- Medical Devices

- Angiography Catheters Market

Angiography Catheters Market Size, Share, and Growth Forecast, 2026 - 2033

Angiography Catheters Market by Product Type (Coronary Angiography Catheters, Others), Application (Coronary Artery Disease, Others), End-user (Hospitals, Ambulatory Surgical Centers, Others), and Regional Analysis for 2026 - 2033

Angiography Catheters Market Share and Trends Analysis

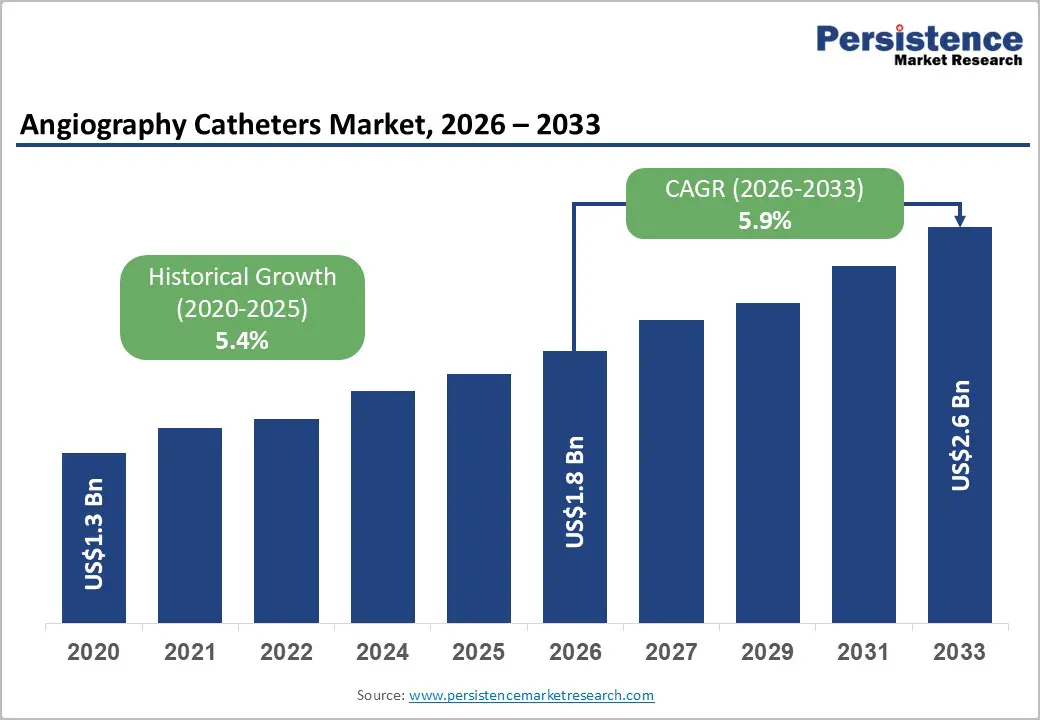

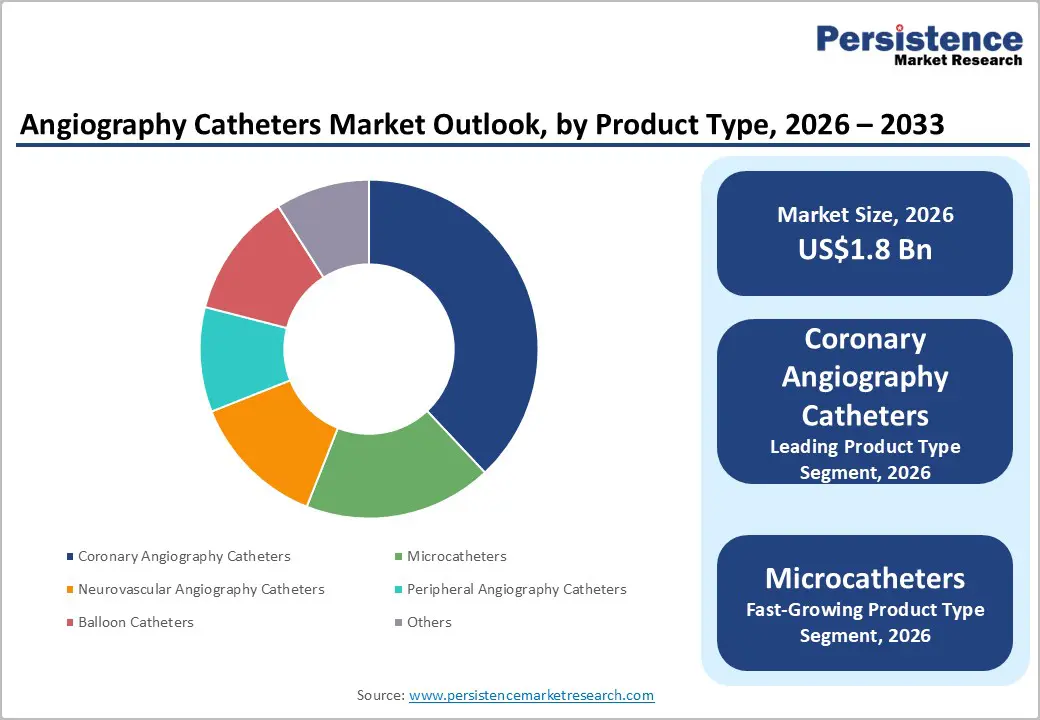

The global angiography catheters market size is likely to be valued at US$1.8 billion in 2026 and is expected to reach US$2.6 billion by 2033, growing at a CAGR of 5.9% during the forecast period from 2026 to 2033, driven by rising cardiovascular disease prevalence, increasing interventional procedure volumes, and expanding adoption of minimally invasive diagnostics.

Growing aging population levels are increasing demand for coronary and neurovascular imaging procedures across hospital networks and specialized cardiac centers. Regulatory approvals for advanced catheter materials and hydrophilic coating technologies are strengthening procedural efficiency and reducing complication rates.

Key Industry Highlights:

- Leading Product Type: Coronary angiography catheters are set to hold around 38% revenue share in 2026, driven by dominant procedural volumes in coronary artery disease diagnosis across global catheterization laboratories.

- Fastest-Growing Product Type: Microcatheters are projected to be the fastest-growing segment, supported by accelerating adoption in complex neurovascular and peripheral interventional procedures requiring distal vascular access capabilities.

- Leading Application: Coronary artery disease procedures are estimated to hold roughly 42% revenue share in 2026, due to the global cardiovascular disease epidemic and universal clinical adoption of invasive angiography as the definitive pre-intervention diagnostic modality.

- Fastest-growing Application: Neurological disorders are forecast to record the fastest application segment growth, driven by expanding comprehensive stroke center infrastructure and the proven clinical superiority of catheter-based neurovascular intervention over pharmacological alternatives.

