- Pharmaceuticals

- Bronchial Spasm Market

Bronchial Spasm Market Size, Share, and Growth Forecast, 2026 - 2033

Bronchial Spasm Market by Diagnosis Type (Spirometry Tests, Imaging Tests, Complementary Technologies), Treatment Type (Bronchodilators, Combination Therapies, Inhaled Steroids, Intravenous Steroids), End-User (Hospitals, Homecare Settings, Specialty Clinics), and Regional Analysis for 2026-2033

Bronchial Spasm Market Share and Trends Analysis

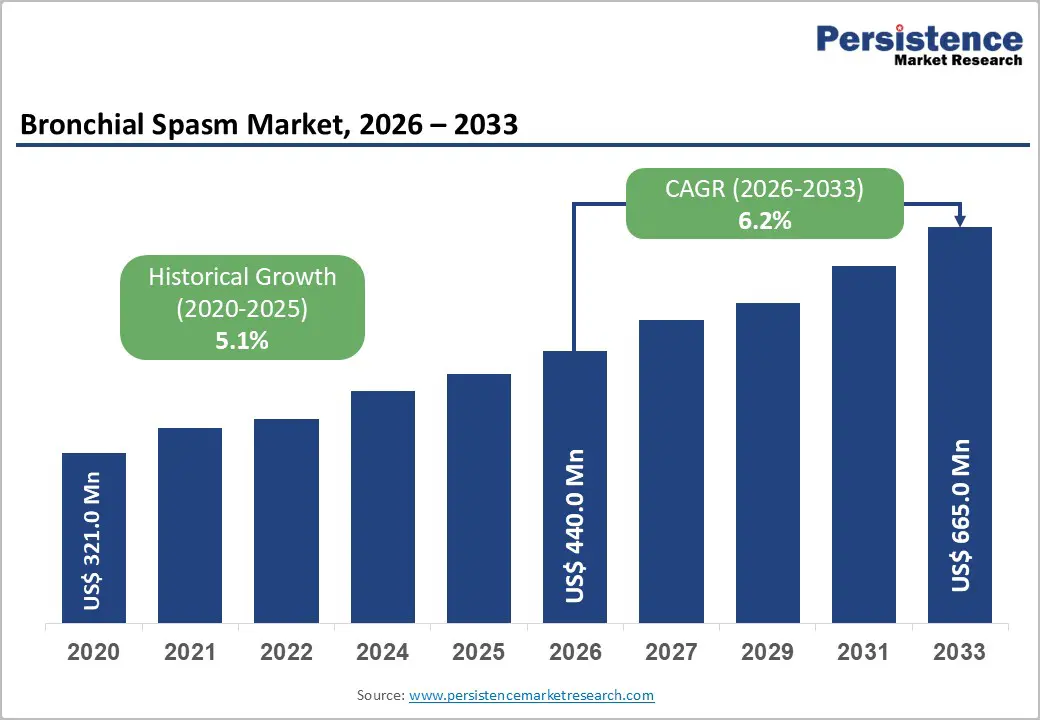

The global bronchial spasm market size is likely to be valued at US$ 440.0 million in 2026, and is projected to reach US$ 665.0 million by 2033, growing at a CAGR of 6.2% during the forecast period 2026−2033. This growth is primarily driven by the rising global prevalence of respiratory disorders such as asthma and chronic obstructive pulmonary disease (COPD), which are continuing to increase across both developed and emerging economies. Urban air pollution, occupational exposure, smoking prevalence, and aging populations are collectively intensifying disease burden, thereby expanding the addressable patient pool requiring bronchial spasm management.

Market momentum is further strengthening as pharmaceutical and medical device companies advance bronchodilator drug formulations and inhalation delivery technologies that improve therapeutic efficacy and patient adherence. Innovations such as smart inhalers, dose-tracking devices, and improved aerosol delivery systems are supporting earlier intervention and better disease control. At the same time, healthcare systems are expanding diagnostic capabilities and outpatient respiratory care pathways, which are enabling timely detection and continuous management of bronchial conditions. Rising healthcare expenditure and increasing awareness of long-term respiratory health management are expected to reinforce sustained demand for effective bronchial spasm treatments across hospital, clinic, and homecare settings.

