- Specialty & Fine Chemicals

- Biochar Market

Biochar Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Biochar Market Technology (Pyrolysis, Gasification, Hydrothermal Carbonization), Feedstock (Woody Biomass, Agricultural Waste, Animal Manure, Other), End-user (Agriculture, Power Generation, Livestock Farming), and Regional Analysis for 2026 - 2033

Biochar Market Size and Trend Analysis

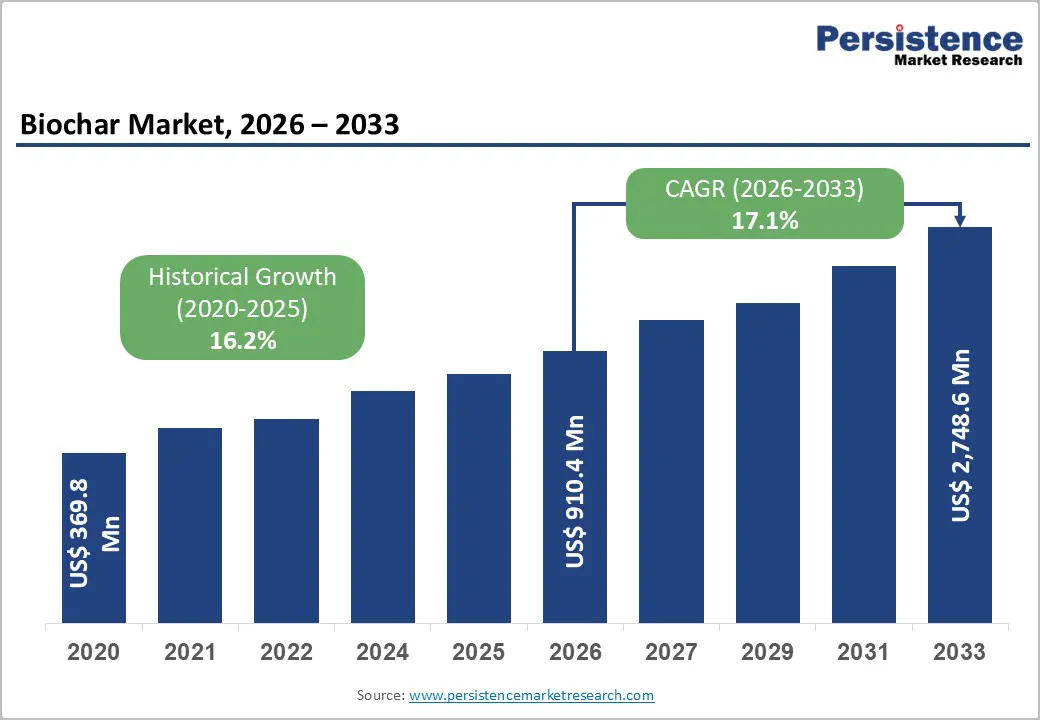

The global biochar market size is supposed to be valued at US$ 910.4 million in 2026 and is projected to reach US$ 2,748.6 million by 2033, growing at a CAGR of 17.1% between 2026 and 2033.

The market demonstrates exceptional growth potential driven by increasing global awareness of climate change mitigation, soil degradation concerns, and supportive government policies promoting carbon sequestration and sustainable agriculture. Rising corporate demand for carbon removal credits, combined with agricultural sector adoption of biochar for soil enhancement and improved crop yields, significantly accelerates market expansion across developed and emerging economies.

Key Industry Highlights:

