- Hardware & Software IT Services

- Smart Pest Monitoring Management System Market

Smart Pest Monitoring Management System Market Size, Share, and Growth Forecast 2026 - 2033

Smart Pest Monitoring Management System Market by Component (Hardware, Software, Services), Pest Type (Insects, Rodents, Birds, Others), Application (Agriculture, Commercial, Industrial, Residential, Others), and Regional Analysis, 2026 - 2033

Smart Pest Monitoring Management System Market Size and Trend Analysis

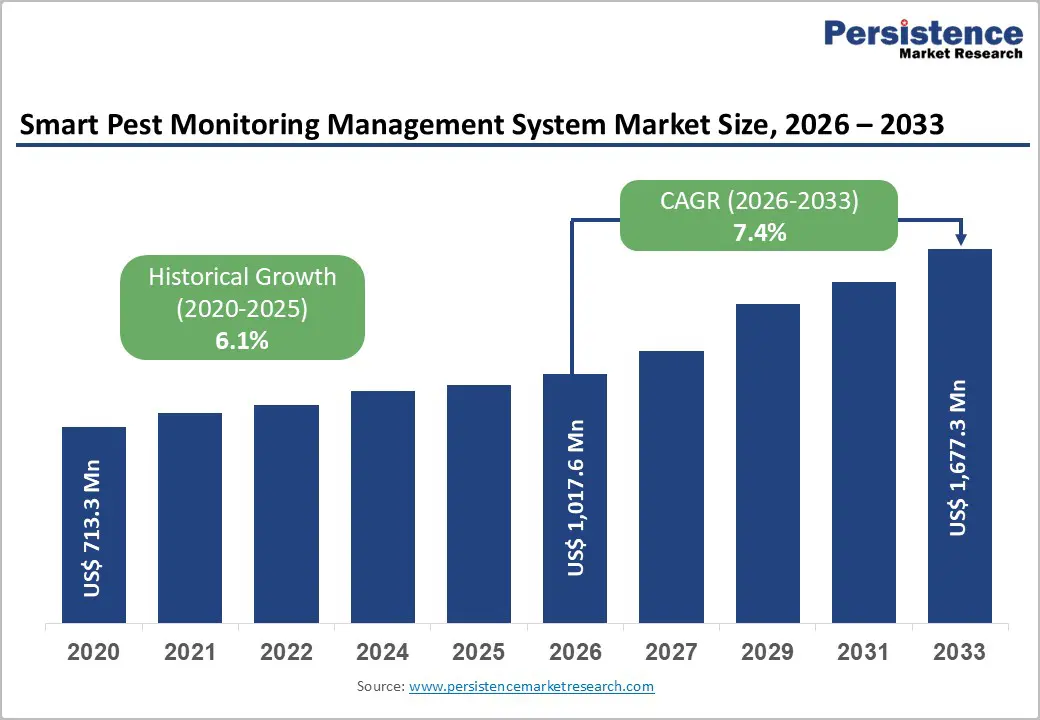

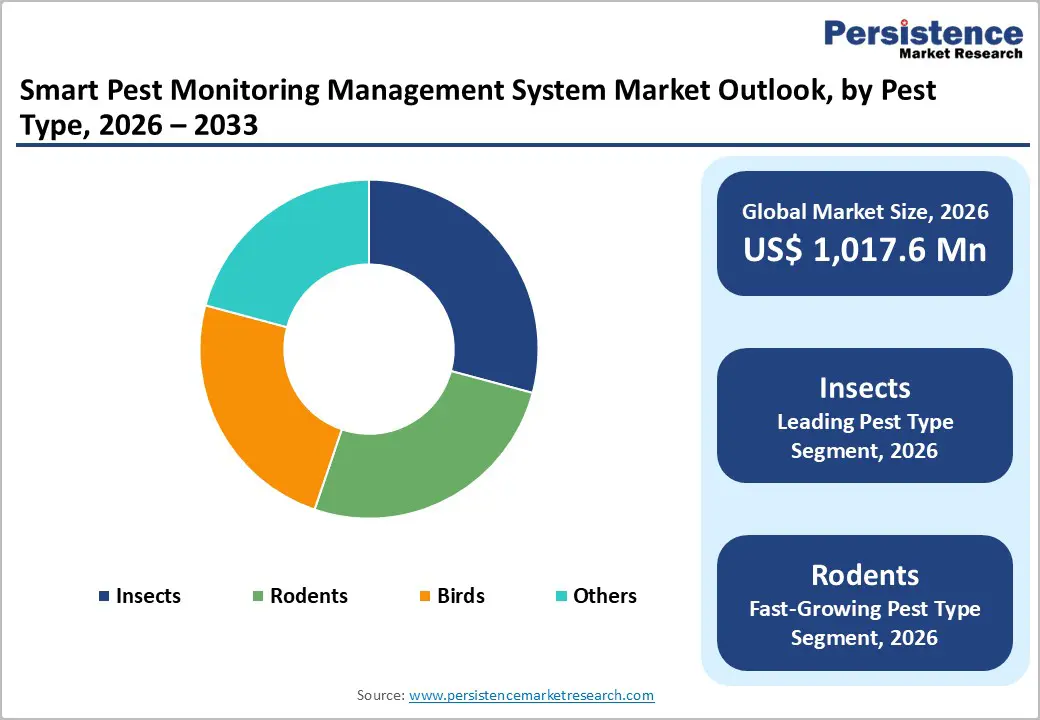

The global smart pest monitoring management system market size is expected to be valued at US$ 1,017.6 million in 2026 and projected to reach US$ 1,677.3 million by 2033, growing at a CAGR of 7.4% between 2026 and 2033.

