- Hardware & Software IT Services

- Data Center Liquid Cooling Market

Data Center Liquid Cooling Market Size, Share, and Growth Forecast, 2026 - 2033

Data Center Liquid Cooling Market by Component (Solution and Services), Cooling Type (Cold Plate Liquid Cooling, Immersion Liquid Cooling, Spray Liquid Cooling), Data Center Size (Small and Medium-sized Data Centers and Large Data Centers), End-user, and Regional Analysis for 2026 - 2033

Data Center Liquid Cooling Market Size and Trends Analysis

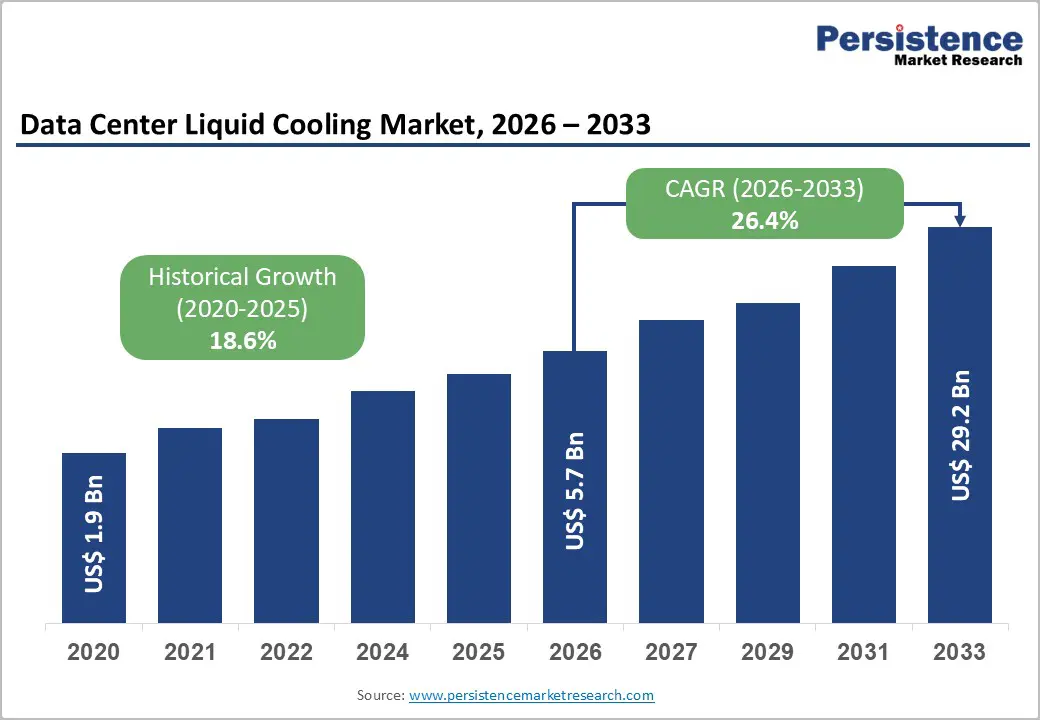

The global data center liquid cooling market size is projected to rise from US$5.7 Bn in 2026 to US$29.2 Bn by 2033. It is anticipated to witness a CAGR of 26.4% during the forecast period from 2026 to 2033.

The surge in AI, high-performance computing (HPC), hyperscale workloads, and cloud expansion is pushing data center operators toward liquid cooling technologies to manage escalating heat loads that traditional air-cooling systems cannot efficiently handle. Cold-plate and immersion cooling systems are being adopted to achieve lower PUE values 1.02-1.2, reduce carbon footprints, and comply with global sustainability mandates aimed at lowering energy consumption in IT infrastructure.

Key Industry Highlights:

- Leading Component: Solutions dominate with over 73% share in 2026 & exceeding the value of US$ 4.2 Bn, addressing high heat densities, energy consumption, and space constraints. Services are growing at a CAGR 27.8%, supporting installation, maintenance, and optimization for complex liquid cooling deployments.

- Leading Cooling Type: Cold plate liquid cooling holds more than 55% share in 2026 & values over US$ 3.1 Bn due to efficient CPU/GPU thermal management, modular design, and ease of integration. Immersion cooling is the fastest-growing, achieving 80% higher energy efficiency and PUE 1.02-1.03, while allowing compact high-density deployments.

