- Telecommunications

- Wholesale Telecom Market

Wholesale Telecom Market Size, Share, and Growth Forecast 2026 - 2033

Wholesale Telecom Market by Service Type (Voice Wholesale, Data Wholesale, Messaging Services, Mobile Roaming Services, Cloud Interconnect & Connectivity, Dark Fiber & Infrastructure Leasing, Satellite & Submarine Cable Services), Solution, Network Infrastructure Type, Business Model, End-user, and Regional Analysis, 2026 - 2033

Wholesale Telecom Market Size and Trend Analysis

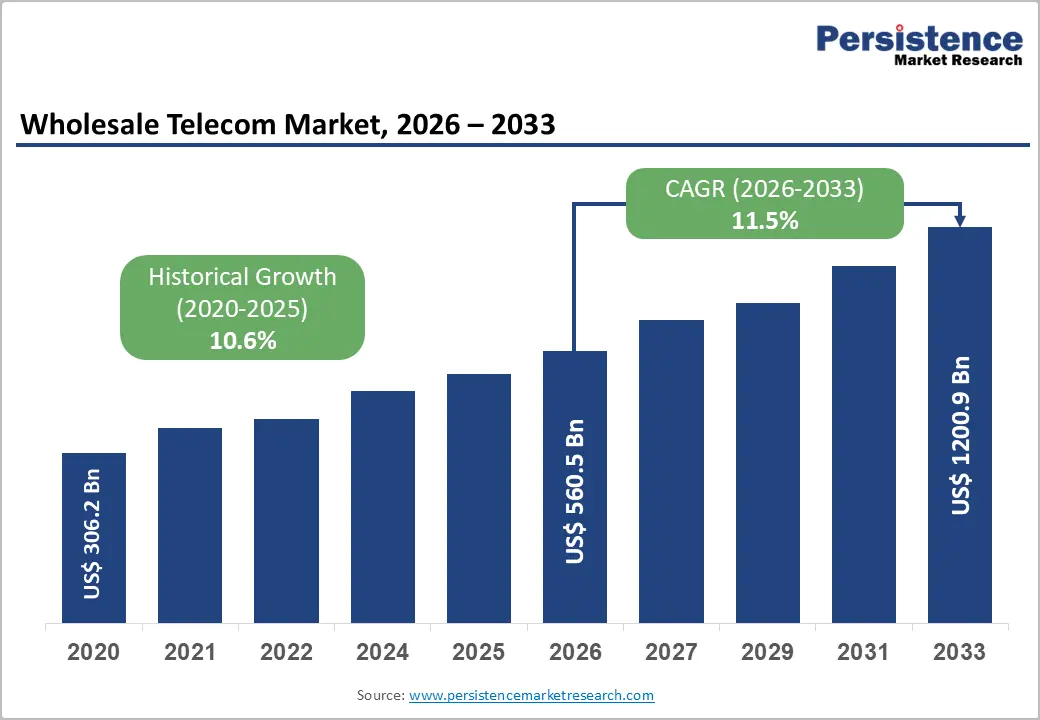

The global wholesale telecom market is expected to reach US$ 560.5 billion in 2026 and US$ 1,200.9 billion by 2033, growing at a CAGR of 11.5% over the forecast period from 2026 to 2033.

The wholesale telecom market is on a robust growth trajectory, driven by an unprecedented surge in global data traffic, the worldwide rollout of 5G network infrastructure, and the rapid migration of enterprise communications to cloud-based platforms.

Key Industry Highlights:

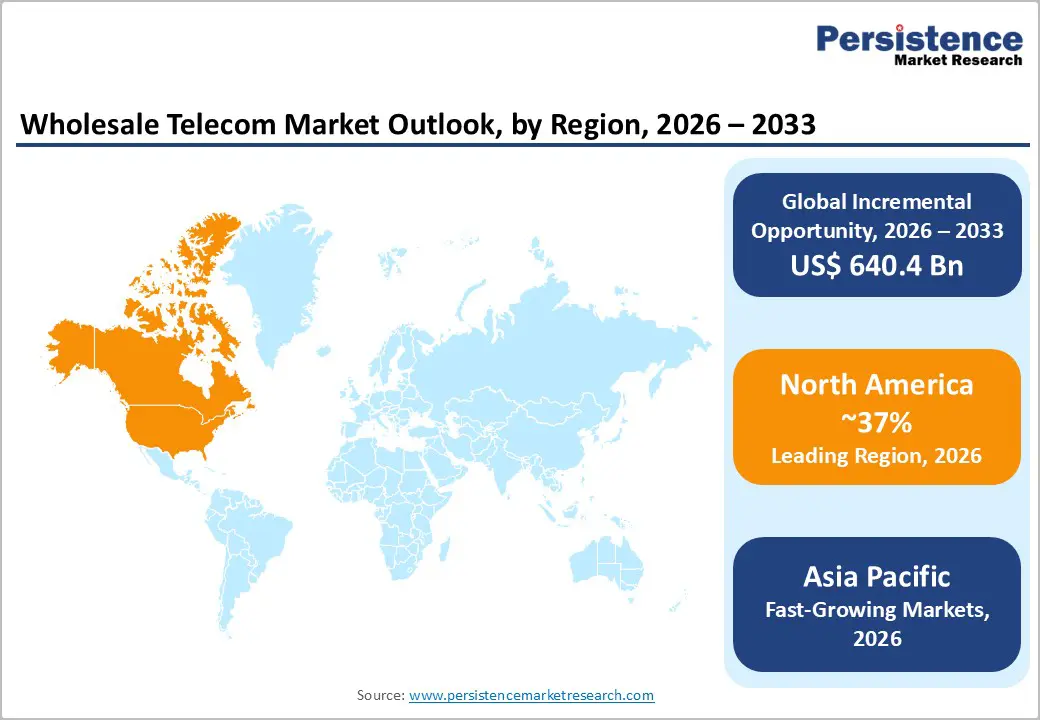

- Leading Region: North America leads the wholesale telecom market, accounting for 37% share, anchored by AT&T and Verizon's global wholesale networks, the world's highest concentration of hyperscale data centers generating massive interconnect demand, and FCC regulatory frameworks shaping wholesale access and internet interconnection standards.

- Fastest Growing Region: Asia Pacific is the fastest growing market with a CAGR of 15.5%, driven by China's three-operator wholesale scale under the 14th Five-Year Plan, India's explosive data consumption via Reliance Jio, Singapore's emergence as a global submarine cable hub, and ASEAN's rapidly digitizing enterprise and consumer connectivity base.

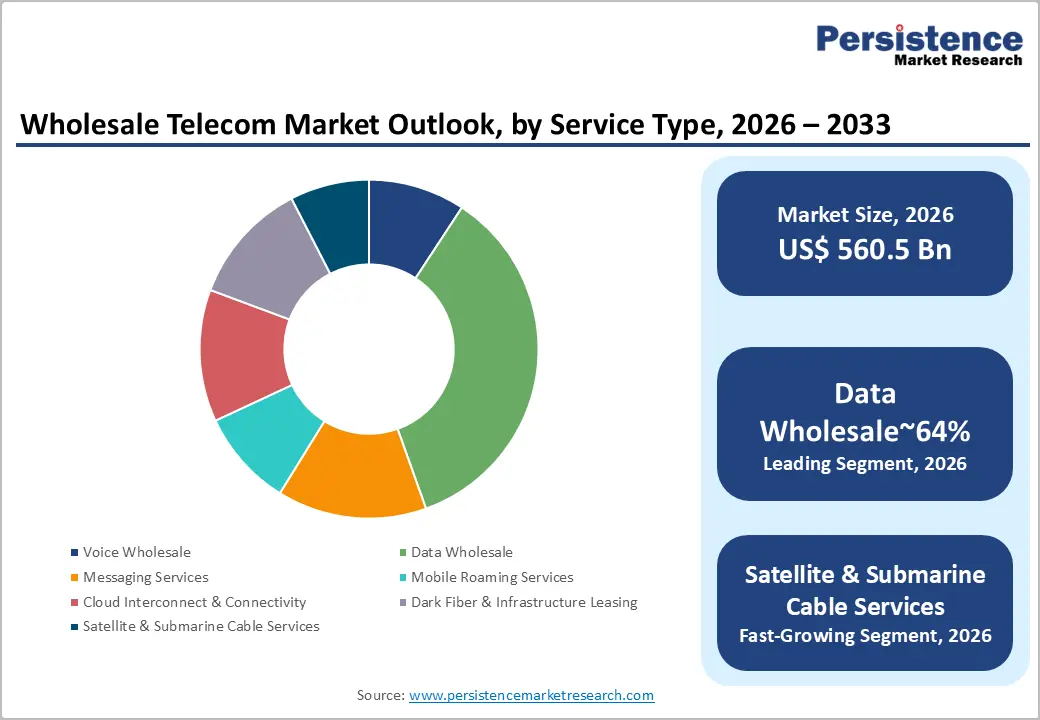

- Dominant Segment: Data wholesale leads with 42% share, underpinned by Ericsson Mobility Report-projected mobile data traffic reaching 325 exabytes per month by 2028, hyperscale cloud provider capacity procurement at scale, and 5G backhaul backbone expansion by operators globally.