Growth is driven by increasing demand for precision agriculture and sustainable pest control solutions amid rising global food security concerns. Significant crop losses due to pests are accelerating the adoption of IoT-enabled monitoring systems for real-time detection and early warning. Advancements in sensors, connectivity, and AI analytics are enabling data-driven pest management, reducing pesticide use, improving efficiency, and ensuring regulatory compliance across agriculture, commercial, industrial, and residential sectors.

Key Industry Highlights:

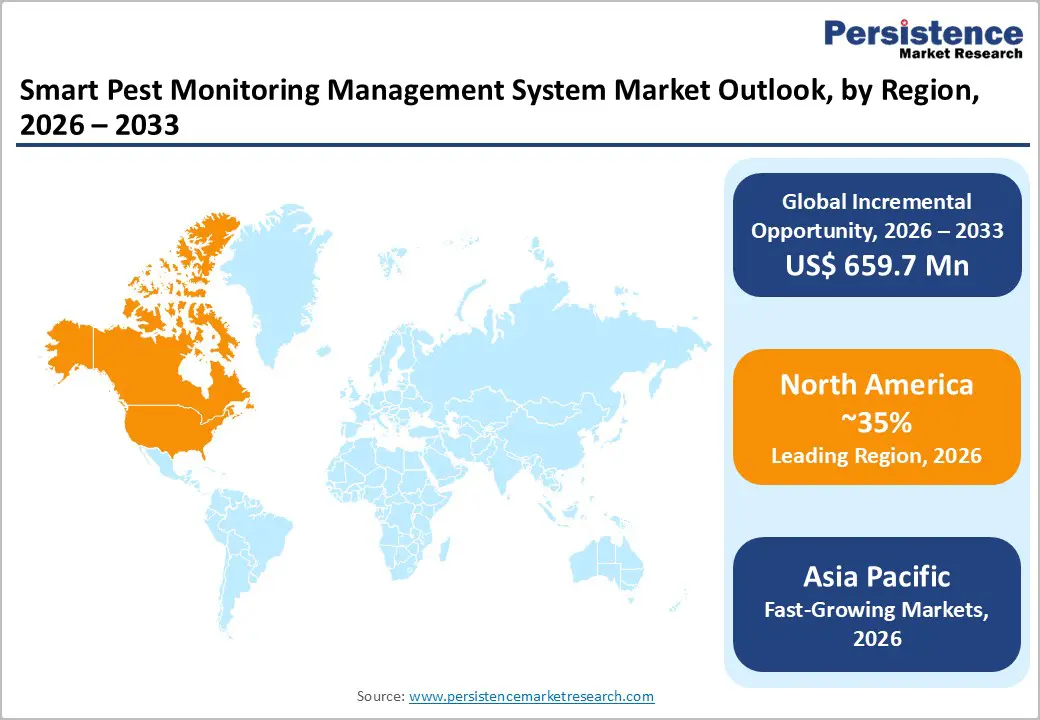

- Leading Region: North America leads the market with approximately 35% share in 2025, driven by adoption of agritech, regulatory support, and advanced monitoring infrastructure.