- Leading Data Center Size: Large data centers (>10,000 sq. ft.) hold over 64% share in 2026, valued at more than US$ 3.6 Bn, driven by high heat density and energy demand. Small and medium facilities are growing at a CAGR 28%, fueled by edge computing and space-efficient cooling needs.

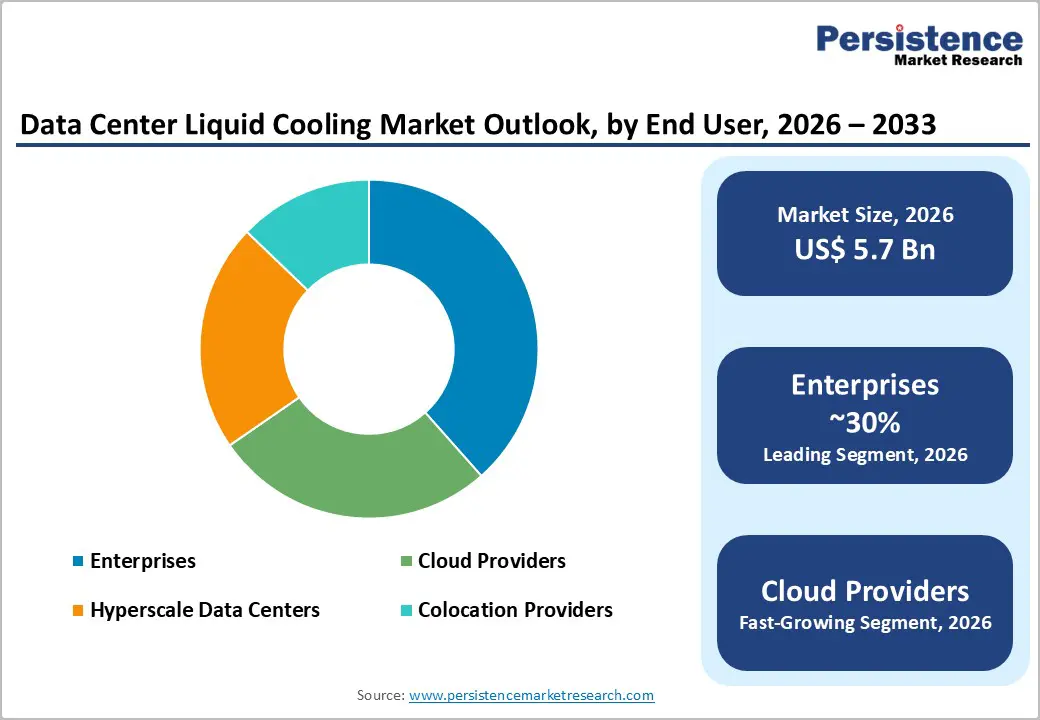

- Leading End-user: Enterprises command over 30% share in 2026 due to high-performance computing demands and sustainability targets. Cloud providers grow at the highest rate, CAGR 29.5%, driven by AI workloads and hyperscale infrastructure investments by AWS, Microsoft Azure, and Google Cloud.

