- Pharmaceuticals

- Anti-Hyperglycemic Agents Market

Anti-Hyperglycemic Agents Market Size, Share, and Growth Forecast, 2026 – 2033

Anti-Hyperglycemic Agents Market by Drug Class Type (GLP-1 Receptor Agonists, Insulin, Others), Disease Type (Type 1 Diabetes, Type 2 Diabetes), Patient Age Groups (Adult, Geriatric, Pediatric), Distribution Channel, and Regional Analysis 2026 – 2033

Anti-Hyperglycemic Agents Market Size and Trends Analysis

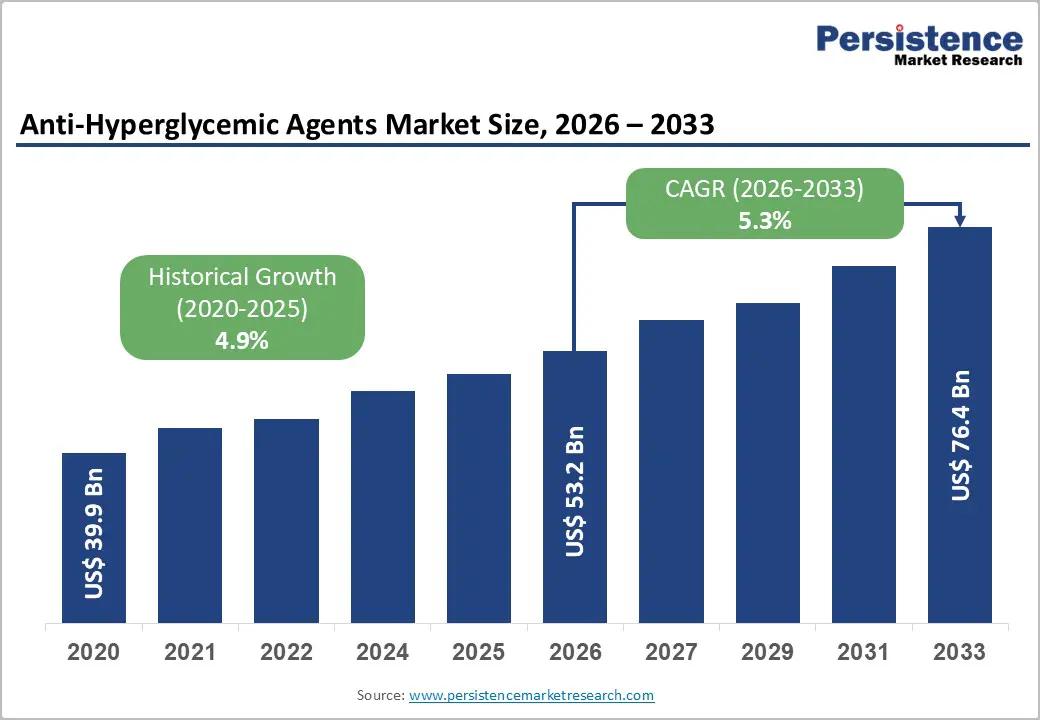

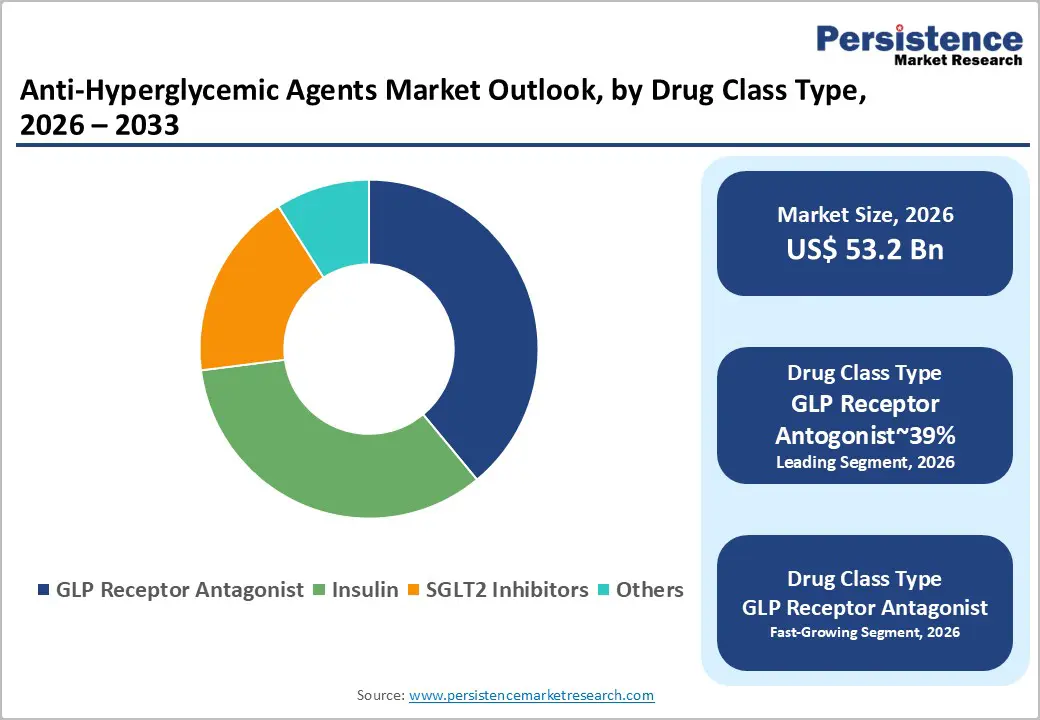

The global anti-hyperglycemic agents market size is likely to be valued at US$53.2 billion in 2026 and is expected to reach US$76.4 billion by 2033, growing at a CAGR of 5.3% during the forecast period from 2026 to 2033, driven by the escalating global prevalence of metabolic disorders