- Hardware & Software IT Services

- Task Management Software Market

Task Management Software Market Size, Share, and Growth Forecast, 2026 - 2033

Task Management Software Market by Offering (Solution, Services), Deployment (Cloud-based / SaaS, On-premises, Hybrid), Application (Project Planning & Scheduling, Task Tracking & Monitoring, Workload & Resource Management, Time Tracking, Communication, Reporting & Analytics, Others), Industry and Regional Analysis for 2026 - 2033

Task Management Software Market Size and Trends

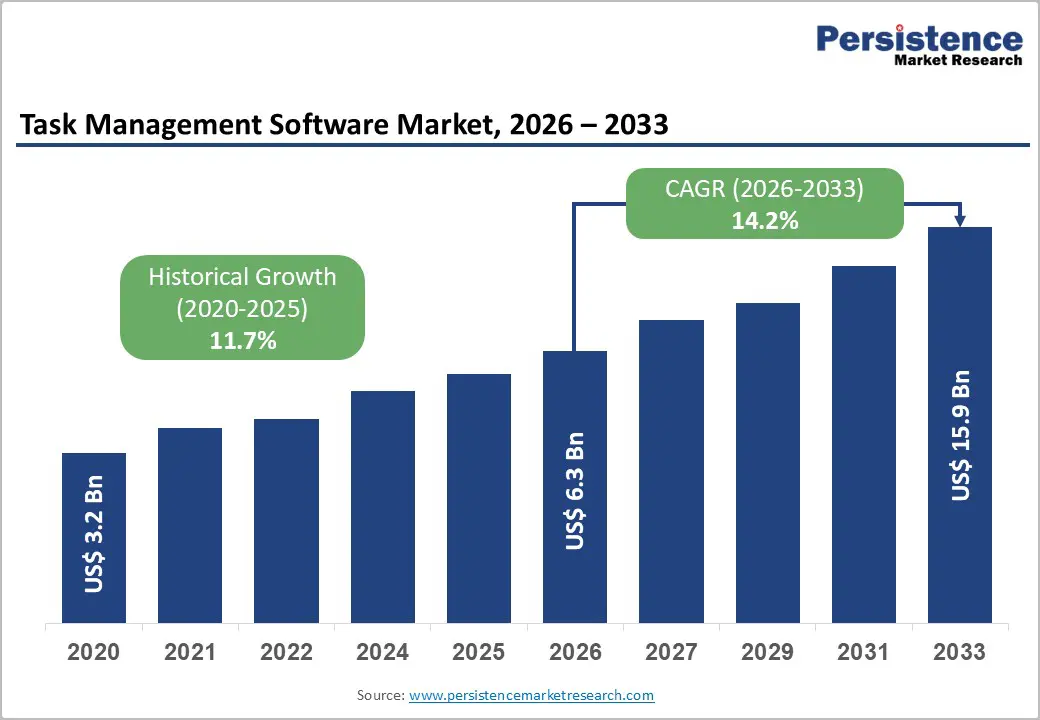

The global Task Management Software Market size is projected to rise from US$6.3 Bn in 2026 to US$15.9 Bn by 2033. It is anticipated to witness a CAGR of 14.2% during the forecast period from 2026 to 2033, driven by the rapid digitalization of workplaces, increasing adoption of hybrid work models, and growing need for real-time collaboration tools.

Organizations are prioritizing productivity optimization and workflow automation, supported by rising investments in cloud-based enterprise solutions and integration with AI-powered analytics. The surge in the remote workforce, estimated to involve over 30% of global employees in flexible arrangements, has significantly accelerated demand for scalable task management platforms across industries.

Key Industry Highlights:

- Leading Offering: Solutions dominate the market with over 76% share in 2026, valued at more than US$ 4.8 Bn, driven by the growing need for centralized platforms that enable real-time task planning, tracking, and collaboration. Services are the fastest-growing, supported by rising demand for implementation, integration, and consulting to maximize platform efficiency and ROI.

- Leading Deployment: On-premises holds over 40% share in 2026, valued at more than US$ 2.5 Bn, due to strong enterprise preference for data security, regulatory compliance, and control over internal systems. Cloud-based / SaaS is the fastest-growing segment, driven by scalability, flexibility, remote accessibility, and increasing adoption among SMEs and distributed teams.

