- Hardware & Software IT Services

- Arduino Compatible Market

Arduino Compatible Market Size, Trends, Share, and Growth Forecast, 2026 - 2033

Arduino Compatible Market by Product Type (Boards, Shields, Modules, Kits, and Others), Component (Microcontrollers, Sensors, Displays, Connectivity ICs, Power Management ICs and Others), Distribution Channel (Online and Offline), Industry (Consumer Electronics, Automotive, Industrial Automation, Healthcare, Telecommunication and Others), and Regional Analysis for 2026 - 2033

Arduino Compatible Market Size and Trends Analysis

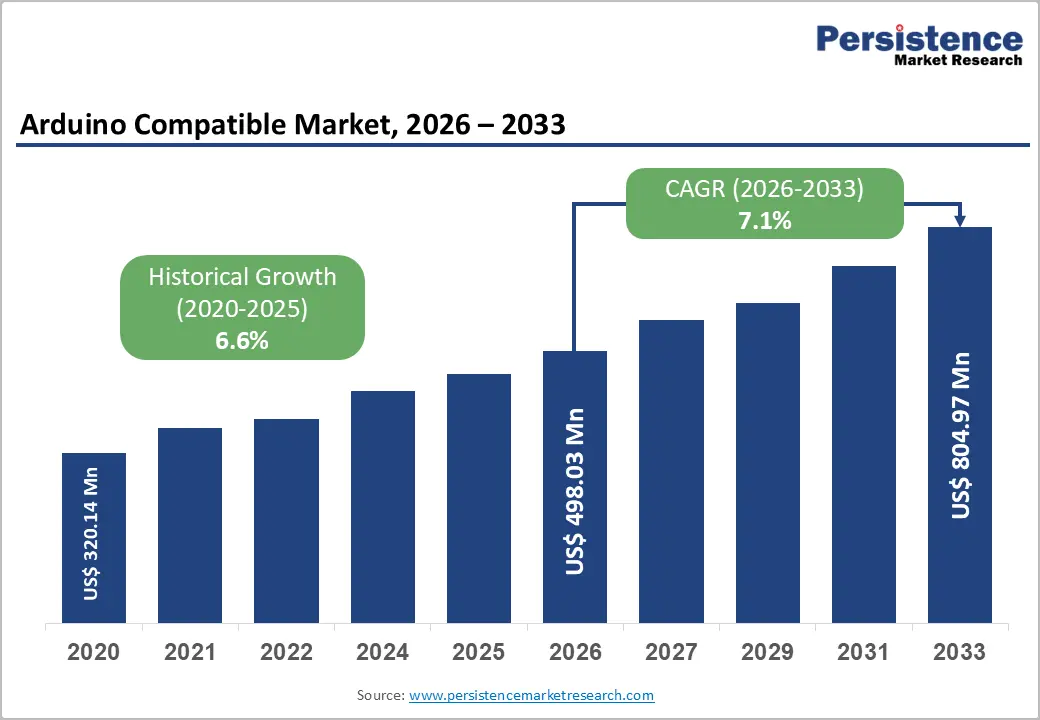

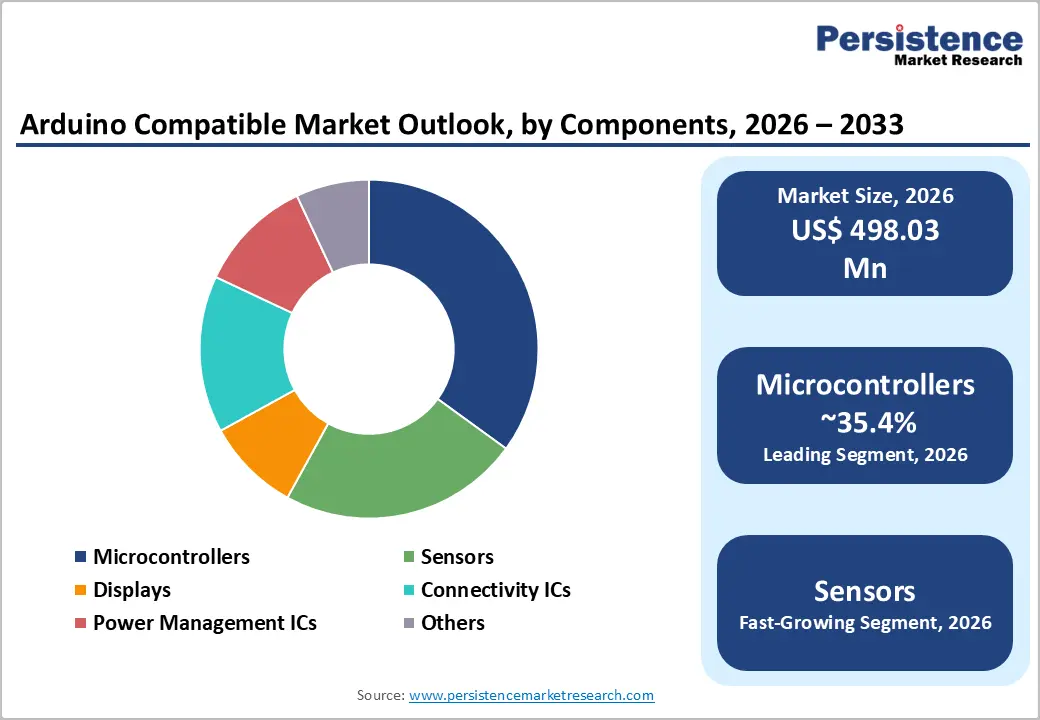

The global arduino compatible market size is likely to be valued at US$ 498.03 million in 2026 and is projected to reach US$ 804.97 million by 2033, growing at a CAGR of 7.1% between 2026 and 2033. The market is driven by DIY electronics accessibility, enabling rapid prototyping, massive global maker community expansion exceeding 10 million active participants, and integration of advanced technologies, including artificial intelligence and edge computing into Arduino-compatible platforms.