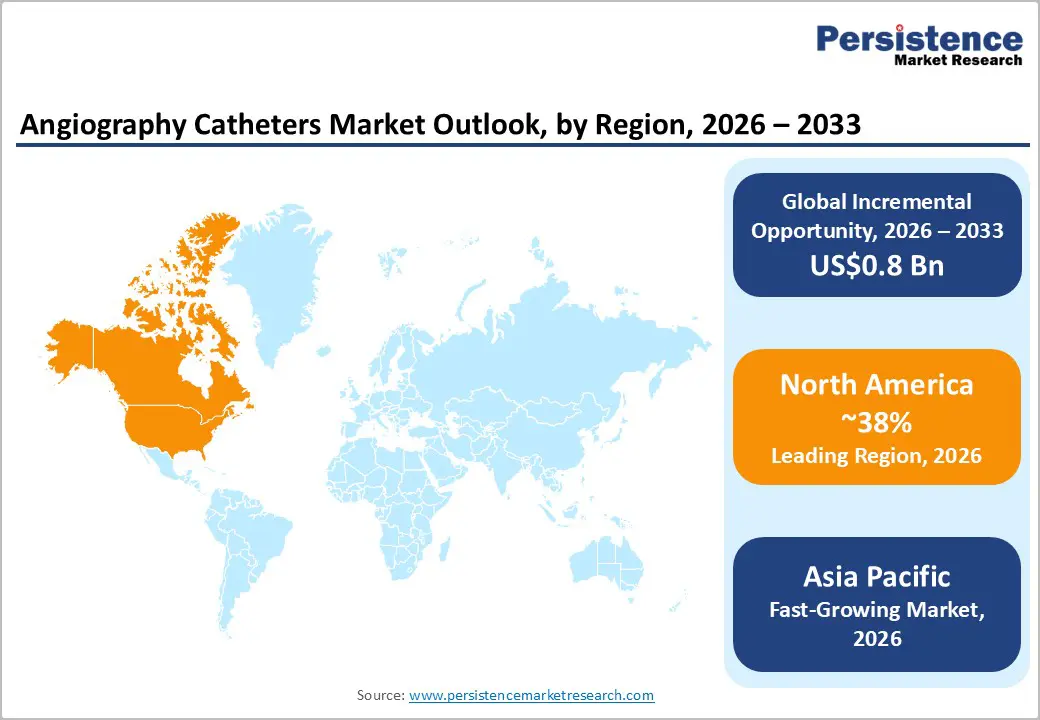

- Regional Leadership: North America is projected to capture approximately 38% of the angiography catheters market share in 2026, while Asia Pacific is forecast to record the fastest growth due to expanding healthcare facility construction.

- Competitive Environment: The market reflects a moderately consolidated structure, with key players including Medtronic, Abbott Laboratories, and Boston Scientific leveraging integrated product portfolios, regulatory approval track records, and hospital system contracting scale to maintain competitive positioning.

DRO Analysis

Driver - Escalating Global Prevalence of Target Vascular Diseases

Surging diagnosis rates of cardiovascular, peripheral, and neurovascular diseases expand the clinical necessity for interventional diagnostic procedures. Chronic conditions such as atherosclerosis, ischemic stroke, and peripheral artery disease demand accurate anatomical mapping. According to the World Health Organization 2025 statistics update, cardiovascular diseases remain the leading cause of global mortality, claiming an estimated 17.9 million lives annually.

This high disease burden forces clinical reliance on catheterization procedures to facilitate subsequent therapeutic choices. Interventional cardiologists utilize specialized tools to ensure the precise delivery of contrast media into the narrowing vasculature. This sustained procedural volume provides a continuous baseline demand for diagnostic tools within acute care settings.

Restraint - High Procedure Costs and Capital Equipment Dependency

High acquisition costs associated with angiography imaging systems and catheterization laboratory infrastructure are limiting adoption across cost-sensitive healthcare institutions. Procurement of imaging consoles, guidewire systems, and advanced disposable catheters requires substantial capital allocation. Smaller healthcare providers face margin pressure because reimbursement variability restricts financial scalability for high-volume interventional programs.

Supply dependence on imported catheter components and specialty polymers is increasing production costs for manufacturers. Sterilization compliance requirements and quality validation procedures are extending manufacturing timelines, creating inventory management challenges. Healthcare facilities in developing economies often delay technology upgrades because operational expenditure associated with interventional imaging procedures remains comparatively high.

Opportunity - Integration of Specialty Microcatheters in Neurovascular and Oncology Interventions

Expanding the application scope of angiography catheters into oncology and neurovascular therapeutics unlocks distinct high-margin growth avenues. Microspheres and targeted chemotherapeutic agents require microcatheters for precise local delivery into hyper-vascularized tumors or intracranial aneurysms. This specific application demands specialized materials designed for high burst pressure resistance and exceptional flexibility.

Producers can capture premium pricing segments by engineering custom co-extruded polymer blends optimized for micro-scale interventions. Entering these specialized therapeutic areas reduces reliance on the highly competitive coronary market. Developing deep partnerships with neurological stroke centers establishes consistent, recurring institutional sales contracts.

