- Inks, Coatings, Adhesives & Sealants (ICAS)

- Anti-Graffiti Coatings Market

Anti-Graffiti Coatings Market Size, Share, and Growth Forecast 2025 - 2032

Anti-Graffiti Coatings Market Analysis By Product Type (Sacrificial Coatings, Non-Sacrificial Coatings, Semi-Permanent Coatings), Technology (Water-Based Coatings, Solvent-Based Coatings, Powder Coatings, Nano Coatings, Fluoropolymer Coatings, Silicone-Based Coatings), By Industry, and Regional Analysis 2025 - 2032

Anti-Graffiti Coatings Market Share and Trends Analysis

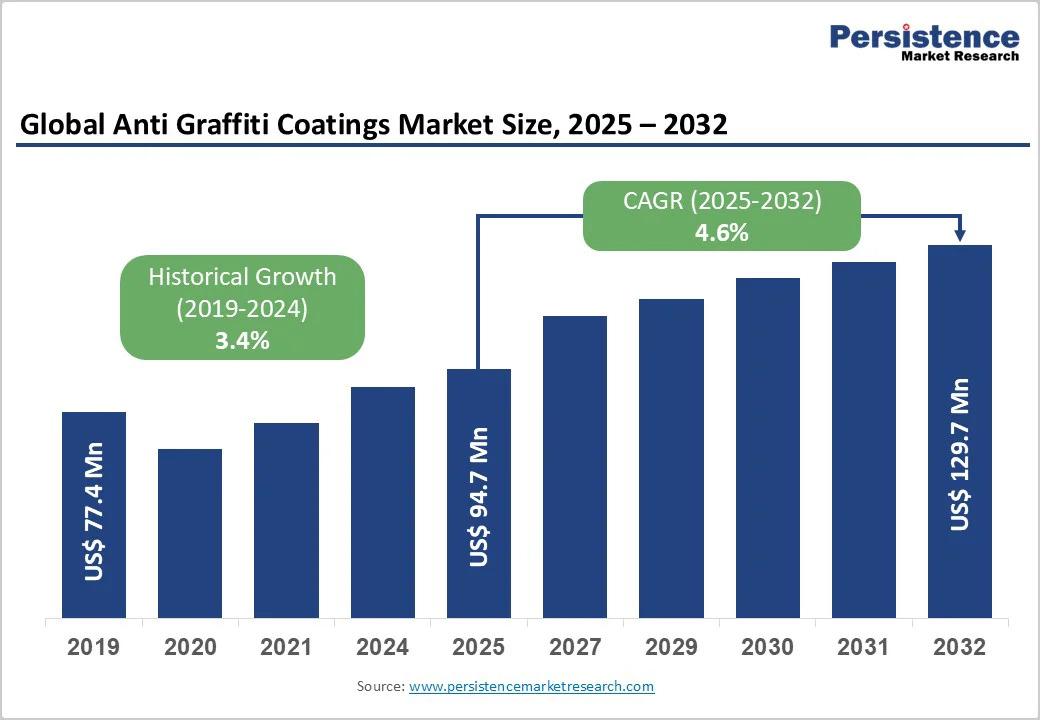

The global anti-graffiti coatings market size was valued at US$94.7 million in 2025 and is projected to reach US$129.7 million by 2032, growing at a CAGR of 4.6% between 2025 and 2032.

Rapid urbanization, massive public and private infrastructure projects, and stringent regulatory mandates drive the need for anti-graffiti coatings. Concurrently, sustainability imperatives and VOC regulations are accelerating the shift toward water-based and powder formulations, further propelling market expansion.

