- Hardware & Software IT Services

- eSIM Subscription Market

eSIM Subscription Market Size, Share, and Growth Forecast 2026 - 2033

eSIM Subscription Market by Subscription Type (Data only plans, Voice + Data plans, IoT / M2M connectivity plans), Application (Smartphones & consumer devices, Wearables, Connected vehicles, Industrial IoT devices), End-user (Consumer, Enterprise, Automotive), by Regional Analysis, 2026 - 2033

eSIM Subscription Market Size and Trend Analysis

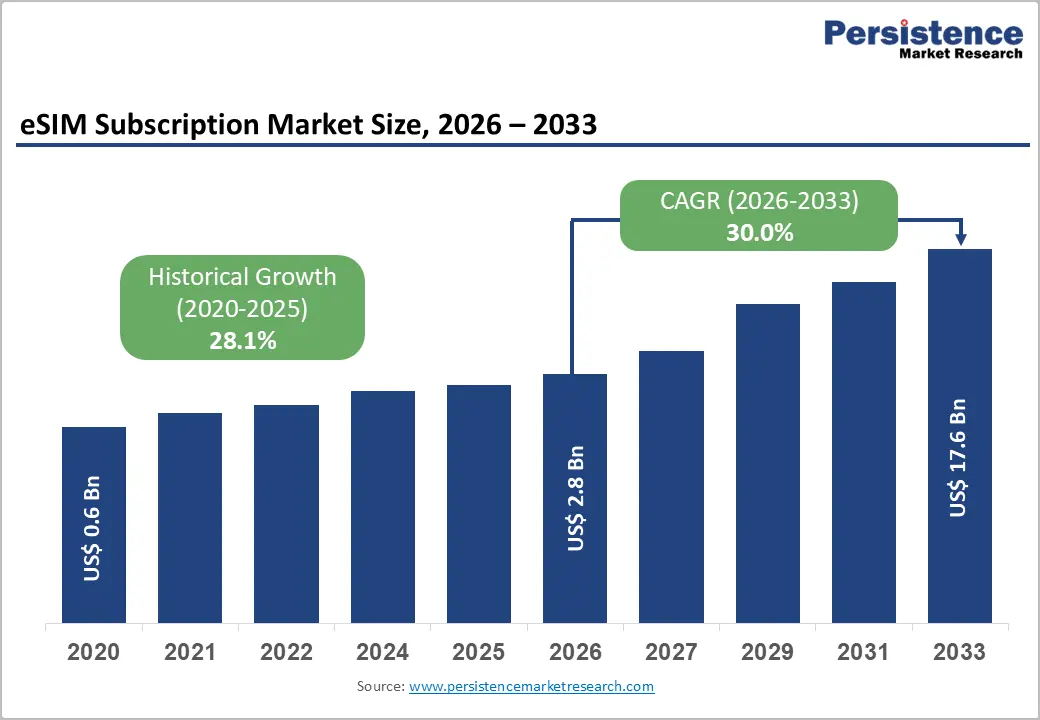

The global eSIM Subscription Market size is expected to be valued at US$ 2.8 billion in 2026 and projected to reach US$ 17.6 billion by 2033, growing at a CAGR of 30.0% between 2026 and 2033. Growth is driven by the rapid adoption of embedded SIM technology across consumer devices, enterprise IoT networks, and connected vehicles.

The shift from physical SIM cards enables cost efficiency for operators, flexible device design for OEMs, and seamless multi-carrier activation for users. Rising smartphone integration, 5G expansion, and increasing eSIM-only devices further accelerate demand, supported by strong growth in global connections, shipments, and digital profile activations.