and the shift toward higher-value incretin-based therapies. Structural advancements in drug delivery systems and the expansion of healthcare infrastructure in emerging economies further underpin the market's upward trajectory.

Demand remains resilient as therapeutic protocols increasingly prioritize cardiovascular and renal protection alongside traditional glycemic control. Demographic shifts, including aging populations, further drive demand, supported by regulatory approvals for biosimilars that enhance accessibility.

Key Industry Highlights:

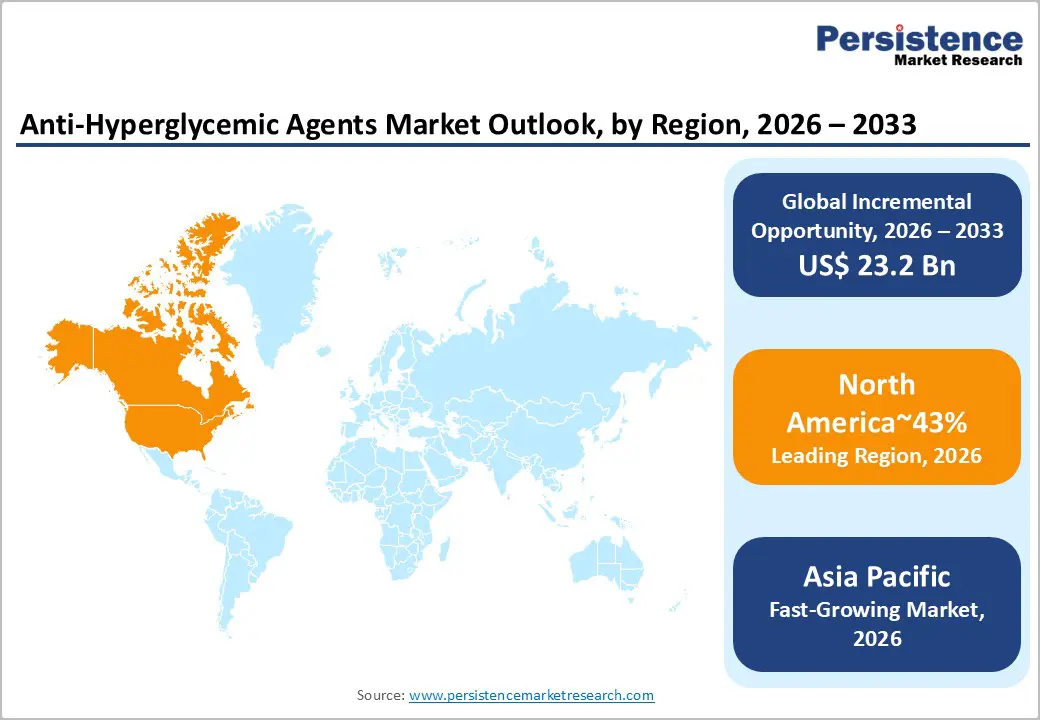

- Leading Region: North America is projected to lead due to high healthcare expenditure, advanced diabetic care infrastructure, and widespread adoption of GLP-1 receptor agonists, accounting for approximately 43% share.