Key Industry Highlights:

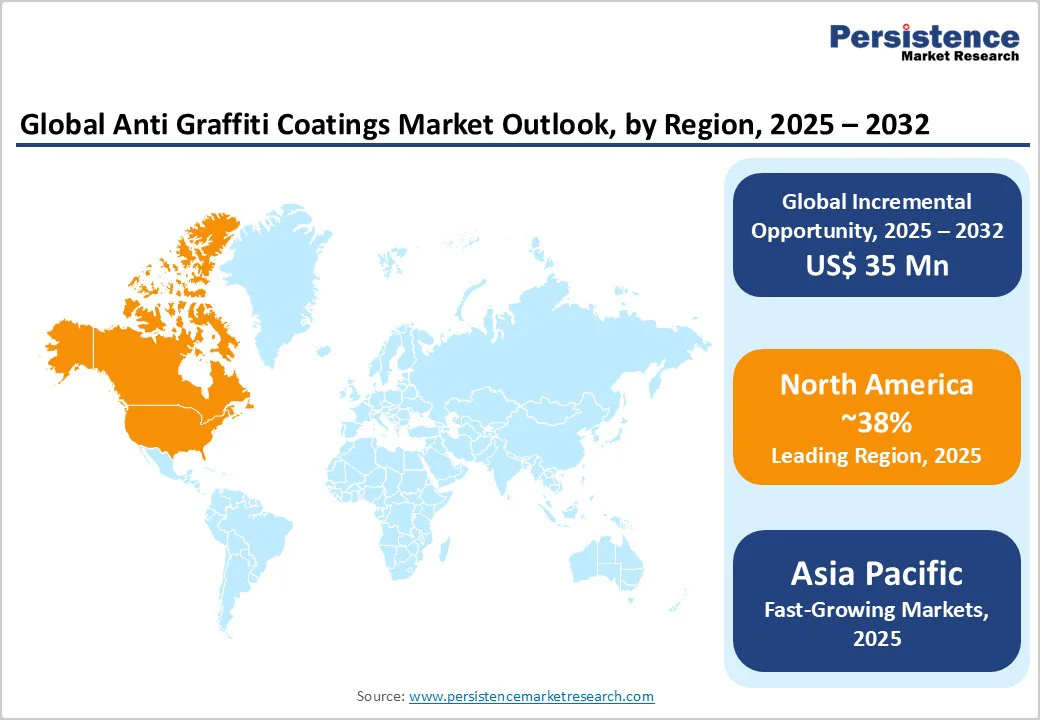

- Leading Region: North America dominates in adoption and regulatory enforcement, with the U.S. leading technological innovation and public spending.

- Fastest Growing Region: Asia Pacific is projected to be the fastest-growing region, driven by large-scale urbanization and infrastructure investments.

