- Pharmaceuticals

- Actinic Keratosis Treatment Market

Actinic Keratosis Treatment Market Size, Share, and Growth Forecast 2026 - 2033

Actinic Keratosis Treatment Market by Treatment Type (Procedural Modality, Topical Treatment, Photodynamic Therapy, Others), by End User (Hospitals, Private Dermatology Clinics, Laser Therapy Centers, Cancer Treatment Centers, Spas and Rejuvenation Centers, Homecare), by Regional Analysis, 2026 - 2033

Actinic Keratosis Treatment Market Size and Trend Analysis

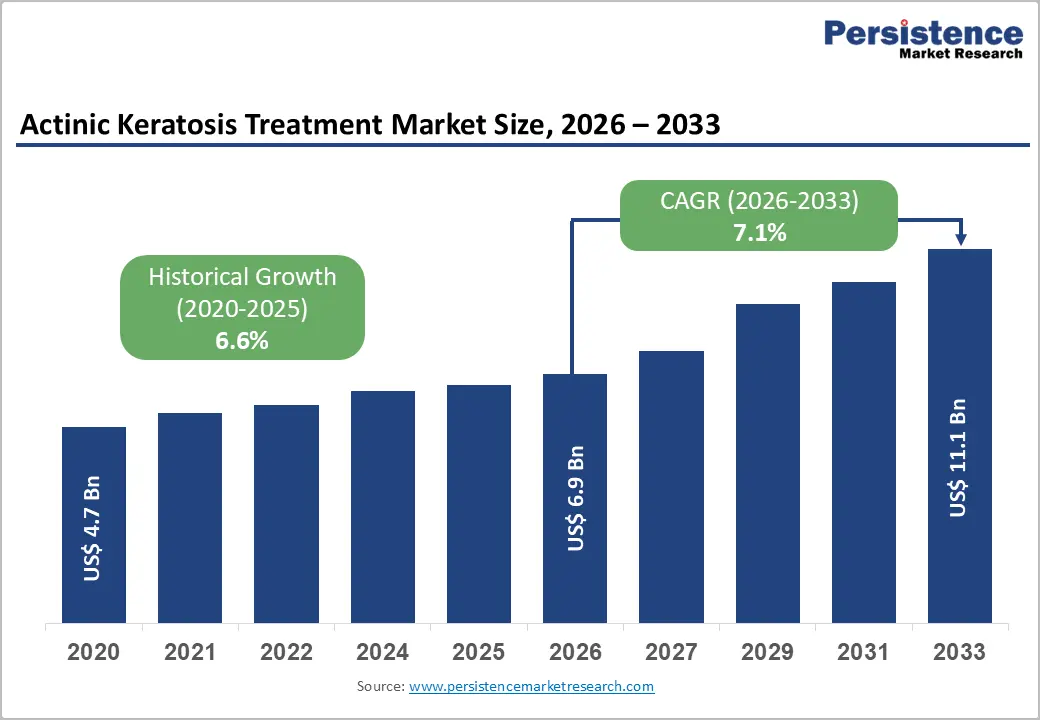

The global actinic keratosis treatment market is expected to be valued at US$ 6.9 billion in 2026 and projected to reach US$ 11.1 billion by 2033, growing at a CAGR of 7.1% between 2026 and 2033.

The actinic keratosis treatment market is expanding steadily, fueled by rising disease prevalence linked to prolonged ultraviolet exposure and rapidly aging populations worldwide. Millions of patients, particularly in high-sunlight regions, now undergo routine dermatologic screening because untreated lesions can progress into squamous cell carcinoma. Innovation is reshaping care delivery, with improved topical agents, shorter-course regimens, and advanced photodynamic therapies gaining traction after regulatory clearances in major markets. Approvals from authorities such as the FDA and EMA are accelerating product adoption and physician confidence. At the same time, public health campaigns led by dermatology organizations are increasing awareness of early symptoms and encouraging preventive treatment, thereby shifting patient behavior toward earlier diagnosis, repeated therapy cycles, and long-term disease management.

