- Animal Health

- Animal Genetics Market

Animal Genetics Market Size, Share, and Growth Forecast 2026 - 2033

Animal Genetics Market by Product (Live Animals, Genetic Materials, Semen, Embryos, Others), Animal Type (Poultry, Porcine, Bovine/Cattle, Canine, Others), Application (Reproduction, Genetic Disease Screening, Trait Improvement, Breed Identification, Others), Technology (Artificial Insemination, Embryo Transfer, In Vitro Fertilization, DNA Sequencing, Others), End-user (Veterinary Hospitals, Veterinary Clinics, Animal Breeding Companies, Research Institutes & Universities, Others), and Regional Analysis, 2026 - 2033

Animal Genetics Market Size and Trend Analysis

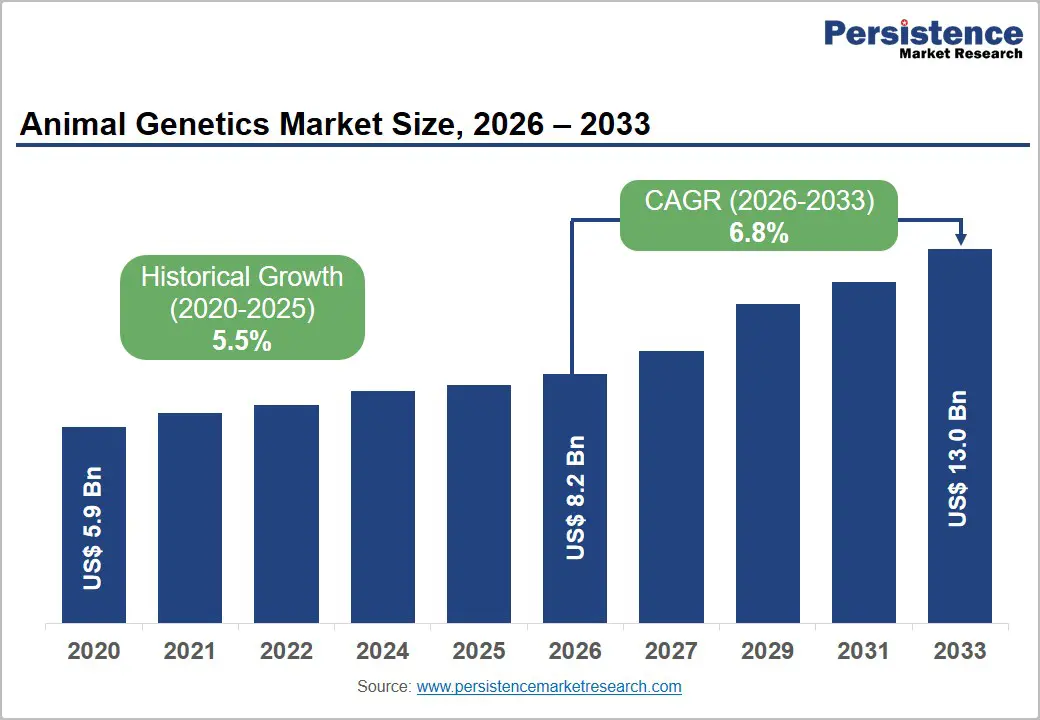

The global animal genetics market size is expected to be valued at US$ 8.2 billion in 2026 and projected to reach US$ 13.0 billion by 2033, growing at a CAGR of 6.8% between 2026 and 2033.

Robust market growth is primarily driven by intensifying global demand for food security, accelerating adoption of genomic selection technologies, and the rising commercial importance of precision livestock breeding. According to the Food and Agriculture Organization of the United Nations (FAO), the global livestock sector contributes approximately 40% of total agricultural GDP and supports the livelihoods of over 1.3 billion people worldwide.

The convergence of next-generation DNA sequencing, advanced reproductive technologies such as embryo transfer and in vitro fertilization, and large-scale genomic databases is enabling breeders to achieve unprecedented genetic gain per generation, substantially compressing selection intervals and driving sustained investment in animal genetics products and services across all major livestock species.