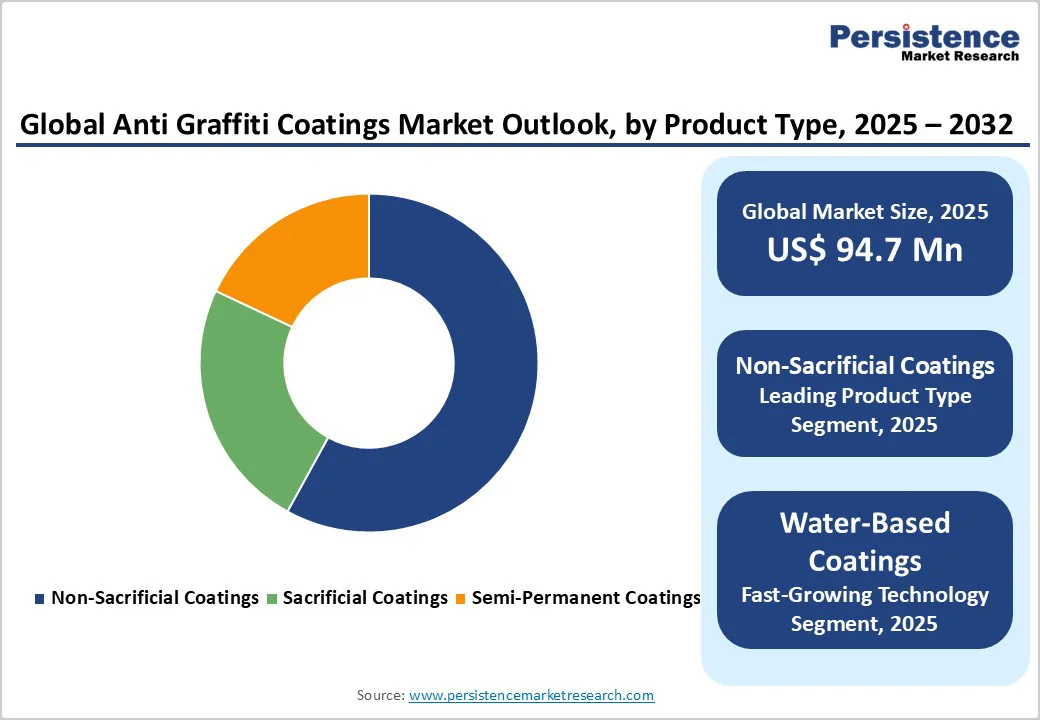

- Dominant Segment: Non-sacrificial (permanent) coatings are the most widely used product type, offering superior durability and cleanability.

- Fastest Growing Segment: Water-based anti-graffiti coatings represent the fastest-growing technology, favored for low VOC emissions and sustainability.

- Key Market Opportunity: A Significant market opportunity exists in developing high-performance, eco-friendly coatings for transportation and public infrastructure projects.

| Key Insights | Details |

|---|---|

| Global Anti-Graffiti Coatings Market Size (2025E) | US$94.7 million |

| Market Value Forecast (2032F) | US$129.7 million |

| Projected Growth CAGR (2025 - 2032) | 4.6% |

| Historical Market Growth (2019 - 2024) | 3.4% |

Market Dynamics

Driver - Rising Urbanization and Infrastructure Expansion

The rapid pace of urbanization worldwide has amplified demand for protective surface solutions. Cities across North America, Europe, and the Asia Pacific are investing heavily in infrastructure upgrades, ranging from mass transit stations to public art installations, to foster urban renewal and civic pride.

With graffiti-related vandalism complaints rising by over 50% in major U.S. metros, municipalities are shifting budget allocations from reactive cleaning to preventive measures. As a result, the adoption of anti-graffiti coatings as a cost-efficient, long-term protective strategy has surged, solidifying its role as an essential material in urban construction projects.

Technological Innovation and Eco-Friendly Formulations Innovations in nanotechnology and environmentally benign chemistries have revolutionized the performance and acceptance of anti-graffiti coatings. Next-generation formulations incorporating nanosilica, nanotitanium dioxide, and fluoropolymer additives offer self-cleaning, UV resistance, and superhydrophobic properties, significantly enhancing durability and ease of graffiti removal.

Regulatory frameworks targeting reductions in volatile organic compound (VOC) emissions have also steered the industry toward water-based and powder coatings, which now account for nearly half of all new product launches. These eco-friendly alternatives not only comply with stringent EU and U.S. environmental standards but also cater to growing end-user preferences for sustainable construction materials.

Restraints - High Upfront Costs

Advanced anti-graffiti coatings, particularly permanent and nano-enhanced variants, typically have higher initial prices than traditional solvent-based systems.

Although the total cost of ownership often proves lower over a product’s lifecycle due to reduced maintenance and cleaning expenses, the upfront investment can deter smaller municipalities and budget-conscious property owners. This cost-sensitive market segment may continue favoring sacrificial coatings or routine cleaning services in the short term.

Regulatory and Environmental Challenges

While eco-friendly formulations are on the rise, legacy solvent-based coatings containing hazardous components still require reformulation to meet evolving health and safety regulations.

Manufacturers face stringent compliance requirements in regions like North America and Europe, where regulations on chemical emissions and worker safety are particularly rigorous. Reformulation costs and certification delays can impede new product rollouts, slowing market penetration in regulated territories.

