- Medical Devices

- Stadiometers Equipment Market

Stadiometers Equipment Market Size, Share, and Growth Forecast, 2026 – 2033

Stadiometers Equipment Market by Product (Digital Stadiometers, Mechanical Stadiometers, Portable Stadiometers), Distribution Channel (Online Stores, Medical Supply Stores, Specialty Stores), End-user (Hospitals, Clinics, Others), and Regional Analysis for 2026 – 2033

Stadiometers Equipment Market Size and Trends Analysis

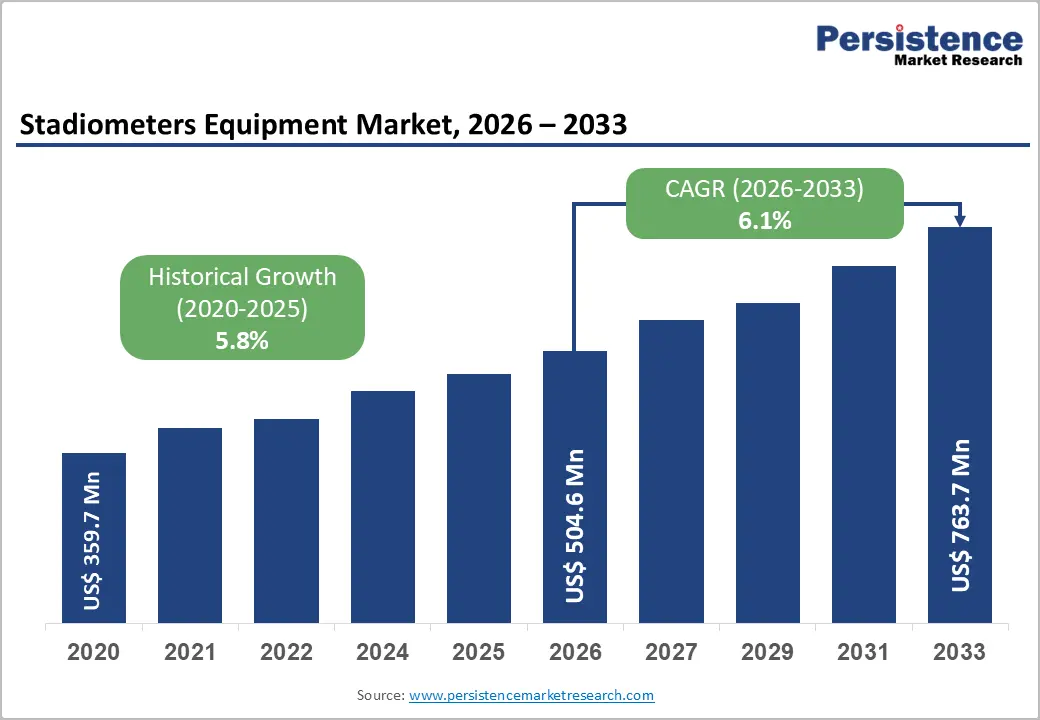

The global stadiometers equipment market size is likely to be valued at US$504.6 million in 2026 and is expected to reach US$763.7 million by 2033, growing at a CAGR of 6.1% during the forecast period from 2026 to 2033, driven by increasing global burden of obesity and other non-communicable diseases, rising importance of anthropometric measurements in clinical diagnosis and child growth monitoring as emphasized in WHO-supported nutrition and growth surveillance programs, expanding hospital and primary care infrastructure especially in emerging economies, and growing adoption of digital stadiometers with EHR integration for accurate, standardized and real-time height measurement across hospitals, clinics, and fitness centers.