Key Industry Highlights:

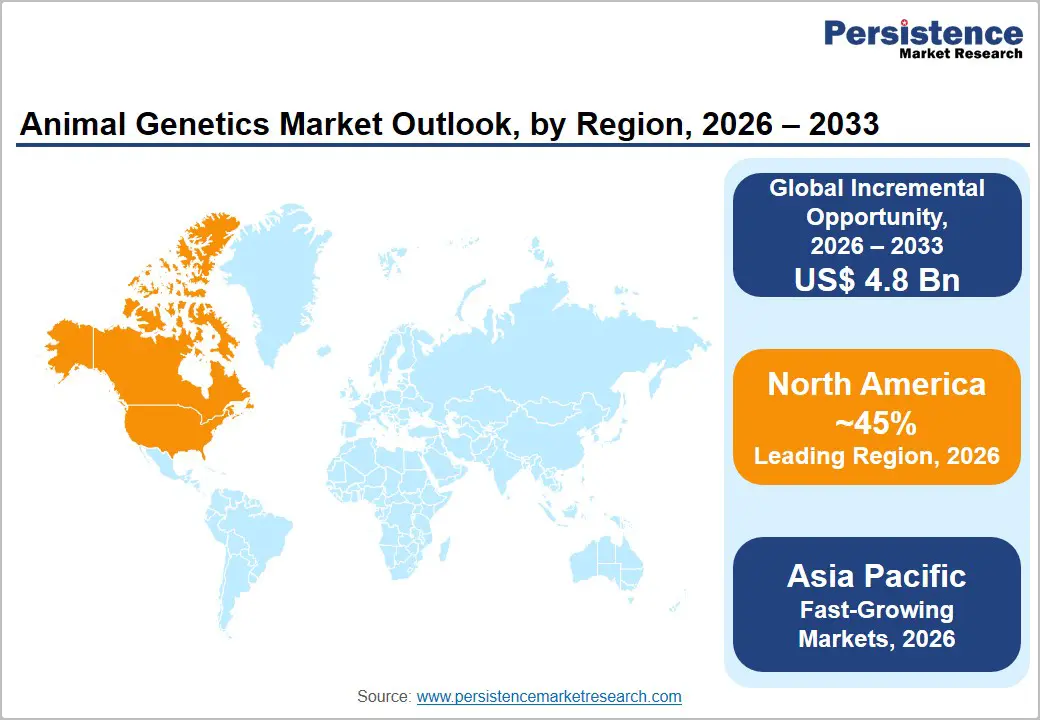

- Leading Region: North America holds approximately 45% of the global animal genetics market share in 2025, driven by world-class genomic reference databases managed by CDCB, leading companies including URUS Group LP and STgenetics®, and strong USDA-regulated genetic material export programs.

- Fast-Growing Market: Asia Pacific is the highest-growth region, driven by China's Seed Industry Revitalization initiative, India's NPBBDD cattle improvement program, Japan's advanced equine genetics, and ASEAN nations expanding commercial poultry and swine breeding operations with global genetics partners.