- Fastest-Growing Region: Asia Pacific, due to the rising diabetes prevalence, expanding healthcare access, and increasing adoption of modern anti-hyperglycemic therapies.

- Leading Drug Class Type: GLP-1 receptor agonists are expected to lead, accounting for approximately 39%, driven by superior efficacy, dual glucose and weight management benefits, and high adoption in developed markets.

- Leading Disease Type: Type 2 diabetes is projected to dominate with approximately 80%, reflecting its high prevalence, chronic management needs, and alignment with therapeutic class innovations.

| Key Insights | Details |

|---|---|

| Anti-Hyperglycemic Agents Market Size (2026E) | US$ 53.2 Bn |

| Market Value Forecast (2033F) | US$ 76.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Rising Prevalence of Type 2 Diabetes and Obesity-Linked Metabolic Syndromes

The anti-hyperglycemic agents market is structurally propelled by the persistent global increase in type 2 diabetes prevalence. Rising obesity prevalence has directly contributed to an expanding population exhibiting insulin resistance, thereby increasing reliance on long-term pharmacological interventions. GLP-1 receptor agonists and SGLT2 inhibitors have gained prominence due to their combined ability to regulate glycemic levels while addressing cardiovascular and obesity-related risks. This dual efficacy is reshaping treatment paradigms, influencing prescribing behaviors, and progressively integrating these agents into standard-of-care guidelines across both mature and emerging healthcare systems. The shift reflects a broader emphasis on therapies that simultaneously manage metabolic parameters and reduce comorbidity burdens.

The mounting chronic disease load exerts significant pressure on healthcare infrastructures, necessitating strategic allocation of resources for sustained diabetes management, including procurement, distribution, and reimbursement mechanisms. Pharmaceutical manufacturers are scaling production to satisfy rising demand for high-efficacy compounds, while regulatory frameworks increasingly prioritize therapeutics with multifactorial benefits. Payer policies are evolving to support agents with favorable health economics, thereby reinforcing sustained revenue growth and therapeutic penetration across diverse regional markets.

Technological Innovation in Drug Delivery and Formulation

The anti-hyperglycemic agents market is increasingly shaped by technological advancements in drug delivery and formulation, which enhance patient adherence and clinical outcomes. The shift from daily subcutaneous injections to once-weekly injectables and oral small molecules represents a structural improvement in chronic disease management. Oral GLP-1 receptor agonists and next-generation formulations have enabled access to patient segments previously reluctant to initiate injectable therapy, reducing clinical inertia in primary care settings. Biosimilar manufacturing innovations are also improving affordability and distribution efficiency, expanding market accessibility in cost-sensitive regions. Simultaneously, biosimilar manufacturing advancements are enhancing affordability and distribution efficiency, enabling penetration in cost-sensitive regions.

These technological shifts also influence procurement and reimbursement strategies by demonstrating improved adherence, real-world efficacy, and reduced hospitalization risk. At the molecular and therapeutic class level, GLP-1 receptor agonists and SGLT2 inhibitors offer superior glycemic control while addressing cardiorenal risk factors, structurally redefining standard-of-care protocols. R&D investments have produced novel oral and long-acting formulations, shaping regulatory approvals, market entry timelines, and competitive positioning. These innovations are reinforcing treatment penetration across diverse geographies, driving sustained demand, and creating high-value opportunities within the overall diabetes pharmacotherapy ecosystem.

Barrier Analysis – Patent Cliffs and Generic Competition

The anti-hyperglycemic agents market faces structural constraints from patent expirations of high-revenue therapeutics, prompting a wave of generic market entry. Loss of exclusivity for key molecules induces significant price erosion, substantially compressing revenue streams for originator manufacturers. This dynamic alters the competitive landscape, as generics capture market share through cost-sensitive channels while maintaining therapeutic equivalence. Healthcare payers and providers increasingly favor lower-cost alternatives, accelerating substitution and impacting branded product volumes across diverse regions. The resulting margin contraction pressures research and development allocation, influencing portfolio prioritization and lifecycle management strategies.

