- Pharmaceuticals

- Vitreous Detachment Treatment Market

Vitreous Detachment Treatment Market Size, Share, and Growth Forecast, 2026 - 2033

Vitreous Detachment Treatment Market by Treatment Type (Laser Therapy, Vitrectomy, Medication Treatments, Others), Patient Demographics (Age Group, Gender, Health Status, Lifestyle Factors), End User (Hospitals, Ophthalmic Clinics, Ambulatory Surgical Centers (ASCs), Others), and Regional Analysis for 2026 - 2033

Vitreous Detachment Treatment Market Share and Trends Analysis

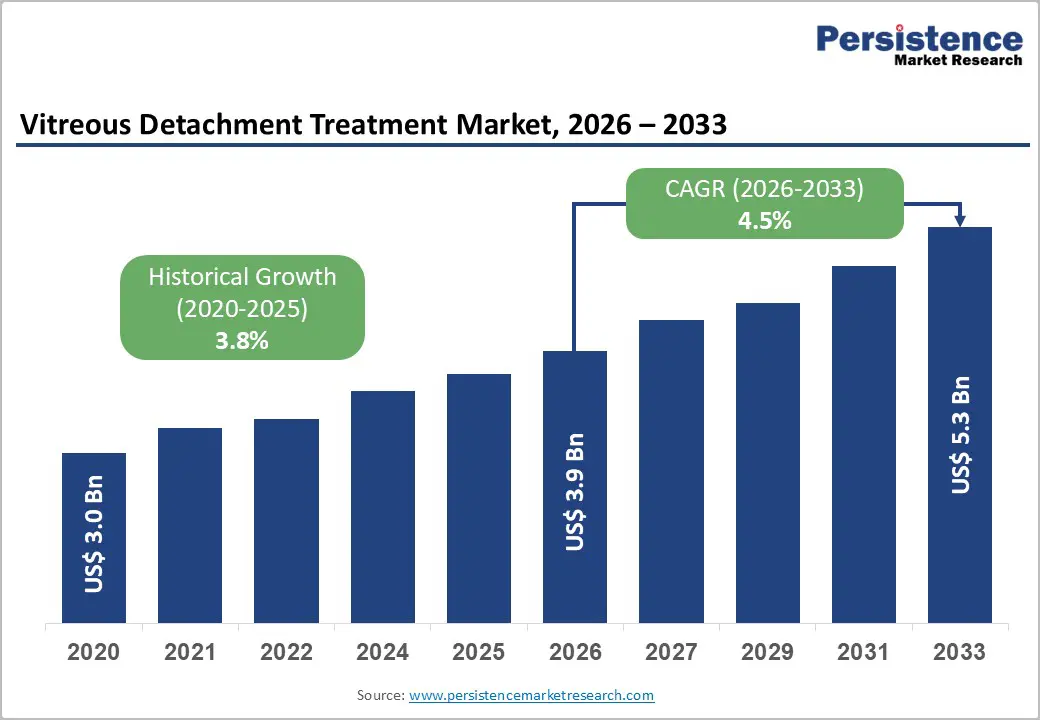

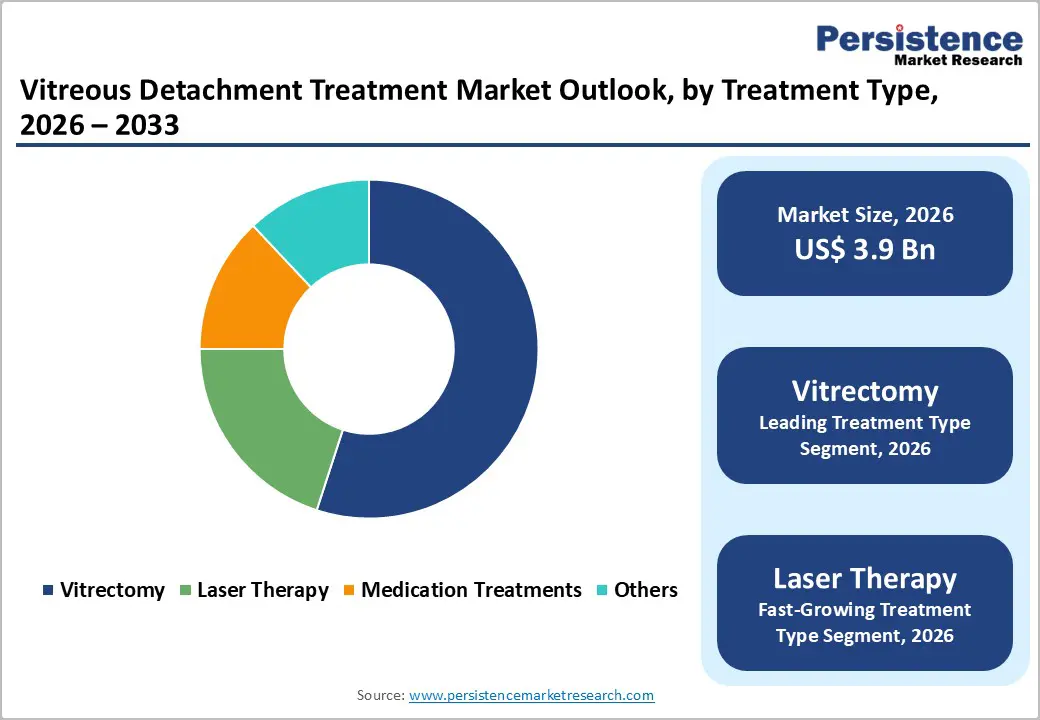

The global vitreous detachment treatment market size is likely to be valued at US$ 3.9 billion in 2026, and is projected to reach US$ 5.3 billion by 2033, growing at a CAGR of 4.5% during the forecast period 2026−2033. Aging populations, which have increased the prevalence of vitreous detachment and associated ocular disorders, are mainly driving market growth.

