- Medical Devices

- Closed Drug Transfer Systems Market

Closed Drug Transfer Systems Market Size, Share, and Growth Forecast, 2026 – 2033

Closed Drug Transfer Systems Market by System Type (Needle-less Systems, Membrane-to-Membrane Systems), Closing Mechanism (Color-to-Color Alignment Systems, Others), Component (Syringe Safety Devices, Others), and Regional Analysis for 2026 – 2033

Closed Drug Transfer Systems Market Size and Trends Analysis

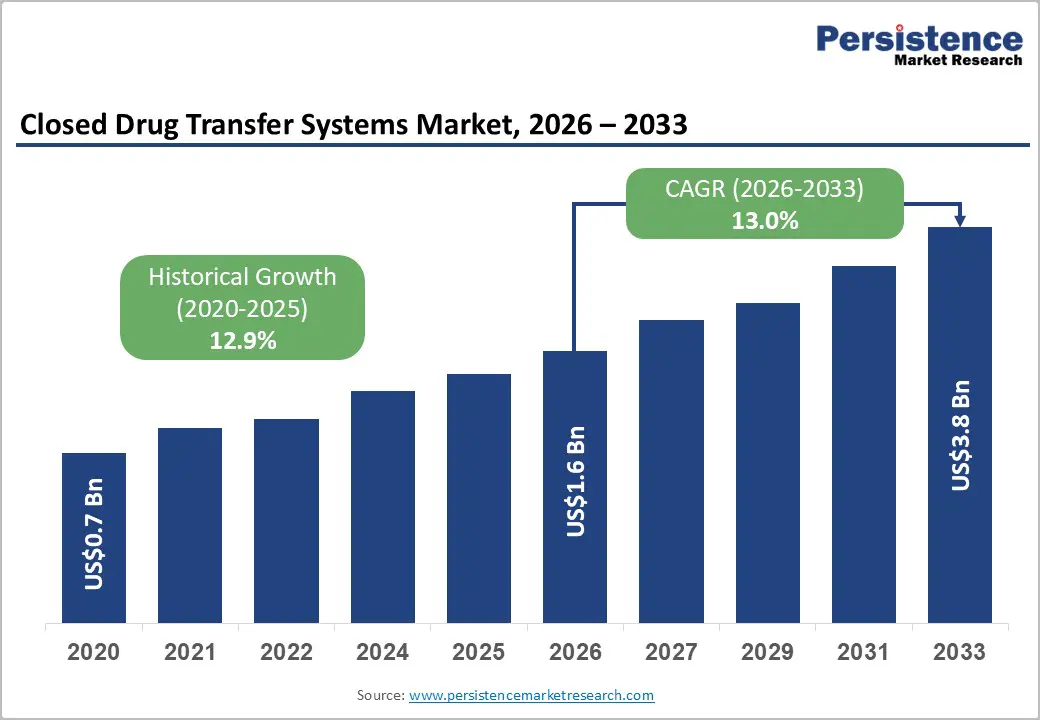

The global closed drug transfer systems market size is likely to be valued at US$1.6 billion in 2026 and is expected to reach US$3.8 billion by 2033, growing at a CAGR of 13.0% during the forecast period from 2026 to 2033, driven by a convergence of clinical demand and safety regulations that underscore the increasing complexity and volume of hazardous drug therapies administered in healthcare settings.

A key underlying driver of this trend is the rising global cancer burden, according to World Health Organization (WHO) and its International Agency for Research on Cancer, which reported that there were an estimated 20 million new cancer cases worldwide in 2022 and nearly 9.7 million cancer related deaths, with the burden expected to climb significantly in the coming decades as populations age and exposure to key risk factors persists. WHO analysis in 2026 emphasized that a substantial proportion of cancer cases are linked to modifiable risk factors such as tobacco use, alcohol consumption, and air pollution, highlighting both the rising demand for effective cancer therapies and the broader imperative for preventative action. Ongoing technological advancements in device design, such as improved needle-free systems, membrane-to-membrane barriers, ergonomic interfaces, and integration with automated compounding equipment, are enhancing workflow efficiency and user safety in clinical practice.