The influx of generic entrants is reshaping the anti-hyperglycemic market by introducing pronounced pressures on supply chain planning, procurement strategies, and distribution economics. The surge of generic entrants affects supply chain planning, procurement strategies, and distribution economics, embedding structural price sensitivities throughout the market. Regulatory frameworks governing bioequivalence and accelerated approval pathways further facilitate rapid generic penetration. Consequently, originator firms face intensified competition, necessitating strategic responses in formulation innovation, combination therapies, and differentiated delivery systems to sustain market presence despite the structural revenue limitations imposed by patent expirations.

Opportunity Analysis – Convergence of AI and Personalized Metabolic Medicine

The anti-hyperglycemic agents market is structurally positioned to benefit from the integration of artificial intelligence and personalized metabolic medicine, enabling precision pharmacotherapy. AI-driven platforms predict individual patient responses to specific drug classes, allowing clinicians to tailor dosing and minimize adverse events such as hypoglycemia. This convergence improves therapeutic efficacy, enhances adherence, and embeds real-world outcomes into clinical decision-making frameworks. Digital health tools, including smart insulin pens and continuous glucose monitoring applications, are increasingly bundled with pharmacological interventions, transforming standalone treatments into integrated diabetes management solutions.

These digital-therapeutic integrations create high-value opportunities for manufacturers, payers, and healthcare providers by aligning treatment performance with patient-centric data. Platforms supporting adaptive dosing and predictive analytics reinforce brand differentiation, encourage patient loyalty, and expand access across both mature and emerging markets. Adaptive dosing and predictive analytics platforms reinforce brand differentiation, foster patient loyalty, and enable broader access across mature and emerging markets. Regulatory recognition of digital therapeutics and interoperability standards further solidifies market potential, embedding AI-enabled precision care as a structural growth driver within the overall anti-hyperglycemic ecosystem.

Biosimilars and Combination Therapies

The anti-hyperglycemic agents market is structurally expanding through the development of biosimilars and combination therapies, which address cost, adherence, and multifactorial disease management. Biosimilar insulin analogs increase affordability and accessibility, particularly in price-sensitive and emerging healthcare markets, while maintaining therapeutic equivalence with originator products. Combination therapies, integrating agents such as GLP-1 receptor agonists with basal insulin or SGLT2 inhibitors, simplify treatment regimens, reduce pill burden, and improve glycemic control, thereby enhancing patient adherence and clinical outcomes. These innovations are reshaping prescribing practices and influencing formulary decisions across both public and private payer systems.

The adoption of biosimilars and fixed-dose combinations alters manufacturing, regulatory, and distribution dynamics, requiring optimized production processes and robust pharmacovigilance frameworks. Payer incentives increasingly favor cost-effective, high-efficacy therapies, facilitating broader adoption and market penetration. The convergence of affordability, simplified administration, and therapeutic efficacy positions these strategies as structural growth opportunities, enhancing market accessibility while sustaining competitive differentiation in the evolving anti-hyperglycemic agents landscape.

Category–wise Analysis

Drug Class Type Insights

GLP-1 receptor agonists are expected to lead, accounting for approximately 39% share in 2026, underpinned by their entrenched clinical efficacy in both blood glucose reduction and substantial weight loss across Type 2 diabetes patient populations. Adoption remains anchored by its dual therapeutic benefit, cardiovascular protection, and favorable impact on metabolic comorbidities, with providers prioritizing treatment standardization and patient adherence in chronic disease management. Brand portfolios such as Ozempic, Trulicity, and Rybelsus consolidate market presence, integrating innovation with patient-centric delivery systems. This combination of established clinical performance, evolving administration routes, and strong ecosystem adoption sustains the segment’s dominance within structured therapeutic deployment models.

GLP-1 receptor agonists are expected to be the fastest-growing segment, driven by emerging unmet needs for convenient, non-invasive treatment modalities and expanded indications across obesity, chronic kidney disease, and cardiovascular risk management. Growth is catalyzed by the transition from injectable to oral formulations and biosimilar development, which materially improves patient adherence, accessibility, and treatment personalization. Accelerating adoption is supported by AI-enabled dosing optimization, continuous glucose monitoring integration, and digital therapeutic platforms that reduce operational friction for clinicians and patients. As clinical validation, guideline inclusion, and workflow familiarity improve, this segment is expected to outpace overall market growth over the forecast period.

