- Executive Summary

- Global Car Electronics and Communication Accessories Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026 - 2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply-Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Global Automotive Industry Overview

- Global Electrical Industry Overview

- Forecast Factors - Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2020 - 2033

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global Car Electronics and Communication Accessories Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Global Car Electronics and Communication Accessories Market Outlook: Product Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Product Type, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Product Type, 2026-2033

- LCDs

- Music System

- Mobile Chargers

- Communication

- Communication

- Market Attractiveness Analysis: Product Type

- Global Car Electronics and Communication Accessories Market Outlook: Vehicle Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Vehicle Type, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Vehicle Type, 2026-2033

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Market Attractiveness Analysis: Vehicle Type

- Global Car Electronics and Communication Accessories Market Outlook: Sales Channel

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Sales Channel, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Sales Channel, 2026-2033

- OEM

- Aftermarket

- Market Attractiveness Analysis: Sales Channel

- Global Car Electronics and Communication Accessories Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Region, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Car Electronics and Communication Accessories Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Product Type, 2026-2033

- LCDs

- Music System

- Mobile Chargers

- Communication

- Communication

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Vehicle Type, 2026-2033

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Sales Channel, 2026-2033

- OEM

- Aftermarket

- Europe Car Electronics and Communication Accessories Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Product Type, 2026-2033

- LCDs

- Music System

- Mobile Chargers

- Communication

- Communication

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Vehicle Type, 2026-2033

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Sales Channel, 2026-2033

- OEM

- Aftermarket

- East Asia Car Electronics and Communication Accessories Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Product Type, 2026-2033

- LCDs

- Music System

- Mobile Chargers

- Communication

- Communication

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Vehicle Type, 2026-2033

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Sales Channel, 2026-2033

- OEM

- Aftermarket

- South Asia & Oceania Car Electronics and Communication Accessories Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Product Type, 2026-2033

- LCDs

- Music System

- Mobile Chargers

- Communication

- Communication

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Vehicle Type, 2026-2033

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Sales Channel, 2026-2033

- OEM

- Aftermarket

- Latin America Car Electronics and Communication Accessories Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Product Type, 2026-2033

- LCDs

- Music System

- Mobile Chargers

- Communication

- Communication

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Vehicle Type, 2026-2033

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Sales Channel, 2026-2033

- OEM

- Aftermarket

- Middle East & Africa Car Electronics and Communication Accessories Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Product Type, 2026-2033

- LCDs

- Music System

- Mobile Chargers

- Communication

- Communication

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Vehicle Type, 2026-2033

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Sales Channel, 2026-2033

- OEM

- Aftermarket

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- Amada Machine Tools Co., Ltd.

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- CHIRON GROUP SE

- DMG MORI. CO., LTD.

- DN Solutions

- Georg Fischer Ltd.

- HYUNDAI WIA CORP

- JTEKT Corporation

- Komatsu Ltd

- Makino Inc.

- Okuma Corporation

- Hurco Companies, Inc.

- Amada Machine Tools Co., Ltd.

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Automotive

- Car Electronics and Communication Accessories Market

Car Electronics and Communication Accessories Market Size, Share, and Growth Forecast 2026 - 2033

Car Electronics and Communication Accessories Market by Product Type (LCDs, Music Systems, Mobile Chargers, Communication, and Cigarette Lighters), Sales Channel (OEM and Aftermarket), and Vehicle Type (Passenger Cars, Light Commercial Vehicles, and Heavy Commercial Vehicles), and Regional Analysis for 2026 - 2033