Rising clinical awareness among ophthalmologists and optometrists encourages early diagnosis and intervention, supporting adoption of advanced treatment modalities. Integration of laser technologies, minimally invasive vitrectomy procedures, and pharmacologic agents enhances treatment precision and patient outcomes. Expansion of healthcare infrastructure, particularly in urban and semi-urban regions, increases accessibility of ophthalmic services and specialized centers. Improved reimbursement policies and patient education campaigns contribute to demand by reducing barriers to treatment uptake.

Key Industry Highlights

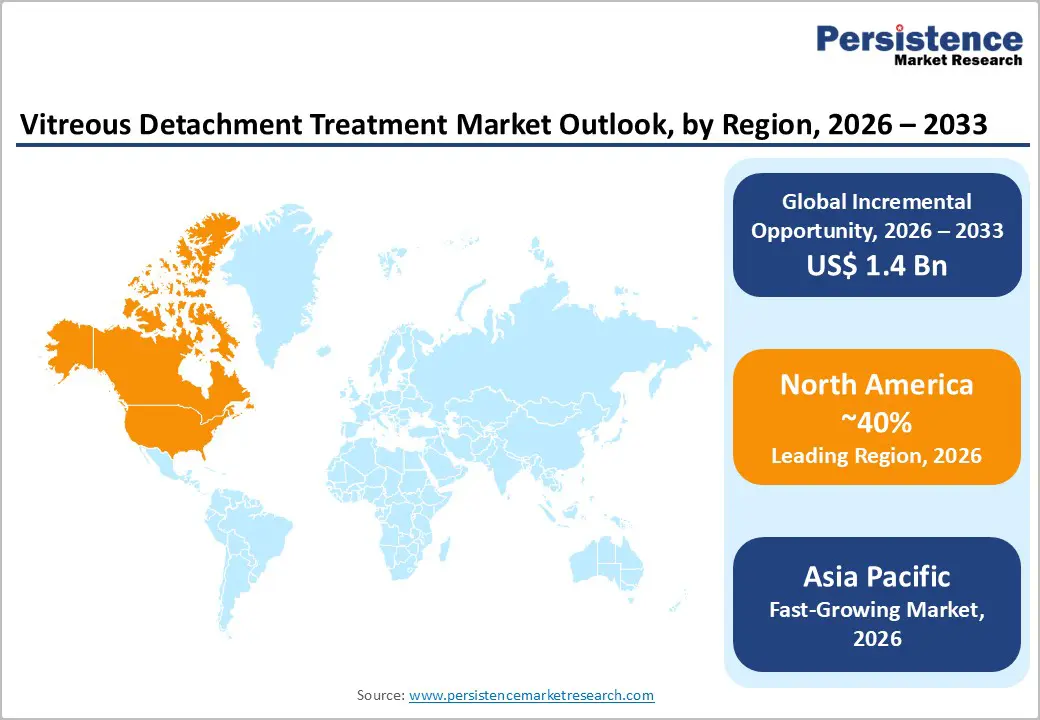

- Dominant Region: North America is anticipated to dominate with roughly 40% market share in 2026 due to its advanced healthcare and medical infrastructure.

