- Advanced Materials

- Ballistics Composites Market

Ballistics Composites Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Ballistics Composites Market by Fiber Type (Aramid Fibers, UHMPE, S-Glass, and Other Fiber Types), Matrix Type (Polymer Matrix, Polymer Ceramic, and Metal Matrix), Application (Vehicle Armor, Body Armor, Helmet & Face Protection, and Other), and Regional Analysis for 2026 - 2033

Ballistics Composites Market Size and Share Analysis

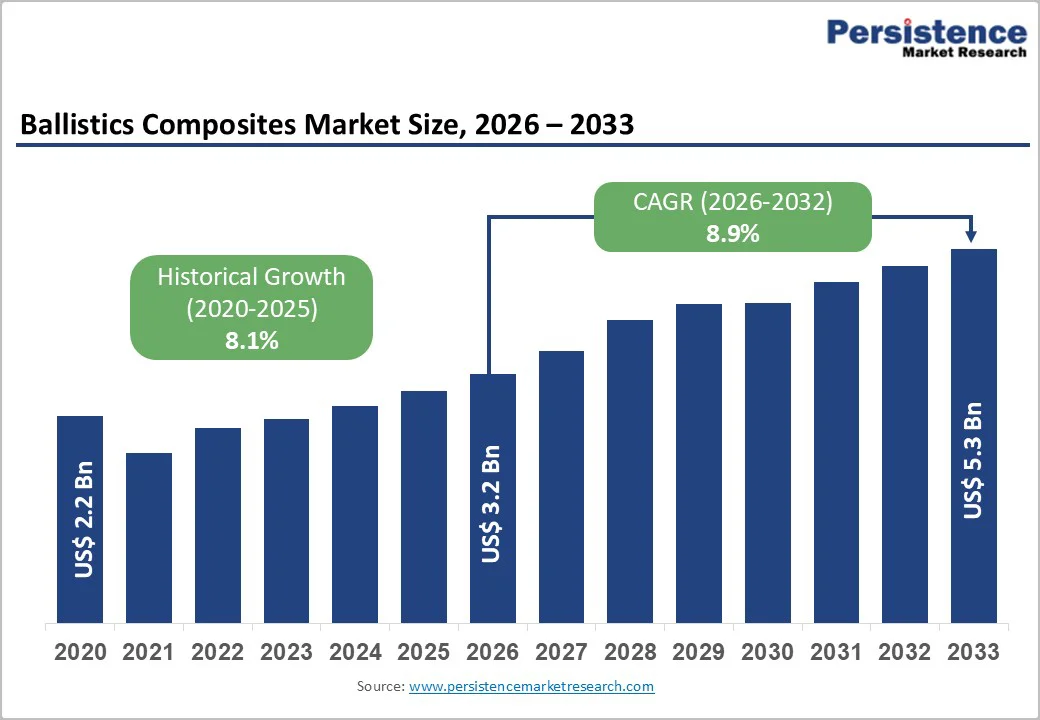

The global ballistics composites market size is likely to be valued at US$ 3.2 billion in 2026 and is projected to reach US$ 5.3 billion by 2033, growing at a CAGR of 7.6% between 2026 and 2033.

The market expansion is driven by escalating global security threats and rising armed conflicts necessitating advanced personnel and vehicle protection systems, accelerating defense modernization programs across developed and emerging economies with substantial government budget allocations supporting procurement of lightweight ballistic materials, and exponential growth in civilian security applications, including armored transport for high-profile individuals and private security sector expansion.