Disease Type Insights

Type 2 diabetes is anticipated to dominate, accounting for approximately 80% share in 2026, underpinned by its entrenched prevalence among adults with lifestyle-induced metabolic dysfunction. Adoption remains anchored by the high volume of patients requiring chronic oral and injectable therapies, with healthcare providers prioritizing standardized treatment protocols and consistent glycemic control across outpatient and clinical settings. Ongoing innovations in drug delivery, including long-acting insulin analogs and GLP-1 receptor agonists, continue to reinforce treatment adherence and utilization intensity. Brands such as Novo Nordisk, Eli Lilly, and Sanofi consolidate market presence, integrating established therapies with evolving patient management ecosystems. This combination of mature infrastructure, high prescription volumes, and predictable demand sustains Type 2 Diabetes as the dominant disease segment within structured pharmacotherapy models.

Type 1 diabetes is expected to be the fastest-growing segment, driven by rising global autoimmune incidence and the high-value nature of insulin-dependent treatment requirements. Growth is catalyzed by advances in next-generation insulin analogs, continuous glucose monitoring integration, and emerging cell-based therapies, which materially improve patient outcomes and long-term disease management. Accelerating adoption is supported by digital health tools and precision dosing platforms that reduce operational complexity for first-time users. Brands such as Novo Nordisk, Eli Lilly, and Vertex are embedding early-cycle demand through innovative therapy models and integrated care pathways.

Regional Insights

North America Anti-Hyperglycemic Agents Market Trends

North America is expected to remain the leading region, accounting for approximately 40% of the global share in 2026, underpinned by deep enterprise penetration, advanced therapeutic infrastructure, and early adoption of high-efficacy branded drugs. Adoption is anchored in robust reimbursement mechanisms and a mature regulatory environment led by the FDA, which fast-tracks innovative dual and triple incretin agonists, accelerating market entry and enhancing revenue per patient. The region’s ecosystem benefits from concentrated R&D investment, particularly in automated insulin delivery systems, AI-enabled metabolic monitoring, and oral GLP-1 formulations, reinforcing treatment adherence and clinical outcomes. Major vendors such as Novo Nordisk, Eli Lilly, and Sanofi consolidate market leadership, integrating portfolio innovation with established care networks.

The U.S. anchors North America’s market momentum, driving adoption through the high prevalence of obesity and type 2 diabetes, coupled with widespread healthcare access and premium therapy uptake. Investment flows target advanced glucose monitoring platforms, AI-driven dosing tools, and next-generation incretin therapies, shaping forward-looking procurement and prescribing patterns. Vendor strategies prioritize portfolio expansion, patient-centric digital integration, and ecosystem lock-in, with Eli Lilly’s Mounjaro and Novo Nordisk’s oral GLP-1 launches exemplifying structural market leverage. Technology integration and strategic clinical trials in the U.S. are expected to continuously accelerate penetration, ensuring North America maintains global market primacy through innovation-led growth and sustained therapeutic sophistication.

Europe Anti-Hyperglycemic Agents Market Trends

Europe is expected to remain a structurally important market, underpinned by regulatory harmonization through the EMA and a mature focus on cost-effectiveness and public health optimization. Adoption is anchored by sophisticated Health Technology Assessments that balance innovation with healthcare budgets, enabling selective uptake of high-efficacy therapies while promoting biosimilars and sustainable care models. The region’s industrial ecosystem benefits from a mix of established manufacturers such as Sanofi and Novo Nordisk, alongside competitive generic entrants, supporting broad treatment access across chronic disease management programs. Integration of SGLT2 inhibitors into heart failure and metabolic care pathways, coupled with investment in hybrid therapy platforms, continues to reinforce structured utilization across diverse patient populations and care settings.

Germany anchors Europe’s market momentum, shaping regional dynamics through advanced reimbursement mechanisms, DiGA-like digital therapeutics programs, and accelerated HTA approval processes. Investment flows target both oral and injectable GLP-1 therapies, biosimilar insulin analogs, and integrated diabetes management solutions, reinforcing forward-looking prescribing patterns. Technology adoption, coupled with demographic pressures from an aging population, is expected to sustain steady uptake, maintaining Europe’s high-value positioning within the global anti-hyperglycemic ecosystem.

Asia Pacific Anti-Hyperglycemic Agents Market Trends

Asia Pacific is expected to register the fastest growth trajectory, driven by rapid urbanization, rising middle-class populations, and a substantial Type 2 Diabetes patient base across China, India, and Southeast Asia. Adoption is anchored by expanding access to modern therapies through structured reimbursement frameworks, the proliferation of digital health platforms, and the integration of biosimilars and generic insulins into treatment protocols. The region’s structural advantage lies in its manufacturing depth, with India and China serving as global hubs for metformin and biosimilar insulin production. Investments in localized R&D, including domestic GLP-1 candidates from Biocon and Innovent Biologics.

