- Medical Devices

- Bioimpedance Spectroscopy Market

Bioimpedance Spectroscopy Market Size, Share, and Growth Forecast, 2026 - 2033

Bioimpedance Spectroscopy Market By Product Type (Multi-frequency BIS Systems, Single-frequency BIS Systems, Others), Application (Lymphedema Assessment, Oncology Monitoring, Others), End-user, and Regional Analysis for 2026 - 2033

Bioimpedance Spectroscopy Market Size and Trends Analysis

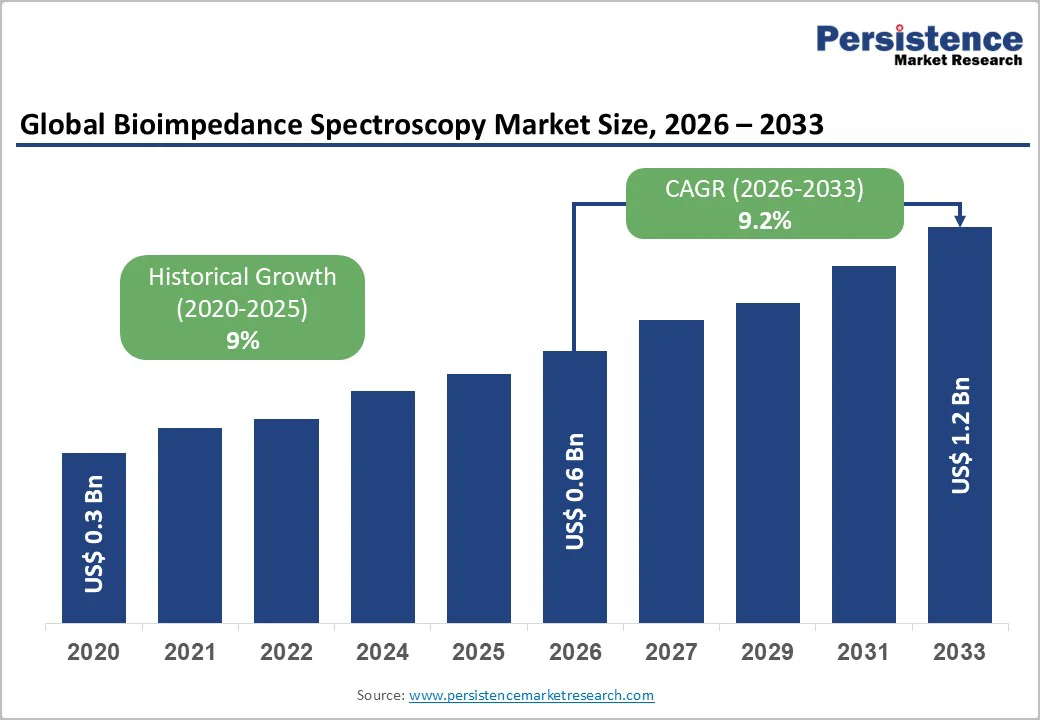

The global bioimpedance spectroscopy market size is likely to be valued at US$0.6 Billion in 2026 and is expected to reach US$1.2 Billion by 2033, growing at a CAGR of 9.2% during the forecast period from 2026 to 2033, driven by rising adoption of body composition assessment technologies, increased prevalence of chronic diseases, and advancements in non-invasive diagnostic tools. Healthcare digitization and clinical demand for real-time physiological monitoring also reinforce market expansion. Clinical acceptance across hospitals and research institutes continues to strengthen the commercial potential of bioimpedance technology.