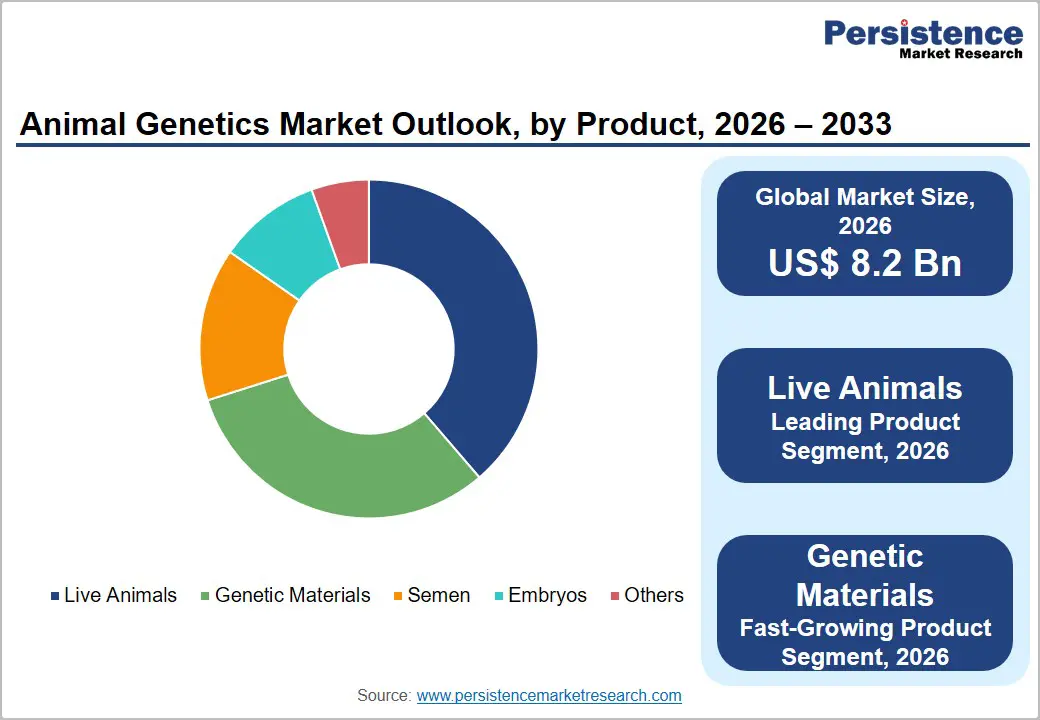

- Live Animals Dominate the Product Segment: Live Animals account for ~39% of the animal genetics product market in 2025, reflecting sustained commercial demand for genomically tested elite breeding stock in bovine and swine sectors, generating substantial price premiums over commodity animals globally.

- Fast-Growing Product: Genetic materials including sexed semen, embryos, and genomic testing kits, are the fast-growing product category, driven by STgenetics® SexedULTRA™ adoption, OPU-IVF expansion, and growing genomic testing demand in poultry and aquaculture species.

- Opportunities: Expanding genomic selection into poultry and aquaculture, where companies such as Hendrix Genetics and Groupe Grimaud are building reference populations, offers a large underpenetrated opportunity, given global poultry production exceeding 140 million tonnes annually.

Market Dynamics

Drivers - Genomic Selection and Next-Generation Sequencing Accelerating Genetic Gain

The widespread adoption of genomic selection underpinned by high-density SNP genotyping arrays and next-generation sequencing (NGS) platforms is the most transformative force in the animal genetics market. Genomic breeding values (GEBVs) now enable breeders to accurately predict the genetic merit of young animals before they reach reproductive age, reducing generation intervals from 5-7 years to as few as 2 years in dairy cattle, as documented in studies published in the Journal of Dairy Science.

The Council on Dairy Cattle Breeding (CDCB) in the United States manages a reference population exceeding 85 million genotyped animals, providing an unparalleled data foundation for genomic predictions. This accelerated genetic progress directly translates into improved milk yields, feed conversion efficiency, and disease resistance, compelling economic benefits that are expanding genomic testing adoption across bovine, porcine, and poultry breeding programs globally.

Rising Global Protein Demand and Livestock Productivity Optimization

Escalating global protein demand driven by population growth and rising per-capita meat and dairy consumption in developing economies is creating structural demand for superior genetics that maximize livestock productivity. The FAO's Food Outlook 2024 projects global meat production to reach 366 million tonnes by 2032, with poultry and pork accounting for the largest growth increments. Genetic improvement of commercial livestock herds and flocks is among the most cost-effective levers for productivity gains: a single elite bull's semen can produce tens of thousands of offspring, amplifying the return on genetic investment.

Leading genetics companies such as Genus plc and Hendrix Genetics BV have demonstrated that genomically superior animals yield measurably higher output per unit of feed, water, and land, aligning genetics investment with sustainability objectives increasingly mandated by institutional food buyers.

Restraints - High Cost of Genomic Technologies and Infrastructure Gaps in Developing Regions

Despite its transformative potential, genomic selection remains inaccessible to smallholder farmers and cooperatives in low-income countries due to the prohibitive cost of high-density genotyping arrays, NGS equipment, and bioinformatics infrastructure. SNP chip genotyping can cost between US$ 20 and US$ 100 per animal, and building the reference population databases necessary for accurate genomic prediction requires substantial multi-year institutional investment.

The FAO estimates that over 60% of the world's livestock are held by smallholder farmers who lack access to modern genetic improvement tools, constraining the addressable market for genomic services in high-potential regions across Sub-Saharan Africa, South Asia, and parts of Latin America.

Biosecurity Risks and Stringent Regulatory Barriers for Genetic Material Trade

International trade of live animals, semen, and embryos is subject to rigorous sanitary and phytosanitary (SPS) requirements governed by the World Organisation for Animal Health (WOAH/OIE) Terrestrial Animal Health Code. Disease outbreaks such as Foot-and-Mouth Disease (FMD) and African Swine Fever (ASF) can trigger immediate export suspensions, disrupting global genetics supply chains.