- Fastest-growing Regional Market: Asia Pacific is expected to be the fastest-growing market during the 2026–2033 forecast period, on account of widening treatment adoption.

- Leading End-User: Vitrectomy is forecasted to lead in 2026 with around 55% revenue share, driven by its efficacy, precision, and broad clinical acceptance.

- Fastest-growing End-User: Laser therapy is projected to grow the fastest between 2026 and 2033, fueled by its minimally invasive nature and higher patient adherence.

| Key Insights | Details |

|---|---|

|

Vitreous Detachment Treatment Market Size (2026E) |

US$ 3.9 Bn |

|

Market Value Forecast (2033F) |

US$ 5.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.8% |

DRO Analysis

Aging Population and Increasing Prevalence of Vitreous Disorders

The progressive increase in older adult populations directly influences demand for clinical management of age?related vitreous changes. With advancing age, vitreous humor transitions from a gel?like to a more liquid state, weakening adhesion to the retina. This degeneration increases the likelihood of posterior vitreous detachment, particularly after age 50 and especially in individuals over 80. The U.S. National Eye Institute reports that vitreous detachment is very common in people over age 80. Age?related structural changes prompt higher clinical intervention rates to address symptomatic detachment and complications such as retinal tears or vision?disrupting floaters.

Global demographic trends reflect a growing elderly population, which raises the prevalence of vitreous disorders requiring medical attention. Older adults show higher incidence of vitreous degeneration and complications, increasing clinical demand for ophthalmic services. Age remains a key risk factor for detachment and vision impairment, necessitating advanced diagnostics and surgical interventions. This combination of demographic shift and physiological susceptibility strengthens the need for treatment pathways addressing vitreous changes. Health systems must allocate resources to manage increasing caseloads of age?linked ocular disorders and their associated visual consequences.

Technological Advancements in Treatment Modalities

Investment in next?generation diagnostic and surgical platforms is reshaping clinical intervention for vitreous separation disorders, supported by public health research and technology funding aimed at precision and efficiency. Government eye health resources note that high?resolution imaging and computer?assisted visualization are increasingly integrated into clinical workflows to detect and characterize vitreous changes earlier, informing decisions that align care pathways with individual patient profiles. Surgeons have greater control over vitrectomy procedures with smaller gauge instruments and real?time intraoperative imaging, which drives provider adoption of advanced systems that reduce procedural risk and improve throughput in high?volume practices. As of the December 2025 update, U.S. health agencies project that the number of people with visual impairment or blindness will double by 2050, signaling growing demand for effective vision?saving interventions.

Public health initiatives under the U.S. Department of Health and Human Services (HHS) focus on data?driven objectives that support eye health surveillance and the uptake of innovative modalities in clinical settings. National Vision and Eye Health Surveillance System data inform clinicians and policymakers on trends in vision loss and related conditions, enabling more efficient allocation of resources and prioritization of technology that can shorten diagnostic timelines and improve patient outcomes. Integration of tele?ophthalmology tools and advanced imaging in outpatient clinics enhances access to specialist support and workflows, driving volume adoption of next?generation care tools in both ambulatory and surgical environments.

Limited Insurance Coverage

Reimbursement policies play a critical role in shaping the vitreous detachment treatment market growth, with restrictive coverage affecting adoption rates. Insurers often categorize vitreous detachment procedures as elective, limiting payment for surgical and pharmacologic interventions. High out-of-pocket costs discourage patients from pursuing advanced treatment, particularly in regions with strict public insurance criteria. Healthcare providers may prioritize procedures with wider insurance acceptance, impacting investment in specialized equipment and training. Variations in private insurance reimbursement create market fragmentation, complicating the introduction of innovative therapies. This unpredictability reduces revenue certainty for manufacturers and service providers, affecting long-term strategic planning and market expansion.

Administrative barriers further influence treatment accessibility and market growth. Complex prior authorization processes and variable reimbursement rates delay patient access to advanced therapies. Insurers may require conservative management or step therapy before approving interventions, reducing procedure volumes. Small and mid-sized ophthalmology practices face financial exposure when offering treatments with uncertain coverage, shaping decisions on service provision and expansion. Geographic differences in insurance frameworks amplify disparities, with urban centers experiencing higher procedure adoption than rural areas.