- Fastest-Growing Segment: Platform-based wholesale and CPaaS is the fastest-growing business model segment, driven by GSMA Open Gateway API standardization, Sinch and iBASIS API-driven wholesale platform growth, and the enterprise shift to cloud-embedded connectivity that consumes wholesale services programmatically.

- Key Opportunity: Hyperscale data center interconnection represents the market's highest-value opportunity, with 900+ hyperscale facilities globally set to double by 2027, AI workload interconnect demand, and premium dark fiber and cloud wholesale services commanding significant margin premiums over traditional voice wholesale.

Market Dynamics

Drivers - Exponential Growth in Global Data Traffic Fueled by 5G, Cloud, and OTT Services

The relentless surge in global data consumption is the most fundamental driver of wholesale telecom market expansion. The Ericsson Mobility Report projects that global mobile data traffic will reach approximately 325 exabytes per month by 2028, an approximately fivefold increase from 2022 levels, driven by video streaming, cloud gaming, AI-powered applications, and the mass proliferation of connected devices.

The worldwide commercial deployment of 5G networks, with over 240 5G networks live globally, as reported by the GSMA, requires a massive expansion of wholesale backhaul and backbone capacity between operators. Simultaneously, hyperscale cloud providers, including Amazon Web Services (AWS), Microsoft Azure, and Google Cloud, are procuring wholesale interconnection capacity at unprecedented scale to interconnect global data center ecosystems, creating structural demand for wholesale data and fiber services.

Rapid Proliferation of IoT, Machine-to-Machine Connectivity, and Enterprise Digitalization

The global IoT and machine-to-machine (M2M) connectivity boom is generating substantial new wholesale telecom capacity requirements across carrier networks globally. The ITU and GSMA Intelligence estimate that the total number of IoT connections globally will surpass 25 billion by 2025 and continue scaling through the forecast period. Each connected device, including industrial sensors, smart meters, autonomous vehicles, and healthcare monitors, generates wholesale connectivity demand through carrier networks and MVNO (Mobile Virtual Network Operator) wholesale agreements.

Enterprise digitalization, accelerated by post-pandemic remote work and cloud migration, has dramatically expanded wholesale demand for SD-WAN, VPN, and cloud interconnect services. The World Economic Forum (WEF) estimates that digital transformation will add over US$ 100 trillion in value to the global economy by 2025, with telecom connectivity as a foundational enabler, reinforcing the demand trajectory for wholesale services.

Restraints - Price Erosion and Commoditization in Voice and Messaging Wholesale

Traditional voice and SMS wholesale services, which have historically accounted for a major share of wholesale telecom revenue, face structural and accelerating price erosion due to the rise of over-the-top (OTT) communication applications such as WhatsApp, Viber, and FaceTime.

The ITU has documented consistent year-on-year declines in international voice traffic termination rates. This commoditization compresses wholesale voice margins, forcing operators to absorb revenue losses in legacy services while simultaneously investing in higher-margin data and cloud wholesale, creating a revenue transition challenge that constrains near-term profitability.

Geopolitical Tensions and Regulatory Fragmentation Affecting Cross-Border Connectivity

The wholesale telecom market is increasingly exposed to geopolitical disruptions and regulatory fragmentation that create barriers to seamless cross-border capacity trading. Restrictions on submarine cable routes, national security reviews of foreign telecom investments, particularly scrutiny of Chinese telecom operators in Western markets under frameworks like the U.S. Team Telecom review process, and divergent data localization requirements across the EU, India, and China fragment the global wholesale connectivity market. These regulatory constraints increase compliance costs, delay infrastructure deployment, and complicate carrier-to-carrier wholesale agreements spanning multiple jurisdictions, thereby moderating the market's potential for globalization.