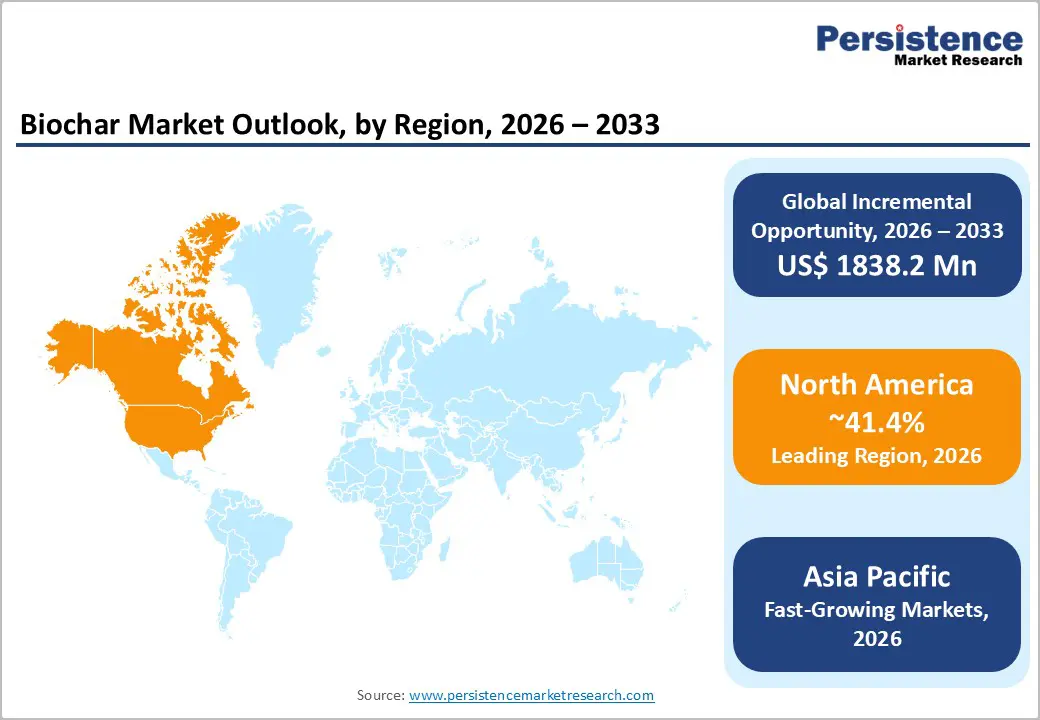

- Regional Leader: North America remains the established market leader, commanding 41.4% global market share with the U.S. as the largest single market, driven by institutional corporate demand for biochar carbon credits from technology sector buyers, including Microsoft, Google, and financial institutions requiring verifiable carbon removal for net-zero commitments.

- Fastest Growing Region: Asia Pacific emerges as the fastest-growing region, expanding at 11.5% CAGR, with India leading regional growth at 26% CAGR through the deployment of government biomass programs, agricultural residue valorization, and biochar adoption in sustainable farming systems addressing severe soil degradation.

- Leading Segment: Pyrolysis technology dominates biochar production, commanding 65% globally due to superior carbon retention, versatility in processing heterogeneous feedstocks, and established certification frameworks validating environmental and carbon sequestration benefits.