Key Market Highlights

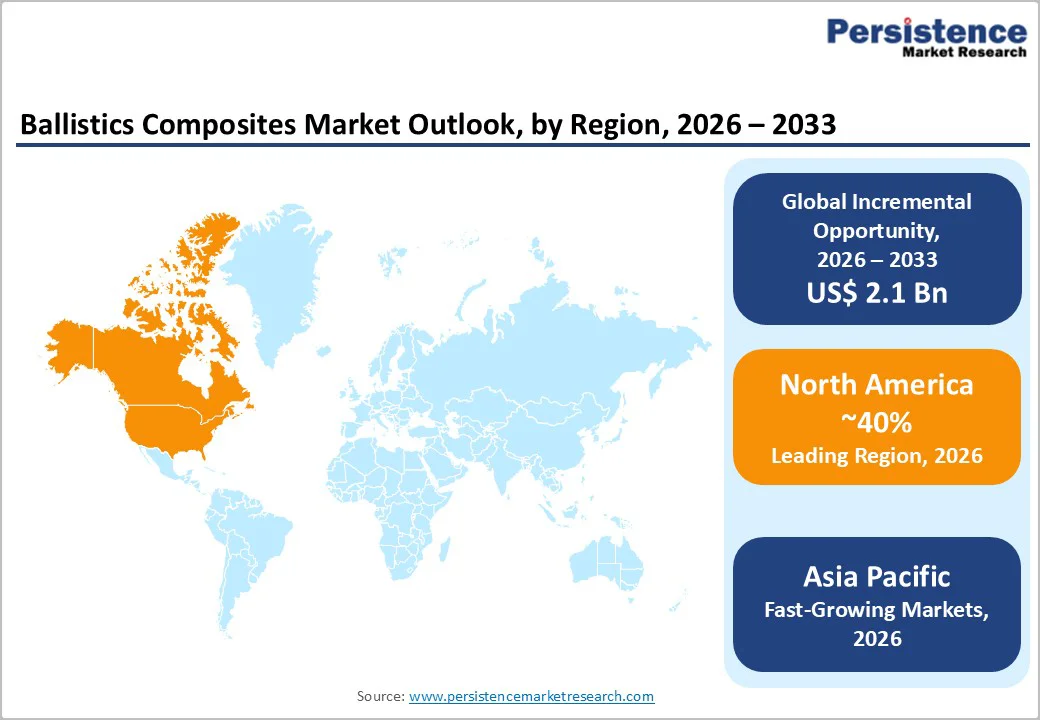

- Leading Region: North America dominates the global ballistics composites market with a commanding 40% share, anchored by the United States with a USD 800+ billion annual defense budget, extensive military and law enforcement infrastructure, and dominant defense contractor presence supporting sustained regional market leadership.

- Fastest-Growing Region: Asia Pacific experiences the quickest market growth, with China at a 10.1% CAGR and India at a 9.4% CAGR through 2033, driven by defense modernization initiatives, indigenous manufacturing expansion, growth in the private security sector, and government armor procurement programs, which support

- accelerated regional demand.

- Dominant Application: Vehicle armor represents the dominant application segment, commanding approximately 45% market share, driven by military vehicle modernization programs, lightweight composite panel adoption reducing vehicle weight 15-20%, and enhanced protection requirements across defense and homeland security applications.

- Growing Application: Body armor applications represent the fastest-growing segment, experiencing an 8-9% CAGR through 2033, driven by escalating security threats, an emphasis on law enforcement modernization, the adoption of modular vest systems, and the expansion of the private security sector, which supports sustained acceleration in segment growth.

- Key Market Opportunity: Smart composite technology integration and sensor-embedded armor system development represent exceptional growth opportunities, with advanced systems enabling real-time monitoring of armor integrity, threat detection enhancements, and performance optimization, thereby supporting the commercialization of next-generation protective equipment.

| Key Insights | Details |

|---|---|

|

Global Ballistics Composites Market Size (2026E) |

US$ 3.2 Bn |

|

Market Value Forecast (2033F) |

US$ 5.3 Bn |

|

Projected Growth CAGR(2026-2033) |

7.6% |

|

Historical Market Growth (2020-2025) |

6.8% |

Market Dynamics

Drivers - Rise in Global Security Threats and Defense Modernization Investment Expansion

Rising armed conflicts, terrorism threats, and cross-border security challenges are compelling governments worldwide to prioritize military modernization and the advancement of personnel protection equipment, driving substantial demand growth for advanced ballistic composites. Global defense spending exceeded USD 2.4 trillion in 2024, establishing unprecedented investment levels supporting the development and procurement of next-generation protective systems incorporating advanced composite technologies. Armed conflicts and geopolitical tensions across multiple global regions are creating urgent procurement requirements for enhanced ballistic protection equipment for military and law enforcement personnel. Defense budgets in major economies, including the United States, that exceed USD 800 billion annually are establishing structural demand drivers that support sustained ballistic composite market expansion.

Governments are increasingly emphasizing soldier survivability and operational effectiveness through investments in lightweight, high-performance armor systems offering superior protection-to-weight ratios, enabling enhanced battlefield mobility. The integration of advanced fiber-reinforced composite materials into body armor, helmets, and vehicle protection systems has become a strategic priority across defense departments globally. Continuous advancements in composite engineering methodologies and fiber technology innovation are enabling the development of superior protective solutions, supporting accelerated market growth throughout the forecast period.