Opportunities - Hyperscale Data Center Interconnection and Cloud Wholesale Expansion

The explosive growth of hyperscale data centers globally represents the single most commercially significant near-term opportunity for wholesale telecom providers. The Synergy Research Group tracks over 900 hyperscale data centers in operation globally, with pipeline projects expected to more than double capacity by 2027. Each hyperscale facility requires massive, redundant wholesale connectivity, dark fiber, submarine cable capacity, internet exchange peering, and cloud interconnect services.

Tata Communications and NTT Communications have built wholesale portfolios specifically targeting cloud interconnection, while Arelion (formerly Telia Carrier) operates one of the world's most connected IP backbones. As AI workloads, requiring low-latency, high-bandwidth GPU cluster interconnection, scale globally, the demand for premium wholesale data center interconnect services is set to accelerate beyond current market projections.

Platform-Based Wholesale and API-Driven Communications (CPaaS)

The shift from legacy carrier wholesale to platform-based, API-accessible wholesale communications represents a structural transformation that creates substantial value-accretion opportunities for telecom operators and wholesale aggregators. Communications Platform as a Service (CPaaS) providers, including Sinch, Twilio, and Vonage (now part of Ericsson), are consuming wholesale voice, messaging, and connectivity capacity at massive scale via programmatic APIs.

The GSMA's Open Gateway initiative, which enables standardized API access to telecom network capabilities for developers, is catalyzing a new tier of platform-based wholesale demand. As enterprise customers increasingly consume communications as a digitally integrated service rather than a physical circuit, wholesale operators that develop robust API platforms and developer ecosystems can capture premium margins in a rapidly expanding addressable market.

Category-wise Analysis

By Service Type Insights

Data Wholesale is the dominant and fastest-growing service type segment, commanding approximately 42% of the wholesale telecom market. Data wholesale encompasses IP transit, Ethernet services, dark fiber leasing, internet exchange peering, and dedicated data circuits, the foundational connectivity layer for the internet economy. The ITU and Ericsson Mobility Report jointly document global internet traffic volumes growing at compound double-digit rates annually, driven by video streaming, cloud services, and AI workloads.

Every exabyte of internet traffic generates wholesale data capacity demand between carriers, cloud providers, and content networks. As legacy voice wholesale revenue contracts, data wholesale has become the primary revenue and growth engine for operators, including AT&T, Deutsche Telekom, and Arelion, cementing its market leadership position.

By Solution Insights

Cloud communication is the leading and fastest-growing solution segment, representing approximately 30% of total wholesale solution revenue. The enterprise shift to cloud-based unified communications, encompassing video conferencing, team messaging, contact center, and programmable voice/SMS APIs, has created an enormous wholesale consumption layer beneath the CPaaS and UCaaS platforms.

Microsoft Teams Direct Routing, Zoom Phone, and Cisco Webex all consume wholesale SIP trunking and carrier services at massive scale. The ITU notes that cloud communications adoption accelerated significantly post-2020, with enterprise unified communications cloud penetration now exceeding 50% in advanced markets. Wholesale operators that have built CPaaS-compatible API platforms, including Sinch and iBASIS, are capturing a disproportionate share of this high-growth segment.

By Network Infrastructure Type Insights

Fiber-optic networks are the dominant network infrastructure segment, accounting for approximately 48% of the wholesale telecom market by infrastructure type. Fiber optic infrastructure, encompassing terrestrial long-haul and metro fiber, dark fiber leasing, and submarine cable systems, underpins virtually all high-capacity wholesale data and voice traffic globally.

The GSMA and ITU both identify fiber as the foundational infrastructure for 5G backhaul, hyperscale data center connectivity, and enterprise broadband applications, all of which are growing rapidly. Dark fiber leasing has emerged as a particularly high-growth wholesale subsegment, as cloud providers and large enterprises opt to lease raw fiber capacity and operate their own optical networking equipment, driving demand from wholesale fiber operators such as Zayo Group and Lumen Technologies.

By Business Model Insights

Carrier-to-Carrier (C2C) is the dominant business model segment, representing approximately 38% of the wholesale telecom market. The C2C model, in which telecom operators exchange traffic, purchase transit capacity, and sell excess network resources to one another, forms the structural backbone of the global internet and PSTN interconnection ecosystem. Every international phone call, cross-border data packet, and roaming session involves at least one C2C wholesale agreement.

The International Telecommunications Union (ITU) and GSMA's Wholesale Carrier Interconnection guidelines govern the technical and commercial frameworks for C2C peering, transit, and interconnection. As 5G roaming agreements proliferate and operators expand international reach without building their own global networks, the C2C model continues to scale as the market's foundational revenue base.