Key Industry Highlights:

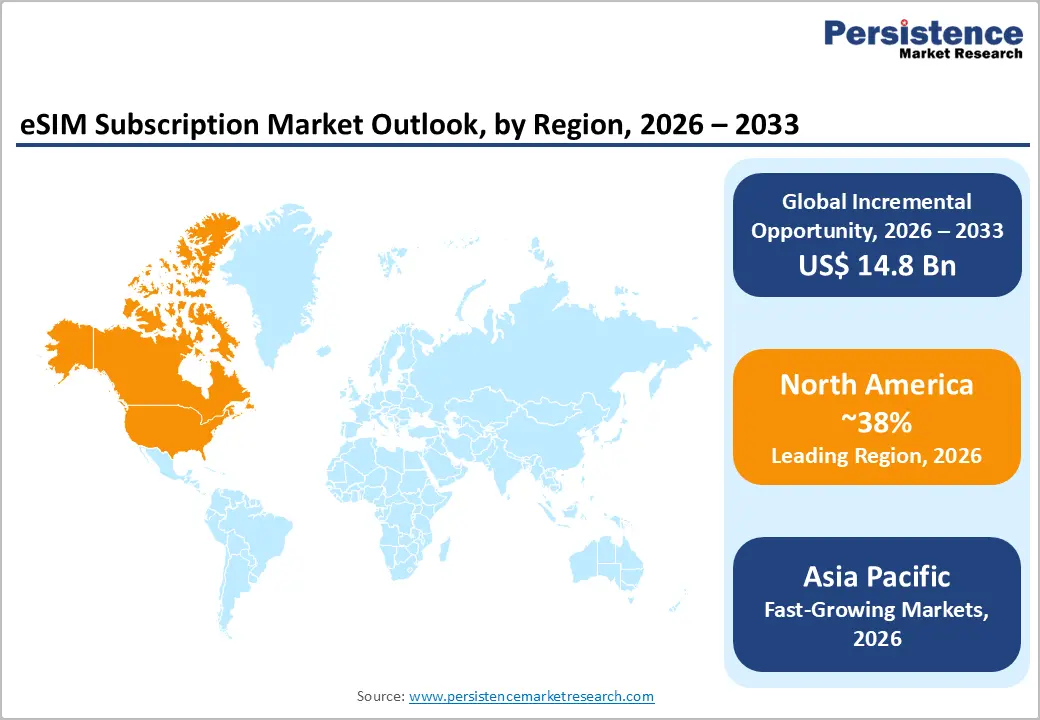

- Leading Region: North America leads with 38% share (2025), driven by strong telecom infrastructure and early eSIM adoption.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, supported by rapid 5G expansion and rising IoT adoption.

- Leading Subscription Type: Voice + Data plans dominate with 45% share (2025) due to integrated communication demand.