- Fastest Growing Region: Asia Pacific is the fastest-growing region with around 25% share in 2025, supported by expanding digital agriculture initiatives and increasing pest management needs.

- Leading Application: Agriculture dominates with about 55% share in 2025, due to high crop loss risks and growing adoption of precision farming solutions.

- Leading Component: Hardware holds nearly 45% share in 2025, as sensors and smart traps form the core of pest monitoring systems.

- Leading Pest Type: Insects account for approximately 52% share in 2025, driven by their significant impact on crop productivity.

- Key Market Opportunity: Integration with precision agriculture and smart ecosystem platforms is creating strong growth opportunities across both agricultural and urban applications.

| Key Insights | Details |

|---|---|

| Smart Pest Monitoring Management System Size (2026E) | US$ 1,017.6 million |

| Market Value Forecast (2033F) | US$ 1,677.3 million |

| Projected Growth CAGR (2026 - 2033) | 7.4% |

| Historical Market Growth (2020 - 2025) | 6.1% |

Market Dynamics

Drivers - Advancements in IoT and AI Driving Smart Pest Monitoring

Integration of IoT sensors, wireless trap networks, and AI-powered analytics is transforming pest monitoring from reactive to predictive, significantly boosting demand for smart systems. Connected traps and imaging devices enable real-time pest detection, reducing response delays and allowing timely interventions. This shift improves operational efficiency by minimizing unnecessary inspections and enhancing decision-making accuracy across agriculture and commercial environments.

In precision agriculture, AI-based pest detection supports targeted treatment, reducing excessive pesticide use while maintaining crop productivity. Expanding deployment of 5G and low-power wide-area networks (LPWANs) further strengthens connectivity, enabling large-scale sensor integration. These advancements collectively enhance data-driven pest management, lower costs, and support environmentally sustainable practices across multiple end-use sectors.

Stringent Pesticide Regulations Accelerating Smart Monitoring Adoption

Increasingly strict regulations on pesticide usage are encouraging the adoption of smart pest monitoring systems worldwide. Governments are promoting Integrated Pest Management (IPM) practices that rely on real-time data and monitoring tools instead of routine chemical spraying. This regulatory push is driving farmers and facility operators to implement digital solutions for improved compliance and reduced environmental impact.

Commercial and industrial sectors are also adopting smart monitoring to meet food safety and public health standards through continuous surveillance and audit-ready reporting. Growing concerns around pesticide resistance, ecological harm, and worker safety are further accelerating the transition toward sustainable pest control methods, positioning smart monitoring systems as essential tools for regulatory adherence and long-term environmental responsibility.

Restraints - High Initial Costs and Infrastructure Limiting Adoption

High upfront investment in sensors, gateways, software, and training remains a key barrier to adoption, particularly for small-scale farmers and businesses. While long-term savings exist, initial capital requirements discourage deployment, especially where low-tech alternatives are still considered sufficient. This cost sensitivity slows adoption across price-sensitive markets and limits widespread implementation of advanced monitoring systems.

Infrastructure gaps further restrict scalability, particularly in developing regions with unreliable power supply and limited broadband connectivity. These challenges affect real-time data transmission and system efficiency, forcing compromises in deployment. As a result, market penetration remains uneven, with adoption largely concentrated in regions that have stronger digital ecosystems and better access to financing.

Limited Technical Expertise Hindering User Adoption and Efficiency

A lack of technical expertise among end users poses a significant challenge to effective utilization of smart pest monitoring systems. Many users struggle with configuring devices, interpreting analytics, and managing cloud-based dashboards, leading to inefficiencies or incorrect decision-making. This knowledge gap is particularly evident in traditional agricultural settings where digital familiarity remains low.