By End-user Insights

Telecom operators remain the dominant end-user segment, accounting for approximately 45% of wholesale telecom demand. Mobile network operators (MNOs), fixed-line carriers, MVNOs, and internet service providers collectively represent the largest and most structurally stable buyers of wholesale voice, data, roaming, and interconnection services. The GSMA Intelligence reports over 800 MNOs operating globally, each requiring wholesale arrangements for international traffic termination, roaming coverage, and capacity overflow.

The expansion of 5G operator ecosystems, with new spectrum licensees requiring wholesale roaming during network build-out phases, is sustaining volume growth in this segment. While enterprise connectivity and data center cloud segments are growing faster, telecom operators' absolute revenue contribution remains dominant, given the sheer scale and volume of carrier-to-carrier traffic.

Regional Insights

North America Wholesale Telecom Market Trends & Analysis

North America leads the wholesale telecom market, contributing 39% of global revenue in 2026. Growth is driven by hyperscale cloud expansion, dense fiber infrastructure, and strong demand for IP transit and data center interconnection. Regulatory developments and broadband funding programs continue to expand wholesale fiber capacity and enterprise connectivity demand.

- U.S. Wholesale Telecom Market Size

The U.S. dominates the regional market, valued at approximately USD 85 billion in 2026, with a 5.6% CAGR. Growth is fueled by large-scale data center ecosystems, 5G backhaul demand, and increasing enterprise reliance on cloud connectivity, with strong wholesale offerings across fiber, Ethernet, and managed services.

- Europe Wholesale Telecom Market Trends, Drivers & Insights

Europe accounts for 28% of the global wholesale telecom market in 2026. The region is characterized by regulatory-driven infrastructure sharing, strong fiber rollout initiatives, and strong demand for cross-border connectivity. EU digital policies and 5G roaming frameworks are accelerating wholesale opportunities, particularly in enterprise networks and international transit services.

- Germany Wholesale Telecom Market Size

Germany’s market is estimated at USD 15 billion in 2026, growing at 4.5% CAGR. Demand is driven by industrial digitalization, private 5G networks, and strong enterprise connectivity requirements, supported by extensive fiber and wholesale infrastructure led by major telecom operators.

- U.K. Wholesale Telecom Market Size

The U.K. market is valued at around USD 13 billion in 2026, with a 5% CAGR. Growth is supported by regulated wholesale access frameworks, increasing fiber penetration, and strong demand for leased lines, broadband backhaul, and interconnection services across enterprises and service providers.

- France Wholesale Telecom Market Size

France’s wholesale telecom market is projected to reach USD 11 billion in 2026, expanding at a 4% CAGR. Growth is driven by nationwide fiber deployment, increasing international bandwidth demand, and strong wholesale participation in Europe-Africa connectivity corridors.

- Asia Pacific Wholesale Telecom Market Drivers & Analysis

Asia Pacific is the fastest-growing region, accounting for 33% of global market revenue in 2026 and posting a 7.9% CAGR. Growth is fueled by rapid digitalization, high mobile data consumption, expanding submarine cable networks, and aggressive 5G deployment across major economies.

- China Wholesale Telecom Market Size

China leads the region with an estimated market size of USD 55 billion in 2026 and a CAGR of 6.7%. Growth is supported by massive telecom infrastructure, government-led broadband expansion, and strong domestic demand for wholesale bandwidth and interconnection services.

- India Wholesale Telecom Market Size

India’s market is projected to reach USD 20 billion in 2026, growing at a 8.10% CAGR. Rapid data consumption, expanding fiber networks, and regulatory support for open access are driving wholesale demand, particularly for mobile backhaul, enterprise connectivity, and international bandwidth services.

- Japan Wholesale Telecom Market Size

Japan’s wholesale telecom market is estimated at USD 17 billion in 2026, with a 5.6% CAGR. Growth is driven by advanced 5G deployment, high enterprise digitalization, and strong demand for low-latency, high-capacity connectivity supporting cloud and IoT ecosystems.

Competitive Landscape

The wholesale telecom market exhibits a moderately consolidated structure at the global tier-1 level, dominated by national champions and global operators including AT&T, Deutsche Telekom, China Mobile, and Vodafone Group, while remaining highly fragmented at the regional and specialist level.