Key Market highlights

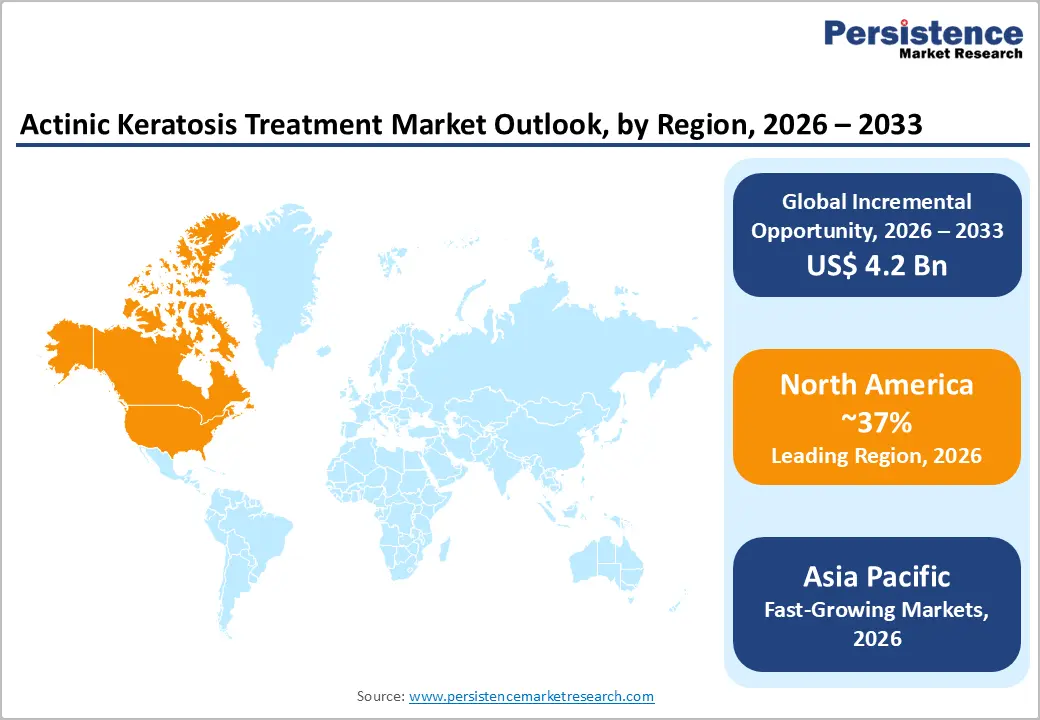

- North America leads the actinic keratosis treatment market, supported by strong dermatology infrastructure, high diagnosis rates, favourable reimbursement frameworks, and rapid uptake of novel therapies.

- Asia Pacific is the fastest-growing region, driven by aging populations, rising ultraviolet exposure, expanding hospital networks, and increasing investments in dermatology services.