Key Industry Highlights:

- Leading Product Type: Boards dominate with a 32.6% share, establishing a platform foundation; Shields are the fastest-growing segment at a 12% CAGR, driven by functionality expansion and adoption of modular design.

- Dominant Component Type: Microcontrollers command 35.4% market share as system-architecture cores; Sensors are the fastest-growing, with an 18% CAGR, driven by IoT application expansion and edge-sensing adoption.

- Primary Industry: Consumer electronics holds 28.4% market share, with hobbyist and educational dominance; Automotive is the fastest-growing at a 16% CAGR, driven by connected vehicle development and IoT telematics.

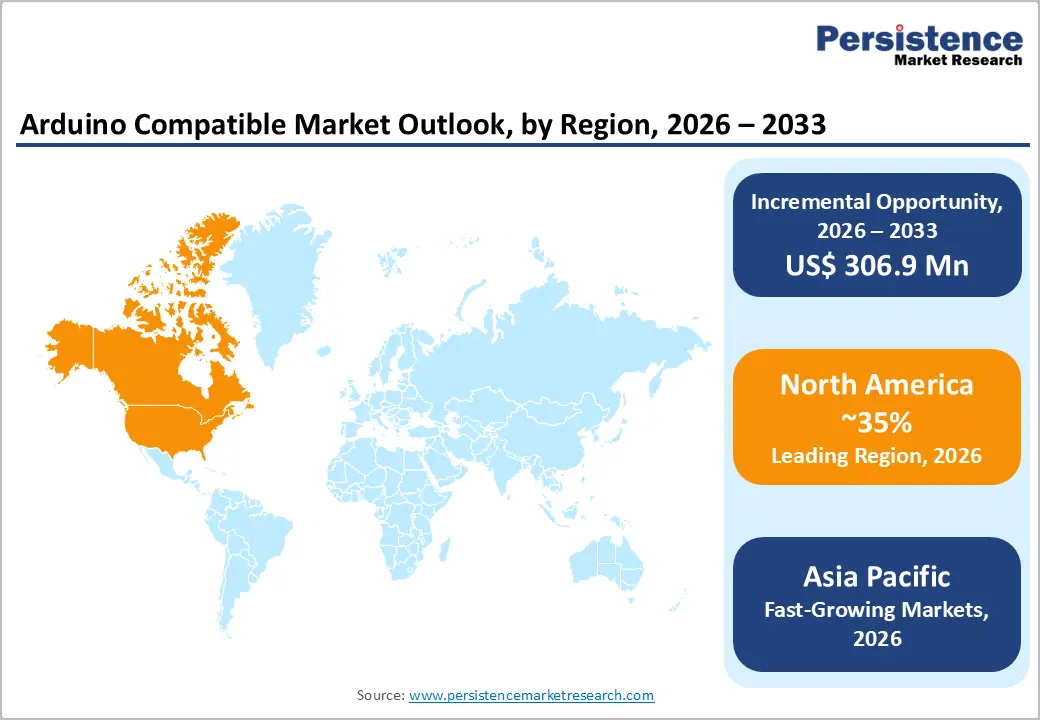

- Regional Market Leadership: North America maintains 35% global market share, driven by maker culture and educational adoption; Europe commands 25% share, with an emphasis on industrial automation; Asia Pacific demonstrates the fastest regional growth at a 12-15% CAGR, expanding from a 22% current share to 30% by 2033.