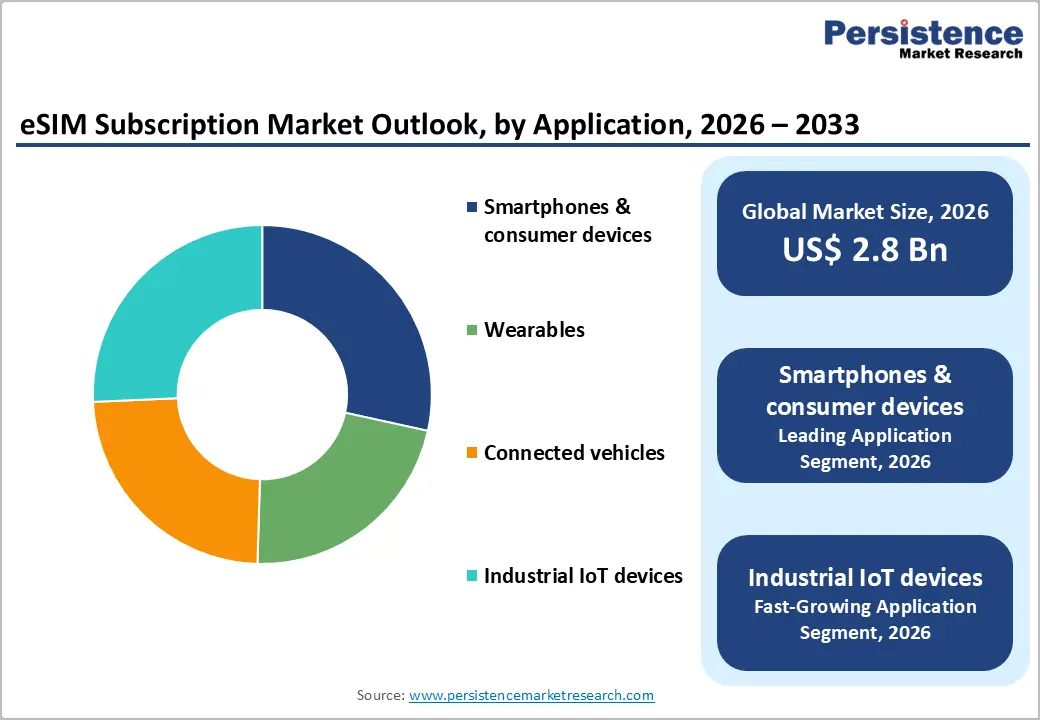

- Leading Application: Smartphones & consumer devices hold 55% share (2025) driven by widespread eSIM-enabled device adoption.

- Leading End-user: Consumer segment accounts for ~50% share (2025) fueled by digital-first connectivity preferences.

- Key Market Opportunity: IoT / M2M connectivity plans are emerging as a major growth opportunity with scalable subscription-based deployments.

| Key Insights | Details |

|---|---|

|

eSIM Subscription Size (2026E) |

US$ 2.8 Billion |

|

Market Value Forecast (2033F) |

US$ 17.6 Billion |

|

Projected Growth CAGR (2026-2033) |

30.0% |

|

Historical Market Growth (2020-2025) |

28.1% |

Market Dynamics

Drivers - Rapid Expansion of IoT and 5G Connected Devices Driving eSIM Subscription Demand Growth

The global proliferation of IoT and 5G-enabled devices is a major structural driver for eSIM subscription growth, with cellular IoT connections surpassing 4 billion in 2024 and continuing to expand steadily. Growth is fueled by increasing deployment of LTE Cat 1 bis and 5G modules across industries such as logistics, utilities, and manufacturing, where scalable and flexible connectivity is essential.

At the same time, eSIM-based IoT connections are rising rapidly as enterprises shift from traditional SIM cards to remotely provisioned solutions. Advancements in remote SIM provisioning standards enable seamless cross-border deployment and reduce operational complexities, encouraging telecom operators to bundle IoT connectivity plans with eSIM subscriptions, thereby strengthening long-term recurring revenue opportunities.

Accelerating Adoption of eSIM in Smartphones and Consumer Connected Devices Globally

The rapid integration of eSIM technology in smartphones and consumer devices is another key growth driver, supported by widespread OEM adoption and increasing availability across both premium and mid-range devices. Global eSIM smartphone connections are expected to rise significantly, driven by growing consumer preference for digital connectivity and simplified activation processes.

Additionally, increasing shipments of eSIM-enabled devices and rising profile downloads highlight a clear behavioral shift toward digital-only provisioning. Users benefit from features such as multi-carrier flexibility, easy switching, and seamless connectivity for travel and work, which enhances user experience while enabling telecom operators to improve customer retention and increase average revenue per user.

Restraints - Fragmented Device Ecosystem and Limited Consumer Awareness Slowing eSIM Adoption

Despite strong growth potential, the eSIM subscription market faces challenges from device fragmentation and uneven consumer awareness. While premium smartphones increasingly support eSIM, penetration across mid- and low-range devices remains limited, especially in price-sensitive markets where physical SIM usage is still dominant, restricting large-scale adoption.

At the same time, many consumers remain unfamiliar with eSIM activation and management, leading to confusion and higher support requirements for operators. This awareness gap, combined with inconsistent device compatibility, slows the transition toward digital SIM models and delays widespread acceptance of flexible, subscription-based connectivity services.

Regulatory Complexity Security Concerns and Interoperability Challenges Limiting Market Expansion

Regulatory and security challenges present another major restraint, particularly for cross-border deployments and enterprise IoT applications. Varying national rules around data localization, SIM registration, and telecom licensing complicate the rollout of unified global eSIM subscription plans across regions, increasing operational complexity for service providers.

In addition, concerns around data security, SIM swap risks, and platform vulnerabilities require advanced encryption and remote provisioning safeguards. These measures significantly increase compliance and infrastructure costs, creating entry barriers for smaller players and slowing the pace of adoption despite the maturity and long-term benefits of eSIM technology.

