- Medical Devices

- Anti-Snoring Devices Market

Anti-Snoring Devices Market Size, Share, Growth, and Regional Forecast, 2025 to 2032

Anti-Snoring Devices Market by Product Type (Mandibular Advancement Devices (MADs), Tongue Retaining Devices (TRDs), Others), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Stores / E-commerce, Others), and Regional Analysis from 2025 to 2032

Anti-Snoring Devices Market Size and Trends Analysis

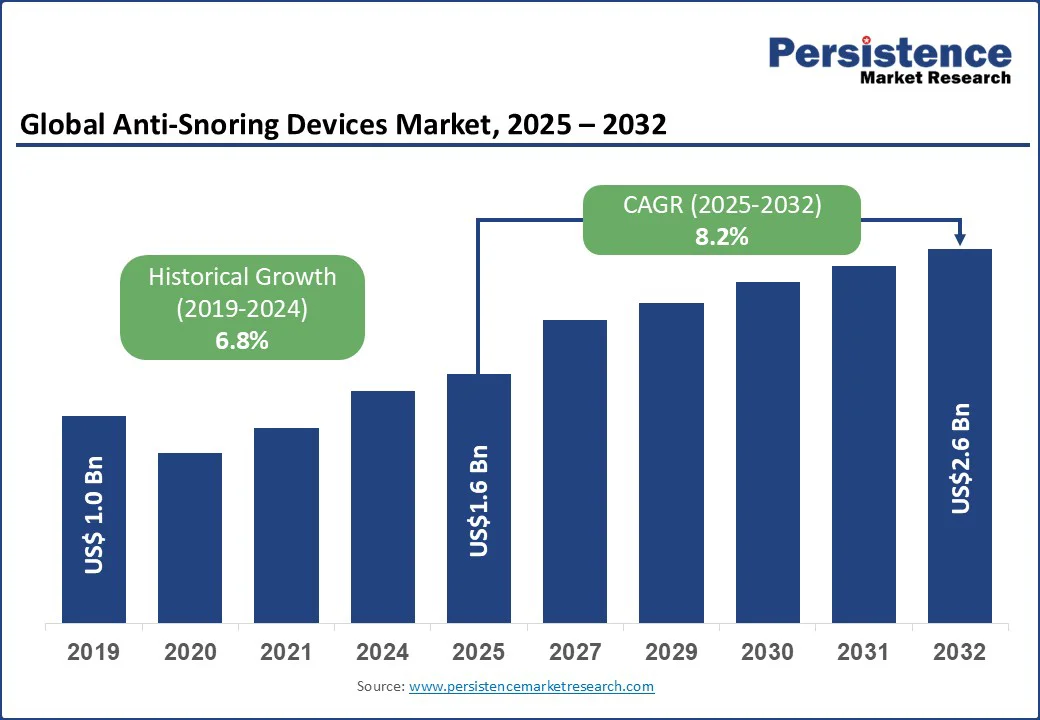

The global anti-snoring devices market size is projected to rise from US$ 1.6 Bn in 2025 to US$ 2.6 Bn by 2032. It is anticipated to witness a CAGR of 8.2% during the forecast period from 2025 to 2032.

The anti-snoring devices market is experiencing steady growth, fueled by the rising prevalence of sleep disorders, increasing awareness about the health risks of chronic snoring, and growing adoption of sleep apnea management solutions. Furthermore, it is supported by technological advancements in mandibular advancement devices, nasal dilators, and CPAP machines, which enhance comfort, usability, and treatment compliance.