Regulatory and Procedural Complexity

Stringent regulatory frameworks exert significant influence on the vitreous detachment treatment adoption, affecting product approvals, clinical evaluations, and market entry timelines. Medical devices, surgical tools, and pharmaceuticals undergo comprehensive assessment to ensure safety, performance, and compliance with both regional and international standards. Compliance requires extensive documentation, quality management audits, and inspections, which prolong approval cycles and increase operational costs. Smaller or new market entrants face additional challenges due to limited regulatory expertise. Differences in country-specific guidelines further complicate multi-regional expansion, requiring tailored strategies for each market and increasing barriers to entry.

Procedural requirements extend to clinical adoption, reimbursement, and operational practices within healthcare settings. Ophthalmology centers and hospitals follow detailed protocols, including preoperative evaluations, surgical procedures, and postoperative monitoring, to meet clinical and regulatory expectations. Insurance coverage criteria and payer policies impose constraints on patient access, affecting treatment uptake. Advanced training requirements for surgeons and support staff increase operational complexity, demanding investment in education and certification. Hospitals and clinics face resource allocation challenges, compliance monitoring, and adherence to procedural standards.

Emerging Markets with Expanding Healthcare Infrastructure

Government-led expansion of clinical facilities and specialist capacity in faster-growing economies strengthens accessibility and service delivery for complex eye interventions. India’s Ministry of Health and Family Welfare outlines targeted programs supporting rural and tertiary care infrastructure through initiatives such as the Pradhan Mantri Ayushman Bharat Health Infrastructure Mission, increasing public health units, critical care beds, and district laboratories across underserved regions up to FY?2025?26. Expanded infrastructure raises patient-throughput potential, facilitates integration of specialized ophthalmology services into broader care networks, and improves diagnostic and treatment access for retinal and vitreous conditions in regions with previously limited availability.

Fast-evolving healthcare systems in Asia and Latin America attract investment and support scaled delivery of ophthalmology services. National commitments to expand facilities and workforce capacity in these regions increase diagnostic volumes and procedural adoption, aligning clinical supply with rising demand from ageing populations. By standardizing and expanding health facilities, government systems improve referral pathways to advanced treatment centers, enabling earlier detection and management of vitreous disorders. Public sector expansion of infrastructure and workforce capacity creates opportunities for private providers and equipment manufacturers to deploy advanced solutions across growing networks of accessible care points.

Integration of Digital Health and Teleophthalmology

Digital health technologies and tele?ophthalmology unlock capacity and precision in clinical workflows, enabling remote specialist consultation, asynchronous diagnostic review, and continuous patient monitoring with minimal need for physical interaction. This model moves care out of centralized hospital settings into distributed points of service, in which primary care clinics capture fundus images, optical coherence tomography (OCT) scans, and symptom data for specialist interpretation digitally, reducing bottlenecks created by specialist shortages and geographic constraints. Telemedicine programs in large health systems improved disease detection in populations at risk for retinal conditions. Real?time digital data supports remote treatment adjustments and structured follow?ups that traditional episodic in?person appointments struggle to deliver in a scalable fashion.

Data from the U.S. Centers for Medicare & Medicaid Services (CMS) shows that about 10.8% of eligible Medicare beneficiaries received care via telehealth in the second quarter of 2025, a share notably higher than pre?pandemic usage.? Digital integration yields operational efficiencies in diagnostic throughput, reduces travel?related costs and time burdens for patients, and expands the reach of scarce retinal specialists into underserved and rural areas. Continuous remote monitoring generates real?world evidence that supports risk stratification and informed allocation of clinical resources throughout the care continuum, enhancing quality measures and clinical decision?making across distributed care environments.

Category-wise Analysis

Treatment Type Insights

Vitrectomy is likely to capture approximately 55% of the vitreous detachment treatment market revenue share in 2026, aided by its broad clinical acceptance and proven efficacy in managing advanced vitreous detachment. Surgical precision allows ophthalmologists to address complications such as retinal tears, hemorrhage, or tractional detachments, directly improving visual outcomes and reducing long-term morbidity. Hospitals and specialized clinics prefer vitrectomy because it minimizes the frequency of follow-up visits compared to conservative or pharmacologic approaches. Innovations including microincision vitrectomy, advanced illumination systems, and high-speed cutters enhance procedural safety, reduce operative time, and shorten recovery periods. Standardized training programs and experienced vitreoretinal surgeons reinforce provider preference and drive adoption consistently across regions.

