- Plastics, Polymers & Resins

- U.S. Plastic Resin Market

U.S. Plastic Resin Market Size, Share, and Growth Forecast, 2026 - 2033

U.S. Plastic Resin Market by Resin Type (Thermoplastic (Polyethylene (PE), Polypropylene (PP), Polyvinyl Chloride (PVC), Polyethylene Terephthalate (PET), Polystyrene (PS), Engineering Plastics), Thermosetting Resins (Epoxy Resins, Phenolic Resins, Unsaturated Polyester Resins (UPR), Polyurethane (PU) Resins) Industry (Packaging (Flexible Packaging, Rigid Packaging), Building & Construction, Automotive, Electrical & Electronics, Consumer Goods, Healthcare & Medical, Agriculture, Textiles & Fibers), and Regional Analysis for 2026 - 2033

U.S. Plastic Resin Market Size and Trends Analysis

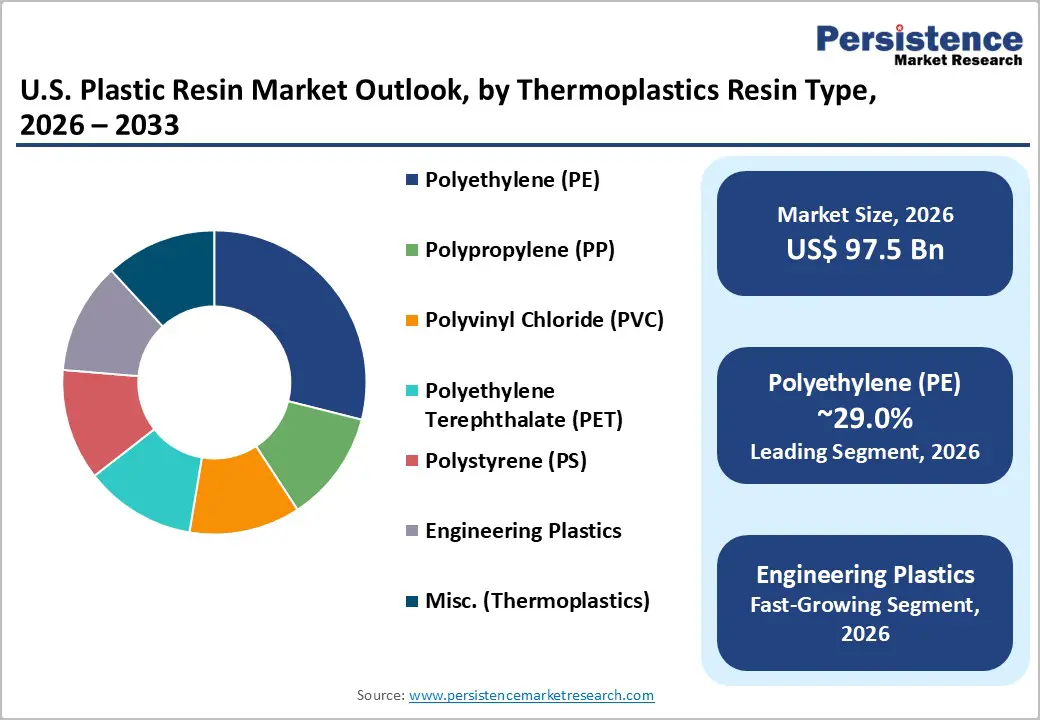

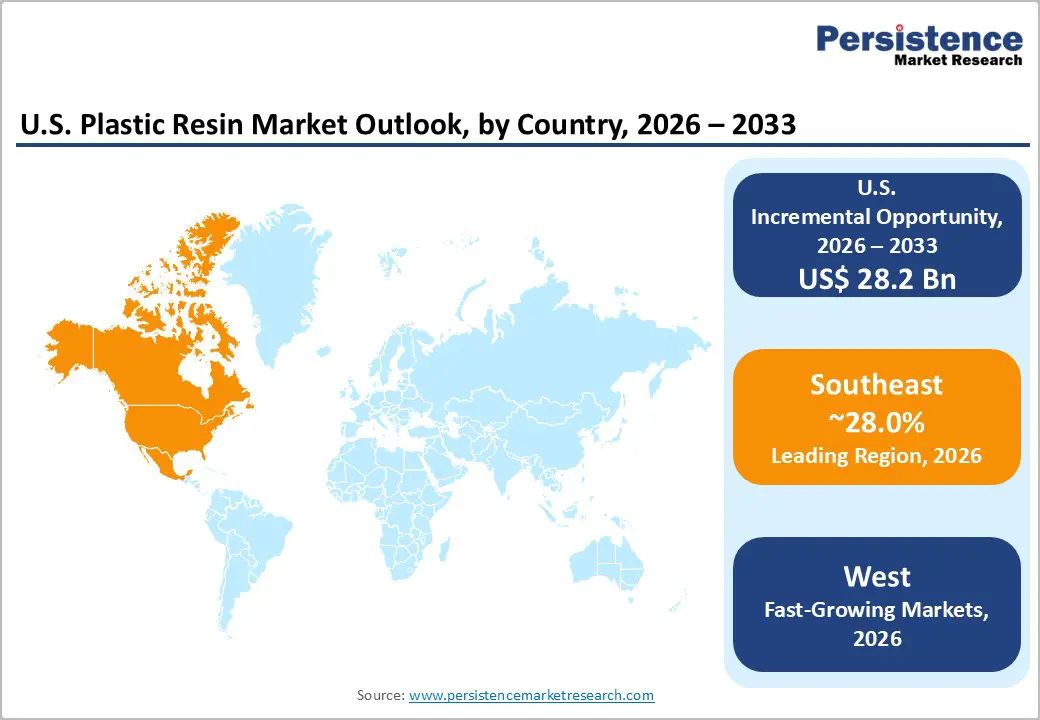

The U.S. plastic resin market size is likely to be valued at US$ 97.5 billion in 2026 and is projected to reach US$ 125.7 billion by 2033, growing at a CAGR of 3.7% between 2026 and 2033. The market recorded a historical value of US$ 79.9 Bn in 2020, reflecting a historical CAGR of 3.3% a steady trajectory driven by sustained demand from packaging, construction, healthcare, and automotive sectors.

According to the American Chemistry Council (ACC), cumulative year-to-date plastic resin sales and captive use reached 103.3 billion pounds in 2025, up 1.8% from the prior year, signaling modest but durable underlying demand resilience. Meanwhile, year-to-date production through 2025 stood at 102.2 billion pounds, essentially flat relative to 2024, reflecting market stabilization rather than contraction. The transition toward recycled-content and bio-based resins, combined with end-use demand from medical and electric mobility applications, continues to channel investment into both commodity and specialty resin segments across the domestic value chain.

Key Industry Highlights:

- Packaging Leads Demand: The Packaging segment dominates with 34% market share in 2026, driven by e-commerce growth and flexible/rigid polyethylene, PET, and polypropylene formats.