Key Industry Highlights

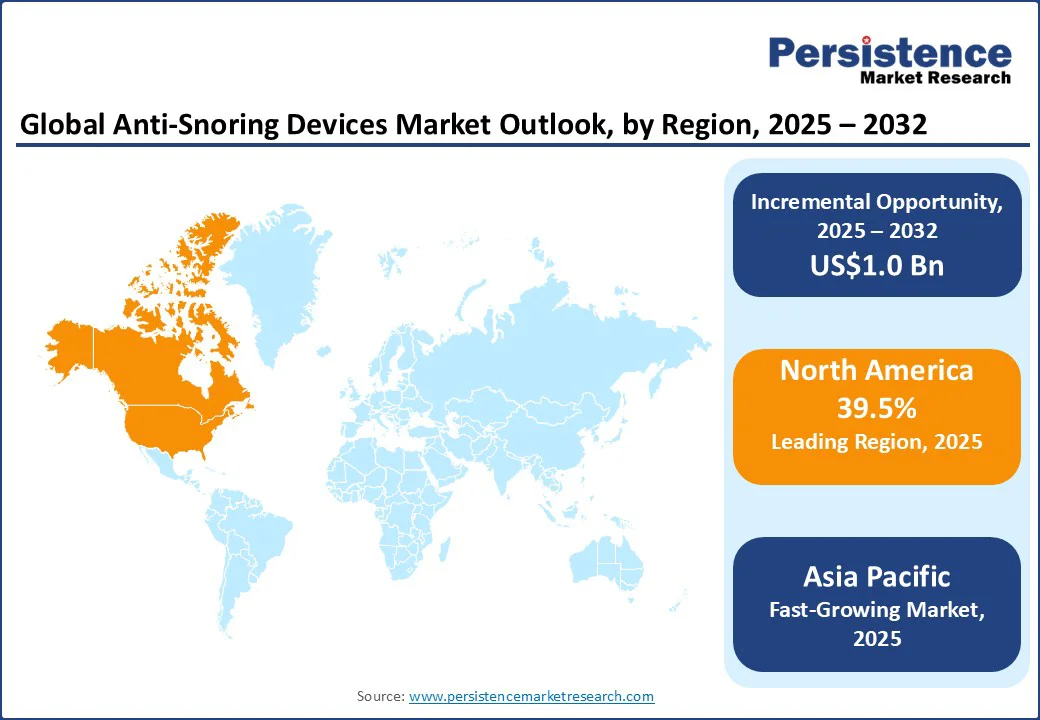

- Leading Region: North America is expected to lead the global market with approximately 39.5% share in 2025, underpinned by a high burden of sleep-disordered breathing and strong diagnosis rates.

- Fastest-growing Region: Asia Pacific is anticipated to be the fastest-growing region, driven by increasing awareness of sleep disorders and expanding healthcare access.

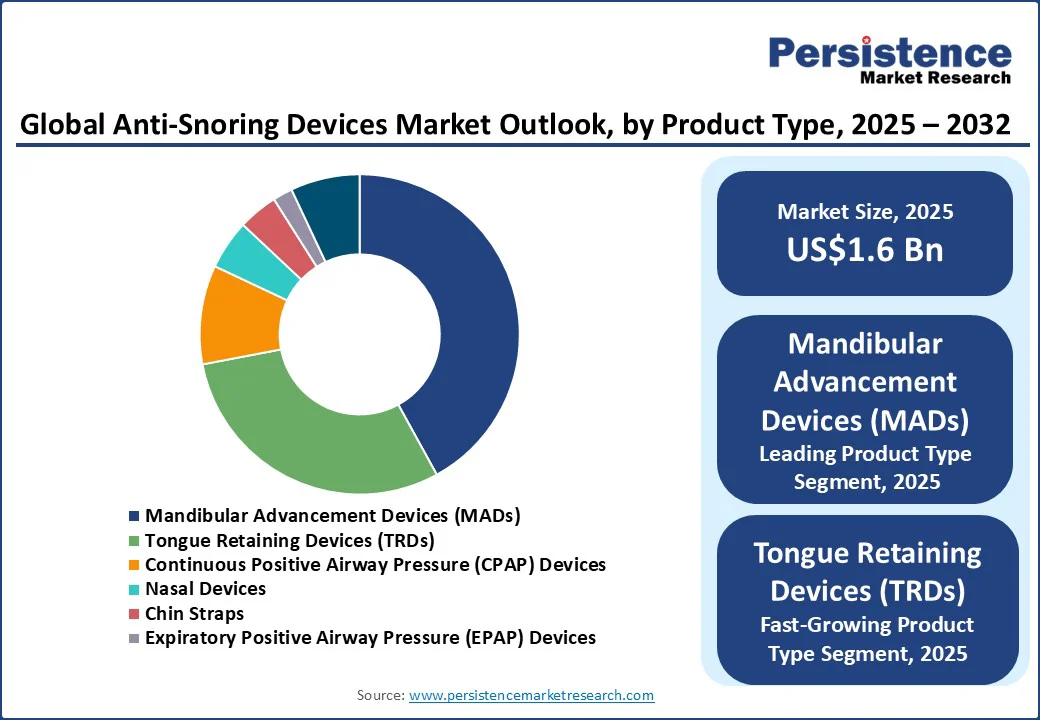

- Dominant Product Type: Mandibular Advancement Devices (MADs) are projected to be the leading segment with approximately 42.3% market share in 2025, due to their proven effectiveness and widespread adoption.

- Leading Distribution Channel: Online stores and e-commerce are likely to be the leading distribution channel, capturing approximately 47.1% market share in 2025, outpacing offline retail and specialty clinics due to shifting consumer behavior and rapid digital adoption.

|

Global Market Attribute |

Key Insights |

|

Anti-Snoring Devices Market Size (2025E) |

US$ 1.6 Bn |

|

Market Value Forecast (2032F) |

US$ 2.6 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

8.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.8% |

Market Dynamics

Driver - Increase in worldwide cases of obstructive sleep apnea (OSA) and habitual snoring

Increasing prevalence of obstructive sleep apnea (OSA) and habitual snoring worldwide indicates the need for anti-snoring devices. OSA is a serious condition where breathing repeatedly stops and starts during sleep, often linked with loud snoring and disrupted rest. According to the American Academy of Sleep Medicine (AASM), around 26% of U.S. adults between the ages of 30 and 70 suffer from sleep apnea, reflecting its widespread impact.