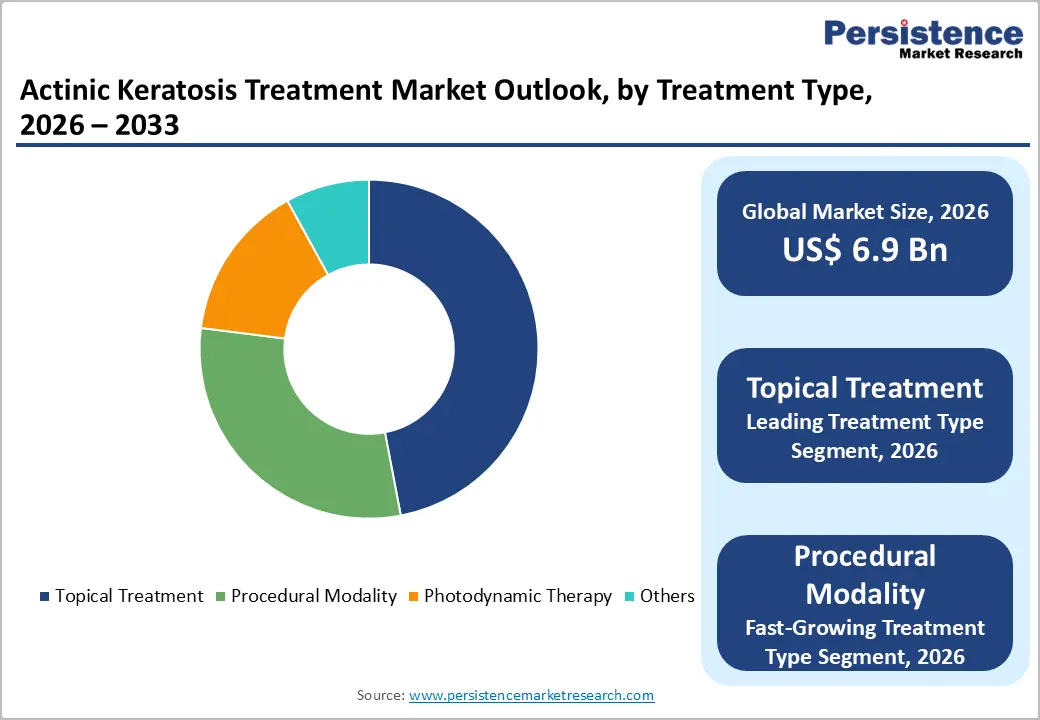

- Topical therapies account for the largest share of treatment due to ease of home application, suitability for field lesions, cost advantages, and widespread physician preference for early-stage disease.

- Photodynamic therapy is the fastest-growing treatment modality, supported by daylight protocols, improved photosensitizers, device approvals, and demand for cosmetically favourable, non-invasive options.

| Key Insights | Details |

|---|---|

|

Actinic Keratosis Treatment Market Size (2026E) |

US$ 6.9 billion |

|

Market Value Forecast (2033F) |

US$ 11.1 billion |

|

Projected Growth CAGR (2026-2033) |

7.1% |

|

Historical Market Growth (2020-2025) |

6.6% |

Market Dynamics

Driver: Rise in the prevalence of actinic keratosis

The rising prevalence of actinic keratosis, greater awareness of disease treatment, and the growing demand for minimally invasive therapies are expected to drive the growth of the actinic keratosis treatment market. The growing awareness of the harmful effects of actinic keratosis is driving demand for actinic keratosis therapy. Furthermore, awareness programs launched by government agencies and non-profit groups contribute significantly to market development. Increasing R&D initiatives are also expected to boost the approval of new medications for actinic keratosis treatment. Furthermore, the increased risk of getting actinic keratosis-related skin cancer has increased detection and treatment frequencies.

Increase in the number of drug approvals and launch of novel therapies

The Actinic Keratosis Treatment Market is expected to grow due to increased approvals of new medications and the introduction of novel treatments for the disease. New drugs for the treatment of actinic keratoses have been authorized by the US Food and Drug Administration (FDA). These drugs include topical fluorouracil, imiquimod, diclofenac, ingenol mebutate, and pharmaceutical treatment combinations. The topical medications category accounts for a sizable market share in the actinic keratosis treatment market and is expected to exhibit a similar trend during the forecast period, owing to the ease of product availability, high target specificity, and lesser risk of scarring. Furthermore, potential pipeline drugs and widespread usage of combination treatment are important driving factors to the market. Another factor expected to drive market expansion is the rise in the adoption and commercialization of novel medications. Increased R&D efforts are likely to boost the approval of novel medications for the treatment of actinic keratosis, further driving the growth of the Actinic Keratosis Treatment Market.