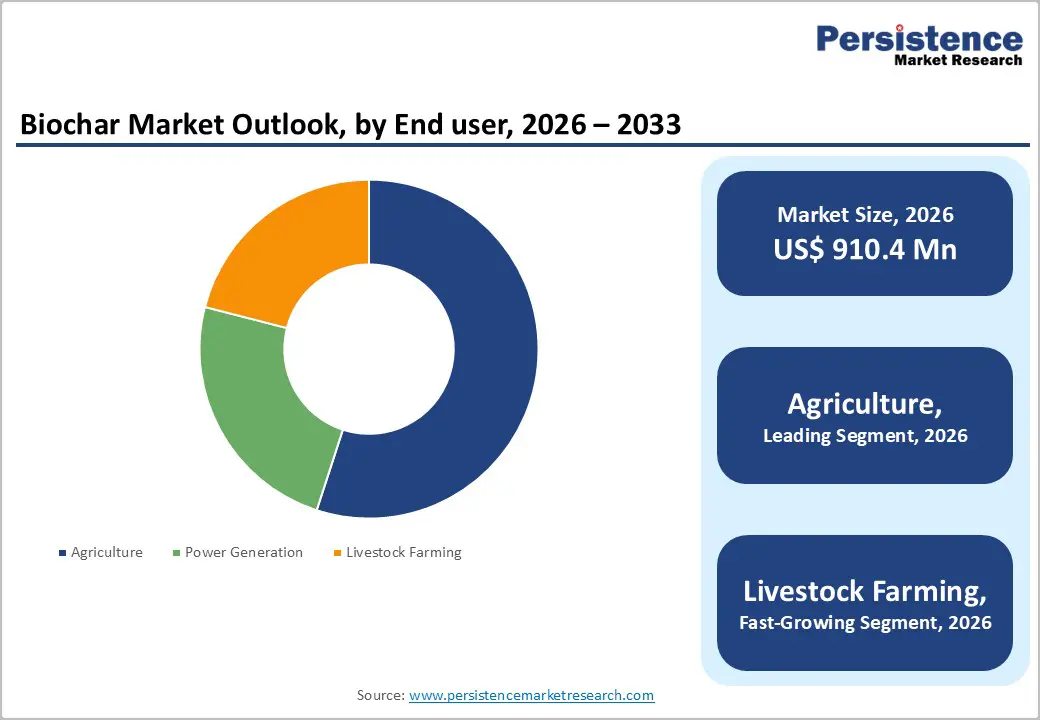

- Fastest Growing Segment: Agricultural applications accelerate fastest through proven benefits in soil restoration, water retention, nutrient cycling, and carbon sequestration, driving farmer adoption across developing agricultural economies.

- Key Market Opportunity: Livestock farming applications unlock substantial growth potential, enabled by regulatory acceptance in Europe and emerging USA state-level approvals, with biochar feed additives reducing enteric methane emissions, enhancing nutrient absorption, and manure applications providing dual revenue streams from soil products and carbon credit monetization.

| Key Insights | Details |

|---|---|

| Biochar Market Size (2026E) | US$ 910.4 Mn |

| Market Value Forecast (2033F) | US$ 2,748.6 Mn |

| Projected Growth CAGR (2026 - 2033) | 17.1% |

| Historical Market Growth (2020 - 2025) | 16.1% |

Market Dynamics

Drivers - Calimate Change Mitigation and Carbon Sequestration Initiatives

The global emphasis on climate action serves as a major catalyst for biochar market growth. Biochar provides a stable mechanism for long-term carbon sequestration in soils, supporting international climate commitments and net-zero objectives. Governments are increasingly incorporating biochar into climate strategies, exemplified by the European Union’s Carbon Removal Certification Framework (CRCF), adopted in December 2024, which standardizes carbon removal verification through biochar production.

In the U.S., amendments to Section 45Q under the Inflation Reduction Act have introduced significant financial incentives for biochar projects. Leading corporations such as Microsoft, Google, Boston Consulting Group, and JPMorgan have secured substantial volumes of biochar carbon removal credits, with Microsoft alone committing approximately 1.24 million tonnes. This alignment of regulatory support, economic incentives, and corporate demand is accelerating market expansion.

Agricultural Productivity Enhancement and Soil Health Restoration

The biochar market is expanding rapidly, driven by growing agricultural demand for sustainable soil enhancement solutions. Biochar significantly improves soil structure and chemistry, enhancing water retention, nutrient availability, and microbial diversity while reducing dependence on synthetic fertilizers. Adoption is particularly strong in the Asia Pacific, notably in China and India, where soil degradation and declining fertility pose major challenges. India alone generates approximately 500-550 million tonnes of crop residues annually, creating substantial opportunities for biochar production through agricultural waste valorization.

Global trends toward organic farming, coupled with regulatory restrictions on synthetic inputs and peat usage, further strengthen demand for biochar as an eco-friendly soil amendment. Research confirms that biochar applications can boost crop yields while minimizing nitrogen leaching and nutrient loss, offering an economically viable solution for farmers worldwide.

Restraint - High Capital Investment Requirements and Production Cost Challenges

Biochar market expansion faces substantial obstacles stemming from elevated capital expenditure requirements for establishing production facilities. Pyrolysis and gasification technologies demand significant infrastructure investments, with equipment costs, land acquisition, and facility development presenting formidable barriers for small and medium-sized enterprises. The production process requires substantial energy inputs, influencing operational costs and profit margins, particularly in regions with high electricity costs.

Limited access to capital, especially in emerging markets and the global south, where institutional financial support remains weak, constrains market growth. Feedstock sourcing and logistics, including collection, transportation, and storage of agricultural residues, animal manure, and woody biomass, add considerable expenses to production. These cost dynamics necessitate substantial government subsidies or carbon credit revenue streams to achieve economic viability, particularly during early commercialization phases when production scales remain limited and unit costs remain elevated.

Regulatory Uncertainty and Varying Quality Standards Across Markets

The biochar industry faces considerable regulatory challenges due to fragmented governance frameworks and inconsistent global quality standards. Regional variations in certification requirements, product specifications, and end-use applications create significant compliance complexities. Standards such as the European Biochar Certificate (EBC), International Biochar Initiative protocols, and emerging regulatory methodologies demand rigorous testing and verification, increasing operational burdens and delaying market entry.