User acceptance is further impacted by the complexity of systems, making intuitive interfaces and automated recommendations essential. Without adequate training and support, systems risk being underutilized or abandoned after initial deployment. This limits the scalability of pilot projects and reduces confidence among potential users, ultimately slowing broader market adoption.

Opportunity - Integration with Precision Agriculture Driving Smart Monitoring Opportunities

A key opportunity lies in integrating smart pest monitoring systems with broader precision agriculture and agritech platforms. Combining pest data with soil sensors, weather analytics, and crop health imaging enables holistic farm management and real-time decision-making. This integration allows automated alerts, optimized treatment recommendations, and improved resource utilization across agricultural operations.

Such platforms can also connect with autonomous spraying and robotic systems, enhancing efficiency and reducing input costs. Government-backed digital farming initiatives across regions are accelerating adoption by supporting pilot projects and scalable deployments. Aligning solutions with these programs enables companies to tap into high-growth opportunities within the agriculture segment.

Emerging Markets Expansion Supported by Agricultural Modernization Initiatives

Emerging economies present strong growth potential as governments focus on agricultural modernization, food security, and climate-resilient farming practices. Increasing adoption of IoT-based farm monitoring systems is creating demand for smart pest detection solutions, particularly in regions with large agricultural bases and evolving digital infrastructure.

To succeed in these markets, companies are developing cost-effective, rugged, and low-maintenance solutions such as solar-powered or battery-operated sensors suitable for remote areas. Flexible pricing models, including subscription or pay-per-use, further enhance accessibility. These factors position emerging markets as key growth engines, particularly for agriculture-focused applications over the forecast period.

Category-wise Analysis

Component Insights

Within the component category, hardware is the leading segment, accounting for approximately 45% of the market share in 2025. This dominance reflects the essential role of sensors, smart traps, cameras, and gateways in capturing real-time pest data, forming the backbone of monitoring systems. End users typically prioritize investment in durable, weather-resistant hardware capable of continuous operation across agricultural fields and industrial environments, reinforcing its strong market position.

The software segment is emerging as the fastest-growing category, driven by increasing demand for cloud-based platforms, AI-powered analytics, and predictive pest management tools. As users seek actionable insights rather than just raw data, software solutions enabling automation, remote monitoring, and decision support are gaining traction, particularly in digitally advanced farming and commercial environments.

Pest Type Insights

Among pest types, insects hold the largest share, estimated at approximately 52% of the global market in 2025. Their dominance is driven by their significant impact on crop yields, especially in staple crops, making them the primary focus of monitoring systems. Technologies such as pheromone traps, image recognition sensors, and acoustic detection are widely used to track insect activity across agricultural and urban environments.

The rodents segment is the fastest-growing category due to increasing concerns in commercial and industrial settings such as warehouses, food processing units, and urban infrastructure. Rising hygiene standards and the need for continuous monitoring are driving the adoption of smart rodent detection systems, which offer real-time alerts and improved control compared to traditional methods.

Application Insights

Within application segments, agriculture leads the market, accounting for approximately 55% of the share in 2025. This is primarily due to the high economic impact of pest-related crop losses and the growing adoption of precision farming techniques. Farmers and large-scale agricultural operations are increasingly deploying smart monitoring systems to enhance yield protection, optimize pesticide usage, and comply with stringent export and food safety standards.

The commercial segment is experiencing the fastest growth, driven by rising demand across food service, retail, and hospitality. Businesses are increasingly adopting smart pest monitoring systems to ensure regulatory compliance, maintain hygiene standards, and enable continuous, audit-ready pest surveillance, making it a key growth area beyond traditional agricultural use.

Regional Insights

North America Smart Pest Monitoring Management System Market Trends and Insights

North America is the leading region in 2025, accounting for approximately 35% of the global market share. This dominance is driven by strong adoption in the United States, supported by advanced agricultural R&D, robust regulatory frameworks, and widespread implementation of Integrated Pest Management practices. High demand from large-scale farms, food processing facilities, and commercial establishments further strengthens the region’s leadership position.