Key Industry Highlights

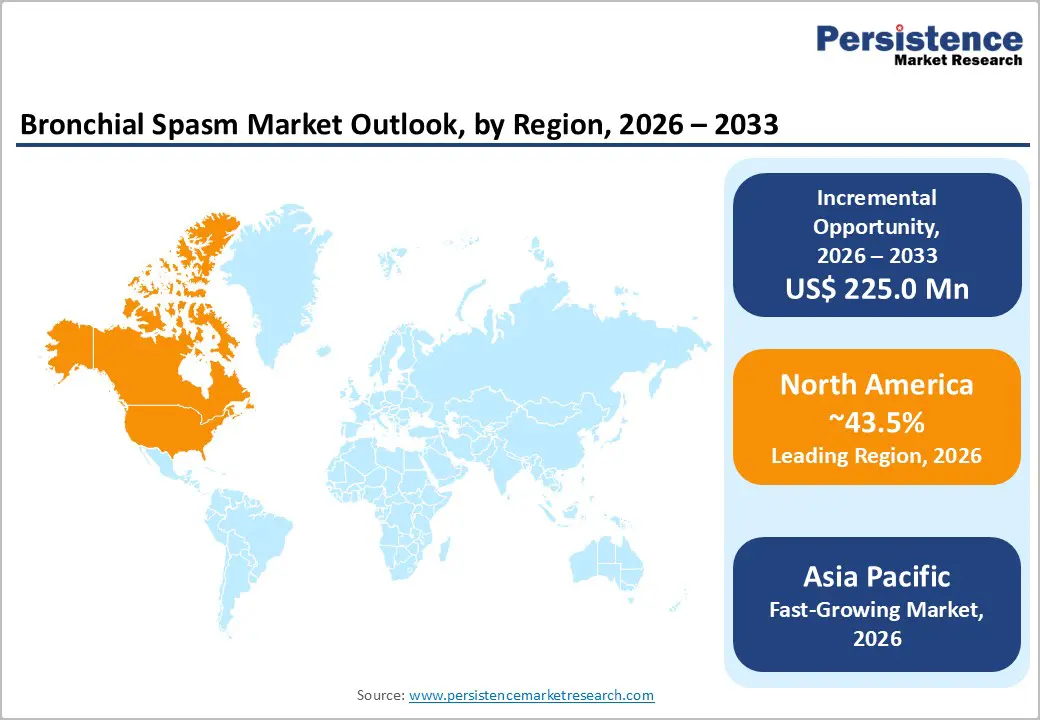

- Dominant Region: North America is expected to command about 43.5% market share in 2026, aided by comprehensive insurance coverage and effective disease management programs.

- Fastest-growing Market: The Asia Pacific market is slated to be the fastest-growing from 2026 to 2033, due to rapidly improving healthcare infrastructure and access.

- Leading & Fastest-growing Diagnosis Type: Spirometry tests are expected to account for approximately 45% of market revenue, while imaging tests are likely to be the fastest-growing segment during the 2026-2033 forecast period.