Car Electronics and Communication Accessories Market Trends and Analysis

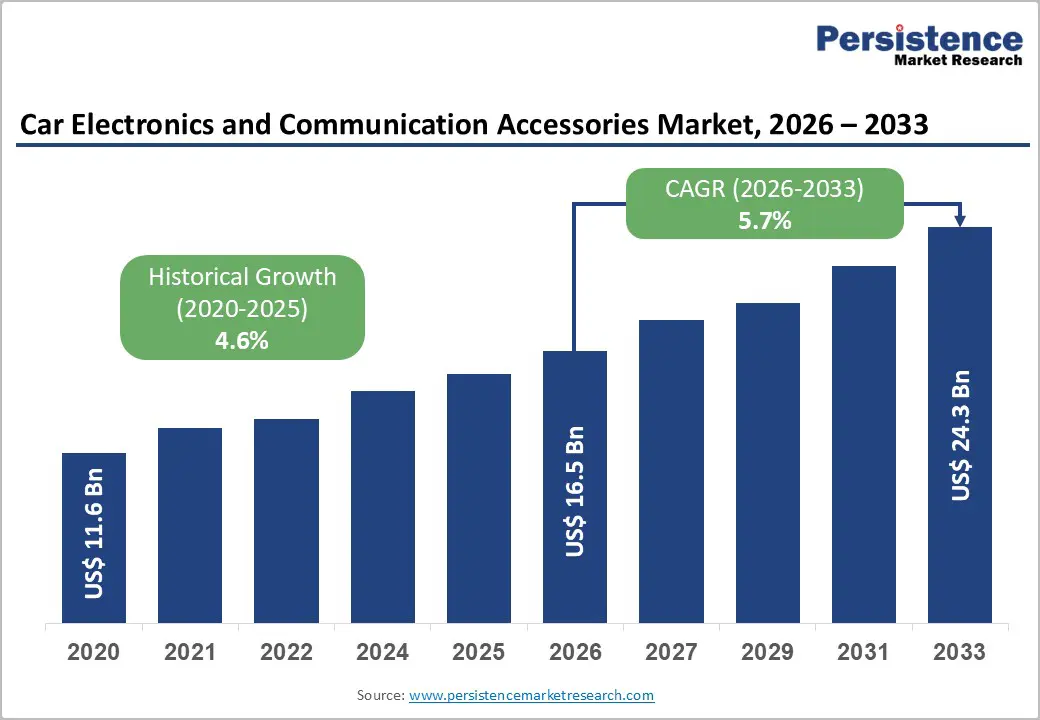

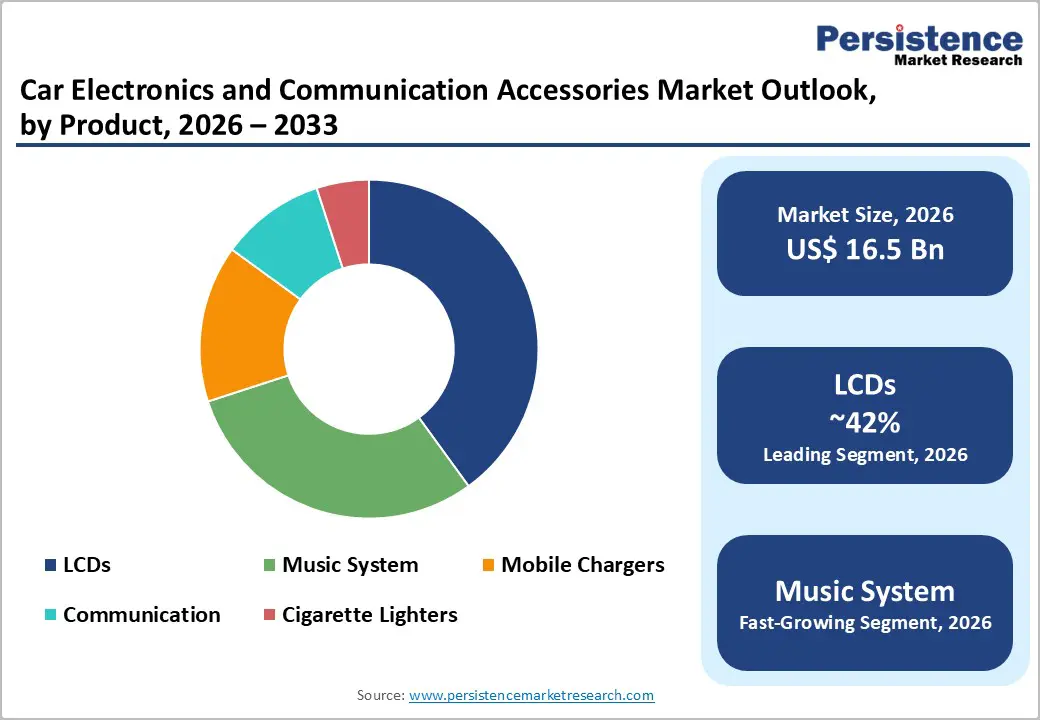

The global car electronics and communication accessories market size is likely to be valued at US$ 16.5 billion in 2026 and is projected to reach US$ 24.3 billion by 2033, growing at a CAGR of 5.7% between 2026 and 2033.

The market's steady expansion reflects fundamental shifts in consumer demand toward enhanced in-vehicle connectivity, entertainment systems, safety features, and seamless smartphone integration. Rising consumer spending on advanced car