Key Industry Highlights:

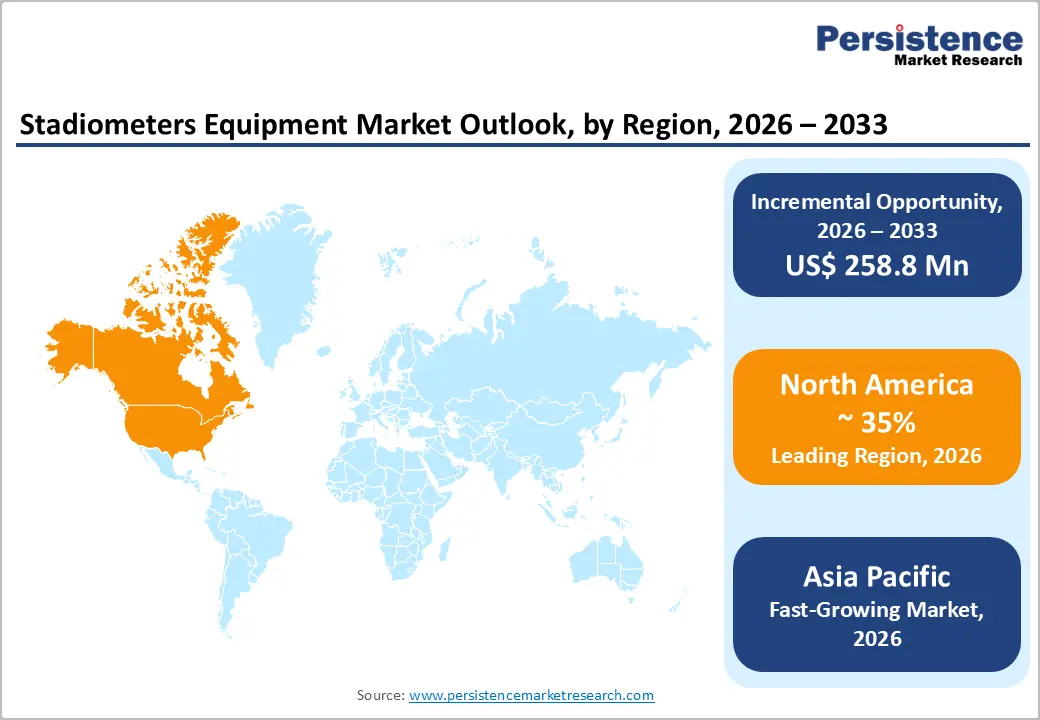

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 35% in 2026, driven by its well-developed healthcare infrastructure.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region in the stadiometers equipment in 2026, supported by the rapid urban development and increasing healthcare spending.

- Leading Product Type: Mechanical stadiometers are projected to represent the leading product type in 2026, accounting for 55% of the revenue share, due to their affordability, durability, and continued widespread use in routine clinical and primary care settings, especially in cost-sensitive healthcare regions.