The region continues to see steady growth due to ongoing innovation in AI-based pest detection, IoT-enabled monitoring systems, and predictive analytics. Collaboration between research institutions, agritech firms, and regulatory bodies is accelerating commercialization. Additionally, increasing compliance requirements in food safety and storage sectors are driving continuous investment in real-time pest monitoring solutions across agricultural and industrial applications.

Europe Smart Pest Monitoring Management System Market Trends and Insights

Europe represents a significant market, supported by strong regulatory emphasis on sustainable agriculture and reduced pesticide usage. The region is projected to grow at a CAGR of approximately 7.8% during the forecast period. Policies promoting organic farming and Integrated Pest Management are encouraging the adoption of digital monitoring systems across key agricultural economies.

Growth is further supported by advancements in sensor technologies and increasing deployment in high-value crops such as fruits, vegetables, and vineyards. Strong research backing and cross-border regulatory alignment enable scalable adoption of standardized solutions. In addition, strict food safety and hygiene regulations across commercial and industrial sectors are boosting demand for connected pest monitoring systems with real-time tracking and compliance capabilities.

Asia Pacific Smart Pest Monitoring Management System Market Trends and Insights

Asia Pacific holds an estimated 25% market share in 2025 and is the fastest-growing region, driven by large-scale agricultural activities and increasing adoption of digital farming technologies. Government-led initiatives supporting smart agriculture and IoT deployment are accelerating adoption across countries such as China and India, particularly in key crop-producing regions.

The region is witnessing rapid growth due to rising food security concerns, increasing pest-related crop losses, and expanding use of cost-effective monitoring solutions. Adoption is further supported by the development of affordable sensor technologies and growing awareness among farmers. Additionally, urbanization and rising demand for pest control in commercial and industrial facilities are contributing to the expansion of smart pest monitoring systems across diverse applications.

Competitive Landscape

The global Smart Pest Monitoring Management System market shows a moderately consolidated structure, with a mix of established agritech and pest control providers alongside numerous regional and niche players. Market participants differentiate through proprietary sensor technologies, AI-driven analytics, and cloud-based platforms integrated with farm and facility management systems. Strategic collaborations with research institutions, distributors, and equipment providers further support market expansion and targeted application development.

Evolving business models such as subscription-based services, pay-per-use pricing, and hardware-as-a-service are reducing upfront costs and improving accessibility. Vendors are also focusing on offline-capable systems and edge computing to address connectivity challenges in remote areas, enabling broader adoption and continued innovation.

Key Developments:

- In March 2025, Fovea launched an AI-powered insect-trap system integrated with drone-based scouting in Europe, enabling automated detection of key pests in orchards and vineyards. The solution reportedly reduces pest-response time by up to 50% and has been adopted in pilot programs across several EU member states.

- In July 2024, Trapview expanded its solar-powered pheromone-monitoring network to India, deploying thousands of units across rice and cotton belts in partnership with ICAR-linked research stations. The rollout targets early detection of major lepidopteran pests and supports government-sponsored digital-farming missions.

- In November 2023, Semios introduced an enhanced cloud-based analytics platform for rodent and insect pest monitoring in North America, integrating data from wireless traps with weather and crop-stage information to generate predictive alerts. The system has been adopted by over 200 orchards and several large-scale berry farms.

Companies Covered in Smart Pest Monitoring Management System Market

- Bayer AG

- Anticimex

- Corteva Agriscience

- BASF SE

- Ecolab Inc.

- Syngenta AG

- Bell Laboratories, Inc.

- Pelsis Group Ltd

- Rentokil Initial plc

- FMC Corporation

- Rollins, Inc.

- SemiosBio Technologies

- FaunaPhotonics

- DunavNET

- Spensa Technologies

Frequently Asked Questions

The global Smart Pest Monitoring Management System market is expected to reach US$ 1,017.6 million in 2026.

Advancements in IoT and AI and stricter pesticide regulations are driving adoption, particularly in agriculture and insect monitoring.

North America leads the market with approximately 35% share, driven by advanced agritech adoption and regulatory support.

A key opportunity lies in integration with precision agriculture and smart ecosystems, especially in Asia Pacific.

Leading players include Fovea, Trapview, Semios, Pessl Instruments, Rentokil Initial, and Bayer.