Key Industry Highlights:

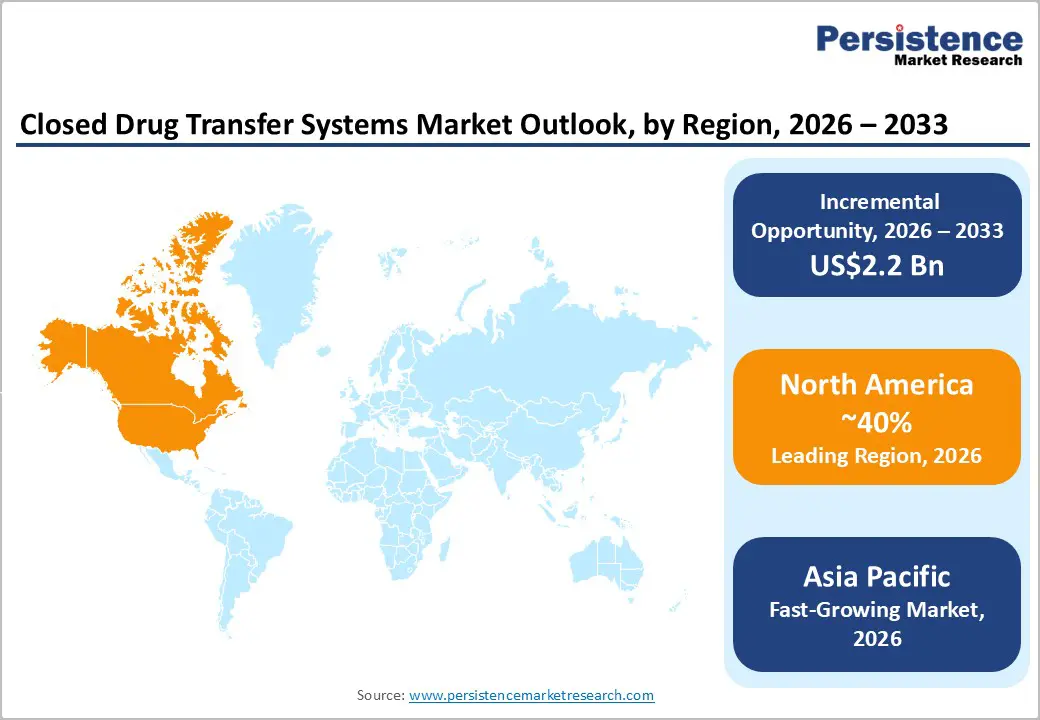

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by strong regulatory enforcement, advanced oncology infrastructure, and high adoption of safety-compliant technologies.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by rising healthcare investments, expanding oncology infrastructure, and increasing adoption of safety-compliant technologies.

- Leading System Type: Needleless systems are projected to represent the leading system type in 2026, accounting for 60% of the revenue share, driven by their ability to reduce needle stick risks and enhance safety for healthcare workers.