The 2023-2024 ASF outbreaks across Southeast Asia caused significant disruptions in porcine genetic material trade, directly impacting revenue for genetics companies reliant on export markets and demonstrating the vulnerability of global supply chains to disease-driven regulatory barriers.

Opportunities - Genomic Testing Expansion in Poultry and Aquaculture Fastest-Growing Species Segments

While bovine genetics has historically dominated the animal genetics industry, rapid expansion of genomic selection into poultry and aquaculture species represents a high-growth, largely underpenetrated opportunity. The International Poultry Council (IPC) reports global poultry meat production exceeding 140 million tonnes annually, with genetic improvement of broiler feed conversion ratio (FCR) and layer egg production intensity representing billions in potential productivity gains.

Companies such as Hendrix Genetics BV and Groupe Grimaud are actively expanding genomic reference populations for turkey, duck, and aquaculture species. The Norwegian Ministry of Trade, Industry and Fisheries reports that genomic selection in Atlantic salmon breeding programs has achieved annual genetic gains of approximately 15-20% for growth rate, signaling transformative potential for genetics companies that extend platforms beyond traditional livestock into aquaculture.

Precision Livestock Farming and Integration of AI with Reproductive Technologies

The convergence of artificial intelligence (AI), machine learning, and advanced reproductive technologies including sexed semen, OPU-IVF (ovum pick-up in vitro fertilization), and embryo cryopreservation is creating a new generation of high-value genetics services. For instance, STgenetics® has commercialized SexedULTRA™ sexed semen technology, achieving greater than 90% accuracy in offspring sex pre-selection, enabling dairy producers to generate primarily heifer calves from elite cows while using beef semen on lower-merit animals a strategy that significantly enhances return on genetics investment.

AI-driven fertility prediction tools integrated with farm management platforms are improving conception rates and embryo transfer success. The International Embryo Technology Society (IETS) reported over 1.4 million bovine embryo transfers globally in 2022, with IVF-derived embryos growing at double-digit annual rates reflecting the commercial momentum of premium reproductive technologies.

Category-wise Analysis

Product Insights

Live animals constitute the leading product segment in the animal genetics market, commanding approximately 39% of total market revenue in 2026. This dominance reflects the enduring commercial importance of direct trade in purebred and elite breeding stock, including dairy bulls, beef sires, boars, and breeding poultry stock across domestic and international markets. Live animal genetics embody a complete, immediately deployable genetic package encompassing superior performance traits, disease resistance, and adaptability, which remains highly valued by commercial breeders who require proven herd-building stock.

The USDA Foreign Agricultural Service reports that the U.S. alone exports breeding cattle and swine worth hundreds of millions of dollars annually. Furthermore, live animal premiums for elite genomically tested bulls from companies such as URUS Group LP and CRV Holding B.V. command substantial price premiums over commodity animals, underpinning strong segment revenue.

Animal Type Insights

Bovine/cattle is the dominant animal type segment, accounting for approximately 44% of the animal type market in 2026. The cattle segment benefits from the longest and most scientifically advanced history of systematic genetic improvement, a massive global population estimated by the FAO at over 1 billion cattle worldwide, and the universal commercial importance of dairy and beef production.

Artificial insemination (AI) with sexed and conventional semen from genomically elite bulls is practiced at scale across North America, Europe, and increasingly in developing regions. The density of the global bovine genomic reference database, particularly for Holstein dairy cattle managed by organizations such as Interbull under the International Committee for Animal Recording (ICAR) provides unmatched prediction accuracy, sustaining bovine genetics' leadership position through the forecast period.

Application Insights

Reproduction is the leading application segment in the animal genetics market, representing approximately 45% of application-based revenue in 2026. This dominance reflects the fundamental commercial role of reproductive technologies including artificial insemination, embryo transfer, and IVF in disseminating elite genetics across large livestock populations at scale. AI with superior semen remains the highest-volume entry point for genetic improvement in cattle and swine worldwide. According to Interbull and the National Association of Animal Breeders (NAAB), over 7 million AI services are performed annually in U.S. dairy cattle alone. The reproducibility, scalability, and relatively low cost of AI compared to natural service or embryo transfer ensure reproduction remains the cornerstone application driving market revenue globally.

End-user Insights

Animal breeding companies represent the leading end-user segment, capturing approximately 40% of total market revenue in 2026. These vertically integrated organizations encompassing pure line breeders, multipliers, and distribution networks are the primary commercial buyers of elite genetics, genomic testing services, and reproductive technologies.