- Polyethylene Dominance: PE holds 29% of the total resin market, supported by versatile applications in packaging, construction, and consumer goods, with Gulf Coast production hubs ensuring supply stability.

- Fastest-Growing Resin Segment: Polyurethane (PU) resins are expanding rapidly, driven by automotive, insulation, and personal care applications requiring rigid and flexible foams.

- Healthcare as Growth Engine: Medical and healthcare end-use is the fastest-growing category, fueled by rising healthcare spending, single-use devices, and advanced specialty resins like PEEK, polyamide, and PET.

- Sustainability & Circular Economy: Development of post-consumer recycled (PCR) and advanced chemically recycled resins, such as Chevron Phillips’ Marlex® Anew™, is enabling compliance with U.S. Plastics Pact and regulatory mandates.

- Regional Supply Strength: The U.S. Gulf Coast and Texas lead domestic resin production, exemplified by Formosa’s 550-million-pound polypropylene reactor, ensuring resilience against import and trade policy uncertainty.

- Market Drivers & Opportunities: Packaging demand, automotive lightweighting for EVs, infrastructure-driven PVC and engineering resin consumption, and advanced recycling technologies collectively sustain multi-year growth opportunities.

| Key Insights | Details |

|---|---|

| U.S. Plastic Resin Market Size (2026E) | US$ 97.5 Bn |

| Market Value Forecast (2033F) | US$ 125.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 3.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.3% |

Market Dynamics

Drivers - Sustained Demand from Packaging Sector and E-Commerce-Driven Consumption Patterns

The packaging sector remains the single most consequential demand driver for the U.S. Plastic Resin Market, anchored by the structural permanence of both flexible and rigid packaging formats across food, beverage, personal care, and industrial distribution channels. The structural shift toward e-commerce over the past decade has materially elevated per-unit packaging intensity, as transit-ready protective packaging relies heavily on polyethylene and polypropylene-based resins.