Market leaders differentiate through global network reach, submarine cable ownership, data center colocation portfolios, and API-driven platform capabilities. Key strategies include strategic acquisitions of fiber assets, investments in new submarine cable systems, and development of open API wholesale platforms aligned with GSMA's Open Gateway initiative. Emerging business model trends include wholesale-as-a-service, NaaS (Network-as-a-Service) pricing models, and embedded connectivity APIs enabling enterprise-grade wholesale access, reflecting the market's shift from circuit-based to software-defined commercial models.

Key Developments:

- March, 2025: Tata Communications expanded its IZO™ Multi-Cloud Connect platform to support direct cloud-to-cloud wholesale interconnection for enterprise customers across AWS, Azure, and Google Cloud, targeting the rapidly growing Carrier-to-Enterprise and data center interconnect wholesale segments.

- November, 2024: Sinch launched an expanded wholesale messaging and voice API platform targeting CPaaS providers and enterprise wholesale buyers, integrating an A2P SMS firewall, number intelligence, and real-time analytics to address growing enterprise demand for secure, compliant wholesale messaging services.

- June, 2024: Deutsche Telekom and Orange S.A. jointly announced the expansion of their cross-European wholesale fiber and IP transit peering agreements, creating an enhanced backbone connectivity pathway for enterprise and OTT wholesale customers across Central and Western Europe.

Wholesale Telecom Market- Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 306.2 Bn |

| Current Market Value (2026) | US$ 560.5 Bn |

| Projected Market Value (2033) | US$ 1200.9 Bn |

| CAGR (2026 - 2033) | 10.6% |

| Leading Region | North America, 37% share |

| Dominant Service Type | Data Wholesale, 42% share |

| Top-ranking End User | Telecom Operators, 45% |

| Incremental Opportunity | US$ 640.4 Bn |

Companies Covered in Wholesale Telecom Market

- AT&T

- Verizon Communications

- Deutsche Telekom

- Orange S.A.

- Telefónica

- Vodafone Group

- China Telecom

- China Unicom

- China Mobile

- Tata Communications

- BT Group

- NTT Communications

- Arelion

- iBASIS

- Sinch

- Lumen Technologies

- Zayo Group

- BICS

Frequently Asked Questions

The global Wholesale Telecom Market is estimated at US$ 560.5 Billion in 2026 and is projected to reach US$ 1,200.9 Billion by 2033, expanding at a CAGR of 11.5%. The market grew at a historical CAGR of 10.6% between 2020 and 2025, reflecting robust structural demand from global internet traffic growth, 5G network deployment, and enterprise cloud migration driving wholesale capacity procurement.

Key drivers include the Ericsson Mobility Report-projected fivefold increase in global mobile data traffic to 325 exabytes per month by 2028, the GSMA-reported deployment of over 240 commercial 5G networks requiring wholesale backhaul expansion, and the GSMA Intelligence-estimated 25 billion+ IoT connections by 2025 generating wholesale M2M connectivity demand at scale.

Data Wholesale is the dominant service type segment with approximately 42% market share, driven by the exponential growth of internet traffic, hyperscale cloud provider capacity procurement, and 5G backhaul requirements. Operators including AT&T, Deutsche Telekom, and Arelion have positioned data wholesale as their primary revenue and growth engine, reflecting the structural displacement of legacy voice wholesale revenue.

North America is the leading regional market, underpinned by the United States' role as the global internet backbone hub, the world's highest concentration of hyperscale data centers, and the wholesale network leadership of AT&T and Verizon Communications. The FCC's regulatory framework for wholesale interconnection, combined with North America's advanced cloud and enterprise digitalization ecosystem, sustains the region's market leadership through the forecast period.

The most compelling opportunity lies in hyperscale data center interconnection, with over 900 hyperscale facilities globally set to double by 2027 per Synergy Research Group, generating massive demand for dark fiber and cloud wholesale. Platform-Based Wholesale (CPaaS) represents a second major opportunity, driven by the GSMA Open Gateway initiative enabling standardized API access to wholesale network capabilities for enterprise and developer customers.

Market leaders include AT&T, Verizon Communications, Deutsche Telekom, China Mobile, Tata Communications, Orange S.A., Vodafone Group, NTT Communications, Arelion, and Sinch. These companies compete on global network reach, submarine cable ownership, data center colocation portfolios, API platform capabilities, and the ability to offer integrated wholesale solutions spanning voice, data, and cloud interconnect services.