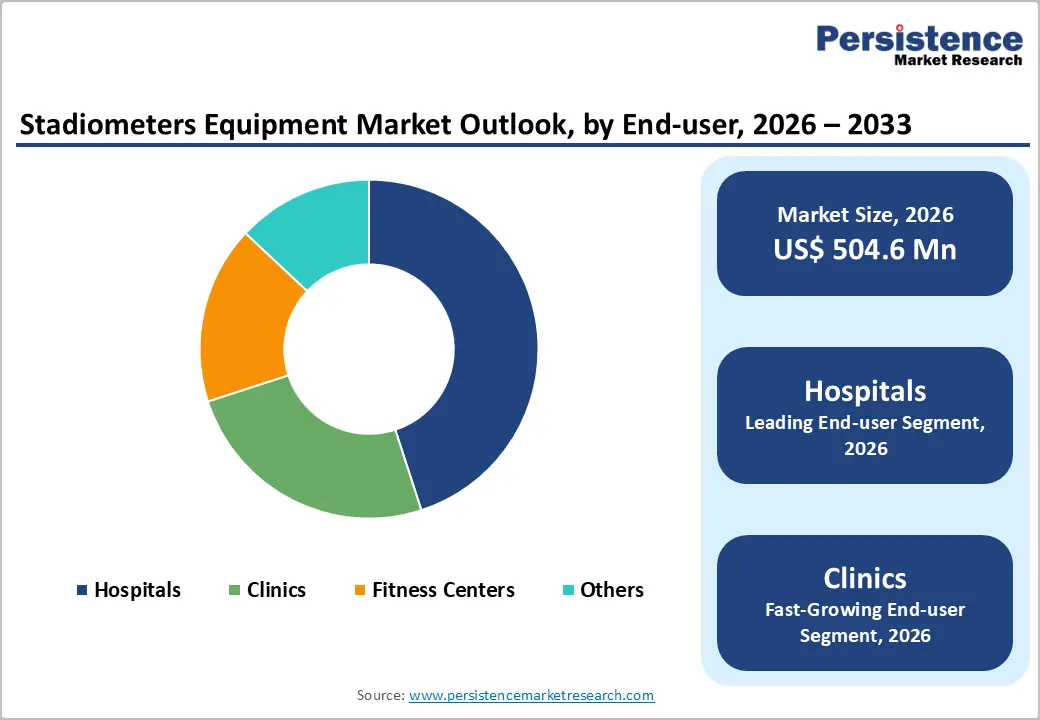

- Leading End-user: Hospitals are anticipated to be the leading end-user, accounting for over 40% of the revenue share in 2026, supported by high patient volume, mandatory height measurement in clinical diagnostics, and growing integration of standardized anthropometric tools in hospital-based electronic health record systems.

- Key Opportunity: The key market opportunity in the stadiometers equipment market lies in the rapid shift toward smart, connected, and digital anthropometric measurement systems integrated with electronic health records and preventive healthcare programs.

DRO Analysis

Driver - Rising Healthcare Infrastructure Investment

The growing prevalence of obesity and nutritional disorders is a major driver of the stadiometers equipment market, as accurate height measurement is essential for calculating BMI and monitoring patient health status. Rising cases of lifestyle diseases such as diabetes, cardiovascular disorders, and metabolic syndrome strengthen the demand for precise body measurement tools.

This has made stadiometers a standard diagnostic instrument in preventive healthcare, pediatric growth monitoring, and nutrition assessment programs across developed and emerging healthcare systems. Increasing public health initiatives focused on early disease detection and wellness tracking are increasing the adoption of stadiometers in primary care settings.

Governments and healthcare organizations are emphasizing regular health screening programs, especially for children and high-risk populations. This has led to greater deployment of digital and mechanical stadiometers in hospitals, clinics, and community health centers. The integration of anthropometric data into electronic health records also supports long-term patient monitoring, improving clinical decision-making.

Restraint - Presence of Low-Cost Alternatives and Counterfeit Products

The stadiometers equipment market faces significant restraint due to the presence of low-cost alternatives and counterfeit products, particularly in price-sensitive regions. Unbranded or locally manufactured measuring tools are widely available at lower prices, making them attractive for small clinics and rural healthcare providers. These alternatives often lack calibration accuracy and durability, but their affordability limits the adoption of premium-grade stadiometers.

Counterfeit and substandard medical measuring devices pose challenges related to quality assurance and patient safety. Inaccurate height measurement can lead to incorrect BMI calculation and misdiagnosis in clinical settings. Despite regulatory efforts by health authorities and standardization bodies, weak enforcement in some regions allows such products to circulate in the market.

Opportunity - Product Innovation in Wall-Mounted and Portable Stadiometers

Wall-mounted stadiometers are gaining popularity in hospitals and clinics due to their accuracy, stability, and ease of use in high-patient-volume environments. Portable versions are increasingly used in field healthcare programs, home visits, and fitness assessments. The growing focus on preventive healthcare and mobile diagnostics has accelerated the adoption of these advanced designs, improving accessibility of height measurement across different care settings.

Integration of digital technologies such as Bluetooth connectivity, LCDs, and cloud-based data storage is enhancing product value. These innovations allow seamless transfer of patient data into electronic health record systems, improving workflow efficiency and accuracy.

Manufacturers are also focusing on lightweight materials and ergonomic designs to improve usability. Rising demand from emerging economies, school health programs, and wellness centers supports market expansion. Increasing integration with digital health platforms and telemedicine systems is enhancing remote patient monitoring capabilities.