Market Opportunity - Surge in Water-Based Coatings Adoption

The transition toward Water-based Anti-Graffiti Coatings represents a key growth opportunity. Water-based systems deliver comparable performance to solvent-based counterparts while drastically reducing VOC emissions.

Governments and urban planners in sustainable cities, such as those under the C40 Climate Leadership Group, are specifying water-based anti-graffiti solutions in public contracts. This shift is expected to accelerate market growth for waterborne formulations by over 6% annually through 2032, particularly in Europe and North America, where green building standards prevail.

Transportation and Public Infrastructure

Modernization: Investments in transportation infrastructure are unlocking new avenues for permanent anti-graffiti coatings that offer repeatable cleanability and resistance to harsh environmental conditions.

Major metro expansions in China, India, and the Middle East, coupled with retrofit projects in Europe and North America, are fueling demand for coatings that withstand abrasive cleaning and heavy foot traffic. Public-private partnerships in transit authorities are increasingly incorporating anti-graffiti measures into project specifications, creating sustained opportunities for manufacturers to showcase high-performance, low-maintenance solutions.

Category-wise Analysis

Product Type Insights

Non-Sacrificial Coatings Dominate Permanent, or non-sacrificial, coatings hold a commanding market share of approximately 59% due to their long-term durability and ability to withstand multiple cleaning cycles without recoating. These formulations are especially valued in high-traffic public areas, transportation hubs, and commercial façades, where maintenance downtime must be minimized.

In contrast, sacrificial coatings-while less costly upfront-require complete removal and reapplication after each graffiti incident, restricting their appeal to heritage sites and low-exposure structures. Semi-permanent coatings bridge the gap by offering moderate longevity with easier recoat procedures, but they occupy a smaller mid-tier segment.

Technology Insights

Water-Based Coatings Lead Water-based anti-graffiti coatings represent about 48% of global market revenues. This segment’s popularity stems from strict environmental regulations, improved formulation performance, and growing contractor preference for low-VOC materials.

Solvent-based coatings maintain a 27% share, favored in scenarios where fast curing and extreme weather resistance are paramount. Emerging technologies such as powder, nano, fluoropolymer, and silicone-based coatings account for the remaining share and continue to capture niche applications that require specialized protective attributes, such as marine exposure or chemical resistance.

Industry Insights

The Building & Construction end-use vertical accounts for roughly 54% of the market in 2025. Public buildings, commercial complexes, and residential developments routinely incorporate anti-graffiti measures into design specifications to safeguard aesthetics and reduce maintenance budgets. The Transportation segment follows closely, with railways, bus terminals, and airports investing in advanced coatings to streamline cleaning operations and uphold brand image.

Automotive applications-primarily for fleet vehicles and utility vans-are growing as fleet operators seek to protect assets from vandalism. Marine vessels and port infrastructure utilize specialized formulations to resist saltwater corrosion and graffiti, representing a smaller yet steadily expanding niche.

Regional Insights

North America Anti-Graffiti Coatings Market Trends

North America leads the Global Anti-Graffiti Coatings Market, driven by proactive municipal budgets and strict environmental regulations. In cities such as New York and Los Angeles, over 10% of maintenance budgets is allocated to graffiti prevention and removal, underscoring the importance of anti-graffiti coatings.

Manufacturers such as The Sherwin-Williams Company, 3M, and Axalta Coating Systems offer innovative nano-enhanced and self-cleaning products designed for durability in harsh conditions.

Additionally, Canada's Green Building Council and infrastructure projects in Mexico are boosting demand for eco-friendly solutions in sustainable development. As municipalities and private developers seek long-term cost savings and improved aesthetics, the North American market is expected to continue moderate growth, supported by ongoing R&D and public-private partnerships.

Europe Anti-Graffiti Coatings Market Trends

Europe’s anti-graffiti coatings market benefits from harmonized environmental regulations and strong public investment in urban beautification. The European Chemicals Agency (ECHA) enforces strict VOC limits, leading to increased use of water-based and nano coatings that prioritize sustainability. Germany spearheads these efforts by integrating anti-graffiti measures into renovation projects, while the UK mandates low-emission coatings through its Green Procurement Policy.