The U.S. Plastics Pact's Roadmap to 2025 has set a target of 100% of plastic packaging being reusable, recyclable, or compostable, and a minimum recycling rate of 50% for packaging on the U.S. market, which has channeled investment into recyclable-grade resin development. Dow, Inc. introduced a portfolio of post-consumer recycled (PCR) resins for flexible and rigid packaging applications in 2025, delivering a 20 to 30 percent reduction in carbon and energy footprints relative to virgin materials, directly enabling brand owners to comply with sustainability mandates.

These developments collectively reinforce multi-year resin procurement cycles within the packaging supply chain, sustaining volume and value growth in the U.S. Plastic Resin Market.

Automotive Lightweighting Mandates and Specialty Resin Adoption for Electric Mobility

Automotive lightweighting imperatives, driven by federal fuel economy and emissions standards, are generating sustained demand for engineering-grade thermoplastics and specialty resins across the U.S. Plastic Resin Market. The U.S. Department of Energy has documented that a 10 percent reduction in vehicle weight translates to a 6 to 8 percent improvement in fuel economy, establishing a quantitative basis for OEM material substitution strategies that prioritize high-performance polymer systems over traditional metals.

The National Highway Traffic Safety Administration (NHTSA) maintains stringent Corporate Average Fuel Economy (CAFE) standards that compel automakers to adopt advanced polymer solutions across structural, under-hood, and interior applications. The transition to electric vehicles (EVs) further amplifies this dynamic, as battery enclosures, thermal management components, and high-voltage insulation systems that require specialty resins including polyamide, polycarbonate, and polyethylene terephthalate. SABIC showcased innovations at K 2025 including MEGAMOLDING™ for large thermoplastic automotive components and BLUEHERO™ for EV battery systems, signaling the commercialization of high-value specialty resin solutions targeting the domestic electric mobility supply chain.

Infrastructure Investment and Construction Sector Demand for PVC and Engineering Resins

Construction-sector demand for plastic resins encompassing PVC for pipes, conduits, and profiles, as well as polyurethane for insulation, sealants, and structural foams is directly linked to U.S. federal and state-level infrastructure investment programs. The U.S. Infrastructure Investment and Jobs Act, enacted in 2021 with a total commitment of US$ 1.2 trillion, continues to channel capital into water systems, transportation infrastructure, and broadband network buildout, all of which require substantial volumes of PVC and engineering plastic components. Additionally, the residential construction market sustained elevated activity through 2024 and into 2025, supported by housing demand driven by demographic trends.

Formosa Plastics Corporation, U.S.A. commissioned the largest horizontal polypropylene reactor in North America at its Point Comfort, Texas facility in September 2025, with an annual capacity of 550 million pounds, producing a full slate of PP resins for construction, consumer goods, automotive, and specialty applications a direct supply-side response to sustained domestic construction and industrial demand within the U.S. Plastic Resin Market.

Restraint - Regulatory and Environmental Pressure on Single-Use and Virgin Plastic Applications

Regulatory scrutiny around single-use plastics and fossil-derived virgin resins represents a material structural restraint in the U.S. Plastic Resin Market. The U.S. Plastics Pact has set a target requiring at least 30% recycled content in plastic packaging by 2030, and bipartisan legislation introduced in 2024 seeks to establish national plastics recycling standards across more than 9,000 jurisdictions that currently operate conflicting recycling frameworks.

Currently, post-consumer recycled content in packaging averages only 11% across the U.S. Plastics Pact's network of 135 Activators, far below the 2025 target of 30%, signaling the gap between regulatory ambition and current supply-chain capability. These mandates elevate compliance costs for producers and converters reliant on commodity virgin resins.

Feedstock Price Volatility and Trade Policy Uncertainty Affecting Supply Economics

Feedstock cost volatility stemming from crude oil, natural gas, and propylene price fluctuations continues to compress margins and introduce supply-chain planning uncertainty for resin producers. U.S. polypropylene experienced monthly price shifts throughout 2024 due to propylene supply-demand imbalances before stabilizing in the first half of 2025.

The imposition of a 25% tariff on South Korean imports in 2025 introduced sourcing uncertainty for converters dependent on Asian resin supply, while proposed tariffs on Canadian material though not price-impactful due to USMCA provisions added procurement complexity. Imports account for only 4.1% of total U.S. PP supply in 2025, down from 4.7% in 2024, indicating domestic production dominance, yet global trade policy shifts continue to create operational risk for the U.S. Plastic Resin Market.

