- Oil & Gas

- Cathodic Protection Market

Cathodic Protection Market Size, Share, and Growth Forecast 2025 - 2032

Cathodic Protection Market by Technology Type (Galvanic (Sacrificial-Anode), Impressed-Current (ICCP), Hybrid), Solution (Products- Anodes, Power Supplies, Junction Boxes, Test Stations, Remote Monitors, Others; Services: Inspection, Design & Construction, Maintenance), Application, Regional Analysis, 2025 - 2032

Cathodic Protection Market Size and Trend Analysis

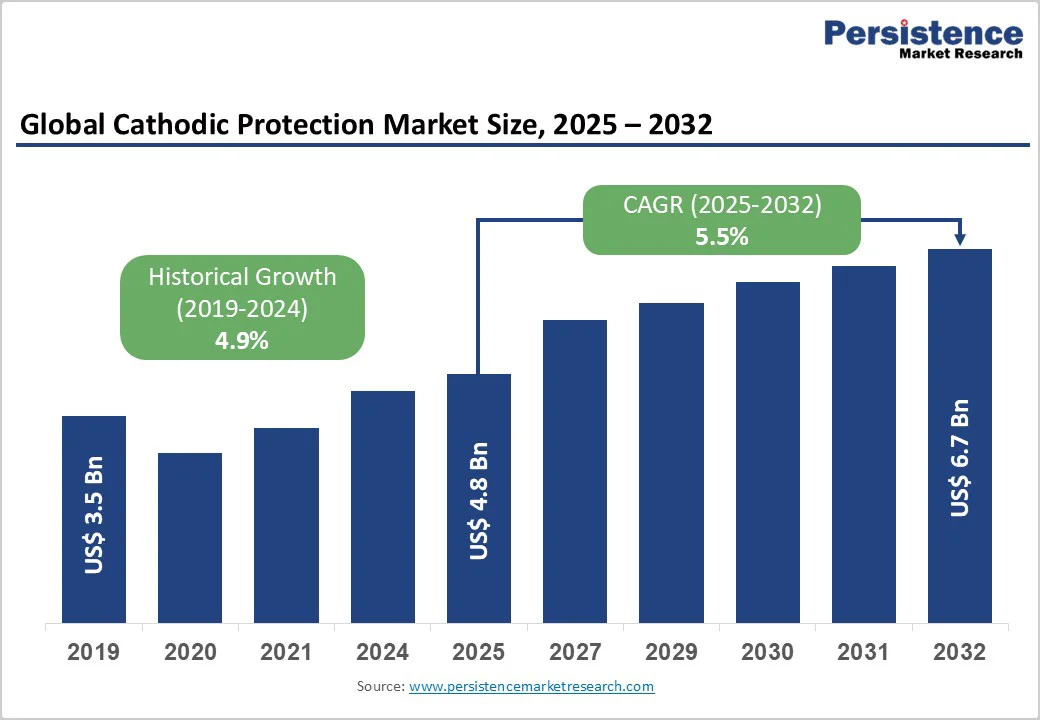

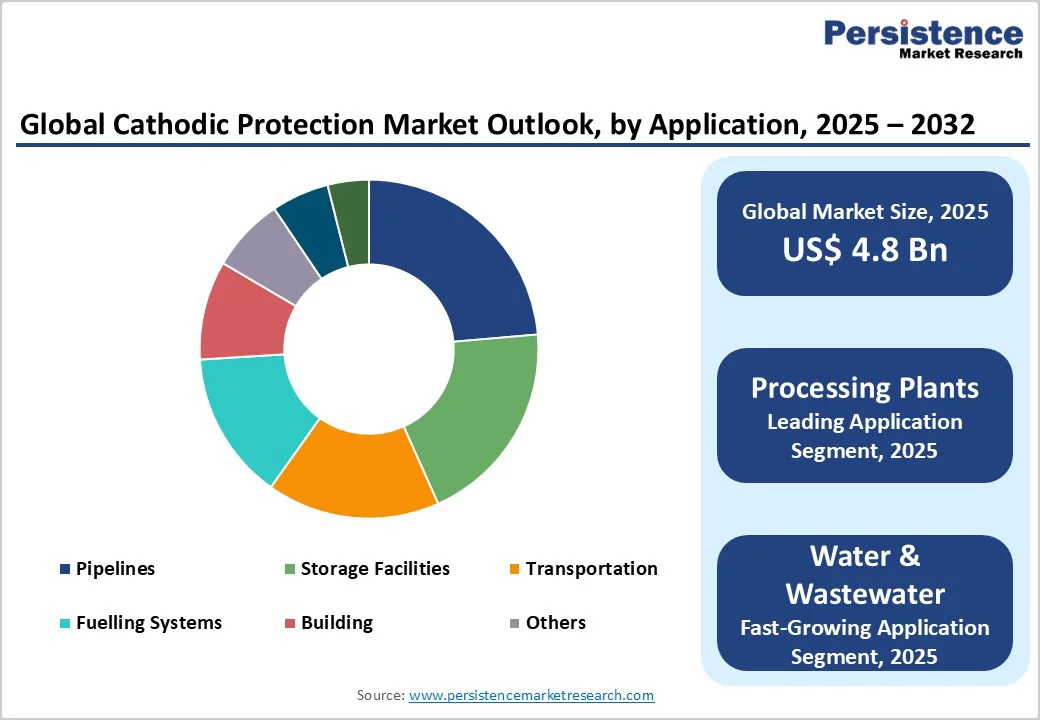

The global cathodic protection market size is valued at US$4.8 billion in 2025 and projected to reach US$6.7 billion, expanding at a CAGR of 4.9% between 2025 and 2032. Growing concerns over infrastructure corrosion, which costs the global economy over US$2.5 trillion annually, are driving demand for cathodic protection systems.