- Leading Application: Task Tracking & Monitoring leads with over 25% share in 2026, valued at more than US$ 1.6 Bn, fueled by the need for real-time visibility, accountability, and performance tracking across projects. Workload & Resource Management is the fastest-growing application, expanding at a CAGR of 18.4% due to increasing focus on optimizing employee productivity and efficient resource allocation.

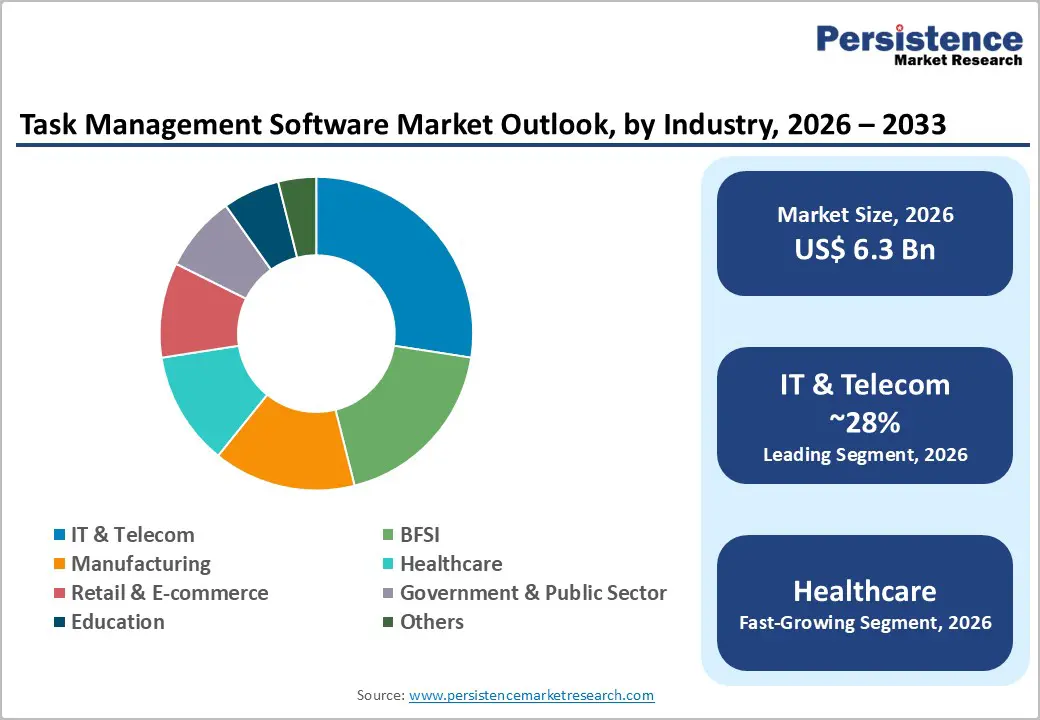

- Leading Industry: IT & Telecom dominates with over 28% share in 2026, valued at more than US$ 1.8 Bn, driven by agile development practices, high project complexity, and demand for seamless collaboration across global teams. Healthcare is the fastest-growing industry, supported by the rising need for workflow optimization, improved care coordination, and compliance-driven task tracking.