Laser therapy is expected to witness the fastest growth between 2026 and 2033, as minimally invasive procedures gain preference among patients and ophthalmologists. Advancements in yttrium-aluminum-garnet (YAG) and neodymium-doped YAG laser systems allow precise vitreolysis, minimizing complications and eliminating the need for extended hospital admission while lowering overall costs. Adoption is also increasing in ambulatory surgical centers (ASCs) and outpatient clinics due to reduced infrastructure requirements and simplified workflows. Integration with imaging technologies such as OCT improves targeting accuracy, enhances patient confidence, and increases adherence. Early-stage recommendations expand the eligible patient population, accelerating revenue growth during the forecast period.

End-User Insights

Hospitals are positioned to dominate with nearly 50% of the market revenue share in 2026, supported by clinical credibility and access to advanced surgical facilities. Full-service hospitals provide integrated ophthalmic departments, including laser systems and vitrectomy units, facilitating complex case management. Physician referral networks enhance patient inflow, while comprehensive care models allow management of pre- and post-procedure follow-up. Investment in digital health and diagnostic equipment strengthens operational efficiency and procedural throughput. Hospitals also benefit from insurance reimbursement infrastructure, reducing financial barriers for patients and supporting stable revenue streams.

Ambulatory surgical centers are expected to emerge as the fastest-growing segment between 2026 and 2033, driven by cost efficiency and procedural convenience. Minimally invasive laser therapy and microincision vitrectomy are increasingly performed in outpatient settings, reducing hospital admission costs and recovery time. Patient preference for shorter treatment duration and lower procedural fees enhances adoption. ASCs leverage digital appointment scheduling, teleconsultation, and patient education platforms to expand accessibility. Growth is also supported by partnerships with insurance providers and local ophthalmology networks, creating scalable revenue opportunities in the outpatient care segment.

Regional Insights

North America Vitreous Detachment Treatment Market Trends

North America is expected to lead with an estimated 40% of the vitreous detachment treatment market share in 2026, supported by advanced clinical infrastructure and a dense network of ophthalmic centers. Well-structured referral systems enable timely diagnosis and intervention, increasing adoption of both surgical and minimally invasive procedures. High procedure volumes in hospitals and specialized clinics contribute to operational efficiency and consistent revenue generation. Integration of microincision vitrectomy, YAG and Neodymium-doped YAG laser systems, and OCT imaging improves procedural precision, reduces complications, and shortens recovery periods. Reimbursement frameworks facilitate access to advanced treatments across diverse patient populations.

North America benefits from a concentrated presence of trained retinal specialists and standardized training programs that maintain procedural quality and optimize patient outcomes. Collaborative research between academic institutions, medical device manufacturers, and clinical networks accelerates adoption of new technologies. Increasing prevalence of age-related vitreoretinal conditions drives demand for both vitrectomy and laser-based solutions. Outpatient facilities and ambulatory surgical centers enhance procedural scalability while lowering operational costs. Patient awareness campaigns and early screening programs increase detection rates, expand eligible patient populations, and strengthen adoption of advanced therapies across clinical settings.

Europe Vitreous Detachment Treatment Market Trends

Europe is projected to maintain a significant position in the market for vitreous detachment treatment through 2033, driven by advanced healthcare infrastructure and a dense network of specialized ophthalmic centers. Rising prevalence of age-related vitreoretinal disorders and an aging population sustains demand for surgical and minimally invasive procedures. Adoption of high-resolution fundus imaging and OCT enables early detection and precise treatment planning. Integration of microincision vitrectomy and laser systems improves procedural safety, reduces recovery time, and increases patient throughput. Standardized training programs and availability of experienced retinal specialists ensure consistent adoption across hospitals and outpatient clinics.

Emerging reimbursement policies and public-private partnerships enhance accessibility and affordability of advanced treatments, encouraging adoption in urban and semi-urban areas. Expansion of ambulatory surgical centers and outpatient clinics reduces procedural delays while improving operational efficiency. Targeted awareness campaigns and early screening initiatives increase patient detection rates and engagement with treatment options. Collaborations between academic institutions and medical device companies drive innovation and introduction of next-generation surgical tools. Focus on patient-centered care, combined with investment in telemedicine and remote monitoring, strengthens follow-up, generates real-world data, and supports revenue growth within established healthcare systems.