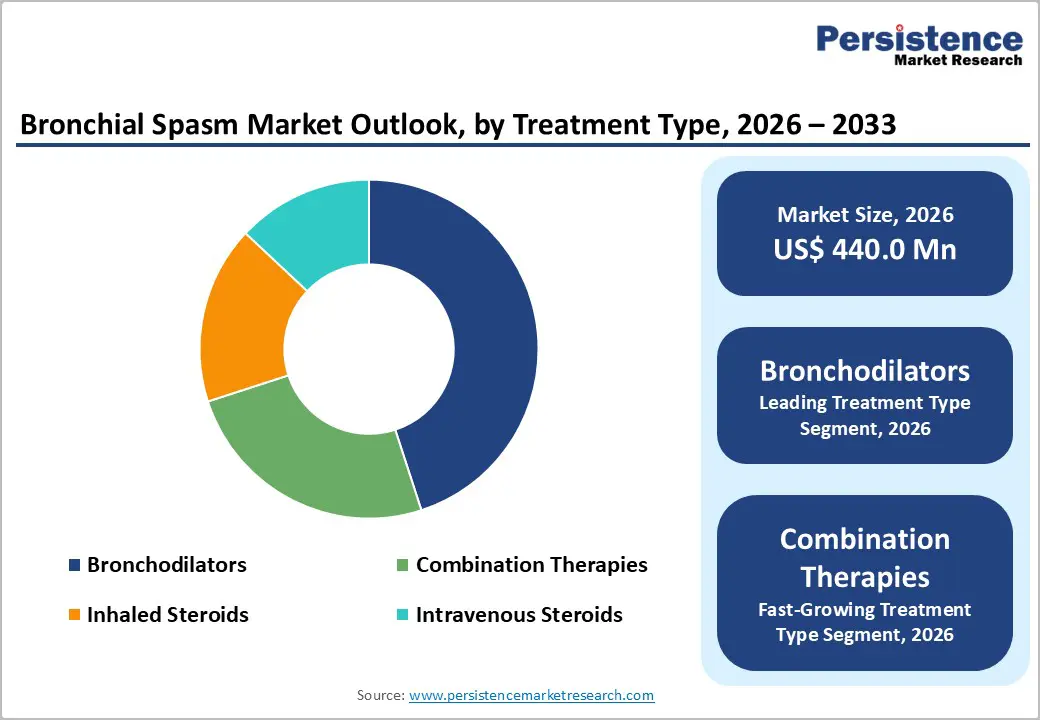

- Leading & Fastest-growing Treatment Type: Bronchodilators are projected to capture an estimated 56.4% revenue share in 2026, while combination therapies are expected to be the fastest-growing segment over the 2026-2033 forecast period.

- November 2025: A King's College London-led WAYFINDER trial showed that monthly tezepelumab injections enable 90% of severe asthma patients to reduce daily oral steroids, improve symptoms, lung function, and quality of life, and cut attacks by two-thirds.

| Key Insights | Details |

|---|---|

| Bronchial Spasm Market Size (2026E) | US$ 440.0 Mn |

| Market Value Forecast (2033F) | US$ 665.0 Mn |

| Projected Growth (CAGR 2026 to 2033) | 6.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Technological Advancements in Inhalation Device Technology

Innovations in pharmaceutical drug delivery systems are transforming the management of bronchial spasm by enabling more precise, patient-centric care. Next-generation bronchodilators provide more consistent symptom relief and better tolerability profiles, helping clinicians design treatment plans that are both effective and easier for patients to follow. Inhalation platforms such as metered dose inhalers, dry powder inhalers and nebulizers now incorporate advanced formulations that improve deposition in the lower airways, supporting more predictable clinical responses and faster relief for acute episodes. These advances allow healthcare providers to tailor therapies to individual inhalation technique, disease severity and care settings, strengthening long-term disease control.

Digital inhaler devices with integrated adherence tracking and real-time feedback capabilities add an additional layer of value by closing long-standing gaps between prescription and actual use. By giving clinicians objective insight into usage patterns and technique quality, these connected systems support earlier interventions and more informed therapy adjustments. Combination inhaler therapies that unite dual bronchodilators with corticosteroids in a single device simplify regimens and strengthen inflammation control, while nanoparticle-based aerosol delivery systems enhance targeting within the bronchial tree for more focused bronchodilator action. Together, these innovations elevate standards of care, create differentiation opportunities for manufacturers and open avenues for integrated disease management solutions across hospital, outpatient and home-care environments.

Stringent Regulatory Requirements and Compliance Challenges

Regulatory complexity remains a structural constraint for the bronchial spasm market, as companies must navigate stringent requirements at every stage of the product lifecycle. Agencies such as the United States Food and Drug Administration (FDA) and the European Medicines Agency (EMA) require detailed evidence on quality, safety and efficacy, which compels manufacturers to commit significant time and capital to clinical development and documentation. These expectations extend into the post-marketing phase, where ongoing safety monitoring, risk management plans and periodic reporting obligations add operational overhead and demand specialized regulatory capabilities. This environment can shift the internal focus from early-stage innovation to compliance management, slowing the pace at which differentiated therapies reach patients.