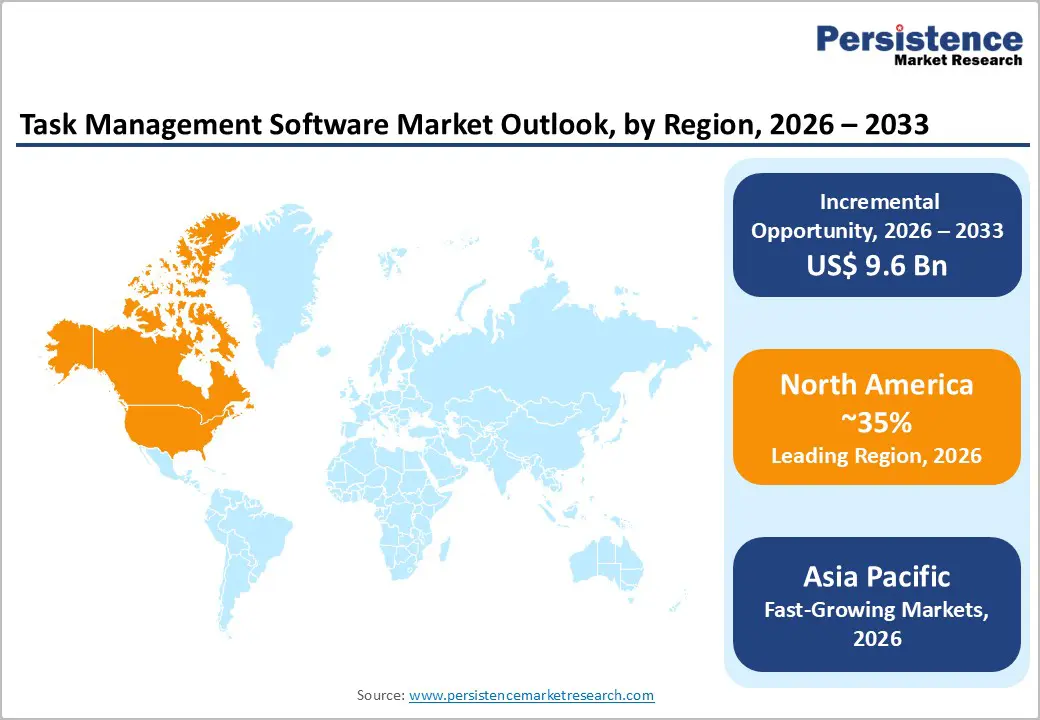

- Leading Region: North America leads with over 35% share in 2026, valued at US$ 2.2 Bn, supported by advanced digital infrastructure, strong SaaS adoption, and presence of major market players. Asia Pacific is the fastest-growing region with a CAGR of 19.5%, driven by rapid SME digitalization, government initiatives like Digital India, and increasing adoption of AI-powered cloud solutions.

| Key Insights | Details |

|---|---|

|

Task Management Software Market Size (2026E) |

US$6.3 Bn |

|

Market Value Forecast (2033F) |

US$15.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

14.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

11.7% |

Market Dynamics

Driver

Increasing Enterprise Focus on Workflow Automation and Productivity Optimization

Organizations are increasingly investing in workflow automation to improve operational efficiency and reduce manual intervention. Studies by World Economic Forum indicate that automation technologies could improve workplace productivity by over 20% across knowledge-based industries. Task management software integrates automation features such as task assignment, notifications, and progress tracking, significantly enhancing operational transparency. Enterprises are also leveraging analytics dashboards to gain insights into employee performance and project timelines. This aligns with the broader expansion of the workflow automation software market, where businesses are adopting digital tools to streamline repetitive processes, optimize resource allocation, and improve overall organizational performance.

Surge in Remote and Hybrid Work Adoption

The shift to remote and hybrid work has fundamentally transformed organizational structures, necessitating robust task management solutions for distributed teams. According to a study, businesses using an average of 3.4 task-related applications report 25 -35% higher productivity through better integration. This is evidenced by the rapid growth in mobile-first platforms, which facilitate real-time updates and collaboration, reducing communication silos. Enterprises embracing these tools have seen 25 - 30% fewer missed project deadlines, as teams gain visibility into workloads across time zones. This is amplified by digital transformation initiatives, where over 80% of business applications are projected to be SaaS-based by 2026, making task management indispensable for agile operations.

Restraint

Tool Saturation and Integration Complexity

Enterprises are grappling with increasing tool sprawl, with the average organization using 106 SaaS applications. Task management platforms frequently overlap with communication, documentation, and ERP systems, creating redundancy and complex integration. A significant approximately 20% of purchased software licenses remain unused across enterprise deployments, reflecting user fatigue and insufficient change management investment. This fragmentation drives organizations toward platform consolidation, favoring established vendors with broader ecosystems but simultaneously slowing incremental license expansion and new client acquisition for niche task management providers.

Data Security and Privacy Compliance Concerns

Task management platforms often store sensitive project and organizational data in cloud environments. According to European Union Agency for Cybersecurity (ENISA), cyberattacks on enterprise software systems increased by over 35% in recent years. Compliance with regulations such as GDPR and other data protection frameworks adds complexity and cost for vendors. Organizations handling confidential data, particularly in BFSI and healthcare sectors, may hesitate to fully adopt cloud-based solutions due to perceived risks.