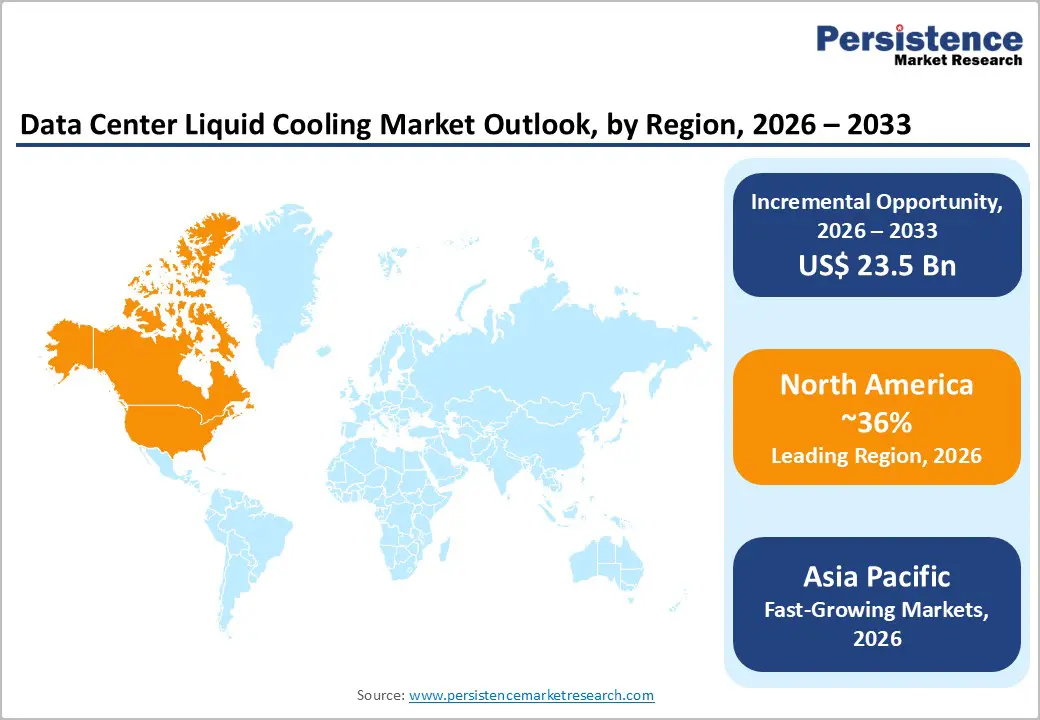

- Regional Leadership: North America leads with more than 36% share in 2026, valued at over US$ 2.1 Bn, projected to exceed US$ 8.7 Bn by 2033, driven by AI/GPU workloads, defense modernization, and regulatory PUE mandates. Asia Pacific is the fastest-growing region CAGR 35.6%, led by China, India, and Japan with rising AI, cloud, 5G edge adoption, and renewable energy initiatives.

| Key Insights | Details |

|---|---|

| Data Center Liquid Cooling Market Size (2026E) | US$5.7 Bn |

| Market Value Forecast (2033F) | US$29.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 26.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 18.6% |

Market Dynamics

Driver - Rising AI and HPC Power Densities Driving Liquid Cooling Adoption

Increasing computational demands from AI and High-Performance Computing (HPC) are driving higher server rack densities, often exceeding 30-50 kW per rack, compared to traditional 5-10 kW, making advanced liquid cooling essential. Liquid cooling improves energy efficiency, offers heat transfer up to 1,000 times more effective than air cooling, and supports AI workloads projected to quadruple electricity use. Global data center electricity demand may surpass 945 TWh by 2030, with advanced economies driving over 20% of growth. Immersion and cold plate cooling are increasingly adopted in sectors like finance, healthcare, and scientific research to manage GPU-intensive workloads, aligning with HPC market expansion.

Energy Efficiency and Sustainability Driving Green Liquid Cooling in Data Centers

Environmental and regulatory pressures are pushing adoption of green liquid cooling, achieving PUE <1.2 versus 1.4-1.6 for air-cooled centers. Companies like Microsoft have introduced water-free AI-optimized designs, saving 125 million liters of water annually per facility. Regulatory bodies like TRAI promote green data center certifications, emphasizing low PUE, renewable energy, and sustainable cooling practices. Liquid cooling dissipates 2-10 times more heat than air, helping operators reduce carbon footprints, comply with ESG standards, and lower operational costs while maintaining high performance.

Restraint - High Initial Capital Investment and Retrofit Challenges

Liquid cooling systems incur 20-30% higher upfront costs than air cooling, especially immersion setups needing specialized infrastructure. Retrofitting existing data centers is complex, requiring redesign of racks, piping, and safety mechanisms. Small and mid-sized enterprises face budget constraints, limiting adoption and slowing overall market penetration. These capital-intensive challenges pose a significant barrier despite long-term efficiency benefits.

Operational, Technical, and Water-Use Challenges

The adoption of data center liquid cooling faces significant challenges due to a shortage of skilled professionals and limited technical expertise, which slows deployment and increases reliance on specialized vendors. Integrating liquid cooling systems requires precise engineering knowledge, while compliance with regional safety, environmental, and building regulations adds complexity. High water consumption in immersion and evaporative cooling systems raises operational costs and sustainability concerns. A 1 MW data center can be used up to 25.5 million liters annually, and according to a Morgan Stanley report, AI data centers are projected to consume 1,068 billion liters by 2028, an 11-fold increase from current levels. These technical, regulatory, and resource constraints collectively hinder rapid adoption, increase upfront costs, and create operational uncertainties for data center operators.