Additionally, the National Council on Aging highlights that nearly 90 million Americans snore, with about half being habitual snorers. On a global scale, the World Sleep Society estimates that about 936 million adults aged 30-69 years are affected by OSA, and nearly half of these cases are moderate to severe.

This rising burden increases the demand for anti-snoring devices, as untreated snoring and OSA are associated with cardiovascular diseases, fatigue, and reduced quality of life, pushing the adoption of effective solutions.

Restraints - Low Patient Compliance and Discomfort

Many users of mandibular advancement devices (MADs), tongue retaining devices (TRDs), or CPAP machines report difficulties in long-term adherence due to discomfort, inconvenience, or side effects. For example, studies cited by the American Academy of Sleep Medicine (AASM) highlight that nearly 30-50% of CPAP users discontinue therapy within the first year due to issues such as nasal dryness, mask leakage, and difficulty sleeping with the equipment.

Oral appliances such as MADs often cause jaw pain, dental discomfort, or excessive salivation, leading patients to abandon regular use. This lack of consistent adherence significantly limits the effectiveness of treatment despite proven clinical benefits. As a result, even though anti-snoring devices are technologically effective, poor patient compliance remains a critical challenge for widespread adoption in managing snoring and obstructive sleep apnea.

Opportunity - Technological Advancements in Smart Wearable Devices

Technological advancements in smart wearable monitoring represent a significant opportunity for the market, driven by increasing adoption of consumer health tracking. A 2023 survey by the American Academy of Sleep Medicine found that over one-third of Americans use sleep-tracking tools ranging from wearable smartwatches to smartphone apps, and importantly, 77% of those users reported it helped them, with 68% subsequently modifying their sleep behaviors.

Research further highlights that devices leveraging built-in sensors such as accelerometers and photoplethysmography (PPG) can accurately detect obstructive sleep apnea (OSA) events. One smartwatch system demonstrated over 92% accuracy in detecting moderate-to-severe OSA.

Additionally, cutting-edge innovations such as "smart pajamas" equipped with fabric-based sensors have achieved nearly 98.6% accuracy in identifying snoring and apnea episodes, while offering comfort and seamless data transmission. Together, these developments suggest a growing market for integrated smart wearable anti-snoring solutions that enhance detection, patient engagement, and seamless user experience.

Category-wise Analysis

Product Type Insights

Mandibular Advancement Devices (MADs) are projected to be the leading segment with 42.3% share in 2025, due to their proven effectiveness and widespread adoption. According to the American Academy of Sleep Medicine (AASM), oral appliances such as MADs are a recommended first-line therapy for patients with mild to moderate obstructive sleep apnea (OSA) who either cannot tolerate or prefer alternatives to CPAP therapy.

Research published in the National Institutes of Health (NIH) indicates that MADs can reduce the apnea-hypopnea index (AHI) by 50% or more in approximately 65-70% of patients. Their non-invasive nature, customizability, and higher patient compliance compared to CPAP devices contribute to their market leadership.

Additionally, a CDC report (2022) highlighted that nearly 26% of U.S. adults report habitual snoring, with MADs being one of the most prescribed solutions by dental and sleep specialists. This widespread clinical acceptance, coupled with better comfort and portability, explains why MADs lead the market.

Distribution Channel Insights

Online stores and e-commerce are likely to be the leading distribution channels, accounting for approximately 47.1% market share in 2025, outpacing offline retail and specialty clinics due to shifting consumer behavior and rapid digital adoption. Patients and caregivers increasingly prefer purchasing anti-snoring devices such as mandibular advancement devices, nasal dilators, and chin straps online, owing to the convenience of doorstep delivery, discreet purchasing, wide product availability, and competitive pricing.

The growth of healthcare e-commerce, which now accounts for a significant share of medical device sales, further strengthens this trend. With consumers relying more on digital platforms to manage sleep-related health concerns, online stores have become the largest and fastest-growing segment in the market.

Regional Insights

North America Anti-Snoring Devices Market Trends

North America is expected to lead the global market with a 39.5% share in 2025, underpinned by a high burden of sleep-disordered breathing and strong diagnosis rates. In the U.S., an estimated 39 million adults suffer from obstructive sleep apnea (OSA), with 94% of those affected reporting snoring as a symptom. A broader epidemiological review indicates that about one in five American adults exhibits at least mild OSA, with prevalence substantially higher in older and overweight populations.