Additional uncertainty surrounds carbon permanence assessments, toxicant levels in certain feedstocks, and accounting methods for avoided emissions, further complicating compliance. U.S. EPA guidance issued in September 2024, while clarifying permitting for cellulosic biomass, introduced new compliance obligations that impose operational restrictions. Environmental safeguards, soil incorporation mandates, and diverse sustainability standards necessitate extensive documentation and monitoring, disproportionately impacting smaller producers and limiting market accessibility.

Opportunities - Hydrothermal Carbonization Technology Expansion for Wet Feedstock Utilization

Hydrothermal carbonization (HTC) presents a significant opportunity for the biochar market by enabling the utilization of high-moisture feedstocks that traditional pyrolysis cannot process economically without extensive drying. HTC efficiently converts organic materials such as food waste, sewage sludge, and agricultural residues into hydrochar and biofertilizer, advancing circular economy objectives and reducing landfill dependency. Commercial-scale HTC plants in Spain and the U.K. validate its viability, with sewage sludge-derived hydrochar serving as a potential coal substitute while retaining soil amendment properties, creating dual revenue streams.

Research indicates HTC delivers superior handling characteristics and enhanced nutrient content compared to pyrolysis biochar, particularly for manure-based feedstocks rich in phosphorus and nitrogen. Growing waste management initiatives and stricter wastewater regulations across developed economies are driving sustained demand for HTC-based biochar solutions.

Emerging Power Generation Integration and Energy Recovery Applications

Integrating biochar with renewable energy systems offers significant commercial potential by extending applications beyond traditional agriculture. Biomass gasification and pyrolysis technologies enable simultaneous generation of electricity, heat, and biochar, addressing multiple economic objectives and making these systems attractive for industrial and agricultural operations seeking energy independence. Livestock farming represents a particularly promising use case, where integrated biochar-energy systems reduce heating costs, process manure waste streams, and generate revenue through biochar sales and carbon credits.

Electricity generation is emerging as the fastest-growing segment, with rural and off-grid communities increasingly adopting distributed biochar-based energy solutions. Advanced reactor designs facilitate syngas and bio-oil recovery alongside solid biochar, while government renewable energy mandates and rising electricity costs in North America and Europe further incentivize biomass-to-energy systems, creating scalable market opportunities.

Category-wise Analysis

Technology Insights

The pyrolysis technology segment holds a dominant position in the global biochar market, driven by its proven efficiency, scalability, and commercial maturity. Pyrolysis involves thermal decomposition of biomass at high temperatures in an oxygen-free environment, producing stable, carbon-rich biochar with consistent quality. This process delivers superior yield compared to alternative methods, with systems generating approximately 45,800 metric tonnes annually versus 36,000 tonnes from gasification using similar feedstock inputs.

Widespread adoption of slow pyrolysis for agricultural applications, coupled with advancements in fast pyrolysis enabling co-production of bio-oil and liquid fuels, reinforces its leadership. The segment benefits from established infrastructure, reliable process controls, and integration with waste management systems. Capturing 64-67% market share in developed economies, North America exhibits a strong preference due to technological maturity and regulatory compliance.

Feedstock Insights

Woody biomass remains the leading feedstock segment in the global biochar market, with 38% market share, supported by its abundant availability, consistent quality, and favorable carbon sequestration properties. Sources such as forestry residues, sawmill byproducts, and wood processing waste streams ensure a reliable supply, particularly across North America and Northern Europe. Woody biomass delivers superior biochar production efficiency, yielding high-quality material with enhanced porosity and surface area, ideal for agricultural applications.

Conversely, agricultural waste feedstocks, including crop residues, straw, and rice husks, represent the fastest-growing category, driven by waste valorization initiatives and government programs. India and China, generating vast crop residues annually, are increasingly converting stubble into biochar via pyrolysis and gasification. Animal manure, enabled by hydrothermal carbonization, also emerges as a valuable feedstock for nutrient-rich soil amendments.

Application Insights

Agriculture remains the dominant end-use segment, accounting for approximately 55% of market share, driven by the need for sustainable soil enhancement and improved crop productivity. Farmers increasingly adopt biochar amendments to combat soil degradation, declining organic matter, and nutrient depletion caused by intensive monoculture practices. Biochar enhances water retention, nutrient availability, and microbial diversity, which are critical for water-stressed regions.