electronics, including infotainment systems, wireless charging solutions, and GPS navigation devices, has become essential for modern vehicle owners seeking superior driving experiences and connected mobility ecosystems.

Key Industry Highlights:

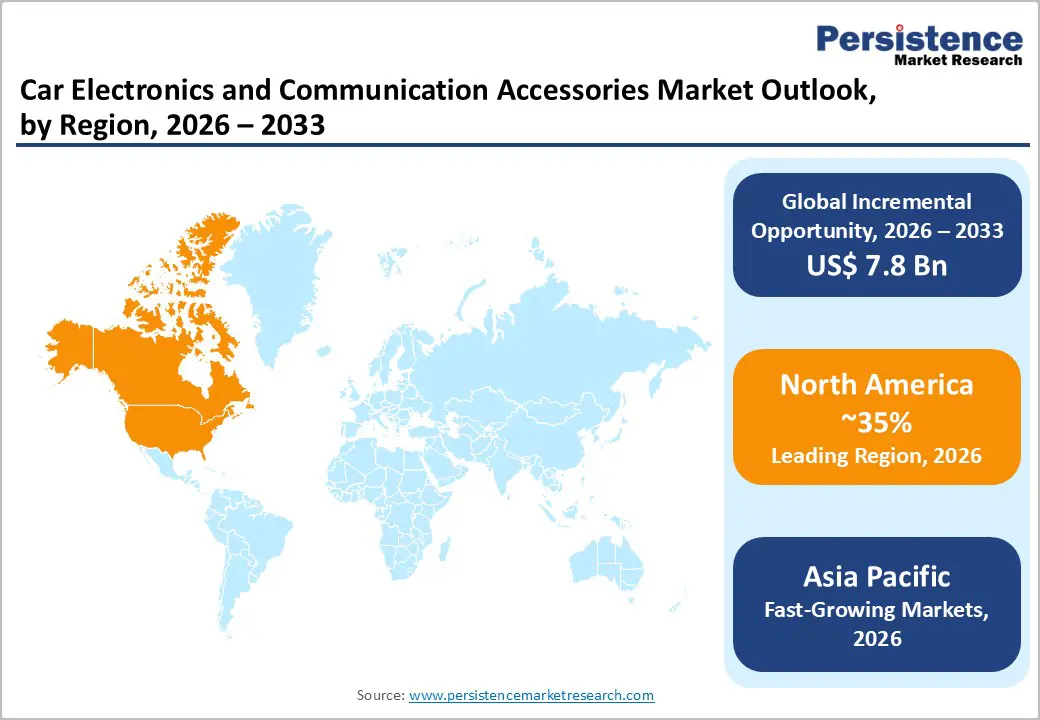

- North America remains the established market leader. It is likely to occupy a 35% of global share, driven by exceptional consumer spending on vehicle electronics, widespread aftermarket adoption, and established dealer networks providing professional installation services for advanced infotainment and communication accessories.