Differences in regulatory standards, data requirements, and review practices across regions create additional hurdles for multinational pharmaceutical companies pursuing coordinated global launches. Firms often need to adapt trial designs, labeling, pharmacovigilance systems and pricing strategies to meet local expectations, which increases complexity and lengthens timelines for market access. The cumulative effect is that regulatory review cycles can lag behind emerging clinical needs, particularly in fast-evolving areas such as digital inhaler technologies and novel combination therapies. Companies that invest early in cross-regional regulatory planning, scalable evidence-generation platforms and proactive engagement with authorities are better positioned to reduce approval delays and preserve competitive agility in this constrained environment.

Development in Biologic Therapies and Targeted Treatments

Growth in biologic therapies that target underlying inflammatory pathways in bronchial spasms is creating meaningful headroom for pharmaceutical innovation and portfolio differentiation. Monoclonal antibodies such as benralizumab, which deplete eosinophils that drive airway inflammation, offer a more targeted mechanism of action than oral corticosteroid tablets and can help clinicians manage eosinophilic asthma and COPD more precisely. Evidence from clinical studies indicates that administering a single dose during exacerbations can reduce subsequent treatment needs, shifting care models toward event-triggered interventions and potentially lessening cumulative steroid exposure over time. This development creates an opportunity to position biologics as high-value options within stepwise treatment algorithms, particularly for patients who remain uncontrolled on standard inhaled therapies.

Tezspire (tezepelumab), approved by the U.S. FDA as an add-on maintenance therapy for severe asthma in individuals aged 12 years and older, illustrates how targeting upstream mediators such as thymic stromal lymphopoietin can broaden eligibility beyond traditional phenotype-restricted treatments. Its mechanism extends the therapeutic reach to patients who do not fit classic eosinophilic or allergic profiles, encouraging payers and healthcare providers to re-evaluate how they segment and prioritize severe asthma populations. The development of novel long-acting muscarinic antagonists and other targeted bronchodilator classes is improving bronchial smooth muscle relaxation while supporting maintenance-oriented care strategies.

Category-wise Analysis

Diagnosis Type Insights

Spirometry tests are expected to dominate in 2026, capturing approximately 45% of the bronchial spasm market share, driven by their status as the gold standard for assessing lung function and diagnosing bronchospastic conditions. Spirometry measures the volume and speed of air movement during inhalation and exhalation, providing critical metrics including forced vital capacity (FVC), forced expiratory volume in the first second (FEV1), and the FEV1/FVC ratio that definitively identify airway obstruction patterns characteristic of bronchial spasm. Healthcare providers rely on spirometry as the primary diagnostic tool for distinguishing between obstructive lung diseases, such as asthma and COPD, and restrictive lung disorders, making it indispensable for accurate diagnosis and treatment planning.

Imaging tests are likely to be the fastest-growing segment during the 2026-2033 forecast period. This segment encompasses chest X-rays, computed tomography (CT) scans, including high-resolution CT (HRCT), and emerging magnetic resonance imaging (MRI) applications utilizing hyperpolarized gas technology. While imaging tests do not directly diagnose bronchospasm itself, they play critical roles in excluding alternative diagnoses such as pneumonia, lung tumors, bronchiectasis, and structural airway abnormalities that present with similar symptoms, and in identifying complications associated with chronic bronchospastic conditions including hyperinflation, mucus plugging, and bronchial wall thickening.

Treatment Type Insights

Bronchodilators are expected to be the dominant application segment, accounting for around 56.4% of market revenue in 2026, driven by their role as first-line therapy for acute symptom relief and long-term disease management. Short-acting bronchodilators (SABAs), including albuterol and levalbuterol, provide rapid relief during acute bronchospasm episodes, making them essential rescue medications. Long-acting bronchodilators, including beta-agonists (LABAs) such as salmeterol, formoterol, and indacaterol, and long-acting muscarinic antagonists (LAMAs) such as aclidinium, offer sustained bronchodilation for chronic disease management.

Combination therapies are expected to be the fastest-growing segment over the 2026-2033 forecast period. LABA/ICS combinations and LABA/LAMA combinations simplify treatment regimens to once-daily administration, significantly improving patient adherence compared to multiple separate medications. These comprehensive treatment approaches demonstrate superior efficacy in reducing exacerbations and improving quality-of-life metrics, commanding premium pricing that drives revenue growth despite representing lower prescription volumes than individual bronchodilator products.