Key Industry Highlights

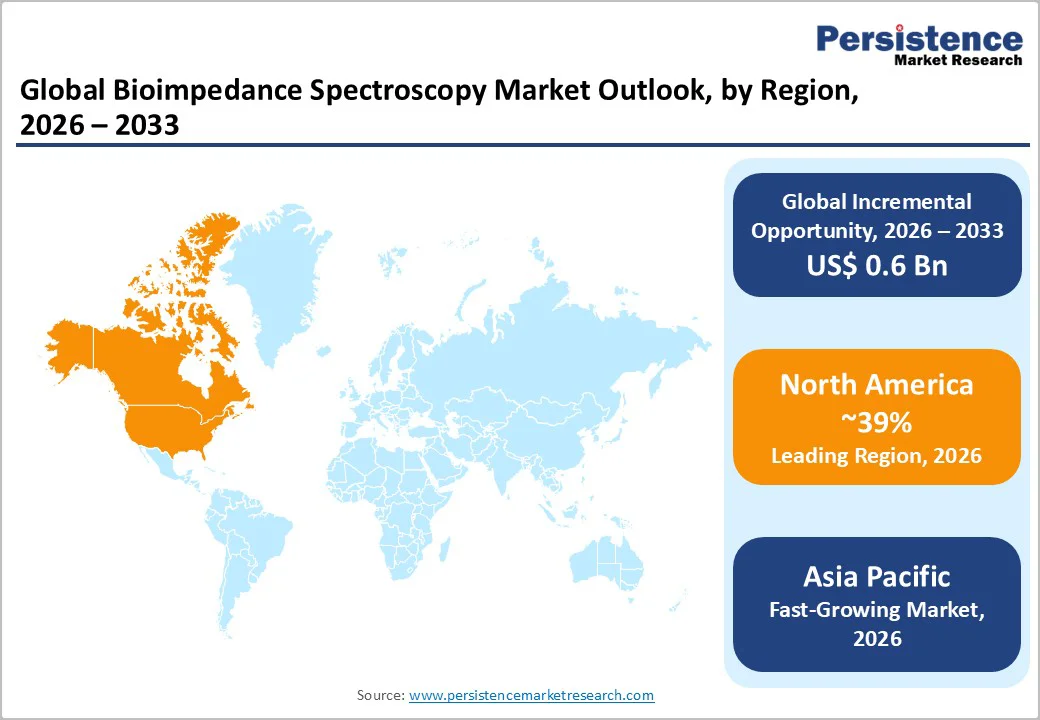

- Leading Region: North America is likely to be the largest regional market, accounting for about 39% of global BIS revenue, supported by advanced clinical adoption, premium system pricing, and higher utilization across oncology, cardiology, and dialysis programs.

- Fastest-growing Region: Asia Pacific is anticipated to be the fastest-growing region, driven by large NCD populations, rapid outpatient infrastructure expansion, and strong demand for affordable portable BIS platforms.

- Investment Plans: Manufacturers are directing over 25–30% of annual growth spending toward portable multi-frequency systems, subscription-based analytics platforms, and regional expansion initiatives, particularly in North America, Europe, and Asia Pacific.

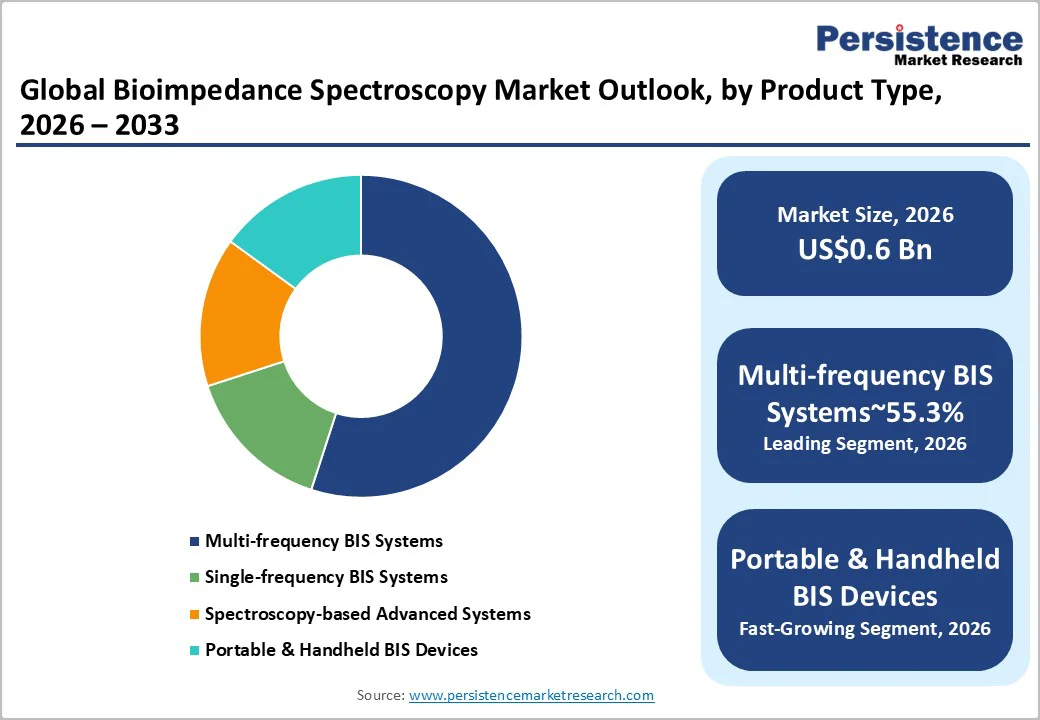

- Dominant Product: Multi-frequency BIS systems are projected to account for nearly 55.3% of the market share in 2026, due to their clinical precision, higher ASPs, and widespread use in hospitals and specialty clinics.