- Asia Pacific demonstrates the fastest regional growth at an 8.3% CAGR. Rising vehicle production, exceeding 50.74 million units annually; rapid electric-vehicle adoption; and government support for 5G infrastructure deployment are establishing Asia Pacific as the highest-growth region through 2033.

- LCDs are expected to dominate the product category, with a 42% share in 2026. Dashboard display units remain essential for navigation, entertainment, climate control, and telemetry visualization across all vehicle segments, with sophisticated touchscreen specifications and advanced display technologies driving product premiums.

- OEM channels are likely to lead with 72% share in 2026. Original equipment manufacturer channels maintain dominance through integrated electronics installation during vehicle assembly and through direct control over quality standards, cybersecurity protocols, and software integration.

- Market opportunity: 5G integration and autonomous vehicle connectivity represent a major market opportunity. Emerging vehicle-to-everything (V2X) communication platforms, telematics infrastructure expansion, and autonomous driving requirements create exceptional growth opportunities for advanced communication accessory manufacturers through 2033.

| Key Insights | Details |

|---|---|

| Car Electronics and Communication Accessories Market Size (2026E) | US$ 16.5 Bn |

| Market Value Forecast (2033F) | US$ 24.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.7% |

| Historical Market Growth (CAGR 2020 to 2024) | 4.6% |

Market Dynamics

Drivers - Accelerated Adoption of In-Vehicle Infotainment Systems and Advanced Connectivity Solutions

Consumer demand for sophisticated in-vehicle entertainment and communication systems is fundamentally transforming automotive electronics markets by integrating advanced display technologies, streaming capabilities, and personalized user experiences. The automotive infotainment systems market reached approximately USD 28.51 billion in 2026 and is expanding at 6.11% CAGR toward USD 38.35 billion by 2030, driven by consumer preferences for seamless smartphone integration, including Apple CarPlay and Android Auto compatibility. General Motors embedded Apple Music natively across its 2026 and 2026 model lineups, offering eight years of complimentary streaming to encourage brand loyalty and differentiation through integrated entertainment ecosystems. Voice recognition technology improvements of approximately 25% over five-year periods are substantially reducing driver distraction, with recognition systems now achieving 80% accuracy in noisy automotive environments, up from 50% historically.

Rising Vehicle Electrification and Connected Vehicle Infrastructure Development

The accelerating transition toward electric vehicles and connected automotive ecosystems is generating substantial demand for specialized electronics, including 5G-enabled telematics, high-voltage power management systems, and integrated diagnostic platforms. The automotive OEM telematics market is projected to expand from USD 39.5 billion in 2026 to USD 147.6 billion by 2035, with a 14.1% CAGR, driven by the widespread adoption of real-time connectivity, predictive maintenance diagnostics, and fleet management solutions. India's automotive OEM telematics market is expected to grow at a 17.6% CAGR, driven by AIS 140 compliance mandates mandating telematics integration in commercial vehicles to enhance safety and tracking capabilities. Project Convergence, the pioneering 5G-enabled hospital initiative at VA Palo Alto Health Care System involving Verizon, Microsoft, and Medivis, demonstrates how advanced connectivity infrastructure enables revolutionary real-time data transmission and remote operational capabilities increasingly demanded in connected vehicle platforms.

Restraints - Increasing Product Complexity and High Integration Costs Limiting Aftermarket Adoption

The complexity of automotive electronics integration is creating significant barriers to aftermarket product adoption and consumer accessibility, driven by escalating design sophistication, software compatibility challenges, and specialized installation requirements. Modern vehicles integrate 150+ electronic control units (ECUs) with increasingly complex interdependencies and software-driven architectures requiring specialized diagnostic equipment and technician expertise substantially exceeding traditional automotive repair capabilities. Integration of vehicle Car Electronics and Communication Accessories into existing vehicle systems demands compliance with proprietary protocols including CAN, Ethernet, and advanced automotive cybersecurity standards, creating technical barriers for third-party accessory manufacturers and limiting consumer installation options. Aftermarket product development timelines have extended to 18-24 months, up from historical 6-9-month cycles, due to the need for vehicle platform compatibility validation, cybersecurity certification testing, and OEM approval processes.