China anchors Asia Pacific’s regional momentum, shaping adoption through extensive urban healthcare infrastructure, evolving National Reimbursement Drug Lists, and government-led chronic disease screening programs. Regulatory acceleration of generics and biosimilars reduces time-to-market, while local manufacturing capacity supports cost-efficient scale-up for domestic and export markets. Technology adoption, rising healthcare coverage, and digital-enabled prescribing are expected to sustain high-volume uptake, positioning China as the primary growth driver and innovation hub for the regional anti-hyperglycemic ecosystem.

Competitive Landscape

The global anti-hyperglycemic agents market is highly consolidated, with top players such as Novo Nordisk, Eli Lilly, Sanofi, AstraZeneca, and Merck capturing the majority of market influence. This concentration reflects substantial technical and financial barriers, including the complexity of biologic development and the execution of large-scale cardiovascular outcome trials, which limit entry for smaller competitors. Market structure is further reinforced by the integration of branded portfolios, global distribution networks, and established clinical trial infrastructures that underpin product adoption across multiple care settings.

Leading players exert significant functional influence through their technological footprint and procurement impact, shaping therapy standards and clinical guidelines. Industry dynamics are characterized by sustained innovation, platform evolution, and incremental consolidation, as vendors expand service models and clinical support ecosystems to reinforce patient adherence and treatment outcomes, maintaining a structurally dominant presence across the global anti-hyperglycemic landscape.

Key Industry Developments:

- In February 2026, the FDA launched the "PreCheck Pilot Program" to strengthen domestic pharmaceutical manufacturing, enhancing regulatory oversight and improving supply chain resilience for critical medications used in treating chronic diseases.

- In January 2026, Sanofi's Teizeild gained approval in the EU for patients with stage 2 type 1 diabetes, offering a breakthrough therapy that delays the onset of clinical (stage 3) type 1 diabetes in at-risk children and adults.

- In May 2025, AstraZeneca received a recommendation for Forxiga (dapagliflozin) to treat chronic kidney disease, expanding the drug's clinical utility and driving its adoption in patients with cardiorenal comorbidities.

Companies Covered in Anti-Hyperglycemic Agents Market

- Novo Nordisk A/S

- Eli Lilly and Company

- Sanofi

- AstraZeneca PLC

- Merck & Co., Inc.

- Boehringer Ingelheim

- Johnson & Johnson

- Pfizer Inc.

- Roche Group

- Biocon Limited

- Novartis AG

- Sun Pharmaceutical Industries

- Takeda Pharmaceutical Company

- Cipla Inc.

- Abbott Laboratories

Frequently Asked Questions

The global anti-hyperglycemic agents market is projected to be valued at US$53.2 billion in 2026 and is expected to reach US$76.4 billion by 2033, driven by the escalating prevalence of type 2 diabetes and the structural shift toward higher-value incretin-based therapies such as GLP-1 receptor agonists.

The increase in insulin resistance, fueled by rising obesity rates, has created a large population requiring long-term pharmacological intervention. GLP-1 agonists and SGLT2 inhibitors have become central to treatment protocols due to their dual efficacy in glycemic control and cardiovascular/renal protection, reshaping prescribing behaviors and embedding these therapies into standard-of-care guidelines.

The anti-hyperglycemic agents market is forecast to grow at a CAGR of 5.3% from 2026 to 2033, reflecting resilient demand from aging populations and the expanding therapeutic applications of modern drug classes.

North America is the leading regional market, accounting for approximately 43% share, supported by high healthcare expenditure, advanced care infrastructure, and rapid adoption of premium GLP-1 therapies. Asia Pacific is the fastest-growing region, driven by a substantial and growing type 2 diabetes patient base, expanding healthcare access, and increasing adoption of modern therapies.

The anti-hyperglycemic agents market is highly consolidated, with leadership concentrated among Novo Nordisk A/S, Eli Lilly and Company, Sanofi, and AstraZeneca PLC. These firms dominate through extensive portfolios of branded therapies, large-scale cardiovascular outcome trial execution, and global distribution networks that reinforce their influence on clinical guidelines and prescribing patterns.