- Renewable Energy

- Solar Street Lighting Market

Solar Street Lighting Market Size, Share, and Growth Forecast 2026 - 2033

Solar Street Lighting Market by Product Type (Standalone Solar Street Lights, Grid-Connected Solar Street Lights, Hybrid Solar Street Lights, Integrated/All-in-One Solar Street Lights, Smart Solar Street Lights), by Component (Solar Panel, Battery, Lighting Fixture/Lamp, Controller, Sensors), by Power Capacity, Installation Type, End-user, and Regional Analysis, 2026 - 2033

Solar Street Lighting Market Size and Trend Analysis

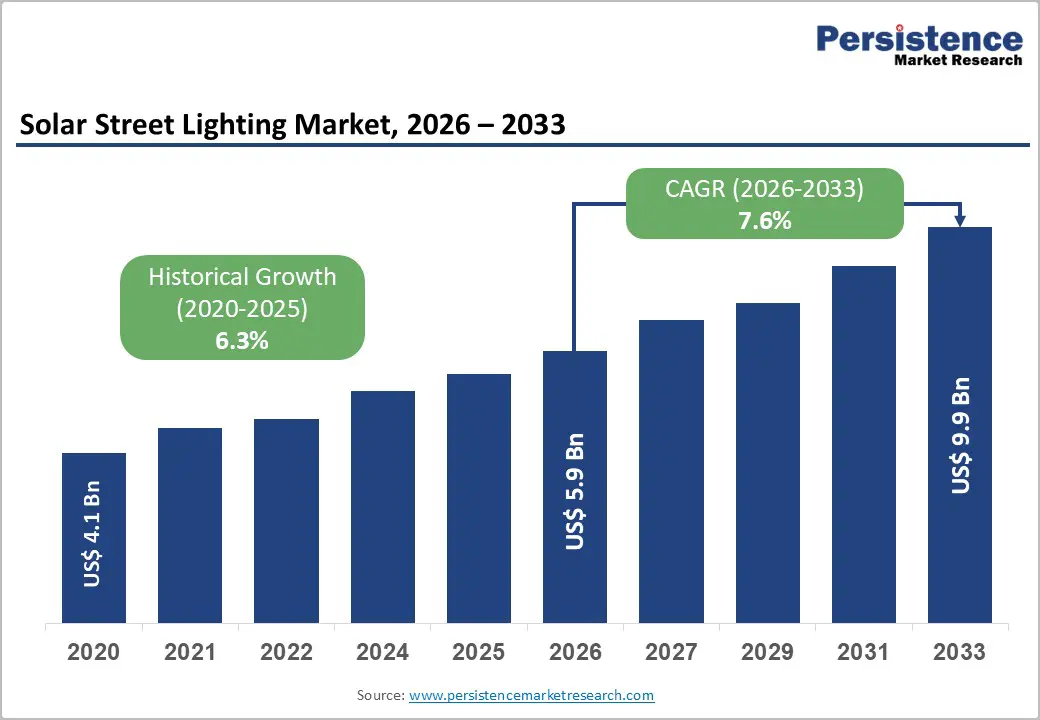

The global solar street lighting market size is likely to be valued at US$ 5.9 billion in 2026 and is expected to reach US$ 9.9 billion by 2033, growing at a CAGR of 7.6% during the forecast period from 2026 to 2033.

Accelerating government mandates for clean energy infrastructure, the rapid cost reduction of solar photovoltaic (PV) modules and lithium-ion batteries, and proliferating smart city development programs across both mature and emerging economies are collectively propelling robust market expansion.

Key Industry Highlights:

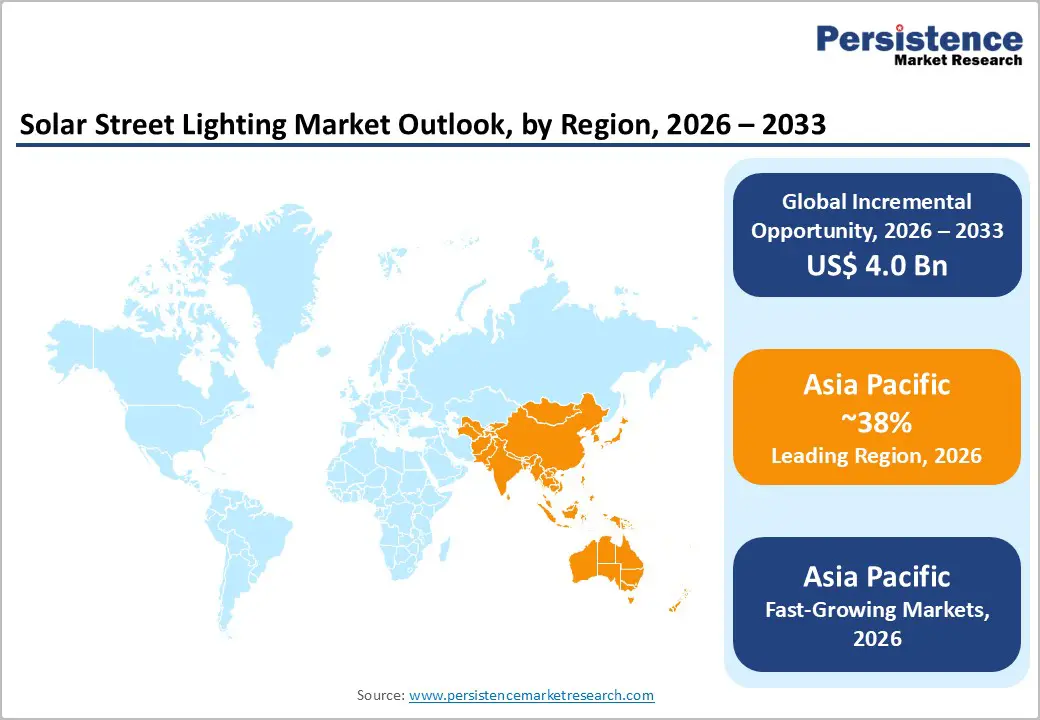

- Leading Region: Asia Pacific leads the global Solar Street Lighting market accounting for 38% share, anchored by large-scale government procurement programs in China and India, extensive smart city infrastructure investment, and robust regional manufacturing competitiveness that collectively sustain the region's dominant revenue contribution.

- Fastest-Growing Region: Asia Pacific is also the fastest-growing regional market with rising CAGR of 9.3%, driven by accelerating urbanization, ASEAN renewable energy policy mandates, and substantial multilateral financing from the World Bank and ADB supporting solar infrastructure deployment across India, Vietnam, and Indonesia.