France and Spain have launched funding programs to refurbish public art and transit shelters, often opting for permanent coatings. Key market players such as AkzoNobel N.V., BASF SE, and Edge Film Technologies offer eco-friendly certifications to meet these standards.

Urban revitalization funds in cities such as Berlin, London, and Paris are also dedicated to anti-graffiti solutions, enhancing aesthetics and protecting assets. This regulatory landscape fosters steady market growth with a focus on eco-compliant technologies and public-private partnerships.

Asia Pacific Anti-Graffiti Coatings Market Trends

Asia Pacific is rapidly becoming the fastest-growing region in the Anti-Graffiti Coatings Market, driven by urbanization and infrastructure investments. China’s “Smart City” initiatives utilize anti-graffiti coatings in metro and housing projects. India’s metro networks in cities such as Delhi and Mumbai require durable coatings to maintain the appearance of stations and bridges. Japan employs advanced nano-coating technologies for heritage site restorations.

Southeast Asian countries such as Singapore and Malaysia are adopting eco-friendly products in green building standards. Collaborations between local specialists and global firms, such as 3M and Sherwin-Williams, foster technology transfers and localized manufacturing. Evolving regulations and government focus on urban renewal are boosting demand for anti-graffiti solutions, solidifying Asia Pacific's role as a key growth driver.

Competitive Landscape

The anti-graffiti coatings market is moderately consolidated, with top players accounting for significant market share. The Sherwin-Williams Company, 3M, BASF SE, AkzoNobel N.V., and Axalta Coating Systems lead through extensive product portfolios, global distribution networks, and sustained R&D investments.

These firms emphasize low-VOC and nano-enhanced solutions to differentiate offerings. Mid-tier companies and regional specialists such as Edge Film Technologies, ChemMasters, and SIKA CORPORATION focus on niche applications and service-based models, providing localized support and tailored formulations.

Key Market Developments:

- March 2025: The Sherwin-Williams Company launched a next-generation low-VOC nano-coating targeting public transit infrastructure, featuring enhanced hydrophobicity and UV resistance.

- February 2025: 3M expanded its Graffiti Shield™ portfolio across major European cities, introducing a 10-year warranty service model.

- December 2024: BASF SE partnered with transit authorities in the Asia-Pacific region to pilot a sustainable anti-graffiti solution capable of withstanding saltwater exposure in coastal metro systems.

Companies Covered in Anti-Graffiti Coatings Market

- The Sherwin-Williams Company

- 3M

- BASF SE

- AkzoNobel N.V.

- Axalta Coating Systems, LLC

- Edge Film Technologies

- ChemMasters, Inc.

- SIKA CORPORATION

- A&A Thermal Spray Coatings

- FSC Coatings Inc.

- RPM International Inc.

- Avery Dennison Corporation

- Evonik Industries AG

- Dulux Group

- Teknos Group

- Wacker Chemie AG

- NanoTech Coatings

- Rainguard

- Hydron Protective Coating (Merck Group)

- Performance Solutions NZ Limited

Frequently Asked Questions

The global Anti-Graffiti Coatings Market is estimated at US$ 94.7 million in 2025 and is forecast to reach US$ 129.7 million by 2032.

Rapid urbanization, expanding infrastructure projects, and regulatory mandates for VOC reduction are the primary drivers.

Non-Sacrificial (Permanent) Coatings dominate, holding around 59% market share due to their durability and ease of cleaning.

North America leads globally, supported by high municipal spending and stringent environmental regulations.

The greatest opportunity lies in the expansion of water-based and nano-enhanced coatings for sustainable public infrastructure applications.

Key market players include The Sherwin-Williams Company, 3M, and BASF SE, known for their innovation, extensive portfolios, and strong distribution networks.