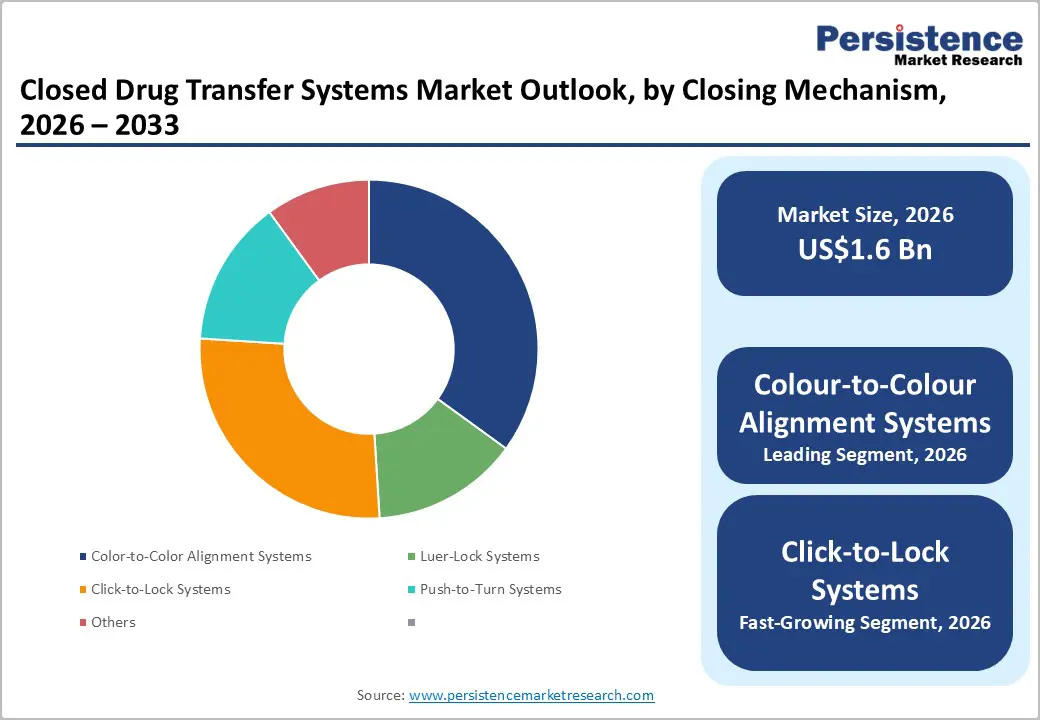

- Leading Closing Mechanism: Color-to-color alignment is anticipated to be the leading closing mechanism, accounting for over 55% of the revenue share in 2026, supported by intuitive visual confirmation of secure connections that minimize errors in busy pharmacy and clinical settings.

| Key Insights | Details |

|---|---|

|

Closed Drug Transfer Systems Market Size (2026E) |

US$1.6 Bn |

|

Market Value Forecast (2033F) |

US$3.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

13.0% |

|

Historical Market Growth (CAGR 2020 to 2025) |

12.9% |

DRO Analysis

Driver Analysis- Rising Incidence of Cancer and Use of Hazardous Drugs

The increasing prevalence of cancer worldwide has significantly contributed to the demand for closed drug transfer systems, as healthcare providers manage growing volumes of cytotoxic and hazardous drugs. As more patients undergo chemotherapy, targeted therapies, and immunotherapies, hospitals, oncology centers, and compounding pharmacies require solutions that minimize exposure to these potent medications. Closed transfer devices ensure safe handling during drug preparation, reconstitution, and administration, reducing the risk of accidental contact. This trend is particularly prominent in regions with high cancer incidence, where rising treatment volumes directly correlate with the need for reliable and efficient containment systems.

The complexity of modern oncology treatments fuels adoption, as multi-drug regimens and high-risk biologics require precise, leak-proof transfer processes. The use of hazardous drugs in pediatric and geriatric oncology, where dosing and handling are critical, also necessitates safer systems to protect healthcare workers. Growing awareness of occupational exposure risks is encouraging healthcare institutions to adopt closed drug transfer systems to protect staff health as well as meet safety requirements. This sustained demand across both emerging and mature markets underscores the direct relationship between cancer prevalence, hazardous drug use, and market growth.

Stringent Regulatory Requirements and Occupational Safety Standards

Regulatory frameworks, including USP <800>, NIOSH guidelines, and equivalent European and Asian standards, have strengthened the need for closed drug transfer systems in clinical environments. These regulations mandate proper handling, preparation, and administration of hazardous drugs to protect healthcare professionals from exposure. Hospitals, pharmacies, and outpatient facilities must comply with these standards, which have accelerated the adoption of CSTDs. Regulatory emphasis on error prevention, containment, and exposure reduction ensures that devices offering enhanced safety, reliability, and compliance are prioritized, creating a favorable environment for market growth and innovation.

Enforcement of occupational safety standards also drives investments in training and infrastructure upgrades. Institutions are increasingly implementing CSTDs as part of mandatory hazardous drug handling protocols, reducing legal and health risks. Adoption is supported by audits, inspections, and accreditation programs that evaluate safety compliance. Healthcare facilities understand that using advanced closed system technologies helps meet regulations while reducing accidental exposure and contamination. Regulatory frameworks and safety mandates remain pivotal in shaping purchasing decisions and fostering steady market expansion in both established and emerging regions.