Growth is further supported by the expansion of organic farming, restrictions on peat usage, and rising awareness of biochar’s carbon sequestration benefits. Livestock farming is emerging as a high-growth segment, utilizing biochar in feed supplements to improve digestion and reduce methane emissions. Integration of biochar production with farming operations creates economic synergies, while power generation applications, driven by renewable energy mandates and technological advances, represent the fastest-growing segment.

Regional Insights

North America Biochar Market Trends

North America remains the leading regional market, accounting for approximately 41% of the global share, supported by technological leadership, robust regulatory frameworks, and advanced carbon credit infrastructure. The U.S. benefits from the Inflation Reduction Act’s revised Section 45Q tax credits, offering strong financial incentives for biochar-based carbon sequestration projects and capacity expansion. EPA guidance issued in 2024 streamlined permitting for biochar production from clean cellulosic biomass, reducing regulatory barriers.

State-level programs, including California’s Cap-and-Trade and the Regional Greenhouse Gas Initiative (RGGI), further strengthen carbon credit markets, ensuring sustained revenue streams. Leading companies such as Airex Energy, Phoenix Energy, and Oregon Biochar Solutions drive innovation in production technologies and feedstock flexibility. Corporate sustainability commitments, exemplified by Microsoft’s 1.24 million-tonne offtake agreement with Exomad Green, underscore growing confidence in biochar’s market maturity and scalability.

Europe Biochar Market Trends

The European biochar market is witnessing accelerated growth, driven by the EU’s Carbon Removal Certification Framework (CRCF), which becomes operational in 2026 as the world’s first standardized voluntary certification system for carbon removals and carbon farming. This framework enhances transparency and credibility in carbon credit trading, addressing greenwashing concerns and strengthening investor confidence. Complementing this, the European Biochar Certificate (EBC), integrated into EU fertilizer regulations, ensures quality assurance for commercialization across member states.

Germany, the U.K., France, and Spain lead regional development, with companies such as Pyreg GmbH and Carbonis GmbH & Co. KG advancing pyrolysis technology. Industrial-scale hydrothermal carbonization plants in Spain and the U.K. validate HTC’s viability for waste valorization. Stringent environmental regulations and circular economy policies further promote biochar adoption in agriculture and waste management sectors.

Asia Pacific Biochar Market Trends

Asia Pacific is the fastest-growing regional market, driven by expansive agricultural sectors, abundant biomass feedstock, and government initiatives addressing soil degradation and climate change. China’s agricultural industry, facing severe soil erosion and fertility decline, increasingly adopts biochar for soil restoration and productivity enhancement, supported by climate-smart agriculture programs and carbon credit development.

India, generating 500-550 million tonnes of crop residues annually, offers significant biochar production potential through stubble valorization policies aimed at reducing air pollution. Collaborative projects, such as IIT(ISM) Dhanbad’s agreement with Sentra.world to explore biochar in steel manufacturing with up to 40% emission reduction, highlight diversifying applications. Japan, South Korea, and Malaysia contribute growth through biotechnology integration, waste valorization, and renewable energy-linked biochar projects, reinforcing regional market expansion.

Competitive Landscape

The global biochar market reflects a moderately consolidated structure, led by established technology providers, innovative emerging players, and regional specialists competing through differentiated platforms and feedstock strategies. Tier 1 companies such as Airex Energy, Pyreg GmbH, Phoenix Energy, and Oregon Biochar Solutions command 55-60% of the Asia Pacific’s market share while maintaining strong influence in North America and Europe through robust production capacity, advanced technologies, and extensive distribution networks. These leaders pursue aggressive growth via organic expansion and strategic acquisitions, leveraging key differentiators including advanced pyrolysis systems, multi-feedstock flexibility, integrated energy recovery, and modular equipment designs. Hydrothermal carbonization (HTC) development is a critical competitive advantage, enabling high-moisture feedstock processing. Emerging mid-tier firms focus on niche applications, customized products, and farmer engagement, while innovation intensity remains high, driven by R&D in carbon credits, filtration, and energy systems.

Key Developments:

- January 2025: CapChar, a U.K.-based biochar developer, initiated public consultation on its proprietary Biochar Carbon Code, establishing a comprehensive methodology for quantifying biochar carbon sequestration within the UK context and providing foundational support for farmers and stakeholders participating in biochar carbon projects.