Companies such as Genus plc (through its PIC® swine and ABS® bovine genetics businesses), Topigs Norsvin, and Select Sires, Inc. deploy genetics at commercial scale, purchasing large volumes of AI doses, embryos, and genomic testing services annually. Their sophisticated understanding of genomic breeding values and production economics, combined with direct farmer relationships, positions them as the highest-value, highest-volume channel in the animal genetics value chain.

Regional Insights

North America Animal Genetics Market Trends and Insights

North America accounted for nearly 45% of the global animal genetics market in 2026, supported by advanced genomic selection infrastructure, high livestock productivity standards, and strong commercialization of bovine and swine breeding technologies. The region benefits from widespread adoption of artificial insemination, sexed semen, and embryo transfer technologies.

Regulatory oversight from agencies such as USDA-APHIS supports international trade of premium genetic materials. Continuous investment in genomic databases, precision breeding, and dairy productivity enhancement further strengthens regional leadership across cattle, poultry, and porcine genetics applications.

U.S. Animal Genetics Market Trends and Insights

The United States represented approximately 81.6% of the North American market in 2026. The country leads global cattle and swine genetics innovation through organizations such as USDA-ARS and CDCB, which maintain extensive genomic evaluation systems. Major companies including STgenetics®, Select Sires, and URUS Group drive exports of elite bovine semen and embryos. Increasing adoption of IVF-based breeding and genomic selection technologies continues to strengthen the U.S. commercial livestock sector.

Canada Animal Genetics Market Trends and Insights

Canada contributed close to 12.9% of the regional revenue share in 2026, led by strong dairy genetics programs in Ontario and Quebec. Canadian producers increasingly utilize genomic testing and artificial insemination to improve milk yield and herd productivity. Government-supported livestock breeding initiatives and rising exports of dairy cattle genetics to Asia and Latin America are supporting steady market expansion. The country is also witnessing growing adoption of embryo transfer technologies in premium cattle breeding operations.

Europe Animal Genetics Market Trends and Insights

Europe held around a 27.4% share of the global animal genetics market in 2026, driven by established dairy genetics programs, harmonized livestock regulations, and advanced breeding cooperatives. The region benefits from strong government support under the Common Agricultural Policy (CAP), promoting sustainable livestock productivity and genetic improvement. Europe maintains a premium position in cattle, poultry, and pig genetics exports through strict breed registration and performance recording standards. Increasing focus on disease-resistant breeds and precision livestock farming continues to support technological advancements across the regional market.

Germany Animal Genetics Market Trends and Insights

Germany accounted for nearly 23.7% of the European market in 2026, supported by its advanced dairy cattle breeding ecosystem. Organizations such as VIT maintain one of Europe’s largest livestock performance databases, improving genomic prediction accuracy for Holstein cattle. Rising investments in automated dairy farming and genetic disease screening technologies are accelerating demand for elite bovine genetics. Germany also remains a major exporter of high-performance dairy cattle and semen products across Europe and Asia.

France Animal Genetics Market Trends and Insights

France represents approximately 19.8% of the regional share in 2026. The country is recognized for its diversified animal genetics capabilities spanning poultry, rabbit, cattle, and swine breeding. Companies such as Groupe Grimaud and national livestock institutes continue to expand international genetic distribution networks. Increasing emphasis on sustainable livestock production and high-value breeding programs is driving adoption of advanced genomic evaluation technologies across commercial and cooperative farming operations.

Asia Pacific Animal Genetics Market Trends and Insights

Asia Pacific captured nearly 19.6% of the global animal genetics market in 2026 and is projected to register the fastest CAGR of about 9.8% in the coming years. Rapid growth in protein consumption, commercial livestock production, and government-backed herd improvement programs are major growth drivers. Countries across the region are increasingly investing in genomic selection, disease-resistant breeding, and advanced reproductive technologies to improve domestic livestock productivity. Expanding poultry and swine industries, coupled with rising dairy modernization initiatives, continue to position Asia Pacific as the key long-term growth engine for the global market.

China Animal Genetics Market Trends and Insights

China accounted for nearly 38.5% of the Asia Pacific market in 2026, supported by aggressive modernization of the domestic swine and dairy industries. Under the “Seed Industry Revitalization” initiative, the country is investing heavily in genomic databases and elite breeding programs to reduce reliance on imported genetics. Increasing industrial-scale pig farming and rising demand for disease-resistant livestock are accelerating adoption of genomic selection and artificial insemination technologies.