Supply Chain Vulnerabilities and Critical Semiconductor Shortages Constraining Production

Global semiconductor shortage persistence and supply chain fragmentation are creating substantial production constraints limiting market growth through extended lead times, inventory volatility, and elevated component costs. Automotive semiconductor demands continue exceeding supply capacity, with critical chip categories including microcontrollers, power management integrated circuits, and display drivers facing chronic allocation restrictions from foundries prioritizing higher-margin consumer electronics applications.

Battery management and power electronics semiconductors, essential for electric vehicle connectivity and advanced infotainment systems, remain constrained despite foundry capacity expansions announced by Taiwan Semiconductor Manufacturing Company (TSMC) and Samsung Electronics. Japan's critical shortage of rare-earth materials, combined with China's strategic control over lithium, cobalt, and graphite extraction and processing, has created material supply vulnerabilities that directly impact the production of wireless charging systems, GPS components, and advanced display technologies.

Opportunities - Autonomous Vehicle Development and Vehicle-to-Everything (V2X) Communication Infrastructure

The rapid advancement of autonomous vehicle development and the deployment of vehicle-to-everything communication infrastructure represent a transformative market opportunity for electronics and communications accessory manufacturers specializing in advanced connectivity solutions. Autonomous vehicles require next-generation Car Electronics and Communication Accessories, including ultra-low latency 5G communication systems, redundant sensor interfaces, and real-time vehicle-to-infrastructure (V2I) communication platforms enabling instantaneous hazard detection and coordinated traffic management. The 5G in the automotive and smart transportation market is projected to reach USD 31.18 billion by 2034 from USD 2.58 billion in 2024, representing 29.8% CAGR driven by the deployment of vehicle connectivity platforms supporting autonomous driving operations. World Economic Forum forecasts indicate autonomous vehicles could represent 10% of global vehicle sales by 2030, requiring widespread integration of communication systems, sensors, and compute infrastructure manufacturers currently unable to meet demand scaling requirements.

Aftermarket Digital Services and Predictive Maintenance Platform Integration

The emergence of digital aftermarket service ecosystems and predictive maintenance platforms presents an exceptional market opportunity for electronics manufacturers that integrate diagnostic capabilities, telematics, and condition-monitoring functionality into vehicle accessory ecosystems. The global automotive digital aftermarket service market is projected to grow from USD 51.04 billion in 2026 to USD 130.96 billion by 2034, expanding at approximately 15% CAGR driven by rising connected vehicle adoption and demand for predictive diagnostics and remote maintenance capabilities. Bosch's integrated suite of smart diagnostics tools, E-HEALTH-Charge battery diagnostic systems that enable 15-minute battery health assessments, and TechPRO® 2 diagnostic equipment featuring artificial intelligence capabilities exemplify emerging business model trends that integrate advanced electronics with software-driven service platforms. Independent service networks and aftermarket repair operators increasingly adopt digital diagnostic platforms, creating demand for accessory manufacturers offering modular integration with existing workshop infrastructure and mobile application interfaces.

Category-wise Analysis

Product Type Insights

LCDs dominate the automotive electronics and communication accessories market with approximately 42% market share, driven by essential dashboard display integration requirements and rapid adoption of touchscreen interfaces across vehicle segments. Liquid crystal displays are the fundamental infotainment technology that enables navigation systems, entertainment interfaces, climate-control interfaces, and telemetry visualization, making LCD products universal across modern automotive platforms.

Modern LCD installations feature increasingly sophisticated specifications, including 10-15-inch diagonal screens, 1920 x 1200 pixel or higher resolutions, capacitive touchscreen technologies enabling smartphone-like responsiveness, and integrated Gorilla Glass protection against UV exposure and mechanical abrasion. Automotive-grade LCD displays integrate specialized environmental hardening, including wide-temperature operation (-30°C to +85°C), glare-reduction coatings for sunlight visibility optimization, and vibration-resistant mounting systems withstanding sustained vehicle acceleration and road impacts.