End-User Insights

Hospitals are well positioned to lead, with an approximate 55% share of the bronchial spasm market in 2026, owing to their role in managing acute exacerbations that require immediate intervention and specialized care. Hospital emergency departments serve as primary access points for patients experiencing severe bronchospasm incidences, administering nebulized bronchodilators, systemic corticosteroids, and advanced therapies, including parenteral medications. Inpatient respiratory units provide comprehensive diagnostic evaluation, treatment optimization, and patient education programs. The presence of specialized pulmonary function laboratories within hospital settings enables advanced diagnostic testing, including bronchoprovocation studies and comprehensive lung function assessment, supporting precise therapeutic decision-making.

Home care settings are projected to be the fastest-growing segment during the 2026-2033 forecast period. The shift toward homecare reflects multiple factors, including cost-containment initiatives, patient preference for home-based treatment, and technological advancements that enable effective at-home therapy delivery. Portable nebulizers, smart inhalers with connectivity features, and telehealth monitoring platforms now facilitate safe and effective home management of chronic bronchospasm. Specialty clinics focusing on respiratory medicine also demonstrate strong growth because they offer specialized expertise, comprehensive disease management programs, and access to novel therapies such as biologics that require specialized administration and monitoring protocols unavailable in general practice settings.

Regional Insights

North America Bronchial Spasm Market Trends

North America is anticipated to secure the largest portion of the bronchial spasm market share at approximately 43.5% in 2026, on the back of its advanced healthcare infrastructure with comprehensive insurance coverage and effective disease management programs. The United States serves as the primary revenue driver due to high prevalence of respiratory disorders and widespread access to specialized respiratory care. Agencies such as the Asthma and Allergy Foundation of America (AAFA) and the Centers for Disease Control and Prevention (CDC) document significant patient populations that require consistent therapeutic interventions. These structural advantages create a stable demand environment in which providers and payers prioritize proven clinical outcomes over cost alone.

The United States FDA has established clear approval pathways that balance innovation speed with rigorous safety standards, which enables rapid adoption of novel biologic therapies and advanced combination products. Canada and Mexico contribute to regional expansion through healthcare access initiatives and growing awareness of respiratory disease management. Investment flows toward personalized medicine platforms, digital health solutions, and specialty pharmacy networks serving complex patient populations that require sophisticated therapeutic protocols.

Europe Bronchial Spasm Market Trends

Europe serves as the second-largest regional market for bronchial spasm treatments with key contributions from Germany, the United Kingdom, France, Spain, and Italy. Aging demographics drive consistent demand, while universal healthcare systems ensure broad access to treatment across member states. Germany leads European markets due to its established healthcare infrastructure and high pharmaceutical consumption. The UK's National Health Service (NHS) implements comprehensive asthma and COPD management programs that standardize treatment protocols and medication utilization.

The EMA has facilitated regulatory harmonization, streamlining market entry for new therapies across member states, though country-specific reimbursement decisions introduce market variation. France demonstrates strong adoption of combination therapies and biologic treatments supported by government policies that prioritize quality outcomes. Spain and Italy increase penetration of generic bronchodilators to balance cost containment with clinical requirements. European markets emphasize evidence-based medicine and health technology assessments (HTAs) that shape treatment guidelines and reimbursement frameworks. Investment opportunities emerge for cost-effective therapies that address budget constraints while meeting clinical effectiveness standards amid post-pandemic financial pressures and demographic shifts requiring expanded respiratory capacity.

Asia Pacific Bronchial Spasm Market Trends

Asia Pacific is projected to be the fastest-growing market for bronchial spasm treatments between 2026 and 2033, driven by large populations, rising disease prevalence, and improving healthcare infrastructure. China represents the largest market in the region, benefiting from government healthcare reforms that expand insurance coverage and medication access. India demonstrates rapid growth potential, with its enormous population, rising air pollution levels contributing to the respiratory disease burden, and expanding pharmaceutical manufacturing capabilities supporting both domestic consumption and export opportunities. Japan maintains a mature market characterized by an aging population, high per capita healthcare spending, and sophisticated clinical practices that incorporate advanced diagnostic and therapeutic technologies.