- Leading Application: The lymphedema screening and management segment is anticipated to remain the highest-value application, contributing about 37.5% of the revenue, supported by adoption across oncology survivorship programs and rehabilitation centers.

| Key Insights | Details |

|---|---|

| Bioimpedance Spectroscopy Market Size (2026E) | US$0.6 Bn |

| Market Value Forecast (2033F) | US$1.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis - Increasing Burden of Chronic and Metabolic Disorders

The prevalence of obesity, cardiovascular disease, diabetes, and renal disorders continues to rise across both developed and emerging markets. Government health statistics consistently indicate an upward trend in conditions associated with fluid imbalance and metabolic dysfunction. Bioimpedance spectroscopy (BIS) provides a non-invasive, rapid, and radiation-free method for tracking body composition parameters, including intracellular and extracellular water, fat mass, and lean tissue. Clinical facilities increasingly integrate these systems to support early diagnosis and patient monitoring. The market benefits from growing clinical demand for objective, reproducible measurement technologies that support treatment planning and long-term disease management.

Technological Advancements and Integration of Digital Health Platforms

Advances in electrode design, frequency-modulated analyzers, and embedded analytical software have improved measurement accuracy, making bioimpedance spectroscopy more attractive for clinical adoption. The rise of connected healthcare platforms enables data synchronization with electronic health records and remote monitoring systems. Several manufacturers have incorporated wireless connectivity and automated interpretation algorithms, enabling multi-frequency data collection with reduced operator dependency. These technological improvements support physician decision-making and broaden device applicability in sports science, nephrology, cardiology, and oncology. Demand for precise, rapid, and contact-efficient measurement solutions is increasing in line with healthcare digitalization, thus strengthening the market’s long-term outlook.

Expansion of Clinical Research and Evidence-Based Diagnostic Practices

Clinical research institutions continue to explore advanced diagnostic modalities for assessing hydration status, nutritional risk, and physiological changes during disease progression. Bioimpedance spectroscopy is increasingly being incorporated into studies focused on sarcopenia, cancer treatment responses, and chronic kidney disease management. Evidence generated from multi-center research strengthens confidence in the diagnostic value of bioimpedance tools. Research funding programs encouraging non-invasive medical device innovation further support market adoption. As clinical validation expands, hospitals demonstrate a higher willingness to invest in specialized measurement systems, thereby improving commercial traction for device manufacturers.

Barrier Analysis - High Cost of Advanced Systems and Limited Reimbursement Coverage

Bioimpedance spectroscopy instruments, particularly multi-frequency research-grade models, require substantial investment, which limits penetration into smaller clinics and resource-constrained markets. Operational costs such as calibration, software upgrades, and training further increase total ownership costs. Reimbursement policies for body composition analysis vary significantly across regions, and a lack of uniform coverage creates financial barriers for healthcare facilities. These economic constraints restrict market adoption despite strong clinical interest, especially in low- and middle-income countries.

Variability in Measurement Accuracy across User Environments

Although bioimpedance spectroscopy is considered reliable, measurement results can vary depending on patient posture, electrode placement, hydration level, and device calibration. Inconsistent measurement conditions may affect diagnostic reliability and clinical decision-making. These challenges require strict protocol adherence, which some facilities struggle to maintain. Concerns about accuracy limitations inhibit broader clinical acceptance, particularly in high-acuity medical settings where diagnostic precision is critical.

Opportunity Analysis - Expansion Potential in Emerging Healthcare Markets

Healthcare modernization across Asia Pacific, Latin America, and parts of the Middle East presents strong adoption opportunities for non-invasive monitoring technologies. As hospitals invest in diagnostic infrastructure, the need for body composition and hydration assessment tools grows. Market potential is significant in nutritional assessment programs, chronic disease management facilities, and dialysis centers. The rising focus on preventive healthcare and lifestyle-related disease management creates a sizable, yet underpenetrated opportunity for vendors, representing a notable share of future market expansion.

Integration with Wearable and Remote Monitoring Ecosystems

The rapid growth of digital health platforms enables new pathways for bioimpedance technologies. Integration with wearable sensors can facilitate continuous monitoring of hydration, muscle mass, and metabolic indicators. Developers are exploring miniaturized and patch-based systems capable of transmitting real-time multi-frequency data to cloud platforms. These innovations have the potential to expand device use beyond clinical environments into home care, elderly monitoring, and sports performance. The commercial opportunity lies in leveraging connected ecosystems to enhance patient adherence and broaden user-level applications.