As corrosion-related damages strain pipelines, bridges, and utilities, governments and industries are increasingly prioritizing preventive corrosion management. The market growth is further supported by expanding infrastructure development in Asia-Pacific and India, as well as by strict regulatory frameworks for pipeline safety and asset integrity management.

Key Market Highlights

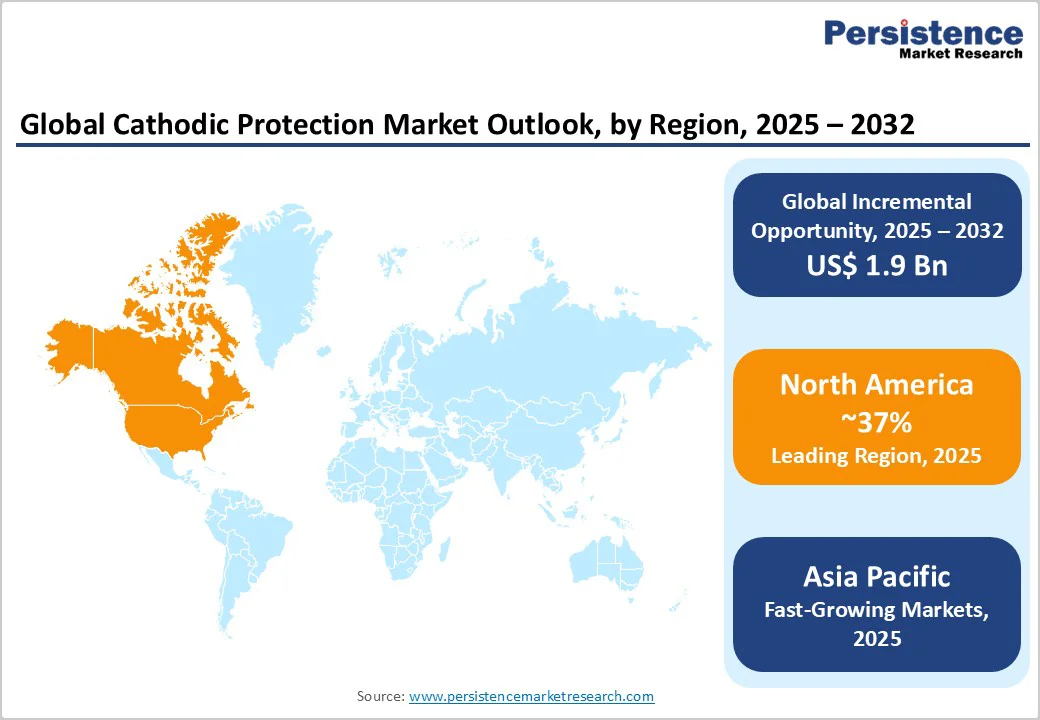

- Leading Region: North America leads the global cathodic protection market with around 37% share, driven by aging infrastructure, stringent PHMSA compliance, and extensive federal funding for pipeline modernization and safety upgrades.