ASEAN nations, including Indonesia, Thailand, and Vietnam, exhibit emerging market dynamics with growing middle classes demanding improved healthcare services. Manufacturing advantages across the region, particularly in India and China, enable the production of affordable generic medications, increasing treatment accessibility while maintaining market profitability through volume growth. Regulatory environments vary significantly across Asia Pacific countries, creating both challenges and opportunities for market entry strategies. Investment trends emphasize affordable innovation, digital health integration to support remote patient populations, and capacity building in respiratory specialty care to address the growing disease burden and evolving patient expectations in rapidly developing healthcare markets.

Competitive Landscape

The global bronchial spasm market structure features moderate consolidation, with GlaxoSmithKline, AstraZeneca, Boehringer Ingelheim, Novartis, and Merck accounting for a significant share of global revenues. These players are strengthening their market positions by focusing on differentiated respiratory portfolios that combine proven active molecules with improved delivery mechanisms. Competitive strategies are increasingly emphasizing patient-centric product design, where ease of use, dosing accuracy, and treatment adherence are becoming critical decision factors for physicians, payers, and healthcare systems.

Market leaders are continuing to invest heavily in clinical research and post-marketing studies to demonstrate superior clinical outcomes, long-term safety, and health economic benefits of their therapies. Evidence generation supporting reduced exacerbation rates, improved lung function, and lower hospitalization costs is playing a central role in securing favorable reimbursement and formulary inclusion. At the same time, the competitive environment is intensifying as patent expirations are enabling the entry of generic bronchodilators, which are increasing price competition in cost-sensitive markets. This dynamic is pushing branded manufacturers to accelerate innovation in combination therapies, device-enabled drug delivery, and lifecycle management strategies to protect market share while maintaining pricing power.

Key Industry Developments

- In December 2025, Amneal Pharmaceuticals received U.S. FDA approval for its albuterol sulfate inhalation aerosol (90 mcg per actuation), the generic equivalent of Teva's ProAir HFA. Indicated for treating or preventing bronchospasm in adults and children aged 12+, the product enters a market with approximately US$ 1.5 billion in the U.S.

- In October 2025, Merck completed its US$ 10 billion acquisition of Verona Pharma, integrating Ohtuvayre® (ensifentrine), a first-in-class inhaled dual PDE3/PDE4 inhibitor for COPD maintenance treatment in adults, into its cardio-pulmonary portfolio.

- In September 2025, Oxford University led a £1.3 million Engineering and Physical Sciences Research Council (EPSRC)-funded project to develop a novel 12-minute breathing test using computed cardiopulmonary graphy that analyzes normal airflow patterns to detect early-stage asthma and COPD more accurately than spirometry.

Companies Covered in Bronchial Spasm Market

- GlaxoSmithKline plc

- AstraZeneca

- Boehringer Ingelheim International GmbH

- Merck & Co., Inc.

- Novartis AG

- Teva Pharmaceutical Industries Ltd.

- Sanofi S.A.

- Pfizer Inc.

- Viatris Inc.

- Sunovion Pharmaceuticals Inc.

- Cipla Ltd.

- Nephron Pharmaceuticals Corporation

- Amphastar Pharmaceuticals

- Sandoz AG

- Lupin Pharmaceuticals, Inc.

Frequently Asked Questions

The global bronchial spasm market is projected to reach US$440.0 Mn in 2026.

The bronchial spasm market size is around US$387.4 Mn as of The market is driven by the rising prevalence of chronic respiratory diseases worldwide, technological advancements in diagnostics/therapeutics, and supportive regulatory frameworks.

The market is poised to witness a CAGR of 6.2% from 2026 to 2033.

Soaring incidence of pollution-induced respiratory conditions in emerging economies, biologic therapy innovation, and digital health integration have created substantial growth potential for the market.

GlaxoSmithKline plc, AstraZeneca, Boehringer Ingelheim GmbH, Novartis AG, and Merck & Co., Inc are some of the key players in the market.