In Canada, approximately 6.4% of adults reported a formal sleep apnea diagnosis during 2016-17, up from 3% in 2009, and 26% exhibit symptoms or risk factors suggesting a high likelihood of OSA. Additionally, CDC data indicate that 48% of U.S. adults report snoring, with 41% having sleep-related breathing symptoms.

This elevated prevalence, combined with widespread screening, clinical infrastructure, and patient awareness, positions North America as the dominant and most mature market for anti-snoring devices.

Asia Pacific Anti-Snoring Devices Market Trends

Asia Pacific is anticipated to be the fastest-growing region, driven by increasing awareness of sleep disorders and expanding healthcare access. Sleep apnea and habitual snoring affect a substantial portion of adults in the region.

For instance, a study published by the Journal of Clinical Sleep Medicine reports that approximately 10-15% of adults in India and 15-20% in China experience moderate to severe obstructive sleep apnea (OSA). The rising recognition of these conditions by healthcare providers has led to higher prescriptions of oral appliances such as Mandibular Advancement Devices (MADs) and other anti-snoring aids.

Technological advancements, such as custom-fitted devices and mobile-connected smart wearables, are enhancing patient comfort and adherence. Urbanization and higher disposable incomes in countries like China, India, and Japan are making these devices more accessible. Furthermore, the expansion of e-commerce platforms allows consumers to purchase devices conveniently and discreetly, contributing to faster adoption across the region.

Europe Anti-Snoring Devices Market Trends

Europe is expected to account for approximately 27.7% of the global anti-snoring devices market in 2025, driven by the high prevalence of sleep-disordered breathing and the growing adoption of treatment solutions across the region. Approximately 175 million individuals across Europe suffer from obstructive sleep apnea (OSA), with about 90 million experiencing moderate to severe forms requiring clinical intervention.

In France, a representative population-based study (CONSTANCES cohort) revealed that 3.5% of adults have verified, treated sleep apnea, and up to 20.9% are at high risk or already being treated, with prevalence rising sharply with age from 11.1% in those under 40 to 31.3% in adults 60 and older. Meanwhile, habitual snoring affects nearly 35% of middle-aged men in Lorraine, France.

These high prevalence rates, particularly of moderate to severe OSA and habitual snoring, underscore a significant need for accessible anti-snoring solutions. The gap between the broad base of affected individuals and those receiving treatment also highlights untapped opportunities for device adoption. Combined with growing clinical awareness and improving diagnostic pathways, Europe’s substantial and evolving demand makes it a key region for market growth and innovation in anti-snoring devices.

Competitive Landscape

The global anti-snoring devices market is moderately fragmented, featuring a mix of specialized sleep device companies, dental appliance manufacturers, and global healthcare firms. Leading players focus on product innovation, comfort, efficacy, and distribution expansion to capture market share. Key competitors include ResMed, SomnoMed, ProSomnus Sleep Technologies, Vivos Therapeutics, Inc., and Koninklijke Philips N.V.

Key Industry Developments:

- In January 2025, ResMed launched a new device for patients with sleep apnea in India. The device was designed to help manage obstructive sleep apnea more effectively, offering improved comfort, ease of use, and adherence for patients.

- In December 2024, ZQuiet launched the ZQuiet Advance, an anti-snoring mouthpiece designed for a custom fit. It features moldable trays and adjustable settings with four levels of jaw advancement. Additionally, the device is slim and lightweight, which addresses common user concerns and discomfort caused by pressure on the front teeth.

- In October 2024, AppySleep launched a wristband to stop snoring. It activates gentle vibrations when snoring is detected, prompting users to a side-sleeping position to reduce snoring.

Companies Covered in Anti-Snoring Devices Market

- ResMed

- SomnoMed

- ProSomnus Sleep Technologies

- Vivos Therapeutics, Inc.

- Koninklijke Philips N.V.

- DynaFlex

- Fisher & Paykel Healthcare Limited

- Apnea Sciences Corporation

- MPowrx Health and Wellness Products

- MEDiTAS Ltd.

- The Pure Sleep Company

- Tomed GmbH

- ZQuiet

- Zeus Sleep

- Smart Nora

- Panthera Sleep

- The Sleep Doctor

- VitalSleep

- Good Morning Snore Solution

- SleepTight

Frequently Asked Questions

The global anti-snoring devices market is projected to be valued at US$ 1.6 Bn in 2025.

Rising sleep apnea prevalence, lifestyle factors, awareness, and the demand for non-invasive treatments drive market growth.

The anti-snoring devices market is poised to witness a CAGR of 8.2% between 2025 and 2032.

Technological innovations, telehealth integration, and growing awareness create strong opportunities in the anti-snoring devices market.

Major players include ResMed, SomnoMed, ProSomnus Sleep Technologies, Vivos Therapeutics, Inc., Koninklijke Philips N.V., and DynaFlex.