Category-wise Analysis

Product Type Insights

Coronary angiography catheters are anticipated to secure around 38% of the angiography catheters market share in 2026, reflecting the dominant procedural volume associated with coronary artery disease diagnosis and the entrenched clinical preference for dedicated coronary catheter shapes, including Judkins Left, Judkins Right, and Amplatz configurations. Medtronic's Launcher guide catheter series exemplifies the category leadership in this segment. The high procedural frequency of coronary angiography in outpatient catheterization settings sustains consistent replenishment demand and reinforces the segment's revenue primacy.

Microcatheters are expected to be the fastest-growing segment, propelled by the accelerating adoption of complex neurovascular and peripheral interventional procedures that require navigation through highly tortuous and distal vascular territories inaccessible to conventional catheter platforms. Stryker's Headway Duo microcatheter demonstrates the clinical precision enabling distal access in intracranial procedures. The proliferation of neurointerventional centers and the growing evidence base supporting catheter-based treatment of cerebrovascular conditions are collectively expanding the procedural indications that generate microcatheter utilization.

Application Insights

Coronary artery disease procedures are poised to dominate with a forecast market share of over 42% in 2026, powered by the global epidemic of atherosclerotic coronary disease and the near-universal adoption of invasive coronary angiography as the definitive diagnostic modality before percutaneous coronary intervention or surgical revascularization. Abbott's coronary catheter portfolio supports high-volume coronary angiography across major cardiac centers.

Neurological disorders are estimated to be the fastest-growing application segment, fueled by the expanding clinical evidence base supporting catheter-based diagnosis and treatment of stroke, cerebral aneurysms, arteriovenous malformations, and intracranial atherosclerosis, combined with the increasing establishment of comprehensive stroke centers equipped with interventional neuroradiology capabilities. Penumbra's neurovascular product ecosystem reflects this category's rapid commercial expansion.

End-user Insights

Hospitals are likely to be the leading segment with a projected 54% of the angiography catheters market share in 2026, due to the concentration of complex cardiovascular and neurovascular procedural capacity within tertiary and quaternary hospital settings that command the institutional infrastructure, specialist physician resources, and post-procedural care capabilities required for high-acuity catheter-based diagnostic and interventional workflows. The Cleveland Clinic's comprehensive catheterization laboratory network exemplifies the hospital segment's procedural dominance.

Ambulatory surgical centers are anticipated to be the fastest-growing end-user segment, fueled by the regulatory expansion of catheterization procedures approved for outpatient settings, the cost-efficiency advantages of ambulatory care delivery relative to inpatient hospital settings, and the growing patient preference for same-day procedures that minimize hospitalization-associated disruption.

Regional Insights

North America Angiography Catheters Market Trends

North America is expected to lead with an estimated 38% of the angiography catheters market share in 2026, supported by the highest per-capita density of cardiac catheterization laboratories globally, a mature private health insurance infrastructure that facilitates procedural reimbursement, and the presence of the world's leading angiography catheter manufacturers, including Medtronic, Abbott Laboratories, and Teleflex, within the regional innovation ecosystem.

U.S. Angiography Catheters Market Insight

The U.S. is projected to maintain a commanding position within the regional landscape due to the rising number of outpatient endovascular procedures performed in office-based labs. Regulatory clearances from the Food and Drug Administration in early 2026 for next-generation microcatheters expand the domestic interventional product selection.

Canada Angiography Catheters Market Insights

Canada is expected to demonstrate steady growth contribution driven by government funding allocations aimed at reducing wait times for elective cardiovascular surgeries across provincial health networks. Public healthcare institutions expand interventional radiology capabilities to manage rising peripheral artery disease diagnoses within aging populations.

Europe Angiography Catheters Market Trends

Europe is likely to hold a prominent market position, sustained by the strict execution of European Medical Device Regulation criteria that favor established manufacturers with proven clinical safety profiles. Interventional cardiology societies across Germany and France advocate for transradial access methodologies, increasing demand for specific long-reach catheter designs.