Opportunity - Advanced Recycling Technologies and Circular Plastic Economy Policy Incentives

Advanced recycling encompassing chemical depolymerization, pyrolysis, and solvolysis represents a transformative opportunity to convert end-of-life mixed-waste plastics into virgin-equivalent resins, unlocking circular supply chains that comply with both regulatory mandates and corporate sustainability commitments within the U.S. Plastic Resin Market. This opportunity is particularly significant given that current mechanical recycling infrastructure in the U.S. cannot fully address the scale and material diversity of post-consumer plastic waste.

Chevron Phillips Chemical achieved the first commercial-scale production of circular polyethylene from recycled mixed-waste plastics in the U.S. under the Marlex® Anew™ brand, demonstrating that performance parity with virgin polymers is technically achievable through advanced recycling routes. In February 2026, Lummus Technology in partnership with Sumitomo Chemical launched commercial PMMA chemical recycling technology capable of depolymerizing end-of-life PMMA into high-purity MMA monomer, reducing lifecycle emissions by 50% and enabling fully closed-loop recycling.

The bipartisan Plastics Recycling Act proposed in 2024 would mandate 30% recycled content in packaging by 2030, creating a compliance-driven demand signal for advanced-recycled resins. These converging policy and technology vectors position advanced recycling capacity as one of the highest-value investment themes in the near-term U.S. Plastic Resin Market landscape.

Healthcare Sector Demand for Specialty Medical-Grade and Biocompatible Resins

The healthcare and medical end-use segment represents one of the most structurally attractive growth opportunities for specialty resin producers in the U.S. Plastic Resin Market, driven by aging demographics, expanded healthcare infrastructure investment, and the accelerating adoption of single-use medical devices, biodegradable implants, and advanced packaging for pharmaceutical products. This opportunity is distinct from commodity resin demand, as medical applications require biocompatibility, sterilization resistance, and regulatory approval from the U.S. Food and Drug Administration (FDA), creating high barriers to entry and premium pricing.

According to the Centers for Medicare and Medicaid Services (CMS), healthcare spending in the United States was projected to reach US$ 4.3 trillion, equivalent to US$ 12,914 per person, with multi-year expenditure growth supporting sustained procurement of medical-grade plastic components. The FDA's clearance of the first 3D-printed PEEK cranial implant in 2024 validated additive manufacturing for permanent implants, opening a new frontier for high-performance engineering resins in patient-specific medical applications.

Eastman received RecyClass Recyclability Approvals for eight of its specialty PET resins in January 2025, including Renew grades with recycled content, reinforcing the dual mandate for performance and sustainability in medical-grade resin procurement. For specialty resin producers positioned in polyamide, PET, polycarbonate, and biopolymer segments, the healthcare vertical offers high-value, regulation-protected demand anchors within the broader U.S. Plastic Resin Market.

Category-wise Analysis

Design Insights

Polyethylene (PE) holds the leading position within the Thermoplastic resin category and the overall U.S. Plastic Resin Market, commanding approximately 29% of total resin-type market share in 2026. PE's dominance is rooted in its unmatched versatility across packaging, agriculture, construction, and consumer goods applications, where HDPE, LDPE, and LLDPE variants are deployed across an enormous range of product formats from bottles and films to pipes and geomembranes.

The American Chemistry Council (ACC) consistently identifies polyethylene as the highest-volume resin in its monthly production tracking, with domestic output reflecting the concentrated production infrastructure along the U.S. Gulf Coast. Chevron Phillips Chemical's commercial launch of Marlex® Anew™ Circular Polyethylene the first commercial-scale circular PE from recycled mixed-waste plastics in the U.S. demonstrates that the segment is also at the forefront of circular economy innovation, which will sustain its demand relevance even as regulatory pressure on virgin plastics intensifies across the domestic market.

Polyurethane (PU) Resins represent the fastest-growing segment within the Thermosetting Resin category, driven by broad and accelerating demand across insulation, automotive seating, adhesives, coatings, and nonwoven hygiene applications. PU's functional versatility spanning rigid and flexible foams, elastomers, and coatings make it irreplaceable in high-value application segments that intersect construction energy efficiency, automotive comfort systems, and personal care.

Carrying Capacity Insights

The packaging segment leads all end-use categories in the U.S. Plastic Resin Market, holding approximately 34 percent of total market share in 2026, encompassing both flexible packaging formats including films, pouches, and wraps and rigid packaging formats such as bottles, trays, containers, and crates. Packaging's structural primacy reflects the fundamental role of plastic resins as the enabling material for food safety, product preservation, and transportation efficiency across the consumer goods supply chain.