- Market Consolidation and Innovation Focus: Top 8 suppliers control 55% global market share (Arduino Inc., Adafruit, SparkFun, Arduino Pro, Seeed Studio, DFRobot leading); AI/ML integration expanding 20% annually; Emerging market educational expansion establishing 15% regional CAGR substantially exceeding developed market dynamics.

| Key Insights | Details |

|---|---|

|

Arduino Compatible Market Size (2026E) |

US$ 498.03 Mn |

|

Market Value Forecast (2033F) |

US$ 804.97 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

7.1% |

|

Historical Market Growth (CAGR 2020 to 2024) |

6.6% |

Market Dynamics

Drivers - Explosive Growth in DIY Electronics and Maker Culture with Global Community Expansion

Global maker and DIY community participation has expanded to 10+ million active users, with surveys indicating that 70% of designers and engineers use Arduino or Arduino-compatible boards for prototyping and proof-of-concept development. Makerspace proliferation, with 1,500+ officially registered makerspaces worldwide and thousands of informal community workshops, establishes infrastructure supporting Arduino adoption across educational and hobbyist segments. DIY electronics market valuation, estimated at US$ 4.5 billion in 2023 and projecting 15% annual growth through 2030, establishes a substantial market foundation.

Educational institution adoption, with 45% of STEM programs incorporating Arduino-based curriculum at primary, secondary, and tertiary levels, drives massive exposure for students. Online community engagement, with Arduino's official forums exceeding 3 million registered users and GitHub repositories containing 500,000+ Arduino-related projects, establishes ecosystem network effects. Eliminating accessibility barriers, with Arduino UNO cost declining to US$ 20-30 for entry-level pricing versus US$ 100+ for alternative development platforms, expands the addressable market to resource-constrained segments.

Accelerating IoT and Connected Device Proliferation with Industry 4.0 Adoption

The Internet of Things device deployment trajectory, with estimated connected devices exceeding 25 billion globally by 2030 per industry forecasts, establishes a proportionate demand driver for Arduino-compatible platforms. Industrial automation adoption, with Industry 4.0 implementations driving IoT sensor deployment across manufacturing facilities at 20% annual growth rates, creates sustained commercial demand. Smart city initiatives, with 600+ smart city projects globally, allocate US$ 200-500 billion in cumulative investment through 2030, establishing government-backed demand drivers for the Arduino ecosystem.

Edge computing integration, with 30% of IoT data processing shifting from the cloud to edge nodes to reduce latency and bandwidth requirements, is driving Arduino platform adoption for distributed intelligence. Prototyping efficiency advantages, with Arduino-based IoT development reducing time-to-market by 30% compared to custom silicon solutions, establish compelling economic justification.

Restraints - Supply Chain Vulnerability and Microcontroller Component Scarcity

Semiconductor supply chain concentration, with 80%+ of Arduino-compatible microcontroller chips manufactured by 3-4 major suppliers, establishes component dependency risks. Lead time volatility, with microcontroller procurement lead times fluctuating from 4-8 weeks to 12-24+ weeks during market shortage periods, constrains manufacturing flexibility and market responsiveness. Cost volatility, with microcontroller unit prices fluctuating 30-50% based on global semiconductor market dynamics, compresses profit margins and pricing predictability.

Manufacturing capacity constraints, with specialty microcontroller production requiring dedicated fabrication plants limiting supply expansion responsiveness. Geopolitical supply chain risks, with US-China tensions and Taiwan semiconductor production concentration, are creating political and economic uncertainties. Component obsolescence cycles, with microcontroller vendors discontinuing legacy products requiring periodic platform redesigns and compatibility management.