Germany Angiography Catheters Market Insights

Germany is forecast to lead continental volume consumption due to its dense network of dedicated chest pain units and comprehensive stroke centers. German hospital networks invest heavily in high-resolution digital subtraction angiography suites, requiring continuous supplies of matching diagnostic catheters. Local production facilities operated by regional medical engineering firms optimize domestic supply chain responsiveness.

U.K. Angiography Catheters Market Insights

The U.K. is expected to experience rising device utilization as National Health Service trusts implement modernized clinical pathways for rapid stroke intervention. Institutional shifts toward ambulatory diagnostic interventional models shorten average hospital lengths of stay. This operational shift drives the uptake of single-use, high-performance neurovascular catheters.

Asia Pacific Angiography Catheters Market Trends

Asia Pacific is forecast to be the fastest-growing market for angiography catheters, stimulated by expanding healthcare facility construction and surging patient populations requiring chronic vascular disease treatments. Government initiatives across emerging countries expand public medical insurance coverage to include advanced endovascular interventions. Regional manufacturing hubs scale up output to deliver cost-competitive medical devices across developing rural healthcare networks.

China Angiography Catheters Market Insights

China is likely to experience rapid structural market expansion due to centralized government procurement programs targeting high-volume medical consumables. Domestic manufacturers such as Lepu Medical expand production lines to fulfill strict localized production mandates. The expanding volume of percutaneous coronary interventions performed in tier-2 and tier-3 cities sustains significant volume growth.

Japan Angiography Catheters Market Insights

Japan is expected to display high value-density driven by a rapidly aging demography requiring complex neurovascular and peripheral interventions. Japanese clinicians exhibit high preferences for premium microcatheters featuring advanced torque transmission properties. Strict pricing controls implemented by the Ministry of Health, Labour and Welfare shape long-term product margin profiles.

Competitive Landscape

The global angiography catheters market is moderately fragmented, featuring a mix of tier-one medical technology corporations and specialized regional medical device producers. Key market participants include Medtronic plc, Boston Scientific Corporation, Terumo Corporation, Cordis, and Merit Medical Systems, Inc., which collectively manage extensive distribution networks.

These prominent industry entities utilize substantial research budgets to engineer proprietary hydrophilic coatings and kink-resistant shaft braids, raising entry barriers for new participants. Smaller specialized entities compete by focusing on custom microcatheter designs for niche neurovascular or oncology applications.

Key Industry Developments:

- In May 2026, Johnson & Johnson launched the Shockwave C2 Aero Coronary IVL catheter for calcified coronary artery disease treatment, reinforcing precision angiography catheter adoption through enhanced lesion crossing and vessel navigation capabilities.

- In September 2025, ASAHI INTECC USA launched Veloute and Tellus embolization microcatheters in the United States, reinforcing angiography catheter precision and navigational control across peripheral vascular intervention procedures.

Companies Covered in Angiography Catheters Market

- Medtronic plc

- Boston Scientific Corporation

- Terumo Corporation

- Cordis

- Merit Medical Systems, Inc.

- Cook Medical LLC

- B. Braun SE

- AngioDynamics, Inc.

- Teleflex Incorporated

- Penumbra, Inc.

- Lepu Medical Technology (Beijing) Co., Ltd.

- MicroPort Scientific Corporation

Frequently Asked Questions

The global angiography catheters market is projected to reach US$1.8 billion in 2026.

Rising prevalence of cardiovascular and neurovascular diseases, increasing minimally invasive diagnostic procedures, and expanding catheterization laboratory infrastructure are driving the angiography catheters market.

The angiography catheters market is poised to witness a CAGR of 5.9% from 2026 to 2033.

Expansion of neurovascular interventions, growth in outpatient angiography procedures, and increasing investment in advanced imaging-compatible catheter technologies are creating significant opportunities in the angiography catheters market.

Some of the key market players include Medtronic plc, Boston Scientific Corporation, Terumo Corporation, Cordis, and Merit Medical Systems, Inc.