Opportunity

Integration of Artificial Intelligence and Predictive Analytics

AI-powered features such as predictive task scheduling, intelligent reminders, and performance analytics enable organizations to make data-driven decisions. According to a study, AI adoption in enterprise software is expected to grow by over 25% annually. These capabilities enhance decision-making and improve productivity by forecasting project risks and bottlenecks. This is also closely linked with the evolution of Artificial Intelligence in the Enterprise Applications Market, where advanced analytics and automation are transforming operational workflows.

Growing Demand from SMEs and Emerging Economies

Small and medium enterprises (SMEs) represent a rapidly expanding customer base for task management solutions. Governments worldwide, including initiatives by the Government of India under Digital India, are promoting digital adoption among SMEs. Over 60% of SMEs globally are expected to adopt cloud-based tools by the end of the decade. Cost-effective SaaS solutions with scalable pricing models are enabling SMEs to improve operational efficiency without significant capital investment. This expansion is further supported by growth in the Cloud Collaboration Software Market, where affordable and flexible solutions are driving widespread adoption across emerging economies.

Category-wise Analysis

Offering Analysis

Solution dominates the market, capturing more than 76% market share in 2026 with a value exceeding US$ 4.8 Bn, due to the rising need for centralized platforms that enable organizations to plan, assign, and monitor tasks in real time. Businesses increasingly demand integrated features within a single interface. The shift toward remote and hybrid work models has further accelerated reliance on software solutions to maintain productivity and visibility. Enterprises prefer scalable platforms that integrate with existing ecosystems like CRM and ERP systems. Continuous innovation in AI-driven task prioritization and automation also strengthens solution adoption.

Services are expected to grow significantly due to the increasing complexity of deployment, customization, and integration requirements across organizations. Many enterprises require consulting, training, and support services to ensure optimal utilization of task management platforms. As businesses scale, the need for ongoing maintenance, upgrades, and workflow optimization becomes critical. Small and medium enterprises especially rely on service providers to reduce implementation risks and accelerate ROI.

Deployment Analysis

On-premises hold over 40% market share in 2026, with a value exceeding US$ 2.5 Bn, due to strong demand from organizations prioritizing data security, privacy, and regulatory compliance. Industries prefer on-premises deployments for greater control over sensitive data and internal workflows. Customization flexibility and the ability to align with legacy IT infrastructure also contribute to its adoption. Companies with strict data governance policies often avoid external cloud dependencies. Long-term cost predictability in certain large-scale deployments further supports this segment.

Cloud-based / SaaS is expected to grow rapidly due to the increasing need for flexibility, scalability, and remote accessibility across distributed teams. Cloud solutions enable real-time collaboration and seamless updates without heavy infrastructure investments. Startups and SMEs particularly favor SaaS models due to lower upfront costs and subscription-based pricing. The growing adoption of mobile-first work environments and global teams further accelerates demand.

Application Analysis

Task Tracking & Monitoring commands the largest market share at over 25% in 2026, with a value exceeding US$ 1.6 Bn, due to the fundamental need for visibility into task progress, deadlines, and accountability across teams. Organizations rely heavily on tracking tools to improve productivity, reduce delays, and ensure project alignment. Real-time dashboards, notifications, and reporting capabilities help managers make informed decisions quickly. The increasing complexity of projects and distributed workforce structures further amplifies the importance of monitoring solutions. Performance measurement and transparency requirements drive sustained demand.

Workload & Resource Management is expected to grow at a CAGR of 18.4% due to the rising need to optimize employee productivity and prevent burnout in dynamic work environments. Organizations are increasingly focusing on balancing workloads and efficiently allocating resources to maximize output. Advanced tools offering predictive analytics and AI-driven recommendations enhance decision-making. As project portfolios grow more complex, efficient resource planning becomes critical for cost control and timely delivery. The shift toward agile and lean management practices also fuels adoption.

Industry Analysis

IT & Telecom holds over 28% market share in 2026, with a value exceeding US$ 1.8 Bn, due to the sector’s strong reliance on agile development, continuous deployment, and collaborative workflows. Task management software is essential for managing complex projects, tracking bugs, and coordinating cross-functional teams. Rapid digital transformation and high project volumes further increase dependency on these tools. Integration with DevOps and software development platforms enhances operational efficiency. The global and distributed nature of IT teams necessitates robust task coordination systems.