India Animal Genetics Market Trends and Insights

India represented around 18.7% of the regional market share in 2026, driven by its large bovine population and expanding dairy sector. Government initiatives such as the National Programme for Bovine Breeding and Dairy Development (NPBBDD) are supporting genetic improvement of indigenous and crossbred cattle. Increasing awareness regarding productivity enhancement, rising milk demand, and broader access to artificial insemination services are contributing to market growth across organized dairy farming operations.

Competitive Landscape

The global animal genetics market is moderately consolidated, with a small number of multinational genetics corporations including Genus plc, Hendrix Genetics BV, URUS Group LP, CRV Holding B.V., and Topigs Norsvin commanding significant global market share across bovine, porcine, and poultry species. Key competitive differentiators include the scale and accuracy of proprietary genomic reference databases, the breadth of species and trait coverage, global semen and embryo distribution infrastructure, and the quality of field technical support.

The market is simultaneously fragmented at the regional and specialty level, with cooperative structures (Select Sires, VikingGenetics, Semex Alliance) competing alongside investor-backed commercial entities. Strategic acquisitions, cross-species genomic platform expansion, and AI-integrated breeding decision tools are the dominant competitive strategies driving differentiation.

Key Developments:

- In May 2026, URUS Group LP, a leading provider of bovine genetics, reproductive technologies, and herd management solutions, announced a definitive agreement to acquire AgriWebb Pty. Ltd., a livestock management and supply chain data platform specializing in beef production operations.

- In February 2026, Leads Genetics, a subsidiary of BL Agro Group, inaugurated an advanced Integrated R&D Centre for Indigenous Cattle Genetics and Genomics at BL Kamdhenu Farms and the company’s headquarters in Bareilly, aiming to strengthen research and innovation in native cattle breeding technologies.

- In February 2026, Zoetis Inc. announced a definitive agreement to acquire the animal genomics business of Neogen Corporation for US$160 million. The acquisition strengthens Zoetis’ precision animal health portfolio by enhancing its genomic technologies, predictive analytics capabilities, and livestock innovation solutions across both livestock and companion animal segments.

- In September 2025, Leads Agri Genetics, a wholly owned subsidiary of Leads Connect, launched India’s first privately owned Integrated Centre of Excellence for cattle and plant genomics in Greater Noida. The initiative marked a significant advancement in agricultural biotechnology and livestock genomics, while the company also became the first private Indian firm to import Gir breed embryos from Brazil under a breed improvement program.

Companies Covered in Animal Genetics Market

- Genus plc

- Hendrix Genetics BV

- URUS Group LP

- CRV Holding B.V.

- Semex Alliance

- Swine Genetics International

- STgenetics®

- Animal Genetics, Inc.

- Zoetis Services LLC

- Topigs Norsvin

- Select Sires, Inc.

- VikingGenetics Fmba

- Groupe Grimaud

- generatio GmbH

- Genetics Australia Co-operative

- Others

Frequently Asked Questions

The global animal genetics market is estimated to reach US$ 8.2 billion in 2026, expanding to US$ 13.0 billion at a CAGR of 6.8%. Growth is driven by rising global protein demand, rapid adoption of genomic selection technologies, and expanding use of advanced reproductive biotechnologies across bovine, porcine, and poultry species.

Rising demand for high-quality animal protein, increasing adoption of genomic selection technologies, and growing focus on livestock productivity and disease resistance are the major demand drivers for the global animal genetics market.

North America leads with approximately 45% of global market share in 2026. The United States drives this leadership through world-class genomic infrastructure managed by CDCB and USDA ARS, elite genetics companies including URUS Group LP and STgenetics®, and a robust APHIS-regulated genetic material export framework serving markets across Latin America, Asia, and the Middle East.

Expansion of precision breeding and advanced reproductive technologies such as IVF, embryo transfer, and genomic testing in emerging livestock economies presents the most significant growth opportunity in the global animal genetics market.

The leading companies include Genus plc, Hendrix Genetics BV, URUS Group LP, CRV Holding B.V., Topigs Norsvin, STgenetics®, Select Sires Inc., VikingGenetics Fmba, Semex Alliance, Zoetis Services LLC, Groupe Grimaud, Animal Genetics Inc., generatio GmbH, and Genetics Australia Co-operative, among others, driving global genomic and reproductive technology adoption across livestock species.