Intellectual Property and Ecosystem Fragmentation Challenges

Open-source licensing complexity, with diverse GPL, MIT, and proprietary licensing arrangements creating compatibility and commercial utilization uncertainties. Trademark and branding fragmentation, with 100+ unofficial "Arduino-compatible" manufacturers creating ecosystem confusion and quality inconsistency. Professional security requirements, with industrial and healthcare applications demanding security certifications and compliance frameworks challenging low-cost open-source business models. Documentation and standardization inconsistencies, with community-developed boards varying significantly in pin configurations and functionality versus official Arduino specifications. Technical support fragmentation, with non-official manufacturers providing inconsistent support quality affecting user experience and platform reputation. Competitive pressure from alternative platforms, including Raspberry Pi, MicroPython, and proprietary embedded systems, is constraining market share growth potential.

Opportunity - Automotive IoT Integration and Connected Vehicle Development

The expansion of the automotive IoT market, driven by connected vehicle adoption reaching 75%+ of new vehicle sales by 2030, establishes a high-growth Arduino application segment. Vehicle telematics requirements, with manufacturers deploying IoT sensors for predictive maintenance, fleet management, and autonomous vehicle development, are driving proportionate demand for Arduino-compatible platforms. Aftermarket customization, enabling consumers to prototype vehicle connectivity solutions and sensor integrations, establishes a DIY automotive market opportunity. Market opportunity estimates suggest automotive IoT Arduino applications will expand from US$ 40-60 million (2026) to US$ 150-200 million (2033), representing 18% CAGR substantially exceeding overall market growth. OEM partnerships, with major automotive manufacturers integrating Arduino platforms into development and prototyping workflows, establish ecosystem validation.

Healthcare Wearables and Remote Patient Monitoring Evolution

Healthcare IoT market expansion, with the wearable medical devices market projected to reach US$ 30-40 billion by 2033, establishes a high-growth opportunity for Arduino-compatible health monitoring platforms. The development of telehealth infrastructure, with remote patient monitoring systems requiring distributed IoT sensors and edge processing, drives Arduino adoption for prototype development. Personalized medicine applications, which enable genetic and biometric data collection via wearable sensors, create novel Arduino prototyping opportunities. Regulatory pathway simplification, with FDA providing expedited pathways for open-source medical device development, reduces commercialization barriers. Market opportunity estimates suggest healthcare Arduino applications will expand from US$ 50-70 million (2026) to US$ 180 million (2033), representing 18% CAGR. Integration with healthcare information systems and cloud platforms establishes ecosystem validation.

Category-wise Analysis

Product Type Insights

Arduino boards hold 32.6% market share in the product type segment, reflecting their role as the core platform of the Arduino-compatible ecosystem. These boards serve a wide range of users, from education to professional prototyping, with models such as the entry-level Arduino Uno, mid-range Mega, and advanced Due covering diverse price and performance needs. Support for multiple microcontroller architectures, including ARM Cortex and RISC-V, enhances versatility and future readiness. High annual shipment volumes and a large installed base reinforce ecosystem stability, while standardized pin layouts ensure compatibility across accessories and peripherals.

Arduino shields are the fastest-growing segment, expanding at a CAGR of around 12% through 2033. Shields extend functionality through modular, plug-and-play designs supporting connectivity, sensing, and control applications. Their low development cost and broad community participation enable rapid innovation, driving adoption across emerging IoT, automation, and edge-computing use cases.

Component Insights

Microcontrollers account for 35.4% of the component segment, reflecting their foundational role in Arduino-compatible system architecture. These components define processing capability, ranging from legacy 8-bit ATmega328 devices used in Arduino Uno to advanced 32-bit ARM Cortex-M processors deployed in Due and MKR series boards. Strong OEM partnerships with Microchip, ARM, and other silicon providers ensure supply stability and long-term platform continuity. Continuous performance improvements, enabled by firmware optimization in the Arduino IDE and standardized libraries, accelerate development and improve scalability for complex applications.

Sensors represent the fastest-growing component category, expanding at 14% CAGR through 2033. Rapid IoT adoption is driving demand for a diverse range of sensors, including environmental, motion, and biometric sensors. Falling component costs and increased integration of calibration and wireless features simplify system design, accelerating adoption across consumer, industrial, and wearable applications.

Industry Insights

Consumer electronics applications account for 28.4% of end-use demand, driven by strong adoption among hobbyists, DIY users, and educational institutions. Arduino platforms support a wide range of applications, including home automation, robotics, environmental monitoring, and interactive entertainment systems. Growth in smart homes, with global device deployments exceeding 500 million units, sustains long-term demand. Educational robotics programs and STEM curricula increasingly rely on Arduino-based kits for hands-on learning and competitions. A large maker community, supported by online repositories hosting over 100,000 project designs, reinforces ecosystem engagement and repeat purchases. Direct-to-consumer sales channels further enhance profitability and supplier focus.