Restraint Analysis - Integration Challenges with Existing Workflows

Integrating closed drug transfer systems into existing pharmacy and clinical workflows can pose significant challenges. Facilities with established preparation and compounding processes may face operational disruptions during the adoption of new devices, particularly if equipment compatibility is limited or additional training is required. Workflow adjustments, staff retraining, and procedural revisions can increase initial implementation costs and create temporary inefficiencies. These barriers are particularly pronounced in high-volume hospitals where speed and efficiency are critical, making healthcare professionals hesitant to transition without clear operational benefits or seamless device compatibility with current equipment.

The challenge is compounded by diverse infrastructure and procedural standards across healthcare facilities. Facilities may struggle with balancing safety compliance and efficiency, as some devices require additional steps or unique handling techniques. Hospitals with limited automation or outdated equipment may face difficulty incorporating CSTDs without operational bottlenecks. Resistance may also arise from staff accustomed to conventional systems, emphasizing the importance of comprehensive training programs, user-friendly designs, and clear protocols to ensure smooth integration. Addressing these workflow challenges is critical for widespread adoption and maximizing the benefits of CSTDs.

Lack of Testing Standardization

The absence of standardized testing protocols for closed drug transfer systems limits consistency in evaluating device performance. Variations in methods for assessing containment efficiency, leak-proof integrity, and resistance to hazardous drug exposure make it difficult for healthcare providers to compare products objectively. This lack of standardization slows adoption, as institutions hesitate to invest in devices without clear performance benchmarks, particularly when multiple manufacturers offer varied designs, mechanisms, and certifications. Standardized testing is critical for ensuring safety, regulatory compliance, and effective device selection in diverse clinical settings.

Stakeholders face challenges in validating the effectiveness of CSTDs across different hospital environments and drug types. Disparities in testing methods also impact regulatory approvals and create uncertainty regarding device reliability under real-world conditions. Healthcare facilities often rely on internal evaluations, manufacturer claims, or third-party studies, which vary in rigor and scope. Without uniform standards, procurement decisions can be inconsistent, potentially exposing staff to risks or limiting adoption in regions with strict regulatory expectations. Establishing universally accepted testing protocols would strengthen confidence and accelerate market growth.

Opportunity Analysis - Technological Convergence and New Applications

Emerging technological innovations present significant opportunities for CSTDs, including integration with automated compounding systems, robotic handling, and smart monitoring solutions. Advanced designs, such as membrane-to-membrane barriers, air-filtration devices, and ergonomic mechanisms, improve safety, usability, and efficiency. These innovations expand the scope of applications beyond traditional chemotherapy compounding, encompassing biologics, immunotherapies, and high-potency drug administration. Integration with digital monitoring and tracking systems can enhance compliance, reduce errors, and provide real-time safety feedback, creating new market opportunities for device manufacturers and healthcare providers seeking advanced solutions.

Technological convergence also enables cost-effective and scalable solutions suitable for both large hospitals and smaller clinics. By offering multi-functional systems that accommodate diverse drug types and workflows, manufacturers can address unmet needs in emerging markets where infrastructure and skilled labor are limited. Continuous research and development fosters product differentiation, strengthens competitive positioning, and supports adoption in high-growth segments. The trend toward innovative, adaptable, and user-friendly closed drug transfer systems positions the market for sustained expansion and cross-industry collaboration.

Oncology Infrastructure Growth

The expansion of oncology facilities, cancer treatment centers, and specialized outpatient clinics worldwide drives demand for closed drug transfer systems. As healthcare providers invest in modern infrastructure to support increasing patient volumes, the need for reliable, safe, and compliant drug handling solutions grows. Upgraded pharmacies, compounding labs, and infusion centers require CSTDs to ensure staff safety, minimize contamination, and meet accreditation standards. This structural growth in the oncology ecosystem provides manufacturers with new avenues to deploy devices and integrate them into standard workflows, creating a long-term market opportunity tied to healthcare modernization.

Urbanization, rising healthcare budgets, and increased public-private partnerships contribute to the establishment of state-of-the-art oncology centers, particularly in emerging regions. These facilities prioritize safety protocols and advanced technologies to accommodate complex treatment regimens and higher chemotherapy volumes. The expansion of oncology infrastructure also facilitates training programs, awareness campaigns, and technology adoption, reinforcing the role of CSTDs as an essential component of modern cancer care. The growth of oncology infrastructure directly supports both device penetration and market scaling.