Opportunity - Advanced Coolant Materials and Closed-Loop Innovation

Development of advanced dielectric fluids with improved thermal and environmental properties addresses regulatory pressures and enhances performance. Heat reuse through municipal district-heating systems creates new revenue streams, turning cooling into a profit center. AI-powered thermal management with predictive maintenance and dynamic optimization opens opportunities for intelligent infrastructure. Companies like Chindata Group are integrating hybrid X-Cooling systems, combining air, liquid, and hybrid methods for sustainable, high-density deployments.

Government Support Accelerating Green Data Center Adoption

Governments are promoting green data centers through subsidies, tax breaks, and infrastructure support, lowering costs and driving adoption of liquid cooling for energy efficiency. Policies like the EU Energy Efficiency Directive, the U.S. Inflation Reduction Act 2022, and Germany’s EnEfG mandate stricter PUE targets ≤1.5 by 2027, ≤1.3 by 2030, and 1.2 for new centers from 2026, along with waste heat reuse requirements 10-20% between 2026-2028. Waste heat reuse requirements 10-20% by 2026-2028 and ESG goals further accelerate green cooling. Growth of edge computing and 5G networks increases demand for compact, energy-efficient, modular liquid cooling solutions suitable for high-density, space-constrained deployments.

Category-wise Analysis

Component Insights

Solution segment is expected to account for more than 73% share in 2026, driven by the need for complete cooling systems that tackle rising heat densities, excessive energy consumption, and limited data center space. As AI, cloud, and HPC workloads surge, operators increasingly seek advanced cooling solutions that ensure immediate performance, efficiency, and reliability improvements.

Services are expected to grow at a leading CAGR due to data centers increasingly requiring specialized installation, maintenance, and optimization support for complex liquid cooling systems. The need for continuous performance optimization, energy efficiency, and regulatory compliance drives reliance on external service providers, ensuring reliable operation and reduced downtime.

Cooling Type Insights

Cold plate liquid cooling is expected to account for more than 55% share in 2026 due to efficiently addressing the growing need for high-density server cooling. It provides direct contact cooling for CPUs and GPUs, offering superior thermal management and energy efficiency compared to other methods. Its modular design allows easy integration into existing data center infrastructure, reducing operational downtime.

Immersion liquid cooling is expected to grow at the highest rate as it efficiently manages high-density server heat, meeting the growing demand for energy-efficient solutions. Its ability to drastically reduce power usage for cooling aligns with operators’ needs to cut operational costs and carbon footprints. Technology also addresses space constraints by allowing more servers per rack, fulfilling the need for compact, high-performance infrastructures. Single-phase immersion cooling achieves 80% higher energy efficiency compared to cold plate systems, delivering PUE scores of 1.02-1.03.

Data Center Size Insights

Large data centers (more than 10,000 sq. feet) are expected to account for over 64% share in 2026 and are expected to reach over US$ 3.6 Bn in value as they face higher heat densities and energy demands compared to smaller facilities. Their need for efficient, high-capacity cooling solutions to maintain uptime and reduce operational costs drives adoption. Liquid cooling helps large data centers achieve better energy efficiency, meet sustainability targets, and support advanced computing workloads, which are increasingly common in large facilities.

Small and medium-sized data centers are expected to grow at a positive CAGR as they face increasing demands for high-performance computing in limited spaces. These facilities require efficient, compact cooling solutions to manage rising heat densities without expanding their physical footprint. The growing adoption of edge computing and localized data processing further drives demand.

End-user Insights

Enterprises are expected to account for over 30% share in 2026 as they face growing demands for high-performance computing, low-latency applications, and efficient energy use. It helps enterprises manage increasing server densities and heat loads while reducing operational costs. The need for reliable uptime, faster processing, and sustainability targets drives enterprises to adopt advanced liquid cooling solutions more aggressively.

Cloud providers are expected to grow at the highest rate with a CAGR of 29.5% due to AI workload expansion, machine learning infrastructure, and scalable computing platform requirements. Hyperscale operators, including AWS, Microsoft Azure, and Google Cloud, invest heavily in liquid cooling to support large-scale AI model training and inference services. Net-zero emission commitments and sustainability targets among major cloud operators drive the adoption of energy-efficient cooling technologies.