Opportunities - Rising Industrial IoT and M2M Connectivity Platforms Unlocking Subscription Revenue Opportunities

A major opportunity lies in the expansion of industrial IoT and M2M connectivity platforms built around eSIM-enabled remote provisioning. Rapid growth in connected devices across sectors such as utilities, logistics, and manufacturing is driving demand for scalable, always-on connectivity solutions with minimal maintenance requirements.

eSIM technology enables factory-embedded connectivity, eliminating the need for physical SIM handling and allowing remote profile updates across networks. Providers offering multi-carrier connectivity, data management tools, and cloud-based analytics can capitalize on recurring enterprise subscriptions, particularly as Industry 4.0 initiatives and smart infrastructure projects accelerate globally.

Growing Enterprise Mobility and Connected Vehicle Ecosystems Creating New Subscription Models

Another key opportunity is emerging in enterprise mobility and connected vehicle ecosystems, where eSIM enables centralized and flexible connectivity management. Businesses are increasingly adopting eSIM-enabled devices integrated with management platforms to support hybrid work environments and secure global connectivity for employees.

Simultaneously, the automotive sector is expanding eSIM integration in connected vehicles for telematics, infotainment, and over-the-air updates. This creates strong potential for bundled subscription models combining data, voice, and digital services, allowing telecom operators and platform providers to generate sustained revenue from both enterprise and automotive segments.

Category-wise Analysis

Subscription Type Analysis

Voice + Data plans dominate the eSIM Subscription Market, accounting for approximately 45% share in 2025. This leadership is driven by widespread smartphone usage, where consumers prefer integrated communication services within a single eSIM profile. Dual SIM and dual eSIM functionalities further support demand, enabling users to manage personal and professional connections simultaneously while increasing overall subscription value.

IoT/M2M connectivity plans are emerging as the fastest-growing segment, driven by rapid expansion of connected devices across industries. Enterprises increasingly prefer scalable, remotely managed connectivity solutions for long-term deployments, making IoT-focused eSIM subscriptions a critical future growth engine beyond traditional consumer telecom usage.

Application Insights

Smartphones & consumer devices lead the Application segment, holding around 55% of the eSIM subscription base in 2025. This dominance is supported by strong OEM adoption, with most flagship smartphones and an increasing number of mid-range devices integrating eSIM functionality, thereby expanding the addressable market for subscription-based connectivity services globally.

At the same time, Industrial IoT devices are the fastest-growing application segment due to increasing adoption in sectors such as logistics, utilities, and manufacturing. These devices require reliable, always-on connectivity and benefit significantly from remote provisioning, making eSIM an ideal solution for scalable, long-term deployments across diverse industrial environments.

End-user Insights

The consumer segment leads the eSIM subscription market, accounting for nearly 50% share in 2025, driven by strong adoption among individual mobile users. Increasing preference for digital activation, seamless carrier switching, and global connectivity has accelerated uptake, especially among younger, tech-savvy users who value flexibility and convenience in telecom services.

In contrast, the enterprise segment is the fastest-growing, supported by rising adoption of eSIM-enabled devices in corporate mobility and IoT deployments. Businesses are increasingly leveraging centralized connectivity management and secure communication systems, driving demand for scalable subscription models tailored to operational efficiency and global workforce connectivity.

Regional Insights

North America eSIM Subscription Market Trends and Insights

North America leads the eSIM Subscription Market, holding an estimated share of around 38% in 2025, driven by strong telecom infrastructure, early regulatory support, and close collaboration between operators and device manufacturers. High smartphone penetration and widespread availability of eSIM-enabled devices have accelerated adoption, with carriers increasingly shifting toward digital-first activation models.

The region continues to see rapid momentum due to expanding 5G coverage and growing demand for seamless, multi-carrier connectivity. Enterprise IoT deployments and private network initiatives across industries such as logistics and healthcare are further boosting adoption, positioning North America as a key hub for both consumer and enterprise eSIM subscription growth.