Restraint: Lack of skilled professionals and low penetration of treatment

The primary challenges impeding the growth of the actinic keratosis treatment market are a lack of skilled professionals and limited treatment penetration in emerging economies. Actinic keratosis treatment requires skilled professionals and surgeons to perform procedures such as chemical peels, cryotherapy, and photodynamic therapy. However, a significant scarcity of general surgeons is expected to hinder the growth of the actinic keratosis treatment market. Furthermore, less awareness about the health problem in developing countries, as well as higher treatment costs are projected to limit market expansion. The emergence of alternative natural remedies is also expected to hamper market growth.

Opportunity: Expansion in Daylight Photodynamic Therapy

Daylight photodynamic therapy (PDT) represents a major growth opportunity within the Actinic Keratosis Treatment Market, driven by its convenience, favorable tolerability profile, and comparable efficacy to conventional lamp-based PDT. Clinical studies have shown that indoor or outdoor daylight protocols can clear actinic keratosis lesions year-round while significantly reducing treatment-related pain and post-procedure discomfort. Innovation in photosensitizers is strengthening adoption, with Biofrontera’s optimized Ameluz formulation receiving European regulatory approval in 2024, extending product exclusivity and enhancing real-world outcomes. In parallel, U.S. regulatory clearances for illumination systems such as Sun Pharma’s LED BLU-U device are improving scalability across dermatology clinics. Rapidly aging populations in the Asia Pacific, coupled with increasing ultraviolet exposure, further expand the addressable patient pool. Together, these trends are accelerating the shift toward non-invasive, patient-friendly therapies and positioning manufacturers for sustained revenue growth.

Category-wise Insights

Treatment Type Analysis

Topical treatment dominated the actinic keratosis market in 2026 with an estimated 47% share, reflecting its widespread use as a first-line therapy for early-stage and field cancerization lesions. Dermatologists frequently prescribe agents such as 5-fluorouracil, imiquimod, diclofenac, and newer options like tirbanibulin because they can be self-applied, avoid procedural visits, and treat multiple lesions simultaneously. FDA-approved 5-fluorouracil has demonstrated high clearance rates reported up to 74% and remains a benchmark therapy for reducing progression risk toward squamous carcinoma, contributing to its substantial drug-level share. Tirbanibulin 1% ointment has further strengthened the segment, with phase III trials showing that nearly half of patients achieved complete clearance and significant reductions in lesion counts. Favorable guidance from regulatory bodies and professional associations supports topical therapy in appropriate patients, while comparatively lower treatment costs versus cryotherapy or photodynamic procedures enhance adoption. High adherence in home-care settings and growing awareness campaigns continue reinforcing topical treatment’s leadership position globally.

End User Analysis

Hospitals represented the leading end-user segment in 2025, supported by their ability to manage complex dermatologic cases through multidisciplinary teams, advanced diagnostic tools, and in-house access to photodynamic therapy systems. Many tertiary and academic hospitals have invested heavily in dedicated dermatology and oncology units, enabling comprehensive lesion assessment, biopsy confirmation, and combination-treatment protocols when needed. Favorable reimbursement frameworks for inpatient or hospital-based procedures, particularly in developed markets, further channel patient volumes toward these facilities. Rising skin cancer prevalence, especially in high-UV-exposure regions, has increased referrals for higher-risk or extensive actinic keratosis cases, which are more often handled in hospital settings than in small outpatient clinics. Integration of digital dermoscopy, artificial-intelligence-supported screening tools, and electronic care pathways is also improving diagnostic accuracy and workflow efficiency. Together, expanding patient caseloads, infrastructure upgrades, and technological adoption continue to sustain hospitals’ dominant role within the actinic keratosis treatment ecosystem.