The U.S. Plastics Pact, operating through a network of 135 Activators, has set a target of 100% of plastic packaging being reusable, recyclable, or compostable, which is driving investment in recyclable-grade polyethylene, PET, and polypropylene resins. Dow's 2025 portfolio of PCR resins for flexible and rigid packaging delivering 20 to 30 percent lower carbon and energy footprints versus virgin material exemplifies the innovation response to sustainability mandates that is keeping resin demand robust within packaging even as brands shift toward circular content requirements.

The Healthcare and Medical segment is the fastest-growing end-use category in the U.S. Plastic Resin Market, supported by rising healthcare expenditure, demographic aging, expanded single-use device adoption, and the integration of advanced engineering resins into implantable and wearable medical technologies. The CMS projected U.S. healthcare spending to exceed US$ 4.3 trillion, creating sustained, non-discretionary demand for medical-grade plastic components across diagnostics, surgical devices, pharmaceutical packaging, and laboratory consumables.

Competitive Landscape

The U.S. plastic resin market is largely consolidated, dominated by a handful of major players that control a significant portion of domestic production capacity. Leading companies such as Dow, LyondellBasell Industries, Chevron Phillips Chemical, Formosa Plastics Corporation, BASF Corporation, and Eastman Chemical Company hold strong positions across key types including polyethylene (PE), polypropylene (PP), and PET. These players benefit from extensive manufacturing infrastructure, advanced technology platforms, and well-established distribution networks, allowing them to meet the diverse demands of packaging, automotive, construction, and consumer goods sectors.

Market competition is primarily based on product quality, technological innovation, sustainability initiatives, and pricing strategies, with companies increasingly investing in recycled resins and circular economy solutions to meet regulatory and consumer-driven sustainability requirements. Smaller regional producers exist but have limited influence due to scale, making market entry challenging for new participants. Consolidation is further reinforced by strategic expansions and capacity upgrades, such as Formosa’s new polypropylene reactor in Texas and Dow’s developments in post-consumer recycled resins.

Key Industry Developments:

- In September 2025, Formosa Plastics Corporation, U.S.A., commissioned the largest horizontal polypropylene reactor in North America at its Point Comfort, Texas facility, with an annual capacity of 550 million pounds. The new line, using advanced JPP technology, produces a full slate of high-quality polypropylene resins including homopolymer, random copolymer, and impact copolymer supporting key U.S. markets such as consumer goods, industrial packaging, automotive, and specialty applications. This expansion enhances domestic polypropylene supply, strengthens the U.S. plastic resin market, and is expected to generate approximately sixty new local jobs while improving production flexibility and supply chain reliability.

- In September 2024, Dow launched REVOLOOP™ Recycled Plastics Resins incorporating post-consumer recycled (PCR) content for cable jacketing applications, expanding circular polymer solutions within the U.S. plastic resin market. Introduced from Midland, Michigan, the product line enables power and telecommunications manufacturers to integrate recycled content without compromising performance, reinforcing sustainability-driven resin demand in the U.S. wire and cable sector. The development strengthens Dow’s circular plastics portfolio and supports the broader transition toward recycled-content resins across domestic industrial and infrastructure applications.

Companies Covered in U.S. Plastic Resin Market

- BASF SE

- SABIC

- Dow

- DuPont de Nemours, Inc.

- Evonik Industries AG

- Sumitomo Chemical Co., Ltd.

- Celanese Corporation

- Eastman Chemical Company

- Chevron Phillips Chemical Co., LLC

- LOTTE Chemical Corporation

- Exxon Mobil Corporation

- Formosa Plastics Corporation

- TORAY INDUSTRIES, INC.

- MITSUI & CO. LTD

- TEIJIN LIMITED

- LG Chem

Frequently Asked Questions

The U.S. plastic resin market is projected to be valued at US$ 97.5 Bn in 2026.

The Polyethylene (PE) segment is expected to account for approximately 29.0% of the U.S. Plastic Resin Market by Design in 2026.

The U.S. plastic resin market is expected to witness a CAGR of 3.7% from 2026 to 2033.

The U.S. Plastic Resin Market growth is primarily driven by sustained demand from the packaging sector fueled by e-commerce, automotive lightweighting and EV adoption requiring specialty resins, and construction/infrastructure investments boosting PVC and engineering resin consumption.

Key opportunities in the U.S. Plastic Resin Market lie in advanced recycling technologies enabling circular plastics and in high-value specialty medical-grade resins driven by healthcare demand and regulatory mandates.

Key players in the Plastic Resin Market include Dow, LyondellBasell Industries, Chevron Phillips Chemical, Formosa Plastics Corporation, BASF Corporation, and Eastman Chemical Company.