Vehicle Type Insights

Passenger cars maintain dominant market position with approximately 68% market share, reflecting substantially larger production volumes and greater per-vehicle electronics content compared to commercial vehicles. Premium and luxury passenger vehicle segments demonstrate accelerated electronics adoption, with Mercedes-Benz, BMW, and Audi vehicles averaging 18-24 integrated electronic components compared to mainstream segment vehicles averaging 12-15 components. Light Commercial Vehicles account for approximately 22% of the market and are experiencing accelerated growth at a 6.8% CAGR, driven by fleet operators' adoption of telematics systems for electronic logging compliance, driver coaching applications, and predictive maintenance optimization.

Euler Motors, an Indian electric vehicle startup, has equipped delivery vans with 10-inch Chimera head units integrating geofencing and predictive maintenance dashboards, exemplifying emerging business model trends. Commercial vehicle segments demonstrate highest aftermarket electronics adoption rates, with fleet operators upgrading communication systems, navigation platforms, and telematics solutions to support evolving regulatory compliance and operational efficiency requirements.

Sales Channel Insights

OEM (Original Equipment Manufacturer) channels maintain a dominant position with approximately 72% share, driven by vehicle manufacturer preference for integrated electronics installed during assembly and OEM direct control over quality standards, cybersecurity protocols, and software integration. OEM manufacturing relationships provide manufacturers with preferred supplier status, long-term volume commitments, and standardized pricing structures enabling cost optimization through production scale economies. OEM segment demonstrates resilience despite cyclical automotive production fluctuations, as original equipment manufacturers maintain design continuity and component requirements across model generations and market segments.

Aftermarket channels represent approximately 28% market share and are expanding at 7.8% CAGR, driven by increasing vehicle fleet age, consumer demand for feature upgrades, cost-effective repair alternatives, and rapid technological obsolescence, encouraging aftermarket accessory additions. Aftermarket expansion is facilitated by expanding e-commerce platforms, direct-to-consumer sales channels, and simplified product installation interfaces reducing technician skill requirements.

Regional Insights

North America Car Electronics and Communication Accessories Market Share and Trends

North America maintains established market leadership position driven by exceptional consumer spending on vehicle electronics, advanced manufacturing infrastructure, and widespread adoption of premium infotainment systems across mainstream vehicle segments. The United States market represents approximately 68% of regional revenue, supported by high average consumer vehicle spending, substantial aftermarket accessory installation adoption, and extensive dealer networks providing professional installation and integration services. Project Convergence, the pioneering 5G-enabled surgical infrastructure at VA Palo Alto Health Care System involving Microsoft HoloLens 2, Verizon 5G infrastructure, and Medivis surgical visualization technology, demonstrates how advanced connectivity standards are cascading into automotive applications.

Canada's automotive aftermarket demonstrates strong growth momentum, with independent repair networks and consumer retailers expanding electronics installation offerings. Mexico's role as a significant automotive manufacturing hub creates substantial OEM demand for integrated electronic systems, navigation platforms, and communication modules incorporated into vehicles assembled for North American distribution.

Europe Car Electronics and Communication Accessories Market Share and Trends

Europe represents the second-largest regional market with approximately 26% global market share, characterized by stringent regulatory frameworks, emphasis on sustainable technologies, and leading-edge connectivity infrastructure development. Germany, the region's primary automotive manufacturing hub, accounts for approximately 34% of European market value, supported by Bosch, Continental, and Harman regional headquarters and substantial automotive electronics research and development investments. Germany's Federal Ministry of Health reports that VR-based therapies achieve a 25% reduction in treatment costs and a 30% increase in recovery rates, indicating broader government support for advanced technology infrastructure relevant to automotive electronics development.