Technological Advancement in Fiber Materials and Composite Engineering Capabilities

Continuous innovation in aramid fiber technology and ultra-high molecular weight polyethylene (UHMWPE) development is enabling the creation of ballistic composites with exceptional strength-to-weight ratios and superior energy absorption, supporting market expansion across diverse application segments. Aramid fiber manufacturers, including Teijin Aramid, with 35+ years of ballistics expertise, are advancing hybrid composite systems combining aramid and UHMWPE, achieving optimized ballistic performance through sophisticated interface adhesion control.

Research demonstrates that PPTA/UHMWPE laminate combinations with optimized interlayer adhesion and plasma treatment achieve significant ballistic performance improvements, with failure rates reducing to 0.05 and penetration depths decreasing to 21.71 millimeters. The development of modular armor systems enabling customized protection solutions tailored to specific threat profiles is expanding ballistic composite applications across diverse end-user requirements.

Smart composite technologies incorporating embedded sensors and real-time armor monitoring systems are emerging as next-generation protective innovations, enhancing threat detection and performance optimization capabilities. Lightweight ballistic panel innovations reducing weight by 15-20% compared to conventional metallic armor while maintaining superior protective capabilities are accelerating adoption across military fleets and law enforcement agencies. Continued research advances and the commercialization of hybrid composite formulations are establishing sustained momentum, supporting market expansion through the forecast period.

Restraints - High Raw Material Costs and Manufacturing Complexity Constraints

Ballistic composite production involves expensive specialty fibers, including aramid and UHMWPE, with limited supplier availability and pricing dependent on global supply constraints, creating substantial cost barriers limiting market penetration in price-sensitive application segments. The manufacturing process requires controlled environmental conditions, precise layering methods, and specialized equipment, which increase production costs compared to conventional protective materials.

Import dependencies for high-performance fibers create supply chain vulnerabilities and price volatility, affecting manufacturing margins and market competitiveness. Quality assurance requirements for ballistic applications, including NATO-standard testing protocols and threat level certifications, impose additional manufacturing costs and operational complexity. Development of high-purity composite materials requires sophisticated synthesis and purification processes, elevating production expenses and limiting manufacturing scalability.

Technical Standardization Challenges and Interface Adhesion Optimization Complexity

Ballistic composite optimization requires sophisticated control of interlayer adhesion and stacking sequence parameters, where excessive adhesion can paradoxically reduce protective performance by preventing delamination, creating technical design challenges that limit product development efficiency. Multi-hit performance requirements and fragmentation-resistance specifications impose complex engineering constraints that require extensive field testing and validation before market introduction.

Delamination control optimization, balancing sufficient adhesion, enabling energy absorption, and adequate delamination, enabling projectile dissipation, requires advanced materials science expertise and iterative development cycles. Environmental durability requirements, including thermal stability, moisture resistance, and retention of mechanical properties under extreme conditions, impose additional design and testing complexity. Standardization gaps across geographic markets and military specifications create barriers to commercialization and global product deployment.

Opportunity - Civilian Security Market Expansion and Armored Vehicle Manufacturing Growth

Civilian security applications, including armored transport for government officials, diplomatic personnel, and high-profile business executives, represent exceptional growth opportunities driven by rising geopolitical tensions and terrorism threats. The expansion of the private security sector, driven by increasing demand for lightweight, modular protective systems, supports sustained adoption of ballistic composites across commercial vehicle protection applications. Armored vehicle manufacturing for government and private-sector applications is experiencing exceptional growth, with manufacturers standardizing on composite-based protective panels that replace traditional metallic armor, reducing vehicle weight by 15-20% while maintaining superior ballistic protection.

VIP protection and armored transport markets in emerging economies, including India and China, are experiencing rapid expansion driven by growing wealth disparity and security threats, establishing incremental demand for specialized ballistic protection systems. The global expansion of commercial law enforcement and the growth of private security forces are creating new market segments for body armor and protective equipment incorporating advanced composite materials. Retrofit market opportunities for existing vehicles and protective systems offer high-margin business for suppliers of modular panel systems and installation services.

Smart Composite Technology Integration and Sensor-Embedded Armor System Development

Smart composite technology incorporating embedded sensors for real-time armor integrity monitoring and threat detection represents an exceptional growth opportunity driven by military emphasis on enhanced situational awareness and personnel safety optimization. The development of adaptive composites that dynamically respond to threat characteristics through smart material integration and artificial intelligence optimization is emerging as next-generation protective technology. Real-time performance monitoring systems enabling field assessment of composite degradation and protective capacity are creating new revenue streams for suppliers offering integrated protection and monitoring solutions.