- Fastest Growing Region: Asia-Pacific holds nearly 31% share and is the fastest-growing region, driven by large-scale infrastructure, industrial, and energy sector investments.

- Dominant Segment: Galvanic (Sacrificial-Anode) systems dominate the technology landscape with about 45% market share, driven by cost-effectiveness, passive operation, and proven reliability across pipelines and marine assets.

- Fastest Growing Segment: Processing plants account for approximately 22.7% share and represent the fastest-growing application area, owing to intensive corrosion exposure in the chemical, refining, and power generation industries.

- Key Market Opportunity: IoT-integrated monitoring and AI-based predictive maintenance platforms are transforming corrosion management, reducing manual inspection needs by up to 30%, and enhancing system reliability through real-time data analytics.

| Key Insights | Details |

|---|---|

|

Cathodic Protection Market Size (2025E) |

US$4.8 Billion |

|

Market Value Forecast (2032F) |

US$6.7 Billion |

|

Projected Growth CAGR (2025-2032) |

5.5% |

|

Historical Market Growth (2019-2024) |

4.9% |

Market Dynamics

Driver - Infrastructure Aging and Regulatory Compliance Requirements

Aging infrastructure across North America and Europe is driving major investments in corrosion prevention technologies. Regulatory mandates such as those from the PHMSA (Pipeline and Hazardous Materials Safety Administration) require external corrosion control for buried and submerged pipelines installed after July 31, 1971. Governments are boosting infrastructure maintenance budgets, with the U.S. Natural Gas Distribution Infrastructure Safety and Modernization (NGDISM) Grant Program allocating US$1 billion over five years, and an additional US$400 million for replacing aging distribution pipes.

These regulations and funding initiatives are intensifying the need for cathodic protection systems to ensure long-term asset reliability and compliance. With more than 85% of North America’s infrastructure now under regulatory inspection, pipeline operators and utilities are increasingly prioritizing corrosion control measures to extend asset lifespans and reduce maintenance costs.

Expansion of Offshore Renewable Energy and Emerging Applications

The offshore renewable energy sector, particularly offshore wind, has become a key growth area for cathodic protection systems. Offshore wind turbine foundations are exposed to highly corrosive marine environments and must sustain operational lifespans of 25–35 years with minimal maintenance. This has led to the development of specialized cathodic protection designs optimized for offshore wind structures, moving beyond conventional oil and gas standards.

Collaborations between leading industry players like Sherwin-Williams and standards bodies are shaping new international guidelines such as ISO/AWI 25249, tailored for offshore wind applications. The rapid expansion of offshore wind projects across Europe and Asia-Pacific is significantly boosting demand for advanced, long-life cathodic protection technologies engineered for challenging marine conditions.

Restraint - High Initial Capital Investment and Installation Costs

Cathodic protection systems require significant upfront capital due to the high costs of specialized materials, installation labor, and maintenance services. Depending on system complexity, installation costs typically range from US$1,000 to US$10,000 per unit, posing financial barriers for municipal utilities and smaller industrial operators. Budget constraints often lead public sector entities to delay implementation or to opt for temporary, less effective corrosion-prevention measures.

The need for skilled technicians to design, install, and monitor these systems adds a significant labor cost component, especially in regions with limited technical expertise. This combination of capital intensity and workforce dependency continues to restrain widespread adoption across cost-sensitive sectors and developing markets.

Technical Complexity and Performance Uncertainties in Deepwater and Extreme Environments

Implementing cathodic protection systems in deepwater and harsh environments poses major technical challenges that hinder adoption. In offshore applications, maintaining consistent protection levels under high-current demands and corrosive marine conditions is complex and often uncertain. Concerns persist about long-term system durability, anode replacement frequency, and the compatibility of cathodic protection systems with aging or poorly coated infrastructure. These performance uncertainties elevate operational risks and discourage investment in critical deepwater and high-salinity applications. The industry continues to face limitations in optimizing current distribution and material performance under extreme conditions, compelling some operators to consider alternative corrosion control methods in such demanding environments.

Opportunity - IoT-Enabled Remote Monitoring and Predictive Maintenance Technologies

The integration of Internet of Things (IoT) and artificial intelligence (AI) into cathodic protection systems is unlocking transformative growth opportunities. Smart sensor networks enable real-time corrosion monitoring across pipelines and infrastructure, minimizing manual inspections and reducing unplanned downtime by up to 30%. Companies such as ElSyca are pioneering digital twin technologies and advanced modeling software that deliver deep visibility into corrosion performance, supporting proactive risk management and optimized system design.