The automotive markets of the United Kingdom, France, and Spain demonstrate accelerating adoption of connected vehicle platforms and wireless charging infrastructure. European regulatory frameworks, including the General Data Protection Regulation (GDPR) and emerging cybersecurity directives, are establishing stringent data protection requirements influencing automotive electronics design specifications and cloud infrastructure integration strategies.

Asia Pacific Car Electronics and Communication Accessories Market Share and Trends

Asia Pacific emerges as the fastest-growing regional market, expanding at approximately 8.3% CAGR and projected to command approximately 30% global market share by 2033 through extraordinary vehicle production volumes and rapid technological adoption. China leads regional growth with 31.28 million vehicles produced in 2024, including 10 million new-energy models, establishing the region as the primary demand engine for advanced automotive electronics and communication accessories.

Japan maintains technological leadership through advanced automotive electronics manufacturing, with companies such as Panasonic, Sony, Alpine, Clarion, and Kenwood pioneering innovative infotainment systems, premium audio solutions, and wireless charging technologies. India's automotive production, which is expanding at a 6.2% CAGR through government support programs, including the Production-Linked Incentive scheme, is generating substantial demand for cost-effective automotive electronics platforms that balance affordability with essential connectivity and entertainment features.

Competitive Landscape

The car electronics and communication accessories market exhibits moderate consolidation with dominant global technology suppliers, including Bosch, Continental, Harman, Panasonic, Sony, and Alpine commanding approximately 65% of aggregated market share through comprehensive product portfolios, established OEM relationships, and advanced research and development capabilities.

Market leaders pursue growth through strategic acquisition of specialized electronics companies, establishment of enterprise partnerships with automotive manufacturers, and substantial investment in emerging technologies, including 5G connectivity, artificial intelligence, and autonomous driving platforms. Competitive differentiation increasingly reflects software capabilities, cloud platform integration, and over-the-air update competencies rather than traditional hardware specifications. Emerging business models include subscription-based infotainment services, predictive maintenance platforms, and integrated telematics ecosystems generating recurring revenue streams and enhancing customer lifetime value beyond traditional component sales.

Key Developments:

- In March 2024, Panasonic Corporation introduced a new range of AI-powered infotainment systems designed for next-generation connected vehicles. The new systems focus on seamless smartphone integration, improved voice control, and immersive sound, enhancing in-car entertainment and communication experiences.

- In July 2024, Sony Corporation announced a strategic partnership with Honda to co-develop advanced in-vehicle communication platforms for electric cars. This collaboration aims to deliver high-quality entertainment and safety-focused communication systems tailored for EVs, supporting Sony’s diversification into automotive electronics.

Companies Covered in Car Electronics and Communication Accessories Market

- Panasonic Corporation

- Pioneer Corporation

- Sony Corporation

- Robert Bosch GmbH

- Alpine Electronics, Inc.

- Harman International Industries

- Clarion Co., Ltd.

- Continental AG

- Delphi Technologies

- Kenwood Corporation

- Other Key Players

Frequently Asked Questions

The global Car Electronics and Communication Accessories market was valued at US$ 16.5 billion in 2026 and is projected to reach US$ 24.3 billion by 2033, expanding at a 5.7% CAGR.

Primary growth drivers include accelerating adoption of sophisticated infotainment systems, achieving 6.11% CAGR expansion, rapid electric vehicle adoption requiring specialized electronics and telematics integration, 5G connectivity deployment enabling vehicle-to-everything communication.

LCDs dominate with approximately 42% market share, driven by essential dashboard display integration requirements, touchscreen interface adoption across vehicle segments, and rapid expansion to 10-15-inch high-resolution displays.

North America maintains established market leadership with approximately 35% of the global market share, driven by exceptional consumer spending and advanced manufacturing infrastructure.

Market leaders include Panasonic Corporation, commanding comprehensive infotainment and premium audio portfolios; Robert Bosch GmbH, pioneering integrated vehicle computing platforms, Harman International Industries (Samsung subsidiary), leading advanced telematics and connectivity solutions.