Rising Adoption in Oncology, Nephrology, and Critical Care Programs

Bioimpedance spectroscopy offers meaningful value in tracking nutrition decline, fluid imbalance, and treatment response in oncology and nephrology patients. Growth in dialysis facilities and chemotherapy centers drives demand for objective hydration assessment. Similarly, intensive care units are exploring non-invasive alternatives for fluid management. These specialized applications create a growing niche market representing an expanding volume of device purchases for advanced care settings.

Category-wise Analysis

Product Insights

Multi-frequency BIS devices are projected to hold about 55.3% of the market in 2026, driven by superior diagnostic accuracy and extensive clinical validation. Their ability to differentiate intracellular and extracellular water supports precise assessments for dialysis planning, heart-failure monitoring, and lymphedema detection. These systems command the highest revenue due to premium pricing, advanced analytics, algorithm-based interpretation, and robust interoperability. Hospitals and specialty centers favor them for precision, validated protocols, and scalable data-management capabilities. Recurring revenue from software upgrades, service contracts, and extended warranties further reinforces this segment’s dominance.

Portable and compact BIS platforms, especially cloud-enabled devices, represent the fastest-growing category, with projected high single-digit to low double-digit growth. Rising point-of-care diagnostics, decentralized specialty services, and telehealth expansion are key drivers. Advances in sensor miniaturization, wireless connectivity, and power efficiency allow routine use in outpatient clinics and community health settings. Subscription-based models that integrate hardware, cloud analytics, remote monitoring, and calibration support are accelerating adoption, particularly for lymphedema screening and dialysis fluid-management programs.

Application Insights

Lymphedema screening and management is the leading application, expected to account for about 37.5% of the market share in 2026, supported by well-established protocols across oncology survivorship and rehabilitation programs. BIS is widely preferred for its ability to detect subtle extracellular fluid changes, enabling early intervention in breast cancer–related lymphedema. Many cancer centers have incorporated BIS into routine follow-up schedules, creating consistent device utilization and high operational dependence. A robust clinical evidence base has strengthened procurement among oncology departments, generating strong per-device economic value. This segment leads in application-level revenue due to frequent testing, clinical endorsement, and seamless integration into existing post-treatment care pathways.

Renal and cardiac fluid-management applications represent the fastest-growing area, supported by mounting pressure to reduce preventable hospitalizations and improve therapy decision-making. Dialysis centers increasingly adopt BIS for dry-weight assessment, while cardiology programs evaluate its value for both in-clinic and remote heart-failure monitoring. Growth is propelled by the need for objective, repeatable measures of fluid status and by payer incentives aimed at lowering readmission risks. As value-based care frameworks expand across nephrology and cardiology, clinicians seek more precise monitoring technologies. Early pilot programs demonstrate rising utilization intensity, reinforcing strong momentum for BIS adoption in chronic-care settings.

Regional Insights

North America Bioimpedance Spectroscopy Market Trends - High Clinical Adoption & Advanced Multi-Frequency Integration

North America accounts for the largest regional share of the global BIS market, and its share is anticipated to remain above 39% in 2026, supported by high clinical adoption and strong institutional purchasing power. The U.S. continues to represent the primary demand center, where hospitals and oncology networks integrate BIS into routine pathways for lymphedema surveillance and chronic-disease management.

Premium multi-frequency systems dominate sales due to their advanced diagnostic capability and widespread compatibility with electronic medical record platforms. The U.S. maintains the highest per-capita BIS penetration, driven by adoption across academic medical centers, large hospital networks, and oncology groups implementing structured survivorship programs. Outpatient dialysis providers and cardiology practices in the U.S. are increasingly evaluating BIS for objective fluid-status monitoring, which expands utilization beyond oncology.

Regional growth is driven by established oncology guidelines, emerging cardiology evidence, initiatives focused on reducing preventable admissions, and steady product innovation that broadens clinical applicability. The regulatory environment in the U.S. supports predictable device pathways, although reimbursement inconsistency remains a barrier to universal integration. Competition is shaped by differentiation in clinical evidence strength, data accuracy, interoperability, and cloud-enabled analytical capabilities. In February 2024, a leading U.S. oncology network expanded its survivorship program by integrating BIS-based early-detection screening across multiple centers to enhance lymphedema monitoring efficiency.