Aerospace and naval ballistic protection applications incorporating smart composite systems for cockpit protection and crew safety enhancement represent high-margin growth opportunities. Integration of nanotechnology and advanced materials science into ballistic composites is enabling the development of next-generation protective systems with superior performance characteristics. Government initiatives supporting next-generation soldier modernization programs are establishing procurement pathways for advanced composite armor systems that incorporate digital monitoring and performance-enhancement capabilities. Research partnerships between defense departments and advanced materials manufacturers are accelerating the commercialization of smart composite technologies, supporting market expansion.

Category-wise Analysis

Fiber Type Insights

Aramid fibers, particularly para-aramid (PPTA) materials, including Teijin Aramid's Twaron® brand, command market dominance, accounting for approximately 50-55% of the ballistic composite market share, driven by exceptional energy absorption, tenacity, and toughness, establishing the material as the industry standard for protective applications. Teijin Aramid's 35+ years of ballistics expertise has positioned the supplier as a technology leader with comprehensive support spanning yarn development, fabric innovation, laminate optimization, and manufacturing process enhancement. Aramid fibers demonstrate superior durability across extensive environmental and mechanical stress testing, providing users with confidence and reliable performance in critical operational scenarios.

Hybrid composite systems combining aramid with UHMWPE are achieving synergistic performance advantages that exceed the capabilities of the individual materials. 100% recyclability of aramid materials aligns with modern sustainability requirements, enabling the transformation of manufacturing waste and end-of-life ballistic gear into non-ballistic products. Established supply chain relationships reinforce the segment's leadership, proven regulatory compliance across jurisdictions, and continued innovation supporting sustained market dominance throughout the forecast period.

Matrix Type Insights

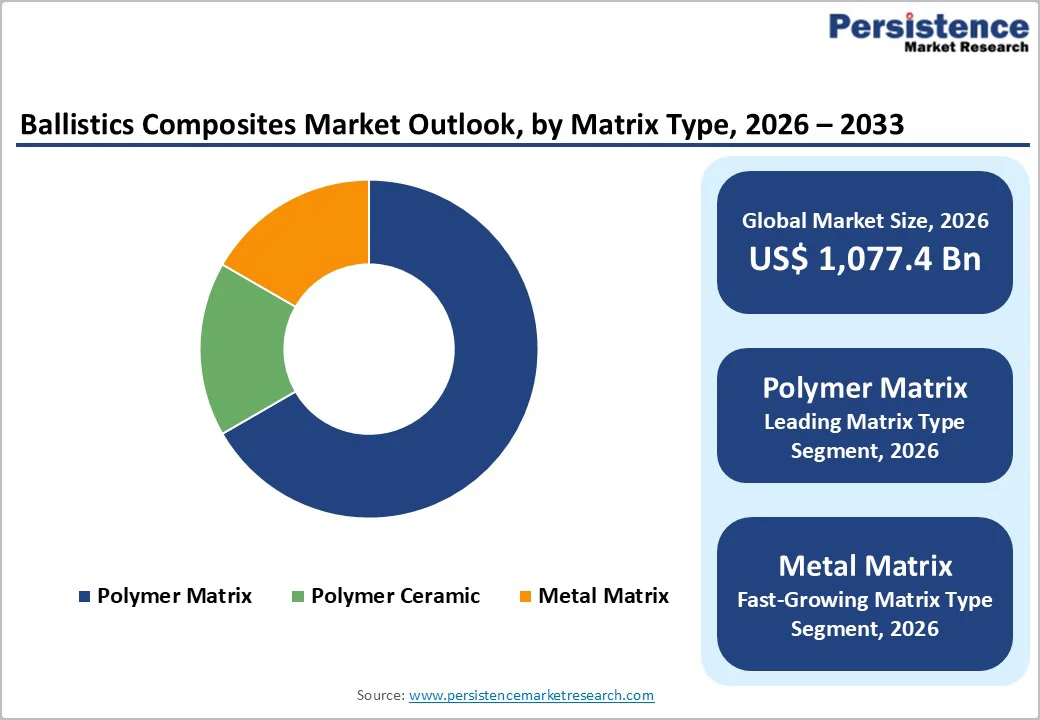

Polymer matrix composites command market dominance, accounting for approximately 45% of the ballistic composite market share, driven by exceptional strength-to-weight ratios, manufacturing flexibility, and integration compatibility with emerging technologies. Favorable properties of polymer matrix systems, including epoxy, polyurethane, and polypropylene matrices, enable the development of modular armor solutions adaptable to diverse threat profiles and operational requirements. Integration potential with smart technologies and embedded sensor systems positions polymer matrix composites as the preferred choice for next-generation adaptive protective equipment.