The growing adoption of cloud-based platforms, combined with AI-driven analytics, enhances asset integrity management by enabling predictive maintenance and automated compliance reporting. These innovations are especially attractive to asset-heavy sectors such as oil & gas, utilities, and transportation, which seek operational efficiency, cost savings, and enhanced regulatory compliance through intelligent corrosion-control systems.

Infrastructure Modernization Initiatives in Emerging Economies and Renewable Energy Expansion

Rapid industrialization and extensive infrastructure development across emerging economies, particularly India and China, are creating strong growth opportunities for cathodic protection solutions. Expanding water distribution networks, oil and gas pipeline projects, and renewable energy infrastructure are driving significant demand for corrosion protection systems. Governments in these regions are prioritizing modernization programs to extend the lifespan and improve the safety of critical infrastructure assets.

Global investments in alternative and low-carbon energy systems, supported by initiatives such as the Infrastructure Investment and Jobs Act and the Inflation Reduction Act, are accelerating the construction of hydrogen and carbon capture and utilization (CCUS) pipelines. The transition toward sustainable energy infrastructure necessitates advanced corrosion protection, opening substantial opportunities for manufacturers and service providers offering innovative cathodic protection solutions tailored to emerging renewable and hydrogen applications.

Category-wise Insights

Technology Type Analysis

Galvanic (Sacrificial-Anode) systems dominate the cathodic protection market, accounting for about 45% of the market share due to their cost-effectiveness, ease of installation, and dependable performance. These systems, commonly using aluminum and zinc-based anodes, are widely adopted in marine, offshore, and remote pipeline applications where electrical infrastructure is limited. Their passive operation and low maintenance requirements make them ideal for distributed and hard-to-access assets.

Impressed current cathodic protection (ICCP) systems, however, are gaining momentum across large industrial and offshore installations. They offer higher current capacity, better control precision, and enhanced effectiveness in highly corrosive environments such as refineries and storage tanks. Despite higher initial and maintenance costs, ICCP systems are emerging as the fastest-growing technology category, driven by the need for long-term reliability and adaptable protection performance.

Solution Analysis

Products such as anodes, rectifiers, and power supplies dominate the cathodic protection market, accounting for around 55% of the total share. Supporting components such as junction boxes, test stations, and remote monitoring systems are essential to modern installations, and remote monitoring solutions are growing rapidly as industries adopt digital corrosion management.

The services segment, including inspection, construction, and maintenance, is expanding as asset operators increasingly seek professional optimization and reliability solutions. Leading players such as Corrpro Companies, Inc., MATCOR, Inc., and Aegion Corporation now offer integrated solutions that encompass design, installation, monitoring, and long-term asset management.

Application Analysis

Processing plants lead the cathodic protection market with about 22.7% share, driven by corrosive conditions in chemical processing, oil & gas refining, and power generation facilities. These environments demand advanced protection systems to prevent costly equipment failures and environmental risks. Pipelines are the second-largest segment, supported by the extensive global network that transports oil, gas, water, and chemicals.

Water and wastewater treatment facilities represent the fastest-growing application area, spurred by stricter environmental standards and rising public infrastructure investments. Modernization programs emphasizing corrosion protection for reinforced concrete and steel structures exposed to hydrogen sulfide and other gases are generating high demand for integrated cathodic protection solutions that enhance durability and extend asset life.

Regional Insights

North America Cathodic Protection Market Trends

North America leads the global cathodic protection market, accounting for nearly 37% of the market share, driven by its vast network of over 2.6 million miles of pipelines and stringent regulatory frameworks, such as PHMSA mandates and NACE standards. These enforce comprehensive corrosion control programs across oil, gas, and water pipeline networks. Ongoing modernization and rehabilitation projects, supported by strong federal funding, sustain consistent investment in corrosion management systems across the U.S. and Canada.

Infrastructure upgrades under programs such as the NGDISM Grant and clean energy policies are driving further adoption. The growing hydrogen pipeline and renewable energy infrastructure expansion, incentivized by the Infrastructure Investment and Jobs Act and Inflation Reduction Act, is generating new demand for advanced cathodic protection systems suited for evolving industrial conditions.