Category-wise Analysis

System Type Insights

Needleless systems are expected to lead the closed drug transfer systems market, accounting for approximately 60% of revenue in 2026, driven by their prominence, which stems from the design’s ability to eliminate needles, significantly reducing needlestick injuries and exposure to hazardous drugs for healthcare workers. Hospitals and oncology pharmacies prefer these systems due to their simplicity, ease of use, and alignment with regulatory compliance standards such as USP <800>. For example, BD Medical’s PhaSeal needle-less system is widely adopted in U.S. hospital pharmacies, offering a closed pathway for drug reconstitution that minimizes contamination risk.

Membrane-to-membrane systems assays are likely to represent the fastest-growing segment, supported by their superior containment for high-risk hazardous drugs. These systems provide dual-barrier protection, offering maximum leak prevention during vial-to-syringe transfers, which is essential in advanced oncology and high-volume hospital pharmacies. For example, Equashield’s membrane-to-membrane system has gained adoption in outpatient oncology centers in Asia Pacific region, where high-potency therapies demand stringent safety measures. Its design supports secure transfer of cytotoxic drugs, even in multi-step compounding processes, while maintaining compliance with occupational safety standards.

Closing Mechanism Insights

Color-to-color alignment systems are projected to lead the market, capturing around 55% of the revenue share in 2026, supported by their intuitive design, which provides clear visual confirmation of secure connections. This reduces the risk of disconnections and procedural errors during hazardous drug preparation, particularly in high-volume pharmacy and compounding environments. For example, the Equashield EQUASHIELD® II system, which incorporates color-guided alignment and connection features to ensure proper engagement between vial and syringe components.

The system’s design enhances safety by minimizing handling errors and preventing leakage during drug transfer, making it widely adopted in oncology pharmacies.

Click-to-lock systems are likely to be the fastest-growing closing mechanism, driven by their secure, audible, and tactile feedback that ensures connections are properly locked. For example, the B. Braun Melsungen OnGuard® 2 CSTD system incorporates a click-to-lock mechanism that provides clear confirmation of secure connections during drug transfer. North America and Europe, providing pharmacists and nurses with real-time confirmation that the system is engaged, reducing accidental disconnections during preparation and administration of hazardous drugs.

The segment’s growth is fueled by increased regulatory emphasis on error-proof designs, user safety, and the handling of high-potency therapies in outpatient and hospital settings.

Regional Insights

North America Closed Drug Transfer Systems Market Trends

North America is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by stringent regulatory frameworks, advanced healthcare infrastructure, and widespread adoption of safety-focused technologies. The region accounts for a significant portion of the market, supported by early implementation of USP <800> standards in the U.S., which mandate containment systems for hazardous drug handling across hospitals and oncology centers. Healthcare providers in the U.S. and Canada are prioritizing occupational safety, reflecting strong demand for CSTDs in high-volume oncology settings to minimize exposure to cytotoxic agents during preparation and administration.

Healthcare providers increasingly demand solutions that integrate seamlessly with automated compounding systems and pharmacy robotics, improving efficiency while maintaining safety. Closed system transfer devices are evolving with enhanced leak-proof designs, double-membrane barriers, and compatibility with negative-pressure isolators, reducing drug vapor and aerosol escape during handling. For example, B. Braun’s OnGuard® 2 CSTD, introduced to streamline hazardous drug handling with improved usability and sealing performance, reflects the broader trend toward innovation that balances safety with operational convenience.

Europe Closed Drug Transfer Systems Market Trends

Europe is likely to be a significant market for closed drug transfer systems, due to healthcare providers prioritizing occupational safety and standardized hazardous drug handling. With the region holding a significant share of the market, adoption varies across Western and Eastern Europe, with countries such as Germany leading in institutional uptake of CSTDs in hospital pharmacies and oncology units. This trend is reflected in the rising use of membrane-to-membrane and diaphragm-based systems that provide effective containment for potent chemotherapeutic agents.

For example, B. Braun Melsungen AG has strengthened its presence in European hospital networks with its OncoSafe and infusion-integrated CSTD offerings, designed to meet regional safety standards and ease workflow integration.