Regional Insights

North America Actinic Keratosis Treatment Market Trends and Insights

North America continues to represent a mature and high-value market for actinic keratosis treatment, supported by elevated skin cancer awareness, strong dermatology networks, and routine screening among older adults. The region benefits from rapid uptake of newly approved topical agents and photodynamic therapy systems, with clinicians favoring therapies that combine high clearance rates and cosmetic outcomes. Extensive insurance coverage for physician-administered procedures and prescription drugs encourages earlier intervention and follow-up care, sustaining treatment volumes. Academic hospitals and specialty dermatology chains remain central to innovation, frequently participating in clinical trials that introduce next-generation photosensitizers, daylight PDT protocols, and digital diagnostic platforms. Growth is also reinforced by rising outdoor recreation, occupational sun exposure, and an aging population particularly vulnerable to chronic ultraviolet damage. Together, regulatory support, access to reimbursement, and continuous product innovation are shaping a stable yet technologically advancing North American market landscape.

Asia Pacific Actinic Keratosis Treatment Market Trends and Insights

Asia Pacific is emerging as one of the fastest-expanding regions for actinic keratosis therapies, driven by demographic shifts, increasing dermatology access, and improving public awareness of sun-related skin disorders. Rapid population aging in countries such as Japan, China, and South Korea is expanding the at-risk patient population, while urbanization and recreational travel are increasing cumulative ultraviolet exposure. Governments and private providers are investing in specialty clinics and hospital dermatology departments, supporting greater diagnosis rates than in previous decades. Adoption of topical field therapies is accelerating due to affordability and suitability for home use, while photodynamic therapy is gaining traction in urban centers among patients seeking non-invasive cosmetic outcomes. Local manufacturing of dermatologic drugs and devices is also reducing costs and improving distribution. These combined trends position the Asia Pacific as a key growth engine for global actinic keratosis treatment demand.

Competitive Landscape

The actinic keratosis treatment industry is highly competitive and increasingly consolidated, with a limited number of major players dominating global revenues. These companies actively pursue mergers, acquisitions, and strategic partnerships to strengthen geographic reach, expand dermatology portfolios, and accelerate regulatory approvals. Ongoing investment in research and development supports the launch of next-generation topical agents, improved photosensitizers, and advanced photodynamic therapy devices. Firms are also focusing on lifecycle management strategies, including formulation upgrades and combination regimens, to extend product exclusivity and differentiate offerings. Market participants target emerging regions through local collaborations while reinforcing positions in mature markets, creating intense rivalry as companies seek to capture rising diagnosis rates and expanding treatment volumes worldwide.

Key Market Developments

- In 2025, Torqur AG dosed the first patient in a Phase II trial of Bimiralisib for actinic keratosis, evaluating its safety and efficacy across about 200 participants in European and U.S. study centers.

- In 2025, Biofrontera submitted an sNDA to raise aminolevulinic acid hydrochloride dosage from 20% to 30% for actinic keratosis, aiming to broaden photodynamic therapy options and improve clinical outcomes.

Companies Covered in Actinic Keratosis Treatment Market

- Sun Pharmaceutical Industries Ltd.

- Biofrontera

- Nestle SA

- Bausch Health Companies Inc.

- Novartis AG

- GlaxoSmithKline plc.

- Almirall, LLC

- LEO Pharma Inc.

- Cipher Pharmaceuticals Inc

- Pierre Fabre Pharmaceuticals, Inc.

- BioLineRX

- Alma Lasers

- Valeant Pharmaceuticals

- 3M

- Others

Frequently Asked Questions

The global actinic keratosis treatment market is valued at US$ 6.9 billion in 2026.

Rising elderly populations, increasing UV exposure, skin cancer awareness, dermatologist visits, screening programs, and expanding access to modern therapies worldwide.

North America leads with 37% share in 2025.

Expansion of daylight photodynamic therapy, improved photosensitizers, home-based protocols, Asia Pacific aging populations, and regulatory approvals boosting adoption.

Leaders include Sun Pharmaceutical Industries Ltd., Biofrontera, Nestle SA, Bausch Health Companies Inc., Novartis AG, and GlaxoSmithKline plc.