Europe Bioimpedance Spectroscopy Market Trends - Evidence-Driven Procurement & Structured Hospital Uptake

Europe is anticipated to hold the second-largest regional share, led by Germany, the U.K., and France. Germany benefits from robust hospital infrastructure and structured procurement frameworks that support consistent BIS adoption in fluid monitoring and body composition assessment. The U.K. is expanding use through centrally coordinated procurement pathways, while France shows strengthening uptake within oncology and rehabilitation programs. Southern European countries such as Spain and Italy demonstrate selective adoption in private and tertiary-care facilities.

The EU regulatory harmonization provides a consistent device framework, though reimbursement policies differ across member states and influence purchasing cycles. Hospitals prioritize devices supported by rigorous clinical validation, reliable service networks, and strong track records of accuracy. The competitive landscape features both established European manufacturers and international suppliers, with tender processes emphasizing validation, reliability, and long-term service support.

Asia Pacific Bioimpedance Spectroscopy Market Trends - Fastest Growth via Infrastructure Expansion & Affordable BIS Adoption

Asia Pacific is anticipated to the fastest-growing region in unit volume, driven by rapid healthcare infrastructure expansion, rising chronic-disease prevalence, and growing demand for objective diagnostic tools. Japan and South Korea demonstrate mature clinical adoption with strong emphasis on device accuracy, advanced analytics, and regulatory compliance.

China and India account for the largest addressable populations, with accelerated demand from outpatient centers, diagnostic chains, and primary-care networks. Lower average selling prices make BIS more accessible in these markets, and larger volumes counterbalance pricing differences relative to Western regions.

Regional expansion is supported by growing rates of obesity, chronic kidney disease, and heart failure, which require continuous and objective fluid evaluation. Investments in outpatient diagnostics, preventive-care programs, and telehealth further support BIS integration. Portable and mid-range devices gain traction due to affordability and ease of use, especially in high-volume clinical environments. Regulatory pathways vary widely across the region, with Japan and China requiring extensive technical validation and India applying evolving compliance frameworks. Local manufacturing partnerships, evidence generation, and distributor networks are essential for scalability.

Competitive Landscape

The global bioimpedance spectroscopy market is moderately consolidated, combining major medical device manufacturers with specialized diagnostic-system developers. Leading firms compete through strong clinical evidence, broad product portfolios, reliable service networks, and advanced interoperability with health IT systems. Mid-sized regional players differentiate on affordability, portability, and localized distribution.

Competitive advantages center on accuracy, reproducibility, and validated multi-condition applications. Industry leaders prioritize evidence-based innovation, cloud-enabled analytics, cost-efficient manufacturing, and seamless EHR integration while expanding regional presence and forming partnerships that advance remote monitoring and adoption in outpatient and chronic-care settings.

Key Industry Developments

- In February 2025, ImpediMed announced the launch of an upgraded SOZO multi-frequency BIS platform with enhanced fluid-status analytics, aiming to expand adoption in oncology and heart-failure outpatient monitoring programs across North America and Europe.

- In August 2024, SECA GmbH introduced cloud-enabled BIS systems designed for multi-center hospitals and rehabilitation clinics in Europe, aiming to streamline clinical workflows and enable centralized patient data management.

Companies Covered in Bioimpedance Spectroscopy Market

- ImpediMed

- Sciospec Scientific Instruments

- Maltron International

- SELVAS Healthcare

- Bodystat

- Fresenius Medical Care

- InBody

- Tanita Corporation

- RJL Systems

- Seca GmbH

- Omron Healthcare

- Biotek Medical

- Quantum Health Analytics

- SOZO Health Technologies

- BioTek Instruments

- Akern

- Medisource Technologies

- IoT Health Solutions

- Charder Electronics

- Timpel Medical

Frequently Asked Questions

The bioimpedance spectroscopy market size in 2026 is estimated at US$0.6 Billion.

By 2033, the bioimpedance spectroscopy market is projected to reach US$1.2 Billion, supported by strong adoption across clinical, outpatient, and diagnostic settings.

Key trends include rapid transition toward portable and cloud-connected BIS systems for outpatient and home-based monitoring and strong growth in multi-frequency BIS platforms, driven by higher diagnostic precision.

The leading segment is multi-frequency BIS devices, accounting for the largest share of product-level revenue due to superior measurement accuracy, clinical validation, and premium pricing.

The bioimpedance spectroscopy market is expected to grow at a 9.2% CAGR between 2026 and 2033.

Major players include ImpediMed Ltd., InBody Co., Ltd., SECA GmbH & Co. KG, RJL Systems, and Tanita Corporation.