Europe Cathodic Protection Market Trends

Europe ranks as the second-largest regional market, expanding at a steady 5.0% CAGR, supported by stringent environmental directives and industrial modernization. Germany dominates with nearly 24% regional share, underpinned by its advanced manufacturing and chemical industries, which require high-integrity corrosion control solutions. Strict EU environmental standards and safety protocols further enhance adoption across processing, water treatment, and industrial facilities.

Offshore wind infrastructure across the North Sea and Baltic Sea represents a strong growth driver. The U.K. market, growing at about 4.5% CAGR, benefits from large-scale renewable energy projects demanding durable corrosion protection for submerged turbine components. Collaborative standardization initiatives among European industry bodies continue to refine specialized corrosion protection systems tailored for offshore and renewable applications.

Asia Pacific Cathodic Protection Market Trends

Asia Pacific accounts for around 31% of the global cathodic protection market, making it the fastest-growing regional segment driven by large-scale infrastructure, industrial, and energy sector investments. China dominates regional demand with nearly 55% share of the Asia Pacific’s market, supported by rapid urbanization, industrial expansion, and extensive oil, gas, and water pipeline construction that increasingly integrates cathodic protection systems for durability and sustainability.

India represents the fastest-growing national market, contributing approximately 20% of the regional share, propelled by over US$75 billion in transportation and water supply modernization projects. The expansion of offshore oil, gas, and renewable energy infrastructure particularly wind and solar continues to create strong opportunities for advanced corrosion management and asset protection solutions.

Competitive Landscape

The cathodic protection market is moderately consolidated, with leading players collectively accounting for over half of the global market share. The landscape reflects a mix of consolidation and specialization, as larger firms continue acquiring regional service providers to enhance technical expertise, expand geographic presence, and diversify offerings across infrastructure, energy, and water sectors. Strategic mergers and acquisitions remain central to strengthening integrated service portfolios and global competitiveness.

Market differentiation is increasingly driven by innovation and digital transformation. Companies are investing in advanced simulation software, predictive maintenance systems, and SaaS-based remote monitoring platforms, shifting from traditional hardware-centric approaches to technology-enabled, service-oriented business models.

Key Market Developments

- In March 2024, Aegion Corporation acquired Toncco, expanding its U.S. presence and strengthening pipe rehabilitation capabilities for municipal and private water infrastructure projects. This marks Aegion’s 11th acquisition since 2022, reinforcing its aggressive market expansion strategy.

- In May 2024, PillarFour Capital acquired Corrpro Canada, a key provider of cathodic protection solutions for oil, gas, power, and marine industries, enhancing its technological capabilities and signaling growing investor confidence in the corrosion protection sector.

- In September 2025, Sherwin-Williams promoted new ISO standards for offshore wind corrosion protection, addressing industry gaps and ensuring durability standards better suited to harsh marine environments compared to legacy oil and gas specifications.

Companies Covered in Cathodic Protection Market

- Aegion Corporation

- Corrpro Companies Inc.

- MATCOR Inc.

- Farwest Corrosion Control Company

- Metec Group

- BAC Corrosion Control Ltd.

- The Nippon Corrosion Engineering Co. Ltd.

- Perma-Pipe International Holdings Inc.

- Wilson Walton International Ltd.

- ElSyca NV

- CP TECH

- Ray Murray Inc.

- Berkeley Springs Instruments LLC

- Advance Products & Systems LLC

- Cathodic Protection Co. Ltd.

- Honeywell International Inc.

- Siemens AG, ABB Ltd.

- VCS Engineering

- FORCE Technology

Frequently Asked Questions

The global cathodic protection market is valued at US$ 4.8 billion in 2025 and projected to reach US$ 6.7 billion by 2032, growing at a 4.9% CAGR driven by infrastructure investments and corrosion prevention needs.

Key drivers include aging infrastructure, regulatory mandates (PHMSA), and emerging renewable energy applications like offshore wind and hydrogen pipelines.

Galvanic (sacrificial-anode) systems lead with ~45% market share, while impressed current systems (ICCP) are the fastest-growing due to higher current capacity and advanced control features.

North America leads with extensive regulated pipeline networks, while Asia-Pacific, especially India, is the fastest-growing region driven by large-scale infrastructure investments.

Opportunities include IoT-enabled remote monitoring, AI-based predictive maintenance, and renewable energy and hydrogen infrastructure corrosion protection.