Regional Insights

North America Data Center Liquid Cooling Market Trends

North America is expected to account for more than a 36% share in 2026, valued at over US$2.1 billion, and is projected to exceed US$8.7 billion by 2033, driven by defense modernization, autonomous vehicles, drones, biomedical imaging, and government-backed advanced optics research. The rapid rise of high-density AI/GPU workloads has pushed U.S. data-center electricity from ~76 TWh in 2018 to ~200 TWh in 2025, highlighting the need for efficient cooling according to DOE/LBNL. The U.S. data center liquid cooling market is expected to reach US$ 6.8 billion by 2033, driven by increasing AI workloads and sustainability mandates. Regulatory frameworks such as California’s energy efficiency standards are encouraging operators to reduce power usage effectiveness (PUE), indirectly accelerating liquid cooling adoption.

Asia Pacific Data Center Liquid Cooling Market Trends

Asia-Pacific is expected to reach a CAGR of 35.6%, driven by rapid AI, cloud, and 5G edge growth, which pushes compute density and rack power beyond air-cooling limits, making liquid cooling essential for thermal performance, lower PUE, and reduced energy per compute unit. China targets ~15% annual growth in data-center power and emphasizes renewables and efficiency (national plans), while India’s peak power demand hit 250 GW in FY 2024-25, with policies from BEE, CEA, and MOSPI promoting low-energy DC designs. Japan’s high electricity costs and focus on energy efficiency are accelerating the adoption of liquid cooling technologies, particularly for HPC and advanced computing applications.

Europe Data Center Liquid Cooling Market Trends

Europe is expected to reach a market value of approximately US$7.1 billion by 2033, driven by stringent sustainability regulations and the expansion of digital infrastructure across Germany, the United Kingdom, France, and Spain. EU data centers consume around 3% of electricity, with mandates on PUE, energy use, and waste-heat reuse promoting liquid cooling for efficiency. Germany leads adoption due to its dense data center ecosystem and focus on digital sovereignty, while Nordic countries utilize liquid cooling to recover heat for district heating systems. Leading operators such as Equinix are deploying liquid-ready facilities, and recent hyperscaler expansions in Finland underscore Europe’s growing role in AI-optimized, energy-efficient data center infrastructure.

Competitive Landscape

The global data center liquid cooling market is moderately fragmented, with a mix of established global players and emerging technology providers. Leading companies are focusing on innovation, strategic partnerships, and product development to strengthen their market position. Research and development investments are centered on improving cooling efficiency and reducing operational costs. The market is witnessing increased collaboration between IT hardware manufacturers and cooling solution providers to deliver integrated systems.

Key Industry Developments:

- In March 2026, Panasonic Corporation launched new Coolant Distribution Units (400kW, 800kW) and free-cooling chillers (800kW, 1,200kW) in Europe, targeting generative AI data centers with high-efficiency liquid cooling solutions. The move addresses rising heat challenges from GPU-intensive workloads while improving energy efficiency, reducing footprint, and supporting sustainable cooling with low-GWP refrigerants.ss

- In November 2025, Green Revolution Cooling launched the ICEraQ Nano, a compact immersion cooling rack designed for edge deployments, delivering up to 13 kW cooling without requiring chilled water. The system features integrated liquid-to-air heat exchange, pre-filled ElectroSafe fluid, and simplified installation, enabling energy-efficient, high-density cooling with enhanced reliability and a 15-year lifecycle.

Companies Covered in Data Center Liquid Cooling Market

- Schneider Electric

- LiquidStack

- Rittal GmbH Co. KG

- Green Revolution Cooling Inc.

- DCX Liquid Cooling Systems

- IBM

- Asetek

- Emerson Electric Co

- STULZ GMBH

- Alfa Laval

- Vertiv Group Corp.

- Fujitsu

Frequently Asked Questions

The global data center liquid cooling market is projected to be valued at US$5.7 Bn in 2026.

The need to efficiently dissipate high heat loads generated by AI, HPC, and high-density servers and the rising demand for energy-efficient, sustainable cooling solutions to reduce power consumption and operational costs are key drivers of the market.

The data center liquid cooling market is poised to witness a CAGR of 26.4% from 2026 to 2033.

The potential for waste-heat reuse and incentives for sustainable, green data center designs creates strong growth opportunities.

Schneider Electric, LiquidStack, Rittal GmbH Co. KG, Green Revolution Cooling Inc., DCX Liquid Cooling Systems, IBM, and Asetek are among the leading key players.