Asia Pacific Vitreous Detachment Treatment Market Trends

Asia Pacific is forecasted to be the fastest-growing market for vitreous detachment treatment between 2026 and 2033, stimulated by expanding healthcare infrastructure and growing patient awareness in urban and semi-urban areas. China demonstrates strong growth due to increased investment in specialized ophthalmic centers and rising prevalence of age-related vitreoretinal conditions. India shows accelerated adoption driven by expanding outpatient clinics, improved insurance coverage, and rising disposable income. Access to minimally invasive procedures, including vitrectomy and laser therapy, extends treatment reach. Government initiatives promoting vision care and the development of trained retinal specialists support higher procedural volume and overall market expansion.

Japan exhibits growth supported by advanced medical technology adoption and widespread outpatient surgical facilities. South Korea contributes through microincision vitrectomy and advanced laser systems, improving procedural efficiency and patient safety. Expanded patient screening programs enhance early detection, increasing the eligible population for surgical and minimally invasive interventions. Collaboration between academic institutions and medical device companies accelerates clinical research and technology dissemination. Private sector investment in ophthalmology services strengthens infrastructure and procedural capacity. Rising urban middle-class populations prioritize eye health, driving demand for advanced treatments and accelerating revenue growth across clinical networks.

Competitive Landscape

The global vitreous detachment treatment market structure is moderately fragmented, with several multinational and regional ophthalmic device manufacturers competing for share. Key players include Johnson & Johnson Vision, Bausch + Lomb, Alcon, Carl Zeiss Meditec, Nidek, and Topcon. Hospitals, ophthalmic clinics, and ambulatory surgical centers drive demand for advanced laser systems and vitrectomy technologies. Market concentration is higher in North America and Europe due to established clinical infrastructure, experienced specialists, and strong regulatory frameworks that support adoption of innovative treatment solutions.

New entrants focus on technology-driven offerings, including minimally invasive vitrectomy systems and precision laser platforms, to differentiate service portfolios. Competitive strategies emphasize innovation, treatment efficacy, and comprehensive clinical support services to attract ophthalmologists and patients. Strategic collaborations with healthcare providers, research institutions, and device distributors enable wider market penetration. Continuous development of high-precision surgical tools strengthens competitive positioning and ensures alignment with evolving patient needs and procedural standards.

Key Industry Developments

- In October 2025, researchers at Würzburg University Hospital reported progress on developing biohybrid hydrogel vitreous body replacements aimed at offering a better?tolerated substitute for current gases and silicone oils used in eye surgery that can cause complications and require additional operations.

- In September 2025, BVI Medical introduced Virtuoso®, a next-generation dual-function surgical platform that combines phacoemulsification and vitrectomy capabilities in a single system for cataract and retinal procedures. The platform integrates advanced fluidics, ultrasound, and cutting technologies to improve surgical control, efficiency, and versatility.

- In April 2025, Pykus Therapeutics completed enrollment of its pilot clinical trial evaluating PYK-2101, a biodegradable retinal hydrogel sealant for treating retinal detachment. The therapy aims to improve surgical outcomes by sealing retinal breaks without gas or oil, potentially eliminating post-surgery face-down positioning.

Companies Covered in Vitreous Detachment Treatment Market

- Johnson & Johnson Vision

- Bausch + Lomb

- Alcon

- Carl Zeiss Meditec

- Nidek

- Topcon

- Hoya Surgical Optics

- Ellex Medical Lasers

- Optos

- STAAR Surgical

- Heidelberg Engineering

- Rayner

- Haag-Streit

- MediWorks

Frequently Asked Questions

The global vitreous detachment treatment market is projected to reach US$ 3.9 billion in 2026.

Rising prevalence of age-related eye disorders, advanced surgical and laser technologies, and increasing patient awareness are driving the market.

The market is poised to witness a CAGR of 4.5% from 2026 to 2033.

Integration of digital health, tele‑ophthalmology, and minimally invasive treatment solutions can open novel market opportunities.

Some of the key market players include Johnson & Johnson Vision, Bausch + Lomb, Alcon, Carl Zeiss Meditec, Nidek, and Topcon.