demonstrating structural market share gains despite a cyclical correction. The Gas Boiler sub-segment continues to represent substantial installed base volumes across legacy building stock in Germany, Italy, France, and Poland, but faces regulatory headwinds from GEG mandates and the upcoming EU ETS2 carbon pricing beginning in 2027, accelerating replacement cycles.

The fastest-growing equipment type segment is Ventilation Systems, encompassing Air Handling Units (AHUs), Ventilation Fans, Heat Recovery Ventilators (HRV and ERV), ductwork, diffusers, and exhaust systems. This segment's momentum is driven by post-pandemic IAQ awareness, mandatory ventilation standards in commercial and institutional buildings, and the integration of demand-controlled ventilation within EU-compliant building energy management frameworks. The 2024 EPBD recast's emphasis on integrated, performance-verified HVAC solutions including demand-controlled ventilation with CO2 monitoring is accelerating specification of advanced ventilation systems in both new construction and deep renovation projects across Western and Central Europe

Installation Type Insights

Retrofit and Replacement is the dominant installation type segment, holding approximately 57% of the Europe HVAC System Market in 2026. This leading position reflects the structural weight of Europe's ageing building stock, which necessitates continuous system replacement and energy performance upgrading. Countries including Italy, Poland, and the United Kingdom host large volumes of under-insulated and thermally inefficient buildings that are subject to escalating regulatory compliance pressure under the revised EPBD. High-efficiency HVAC system replacements in these markets yield energy consumption reductions of 20 to 40% per installation, creating a compelling economic case alongside regulatory obligation. The ongoing phase-out trajectory of legacy gas boiler systems driven by Germany's Building Energy Act (GEG) and equivalent national regulations is systematically generating replacement demand across residential and light commercial sub-sectors throughout the forecast period.

New Construction represents the fastest-growing installation type segment, supported by infrastructure modernization programmes, urbanization, and commercial real estate development across Central and Eastern Europe (CEE), as well as sustained residential construction activity in Poland, Czechia, and the Nordic markets. The EU Green Deal and Fit for 55 Package mandate that all new buildings constructed from 2030 onward must achieve zero-emission performance standards, compelling developers to specify state-of-the-art HVAC systems from the outset. Haier HVAC Europe's acquisition of KLIMA KFT in Hungary in June 2025, encompassing KLIMA's distribution channels, service network, and building engineering capabilities, directly reflects corporate investment into the fast-growing CEE new construction HVAC segment. This segment benefits from a long-term structural tailwind as new zero-emission building standards embed premium HVAC specification as a mandatory feature rather than an elective upgrade.

Competitive Landscape

Europe HVAC System market is largely consolidated and oligopolistic, dominated by a few key global and regional players that control a significant share of the market. Leading companies such as Daikin Europe N.V., Carrier Global Corporation, Vaillant Group, Johnson Controls, Bosch Group, and Viessmann Climate Solutions leverage extensive product portfolios, technological innovations, and strong distribution networks to maintain their market positions across residential, commercial, and industrial segments.

These players focus on energy-efficient solutions, low-GWP refrigerants, integrated heat pump systems, and digital HVAC controls, aligning with Europe’s decarbonization and energy efficiency mandates. Smaller regional players exist but face high barriers to entry due to stringent regulations, capital-intensive production, and the dominance of well-established brands. Strategic acquisitions, such as Carrier’s purchase of Viessmann Climate Solutions and Bosch’s acquisition of Johnson Controls’ residential and light commercial HVAC business, reflect ongoing consolidation in the market.

Key Developments:

- In June, 2025, Haier HVAC Europe completed the acquisition of KLIMA KFT** in Budapest, strengthening its footprint in Hungary and the broader Central and Eastern Europe (CEE) region. The transaction includes KLIMA’s assets, distribution channels, and service network, enabling Haier to accelerate deployment of high-efficiency and sustainable HVAC solutions aligned with EU green transition policies. This development enhances competitive intensity in the Europe HVAC system market, particularly in the fast-growing CEE region driven by infrastructure modernization and decarbonization initiatives.

- In June 2025, Johnson Controls deployed large-scale commercial and district heat pumps across Europe, notably in southern Germany, delivering high-efficiency heating while cutting customers’ annual energy costs by over 50% and CO2 emissions by up to 60%. The initiative leverages renewable thermal energy sources such as treated wastewater and deep geothermal wells, supporting municipal, institutional, and industrial clients in accelerating climate action, improving energy security, and advancing the transition to sustainable heating solutions.

- In March 2023, Vaillant Group commissioned a new mega factory in Senica, Slovakia, exclusively producing heat pumps with an annual capacity of 300,000 units, doubling the company’s European production to over 500,000 per year. This expansion, part of nearly €1 billion invested since 2016 and additional planned investments, reinforces Vaillant’s role in Europe’s energy transition and supports the EU target of 10 million newly installed heat pumps by 2027.

- In December 2025, Copeland and Daikin announced the expansion of their joint venture into Europe to provide advanced inverter swing rotary compressors, power electronics, and controls for residential heat pumps. This collaboration aims to accelerate the adoption of energy-efficient heating solutions, supporting Europe’s transition away from fossil fuels and strengthening both companies’ positions in the high-growth residential heat pump segment of the Europe HVAC system market.

Companies Covered in Europe HVAC System Market

- Trane Technologies PLC Class A

- Lennox International Inc

- Haier

- Carrier Global Corp

- Daikin Industries Ltd

- LG Electronics Inc ADR

- Samsung Electronics Co Ltd

- Mitsubishi Electric

- Valliant Group

- Viessmann (Acquired by Carrier )

- AAON

- Johnson Controls

- Midea

- Frigidaire HVAC

- Bosch Group

Frequently Asked Questions

Europe HVAC System is projected to be valued at US$ 43.4 Bn in 2026.

The Heating Systems segment is expected to account for approximately 52% of the Europe HVAC System by Heating Systems in 2026.

The market is expected to witness a CAGR of 5.3% from 2026 to 2033.

The Europe HVAC System Market growth is driven by EU decarbonisation mandates, renewable energy targets, zero-emission building regulations, rising demand for energy-efficient heat pumps, indoor air quality awareness, and adoption of IoT-enabled smart HVAC systems.

Key market opportunities in the Europe HVAC System Market lie in accelerated heat pump adoption under REPowerEU and national subsidies, and the integration of smart, IoT-enabled HVAC systems for energy-efficient, digitally managed commercial and light-industrial buildings.

Key players in HVAC System include Daikin Europe N.V., Carrier Global Corporation, Vaillant Group, Johnson Controls, Bosch Group, and Viessmann Climate Solutions.