Category-wise Analysis

Product Type Insights

Mechanical stadiometers are expected to lead, accounting for 55% of revenue in 2026, due to their affordability, durability, and widespread use in routine clinical examinations and primary healthcare facilities. These devices are preferred in hospitals and small clinics as they do not require a power supply, are easy to maintain, and provide reliable height measurements for BMI calculation and growth monitoring. For example, many district hospitals in developing regions continue to use wall-mounted mechanical stadiometers for pediatric assessments.

Digital stadiometers are likely to represent the fastest-growing segment, supported by increasing demand for accuracy, automation, and integration with electronic health record systems. These devices offer quick readings, reduced human errors, and enhanced data management capabilities, making them highly suitable for modern hospitals and diagnostic centers. For instance, advanced urban hospitals are increasingly adopting digital stadiometers with Bluetooth connectivity for seamless patient data transfer to hospital software systems.

End-user Insights

Hospitals are projected to lead the market, capturing around 40% of the revenue share in 2026, supported by high patient inflow, mandatory anthropometric assessments, and standardized diagnostic protocols. Height measurement is a routine part of patient evaluation in outpatient departments, pediatrics, and chronic disease management, making stadiometers essential equipment. A notable example includes large multi-specialty hospitals, which use wall-mounted stadiometers in every general examination room to ensure consistent BMI calculation and clinical documentation, reinforcing their strong demand across healthcare infrastructure.

Clinics are likely to be the fastest-growing end-user driven by increasing outpatient visits, rising awareness of preventive healthcare, and expansion of primary care networks. Clinics are rapidly adopting compact and digital stadiometers to improve diagnostic efficiency and patient experience. For instance, urban polyclinics are integrating portable digital stadiometers for quick health check-ups during routine consultations and wellness screenings.

Distribution Channel Insights

Medical supply stores are expected to lead the stadiometers equipment market, accounting for 45% share in 2026, driven by strong procurement relationships with hospitals, clinics, and government healthcare institutions. These stores provide certified and standardized medical equipment, ensuring reliability and compliance with healthcare regulations. A notable example includes large hospital chains, which often source stadiometers through authorized medical supply distributors to maintain quality assurance and bulk procurement efficiency, making this channel the primary source for institutional buyers.

Online stores are likely to represent the fastest-growing segment, supported by increasing digital adoption and ease of product comparison, pricing, and doorstep delivery. Healthcare professionals and small clinics are increasingly purchasing stadiometers through e-commerce platforms due to convenience and wider product availability. For instance, many private clinics now order portable digital stadiometers online to reduce procurement time and access newer models quickly.

Regional Insights

North America Stadiometers Equipment Market Trends

North America is expected to lead, accounting for a market share of 35% in 2026, supported by a well-developed healthcare infrastructure and strong awareness of health and fitness among the population. Medical facilities are prioritizing accurate measurement tools as part of routine care. The presence of established manufacturers is strengthening supply capabilities and innovation. These factors are collectively reinforcing sustained demand and market leadership within the region.

U.S. Stadiometers Equipment Market Trends

The U.S. dominates the regional market, driven by a well-funded healthcare system, high per-capita medical device spending, and robust regulatory infrastructure through the FDA's 510(k) clearance pathway. School health mandates across all 50 states sustain a large institutional buyer base, while pediatric and geriatric clinical volumes ensure continuous hospital procurement.

Canada Stadiometers Equipment Market Trends

Canada is a significant market for stadiometers equipment supported by publicly funded healthcare systems and national wellness programs that emphasize routine anthropometric screening. Growing adoption of connected healthcare infrastructure and preventive care initiatives is increasing demand for digital and portable stadiometers, particularly within telehealth-supported monitoring frameworks.

Europe Stadiometers Equipment Market Trends

Europe is likely to be a significant market for stadiometers equipment, due to mature healthcare systems and a growing focus on preventive and personalized care. Regulatory frameworks are enforcing strict medical device standards, which ensure high levels of quality and safety. Healthcare providers are adopting compliant stadiometers to meet these requirements, which is strengthening trust and consistency in clinical measurements.