Despite positive momentum, Europe’s CSTD landscape also reflects challenges and evolving trends. Adoption rates differ significantly by country. Western Europe shows higher uptake while regions with constrained healthcare budgets lag, creating a heterogeneous market dynamic. Country-level regulatory frameworks and procurement mechanisms influence how rapidly CSTDs are integrated into everyday clinical practice. Hospitals and specialty clinics are placing greater emphasis on device interoperability with automated compounding systems and established pharmacy workflows, pushing manufacturers toward user-friendly designs backed by training and support.

Asia Pacific Closed Drug Transfer Systems Market Trends

The Asia Pacific region is likely to be the fastest-growing region, driven by rising cancer incidence and greater demand for chemotherapy and biologic therapies, which have prompted hospitals and oncology centers to adopt CSTDs that minimize hazardous drug exposure during preparation and administration. Regional regulatory bodies and hospital policies are gradually strengthening hazardous drug handling standards, encouraging adoption across both public and private healthcare systems.

For example, Terumo Corporation’s expansion of advanced infusion and transfer devices in the Asia Pacific region, with solutions designed to enhance safety and ease of use for clinicians handling cytotoxic drugs.

Developed markets such as Japan and South Korea show higher penetration of safety-compliant closed transfer systems due to stringent hospital protocols and growing oncology caseloads, while emerging markets are catching up as infrastructure investment accelerates. Challenges remain, including the need for greater training on proper CSTD use and harmonization of safety guidelines across countries with diverse healthcare systems. Manufacturers and distributors are responding by expanding education initiatives and local partnerships to smooth implementation and increase awareness of the benefits of CSTDs.

Competitive Landscape

The global closed drug transfer systems market exhibits a moderately fragmented structure, driven by the involvement of both major medical technology firms and specialized safety solution providers that continually innovate to meet stringent regulatory and clinical requirements in hazardous drug handling. Leading incumbents leverage extensive distribution networks, robust research and development programs, and broad product portfolios to maintain their positions, while mid-tier and emerging companies carve niches through targeted offerings and regional strategies.

With key leaders, including BD Medical (Becton, Dickinson and Company), lauded for its comprehensive CSTD solutions and widespread adoption of its BD-PhaSeal™ systems in hospital and oncology settings, the competitive landscape reflects a blend of scale, regulatory compliance, and product efficacy that shapes purchasing decisions in healthcare facilities worldwide. These players compete through continuous product enhancement, strategic partnerships, and expansion into new therapeutic and geographic markets.

Key Industry Developments:

- In December 2025, Equashield launched its EQUASHIELD® Safety Platform at the ASHP 2025 Midyear Clinical Meeting in Las Vegas, introducing an integrated solution combining closed system drug transfer device (CSTD) technology with automated compounding and IV workflow software. The platform is designed to enhance hazardous drug handling by improving safety, reducing exposure risks, and ensuring workflow accuracy through automation and real-time verification.

- In January 2025, Becton, Dickinson and Company highlighted its latest drug delivery innovations at the Pharmapack 2025 event in Paris, focusing on advanced solutions designed to support complex therapies such as biologics. The company emphasized integrating closed-transfer safety features into next-generation drug delivery systems, reinforcing its strategy to enhance hazardous drug handling, improve patient safety, and support evolving pharmaceutical manufacturing and oncology treatment needs.

Companies Covered in Closed Drug Transfer Systems Market

- Becton Dickinson BD

- ICU Medical

- Equashield

- B Braun Melsungen

- Baxter International

- Corvida Medical

- JMS Co

- Simplivia Healthcare

- Yukon Medical

- Terumo

Frequently Asked Questions

The global closed drug transfer systems market is projected to reach US$1.6 billion in 2026.

Rising cancer incidence and stringent regulatory requirements for safe handling of hazardous drugs are driving the closed drug transfer systems market.

The closed drug transfer systems market is expected to grow at a CAGR of 13.0% from 2026 to 2033.

Technological advancements in CSTD design and expanding oncology infrastructure are creating key growth opportunities in the market.

Becton Dickinson (BD), ICU Medical, Equashield, B Braun Melsungen, Baxter International, and Corvida Medical are the leading players.