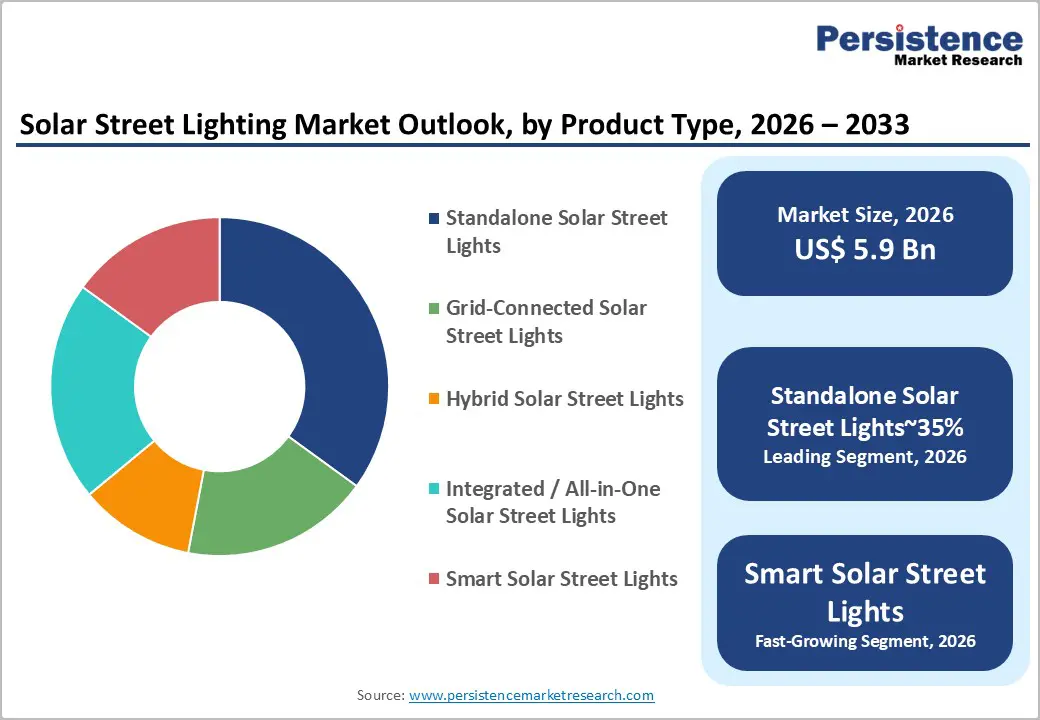

- Leading Segment: Standalone Solar Street Lights dominate the By Product Type category with approximately 35% market share, underpinned by grid-independent operation, simplified installation without cabling requirements, and sustained government-driven rural electrification procurement across Africa, South Asia, and Southeast Asia.

- Fastest-Growing Segment: Smart Solar Street Lights represent the fastest-growing product type segment, propelled by surging IoT adoption, escalating smart cities program pipelines across Asia Pacific and North America, and the demonstrated capacity of smart systems to reduce energy consumption by up to 60% versus conventional fixed-output alternatives.

- Key Opportunity: Off-grid rural electrification across South Asia and Sub-Saharan Africa represents the single most significant near-term commercial opportunity, with concessional financing from the World Bank and ADB combined with national subsidy programs creating an accelerating procurement pipeline for solar street lighting manufacturers through 2033.

| Key Insights | Details |

|---|---|

| Solar Street Lighting Market Size (2026E) | US$ 5.9 Billion |

| Market Value Forecast (2033F) | US$ 9.9 Billion |

| Projected Growth CAGR (2026 - 2033) | 7.6% |

| Historical Market Growth (2020 - 2025) | 6.3% |

Market Dynamics

Market Growth Drivers - Strong government renewable energy policies and infrastructure programs worldwide are accelerating large-scale adoption of solar street lighting systems

Government initiatives and renewable energy policies are among the most powerful drivers accelerating the growth of the solar street lighting market globally. In India, the Ministry of New and Renewable Energy (MNRE) has been actively deploying solar-powered public lighting systems across rural and semi-urban regions through programs such as the National Solar Mission and PM-KUSUM Scheme, covering thousands of villages. In the United States, the Bipartisan Infrastructure Law of 2021 allocated more than US$7.5 billion for clean energy and infrastructure modernization, including energy-efficient municipal lighting upgrades.

The New York State Public Service Commission approved policies allowing municipalities to offset street-lighting costs through solar energy credits, encouraging local governments to adopt solar lighting systems. In Europe, policy frameworks such as the European Green Deal and Fit for 55 aim to reduce greenhouse gas emissions by at least 55%. These global policy initiatives are collectively creating steady procurement pipelines and large-scale deployment opportunities for solar street lighting providers worldwide.

A rapid decline in solar PV module prices and longer-lasting lithium battery technologies is improving affordability of solar street lighting systems

The steady decline in solar panel and battery costs has significantly improved the economic viability of solar street lighting systems worldwide. According to the International Renewable Energy Agency, the global average price of solar photovoltaic modules dropped by more than 90% between 2010 and 2023, making solar-powered lighting solutions far more affordable compared to traditional grid-connected infrastructure. At the same time, advancements in LiFePO4 (Lithium Iron Phosphate) battery technology have increased operational lifespans to more than 10 years, reducing long-term maintenance and replacement costs.

China’s lithium battery solar street lighting industry alone is valued at over US$200 million, and exports from Yangzhou surged by nearly 300% within just ten months in 2024. Industry projections suggest that lithium batteries will power more than 60% of solar street lighting systems globally. As equipment prices continue to fall, municipalities with limited capital budgets are increasingly considering solar street lighting due to shorter payback periods and reduced lifecycle costs.

Restraint - High upfront installation costs of solar street lighting systems remain a major financial barrier for municipalities in developing regions

Despite strong long-term cost advantages, the high initial investment required for solar street lighting systems remains a key barrier to adoption, especially in developing economies with limited financial resources. Installing solar street lighting requires purchasing high-efficiency monocrystalline solar panels, lithium-ion battery storage units, intelligent controllers, and integrated LED lighting fixtures, which can increase upfront costs by 30% compared to traditional grid-connected street lighting systems.