U.K. Stadiometers Equipment Market Trends

The U.K. is a significant market for stadiometers equipment, supported by National Health Service (NHS) screening programs and strong pediatric health monitoring frameworks. Demand remains stable due to structured public procurement and regulatory alignment under European medical device standards. The expansion is being supported by digital health adoption and integration of measurement devices into centralized patient data systems, which is improving long-term population health tracking and equipment standardization.

Germany Stadiometers Equipment Market Trends

Germany dominates the regional market due to strong healthcare expenditure and mandatory child health screening programs that require precise measurement tools. Its industrial base includes key manufacturers such as Seca GmbH, reinforcing domestic supply strength. The EU's Medical Device Regulation (MDR 2017/745) framework has harmonized compliance across member states, simplifying multi-country market entry.

Asia Pacific Stadiometers Equipment Market Trends

The Asia Pacific region is anticipated to be the fastest-growing region, driven by rapid urban development, increasing healthcare spending, and growing awareness of personal health management. Countries such as China, India, and Japan are leading regional progress through sustained investment in hospitals and diagnostic infrastructure. The rising middle-class population is actively prioritizing routine health monitoring, which is strengthening demand for reliable measurement tools across clinical and community healthcare settings.

China Stadiometers Equipment Market Trends

China dominates the regional market, supported by large-scale hospital expansion and domestic manufacturing capabilities. Companies such as Zhongshan Camry Electronic are strengthening local production and cost competitiveness. Government-led healthcare infrastructure upgrades and increasing demand for scalable, affordable diagnostic tools are accelerating adoption, especially across public hospitals and rural health programs.

India Stadiometers Equipment Market Trends

India is a significant market for stadiometer equipment, due to national nutrition missions and school health screening initiatives. Expansion of primary healthcare networks and increased focus on malnutrition tracking are strengthening procurement volumes, while portable and low-cost devices are gaining traction in outreach programs.

Competitive Landscape

The global stadiometers equipment market exhibits a moderately fragmented structure, driven by the presence of several established multinational manufacturers and a large number of regional players competing through innovation, pricing, and distribution strength. The market is characterized by steady consolidation trends, with leading companies focusing on digital transformation, product accuracy, and integration with electronic health record (EHR) systems.

With key leaders including Seca GmbH & Co. KG, Detecto Scale Company, Tanita Corporation, Charder Electronic Co., Ltd., and Befour Inc., the competitive environment remains highly dynamic. These players compete through continuous product innovation, expansion of portable and digital stadiometer portfolios, and strategic partnerships with hospitals, clinics, and healthcare distributors to strengthen reach and brand presence.

Key Industry Developments:

- In April 2026, Tanita Corporation expanded its medical measurement portfolio with the launch of the MC-800 clinical-grade body composition system, enhancing its integrated anthropometric assessment ecosystem used in healthcare and fitness settings. The development strengthens its broader precision measurement solutions by improving data accuracy for BMI-related analysis, where stadiometers play a critical role in height measurement and patient profiling.

Companies Covered in Stadiometers Equipment Market

- Seca GmbH & Co. KG

- Detecto

- Befour Inc.

- Charder Electronic Co., Ltd.

- Holtain Ltd.

- Marsden Weighing Machine Group

- KERN & SOHN GmbH

- Health-O-Meter Professional

- ADE GmbH & Co. KG

- Jiangsu Yuyue Medical Equipment & Supply

- Tanita Corporation

- Natus Medical Incorporated

- Sunbeam Products

Frequently Asked Questions

The global stadiometers equipment market is projected to reach US$504.6 million in 2026.

The market is driven by routine anthropometric screening in pediatric, geriatric, and preventive care; healthcare digitization favors EHR-compatible digital devices.

The stadiometers equipment market is expected to grow at a CAGR of 6.1% from 2026 to 2033.

Major opportunities lie in digital replacement cycles in hospitals, portable solutions for community & outreach care, Asia-Pacific growth, and multi-parameter connected measurement ecosystems.

Seca GmbH & Co. KG, Detecto, Befour Inc., and Charder Electronic Co., Ltd. are some of the key players in the market.