Manufacturing advantages, including simplified production methodologies and cost-effectiveness compared to ceramic and metal matrix alternatives, support broad-based commercial adoption. Thermal stability improvements through advanced resin system development enable high-temperature performance suitable for aerospace and extreme environment applications. The segment's leadership reflects military and law enforcement preference for polymer-based systems, supporting continued market expansion and lightweight armor modernization initiatives.

Application Insights

Vehicle armor represents the largest ballistic composite application segment, commanding approximately 45% market share, driven by critical importance of armored vehicle protection in modern military operations and counterterrorism campaigns. Lightweight composite armor panels enable significant reductions in vehicle weight, improving fuel efficiency, payload capacity, and mobility compared to traditional metallic protection. Mine-resistant ambush protected (MRAP) vehicle development and armored personnel carrier modernization programs globally are generating substantial, sustained demand for advanced composite protection systems. Modular armor design flexibility enables customized protection solutions tailored to specific threat environments and operational requirements.

Body armor is the fastest-growing ballistic composite application segment, with a CAGR exceeding 8.9% through 2033, driven by escalating security threats, the expansion of terrorism, and the emphasis on law enforcement modernization. Personnel protection represents a critical priority for military and law enforcement leadership, establishing sustained procurement commitments for advanced body armor incorporating composite technologies. Soft armor vest development utilizing aramid fiber layering provides flexible protection, enabling operational mobility and comfort. Hard armor plates incorporating ceramic-composite hybrid systems deliver superior multi-hit protection against high-velocity projectiles. Modular armor system design enables customized protection levels, accommodating diverse threat scenarios and operational requirements.

Regional Insights

North America Ballistics Composites Trends

North America represents the largest ballistics composites market, commanding approximately 40% global market share in 2026, with the United States maintaining market dominance through the world's largest defense budget exceeding USD 800 billion annually and extensive military and law enforcement infrastructure requirements. U.S. Department of Defense procurement programs establish a substantial baseline demand for advanced ballistic protection equipment, with continuous modernization initiatives emphasizing lightweight armor systems, improving soldier mobility and survivability. Advanced fiber technology development, including aramid and UHMWPE material innovation, demonstrates superior strength-to-weight ratios, enabling lighter, more effective armor systems, improving operational effectiveness.

Law enforcement agency modernization programs are accelerating the adoption of ballistic composites across body armor, tactical equipment, and protective systems. Private security sector expansion, supporting VIP protection and armored vehicle manufacturing, creates growing commercial market opportunities for ballistic composite suppliers. Police departments' transitions toward modular vest systems incorporating flexible composite shields demonstrate market diversification beyond traditional military applications.

Europe Ballistics Composites Trends

Europe represents a significant ballistics composites market, commanding approximately 25% global share, with Germany maintaining technology and manufacturing leadership through 8.6% CAGR and world-renowned engineering capabilities. Aramid-carbon hybrid composite development incorporating lightweight ballistic doors and protective barriers demonstrates advanced composite innovation supporting military transport systems and personal protective gear. NATO-standard compliance requirements establish stringent testing protocols ensuring superior protection characteristics across diverse threat scenarios.

Aerospace ballistic protection applications leveraging advanced laminates for cockpit protection in rotorcraft and fixed-wing aircraft establish high-performance application segments. Portable ballistic barriers incorporating folding composite frames demonstrate specialized application development for special response teams and tactical operations. United Kingdom and France markets maintain strong law enforcement demand supporting portable shields and compact body armor development.

Asia Pacific Ballistics Composites Trends

Asia Pacific represents the fastest-growing regional market, experiencing growth rates substantially exceeding developed market expansion, with China leading at 10.1% CAGR driven by expanded defense manufacturing capacity and lightweight armor system procurement. Production hubs in Jiangsu and Guangdong are scaling thermoplastic composite integration into ballistic helmets and protective shields. India represents the second-fastest growth at 9.4% CAGR, fueled by Make in India initiatives that emphasize indigenous manufacturing and reduce import dependence, particularly for armor production.