- September 2025: Biochar Credits Market Tightens Supercritical, a carbon removal marketplace, reported that 89% of 2025 biochar carbon removal credits were already committed through offtake agreements as of Q3 2025, up sharply from 62% in March, signaling unprecedented supply tightness and commanding 8% price appreciation from Q2 to Q3 at approximately US$ 150-160 per tonne CO2e.

- October 2025: Microsoft executed a landmark 1.24 million-tonne biochar carbon removal credit offtake agreement with Exomad Green, representing the largest single-corporate commitment to biochar carbon credits and catalyzing second-half 2025 as a record-breaking period for biochar carbon removal (BCR) market activity with 1.6 million tonnes contracted in the first half of 2025 alone.

Top Companies in the Biochar Market

- Pyreg GmbH (Germany) has established market leadership through proprietary pyrolysis technology, enabling decentralized biochar production with unmatched carbon removal efficiency. The company's Pyreg PX system architecture provides customizable fuel capacity with integrated emission control and renewable energy generation, serving municipal biosolids treatment, industrial waste valorization, and agricultural applications. Pyreg operates 50+ commercial installations globally and pioneered carbon credit monetization pathways, with customer access to multiple carbon credit platforms for revenue generation from carbon removal activities.

- Biochar Now LLC (U.S.) specializes in large-scale biochar production with integrated engineering, manufacturing, and sales operations across North America. The company holds 11 patents covering biochar production technology and soil application methodologies, operates multiple production facilities meeting EPA emissions standards, and has established market presence in agricultural soil amendment markets while expanding into carbon credit certification under recognized standards.

- Oregon Biochar Solutions (U.S.) achieved historic market recognition as the first biochar project in the Americas to successfully monetize carbon credits (2021) and obtain Puro.earth certification for responsible biochar production. The company pioneered insured biochar carbon credits through a partnership with Oka Insurance, addressing buyer risk concerns and establishing quality leadership in the voluntary carbon market at premium valuations.

Companies Covered in Biochar Market

- Airex Energy

- Phoenix Energy

- Pyreg GmbH

- Carbon Gold Ltd

- Biochar Now LLC

- Carbonis GmbH & Co. KG

- Oregon Biochar Solutions

- CharGlow LLC

- Charline GmbH

- Farm2Energy

- Exomad Green

- CapChar

Frequently Asked Questions

The global biochar market is projected to reach US$ 2,748.6 Mn by 2033 from US$ 910.4 Mn in 2026, expanding at a CAGR of 17.1%, driven by increasing adoption in agricultural sustainability, carbon sequestration initiatives, and livestock farming applications across North America, Europe, and the Asia Pacific regions.

Market growth is propelled by climate change mitigation demands with corporate net-zero commitments driving biochar carbon credit demand, agricultural soil degradation requiring restoration solutions, government policy support including USDA NRCS Standards and EU CRCF Certification Framework, and sustainable farming practices driven by environmental regulations and organic food market premiums.

Pyrolysis technology dominates with 65% globally due to superior carbon quality and versatility, driven by abundant supply, cost-effectiveness, and environmental imperatives to valorize crop residues currently burned in open fields across India, China, and Southeast Asia.

North America remains the established market leader, commanding 41.4% global market share with the U.S. as the largest single market, driven by institutional corporate demand for biochar carbon credits from technology sector buyers, including Microsoft, Google, and financial institutions requiring verifiable carbon removal for net-zero commitments.

Integrated Energy-Biochar Systems targeting livestock farming and agricultural operations present the most substantial growth opportunity, enabling simultaneous biochar soil amendment production, renewable energy generation, and waste valorization, creating multiple revenue streams through biochar sales, carbon credits, and energy co-products while addressing agricultural waste management challenges and supporting farmer profitability improvement.

Major market players include Airex Energy, Pyreg GmbH, Phoenix Energy, Oregon Biochar Solutions, Carbon Gold Ltd., Biochar Now LLC, Carbonis GmbH & Co. KG, CharGlow LLC, Charline GmbH, Farm2Energy, and Pacific Biochar, competing through differentiated technology platforms, feedstock specialization strategies, and integrated product-service offerings addressing diverse agricultural and industrial applications.