Healthcare is expected to grow significantly due to the increasing need for streamlined workflow management in clinical, administrative, and operational processes. Task management tools help improve coordination among medical staff, reduce errors, and enhance patient care delivery. The growing adoption of digital health systems and electronic records drives demand for structured task tracking solutions. Regulatory compliance and the need for audit trails further encourage implementation. Rising patient volumes and resource constraints make efficient task allocation critical in healthcare environments.

Regional Insights

North America Task Management Software Market Trends

North America holds over 35% share in 2026, reaching US$ 2.2 Bn value, driven by advanced digital infrastructure and early SaaS adoption. The region hosts major players with strong enterprise usage across BFSI, healthcare, and IT sectors. Cloud-based deployments account for over 70–75% of new implementations, reflecting demand for scalability and remote collaboration. Regulatory frameworks such as FedRAMP are influencing public sector adoption. Canada is emerging as a secondary growth hub, supported by digital innovation and startup expansion.

Asia Pacific Task Management Software Market Trends

Asia Pacific is expected to grow at a significant rate with a CAGR of 19.5%, driven by expanding SMEs, rapid cloud adoption, and government initiatives such as India’s Digital India program. Key markets include China, India, Japan, South Korea, and Australia, with rising investments in AI-powered SaaS platforms. Japan’s digital innovation programs and Southeast Asia’s cloud-first policies are further accelerating adoption. Increasing mobile workforce penetration and startup ecosystem expansion are key contributors to regional growth.

Europe Task Management Software Market Trends

Europe is expected to hold more than 26% share by 2026, supported by enterprise digitization across the UK, Germany, France, and the Netherlands. Compliance with General Data Protection Regulation drives preference for private and sovereign cloud deployments to ensure data security and residency. Germany’s Industrie 4.0 and national AI strategies across the UK and EU are accelerating adoption of workflow automation tools. Nordic countries are early adopters of AI-enabled task management platforms due to advanced IT ecosystems. Public sector and education digitization initiatives continue to boost demand across the region.

Competitive Landscape

The global task management software market exhibits a moderately consolidated competitive structure, with dominant positions held by a handful of large-scale platforms, while a long tail of niche and regional vendors competes for specialized use cases. Market leaders differentiate through ecosystem breadth, native AI integration, and enterprise-grade compliance and security frameworks. Key strategic trends include platform consolidation through acquisitions, aggressive AI roadmap investments, and freemium-to-enterprise conversion models targeting the SME segment.

Key Industry Developments

- In May 2025, Asana launched its Smart Workflow Gallery, offering prebuilt AI-powered workflows to help organizations enhance productivity through human + AI collaboration across functions like marketing, IT, and operations. The solution complements its AI Studio, enabling teams to either build custom workflows or quickly deploy ready-made ones to automate tasks, improve efficiency, and maintain human oversight.

- In February 2025, monday.com Ltd. announced its AI Vision for 2025, focusing on AI Blocks, Product Power-ups, and a Digital Workforce to enhance workflow automation and productivity. The initiative aims to empower businesses of all sizes to scale operations and enable users to build AI-driven workflows without technical expertise.

Companies Covered in Task Management Software Market

- Microsoft Corporation

- Atlassian Corporation Plc

- Asana, Inc.

- Monday.com Ltd.

- Smartsheet Inc.

- ClickUp Inc.

- Wrike

- Zoho Corporation Pvt. Ltd.

- Upland Software, Inc.

- Quick Base, Inc.

- Oracle Corporation

- SAP SE

- Others

Frequently Asked Questions

The global market is projected to be valued at US$6.3 Bn in 2026.

Rising adoption of cloud-based solutions and productivity tools to enhance operational efficiency and accountability further fuels market demand are key driver of the market.

The market is expected to witness a CAGR of 14.2% from 2026 to 2033.

The integration of AI-driven automation, predictive analytics, and no-code/low-code customization to enhance productivity and decision-making is creating strong growth opportunities.

Microsoft Corporation, Atlassian Corporation Plc, Asana, Inc., Monday.com Ltd., Smartsheet Inc., ClickUp Inc., Wrike, Zoho Corporation Pvt. Ltd., Upland Software, Inc., Quick Base, Inc. are among the leading key players.