Government-backed ordnance factories and private security equipment firms are driving the adoption of lightweight composite armor across personnel and vehicle protection applications. Modular plating system development featuring multi-layer composites supports paramilitary deployment in border protection zones. Pune and Hyderabad supplier networks are establishing regional manufacturing and distribution capabilities to support the expansion of emerging market demand. ASEAN nations, including Indonesia and Vietnam, are experiencing growing defense investment, establishing incremental ballistic-composite demand that supports regional market expansion.

Competitive Landscape

The ballistics composites market exhibits a moderately consolidated competitive structure dominated by large global defense contractors and specialized ballistic material manufacturers possessing extensive research capabilities and established military relationships. Tier 1 companies including BAE Systems, Honeywell International, and DSM collectively command approximately 55-65% market share through proven product portfolios, comprehensive customer support, and strategic defense partnerships. BAE Systems, the market leader, maintains dominance through comprehensive ballistic protection solutions and established relationships with global defense departments.

Teijin Limited, through its Teijin Aramid subsidiary, maintains technology leadership through 35+ years of ballistics expertise and advanced fiber innovation. Tier 2 manufacturers, including Barrday Corporation, Gurit, and ArmorSource, manage approximately 25-30% market share, differentiating through specialized product development and niche application focus. Tier 3 emerging suppliers and regional manufacturers collectively account for approximately 10-15% market share, establishing competitive positions through cost advantages and regional market expertise. Competitive strategies emphasize R&D investments in hybrid composite optimization and smart technology integration. Supply chain consolidation and vertical integration initiatives are enabling established manufacturers to reduce manufacturing costs, thereby supporting sustained competitive positioning.

Key Market Developments:

- In November 2024, BAE Systems announced the advancement of modular composite armor systems incorporating hybrid fiber configurations, enabling customizable protection solutions tailored to diverse threat environments and operational requirements globally.

- In September 2024, Teijin Limited, through its Teijin Aramid subsidiary, initiated an advanced research program focused on metal-ion-bridge-linked aramid modification, achieving significant enhancements in tensile strength and improved friction characteristics for next-generation ballistic protection systems.

- In October 2024, Honeywell International Inc. unveiled smart composite monitoring systems that incorporate embedded sensors and real-time armor-integrity assessment, enabling enhanced threat detection and optimized protective performance for military and law enforcement applications.

Companies Covered in Ballistics Composites Market

- BAE Systems

- Barrday Corporation

- Honeywell International Inc.

- FY Composites OY

- PRF Composite Materials

- Morgan Advanced Materials

- Southern States LLC

- MKU Limited

- Gaffco Ballistics

- Gurit

- ArmorSource

- Royal Ten Cate NV

- Elmon

- Teijin Limited

- DSM

- DuPont

Frequently Asked Questions

The global ballistics composites market is projected to reach US$ 5.3 billion by 2033, expanding from US$ 3.2 billion in 2025 at a CAGR of 7.6%, driven by defense modernization programs, rising security threats, body armor demand growth, vehicle protection expansion, and emerging smart composite technology adoption supporting sustained market expansion.

Market demand growth is driven by multiple converging factors including escalating global security threats and armed conflicts requiring advanced protection equipment; defense modernization programs with governments allocating substantial budgets for protective systems.

Vehicle armor applications represent the dominant segment, commanding approximately 45% market share, driven by military vehicle modernization programs, lightweight composite panel adoption reducing vehicle weight while maintaining superior ballistic protection, mine-resistant vehicle development, and government investment in fleet modernization programs.

North America commands market leadership with approximately 40% global ballistics composites demand, anchored by the United States with world's largest defense budget exceeding USD 800 billion annually, extensive military and law enforcement infrastructure, and dominant defense contractor presence supporting sustained regional market dominance.

Major market opportunities include smart composite technology integration incorporating embedded sensors for real-time armor monitoring; aerospace ballistic protection applications for cockpit and crew safety; civilian security market expansion including armored transport and VIP protection; adaptive composite development with dynamic threat response capabilities; and next-generation soldier modernization programs.

Leading market players include BAE Systems, maintaining global market leadership through comprehensive protective solutions; Teijin Limited through Teijin Aramid offering 35+ years ballistics expertise and advanced fiber innovation; Honeywell International emphasizing smart technology integration; DSM providing advanced polymer composites; and regional players including MKU Limited in India and FY Composites supporting diverse regional market demands.