Europe eSIM Subscription Market Trends and Insights

Europe represents a significant growth region for eSIM subscriptions, supported by strong regulatory frameworks and high demand for cross-border connectivity. The region benefits from harmonized telecom policies and increasing integration of eSIM technology in consumer devices, particularly across major markets such as Germany, the U.K., France, and Spain.

The market is expected to grow at a CAGR of around 28.3% over the forecast period, driven by rising enterprise adoption and expansion of IoT applications. Increasing deployment of eSIM-based solutions in fleet management, smart utilities, and logistics is strengthening demand, while improved interoperability standards are reducing fragmentation and enabling scalable subscription models across multiple countries.

Asia Pacific eSIM Subscription Market Trends and Insights

Asia Pacific is the fastest-growing region in the eSIM Subscription Market, accounting for approximately 27.3% share in 2025, supported by large-scale smartphone adoption, rapid 5G rollout, and strong government-led digital initiatives. Countries such as China, India, and Japan are driving regional growth through expanding telecom infrastructure and increasing integration of eSIM in consumer and industrial devices.

Growth is further fueled by the region’s strong manufacturing ecosystem, enabling cost-effective production of eSIM-enabled devices at scale. Rising adoption across smart city projects, enterprise IoT deployments, and connected mobility solutions is accelerating demand, positioning Asia Pacific as the most dynamic and high-potential market for eSIM subscription services globally.

Competitive Landscape

The eSIM subscription market is moderately consolidated, with leading telecom operators and platform providers controlling a significant portion of overall subscription revenue. Established network operators dominate both consumer and enterprise segments by leveraging existing infrastructure, large subscriber bases, and strong distribution networks, while technology providers support the ecosystem through secure provisioning platforms and scalable connectivity solutions.

At the same time, emerging players such as virtual operators, travel-focused platforms, and IoT connectivity providers are expanding market competition by targeting niche segments. Differentiation is driven by multi-network access, cloud-based management systems, and integrated digital platforms, creating a competitive environment that combines strong core dominance with innovation-driven growth at the edges.

Key Developments:

- In March 2025, Apple expanded eSIM support to all current U.S. iPhone models, partnering with Verizon to enable instant eSIM activation for new customers. This move strengthened consumer-facing eSIM adoption in North America and further standardized eSIM-only provisioning for flagship smartphones, influencing operator and regulatory strategies in other regions.

- In July 2024, GSMA formally launched updated eSIM profile specifications optimized for IoT and M2M use cases, including enhancements to SGP.32 standards for remote-SIM-provisioning. Major chipset vendors such as Qualcomm and Samsung subsequently integrated these updated profiles, accelerating IoT-eSIM deployment across connected vehicles, smart meters, and industrial sensors.

- In January 2025, Thales and IDEMIA announced a joint collaboration on quantum-resistant eSIM security modules for automotive and critical-infrastructure IoT deployments. Aligned with EU cybersecurity directives and GSMA-aligned security frameworks, this initiative aims to harden eSIM-based subscriptions against emerging cryptographic threats, reinforcing trust in long-term enterprise and automotive connectivity plans.

Companies Covered in eSIM Subscription Market

- Airalo

- GigSky

- Ubigi

- Holafly

- Nomad eSIM

- Yesim

- Truphone

- Deutsche Telekom

- Telefónica

- Vodafone Group

- AT&T

- Orange S.A.

- KORE Wireless

- BNESIM

- Maya Mobile

Frequently Asked Questions

The global eSIM Subscription Market is projected to reach US$ 2.8 billion by 2026, driven by rising smartphone adoption, 5G rollout, and expanding IoT connectivity.

Key drivers include rapid 5G expansion, growing IoT/M2M connections, and increasing adoption of eSIM-enabled smartphones offering flexible, multi-carrier connectivity.

North America leads the market with 38% share (2025), supported by advanced telecom infrastructure and strong eSIM adoption.

A major opportunity lies in IoT/M2M connectivity plans enabling scalable, subscription-based connectivity across industrial and smart applications.

Leading players include AT&T, Verizon, T‑Mobile, Vodafone, Orange, China Mobile, Thales, IDEMIA, Qualcomm, and Apple.