Automotive applications are the fastest-growing segment, expanding at 16% CAGR through 2033. Demand is fueled by connected-vehicle prototyping, telematics development, autonomous-vehicle research, and aftermarket customization, where Arduino enables rapid, cost-effective innovation.

Regional Insights

North America Arduino Compatible Market Insights

North America commands approximately 35% of the global share, valued at approximately US$ 190 million in 2026, with projections approaching US$ 310 million by 2033. The United States represents the dominant regional market contributor, accounting for 85% ofthe North American market value, driven by maker culture prevalence and educational technology adoption.

Maker culture dominance, with North American makerspace concentration and maker faire proliferation establishing regional ecosystem leadership. Educational technology adoption, with STEM program standardization across K-12 and higher education driving institutional procurement. Corporate innovation labs, with tech companies establishing internal maker environments utilizing Arduino for rapid prototyping, drive commercial segment demand.

Europe Arduino Compatible Market Analysis

Europe represents approximately 24% of the global market, valued at approximately US$ 120 million in 2026. Germany, the United Kingdom, France, and Spain collectively represent 78% of the European market value, reflecting an established technology ecosystem and educational emphasis.

Educational standards adoption, with European STEM curriculum integration driving institutional Arduino deployment. Maker culture proliferation, with FabLab network expansion supporting maker community infrastructure. Industrial automation emphasis, with the German manufacturing sector driving IoT automation adoption, leveraging Arduino platforms.

Asia Pacific Arduino Compatible Market Insights and Analysis

The Asia Pacific region demonstrates robust growth dynamics, commanding approximately 22% market share and projections increasing to 30% by 2033. The region is likely to be valued at approximately US$ 110 million in 2026 is anticipated to reach US$ 270 million by 2033, representing the fastest-growing regional market with an estimated CAGR of 12% in the forecast period.

Educational technology expansion, with massive student populations and government digital transformation initiatives driving Arduino adoption in emerging markets. Manufacturing sector IoT integration, with China, Vietnam, and India establishing smart manufacturing initiatives requiring IoT development platforms. Startup ecosystem development, with tech entrepreneurship acceleration programs standardizing Arduino for rapid prototyping and MVP development.

Competitive Landscape

Prominent organizations, including STMicroelectronics, and Adafruit, are at the vanguard of this sector; STMicroelectronics is committed to developing innovative Arduino-compatible boards that meet the needs of its customers. The company invests heavily in research and development to stay ahead of the competition and offer the latest features and technologies.

STMicroelectronics is actively building relationships with key players in the Arduino ecosystem, such as software developers, hardware manufacturers, and educational institutions. These partnerships help to expand the reach of STMicroelectronics' Arduino-compatible products and make them more accessible to users.

Adafruit has cultivated a strong relationship with the maker community, catering to their needs and preferences through a comprehensive range of products, tutorials, and resources. The company engages with makers through online forums, social media, and in-person events, fostering a sense of belonging and loyalty.

Key Industry Developments:

- In March 2024, Spark Fun announced comprehensive open-source standardization effort promoting hardware design democratization and community contribution. Qwiic connector standardization enabling simplified plug-and-play ecosystem integration reduces design complexity.

- In September 2022, Arduino is an Italian open-source hardware and software company launched the Portenta H7 Lite, a low-cost version of the Portenta H7 microcontroller board aimed at students and hobbyists. The affordable pricing makes high-end Arm Cortex technology more accessible.

Companies Covered in Arduino Compatible Market

- Arduino

- Adafruit

- SparkFun

- Seeed Studio

- Microchip

- NXP Semiconductors

- STMicroelectronics

- Texas Instruments

- Cypress Semiconductor

- Silicon Labs

- Others Key Players

Frequently Asked Questions

The Arduino Compatible market is estimated to be valued at US$ 498.03 Mn in 2026.

The key demand driver for the Arduino Compatible market is the rapid growth of DIY electronics, prototyping, and embedded system development across education, hobbyist, and early-stage commercial applications.

In 2026, the North America region will dominate the market with an exceeding 35% revenue share in the global Arduino Compatible market.

Among Components, Microcontrollers hold the highest preference, capturing beyond 35.4% of the market revenue share in 2026, surpassing other component type.

The key players in Arduino Compatible are Arduino, Adafruit, SparkFun, and Seeed Studio.