For municipalities in regions such as Sub-Saharan Africa and parts of Southeast Asia, infrastructure budgets are often constrained, and access to affordable financing remains limited. As a result, many local governments struggle to allocate sufficient capital for large-scale solar lighting projects, even though these systems deliver long-term energy savings and reduced operational costs. Without adequate financial support mechanisms such as government subsidies, concessional loans, or public-private partnership models, many cities delay solar lighting adoption, slowing market penetration across lower-income regions despite the clear long-term economic benefits.

Solar street lighting performance varies across regions due to dependence on sunlight availability and changing climatic and seasonal conditions

Solar street lighting systems depend heavily on solar radiation levels, which creates performance variability across different geographic regions and seasonal conditions. In areas experiencing frequent cloud cover, high humidity, or limited sunlight hours, such as Northern Europe, certain parts of Canada, and monsoon-prone regions in Southeast Asia, solar panels may generate insufficient energy to support continuous overnight lighting.

Even advanced lithium battery systems typically provide only three to five days of backup power under low-irradiance conditions. Companies such as Leadsun have attempted to address this challenge by designing systems with optimized solar panel-to-battery ratios and enhanced energy storage capacity. However, the inherent dependence on solar energy generation still limits system reliability in regions with weak sunlight availability. As a result, municipalities in these areas often prefer hybrid or grid-connected lighting systems, which can reduce demand growth for fully solar-powered street lighting solutions in certain climates.

Opportunities - Integration of IoT platforms, smart sensors, and remote monitoring technologies is transforming solar street lighting into intelligent infrastructure systems

The integration of solar street lighting with Internet of Things (IoT) platforms and intelligent energy management systems presents a significant growth opportunity for market participants. Smart solar street lights equipped with motion sensors, adaptive dimming capabilities, and real-time monitoring software can reduce energy consumption by up to 60% compared with traditional fixed-output lighting systems. Companies such as Leadsun have introduced advanced wireless management technologies such as the EDGE platform, enabling features including GPS tracking, remote diagnostics, battery health monitoring, and automated fault detection across large lighting networks.

The rapid expansion of smart city initiatives further strengthens this opportunity. China currently leads the world in smart city pilot programs, while India has implemented more than 5,002 smart city projects, with approximately 2,740 still in progress. In North America, government programs such as the U.S. Department of Energy's Better Buildings initiative are supporting smart infrastructure investments. These trends are accelerating demand for intelligent, IoT-enabled solar street lighting systems globally.

Growing rural electrification programs in developing countries are creating significant demand for off-grid solar street lighting solutions

Off-grid electrification initiatives in developing economies represent a major opportunity for the Solar Street Lighting market. According to the International Energy Agency, nearly 770 million people worldwide still lack reliable access to electricity, particularly in rural and remote regions. Solar street lighting systems provide a cost-effective solution for improving public safety, mobility, and community infrastructure in areas without stable grid access.

Governments in countries such as India, Nigeria, Indonesia, and Vietnam are prioritizing solar street lighting within rural development and infrastructure programs, often supported by funding from international institutions, including the World Bank and the Asian Development Bank. In India, large-scale deployment programs implemented by the Ministry of New and Renewable Energy and Energy Efficiency Services Limited have accelerated adoption across hundreds of towns and villages. A notable example includes Signify installing solar street lights across 43 villages on Majuli Island in Assam, benefiting more than 32,000 residents. Such initiatives highlight the strong growth potential for solar lighting providers.

Category-wise Analysis

By Product Type Insights

Among all product types, standalone solar street lights represent the leading segment, accounting for approximately 35% of the total product-type market share. These systems operate independently of the electrical grid, eliminating the need for trenching, underground cabling, or connection to centralized power infrastructure. This makes them an ideal solution for off-grid rural regions, remote highways, and municipalities in developing economies. The high installation cost associated with conventional street lighting infrastructure in such areas, combined with ongoing electrification programs across India, Africa, and Southeast Asia, continues to drive strong procurement in this segment. Technological improvements are also strengthening adoption.

Advancements in high-efficiency monocrystalline solar panels and LiFePO4 battery technologies now offer operational lifespans exceeding ten years, significantly improving reliability and lowering maintenance requirements. As a result, standalone solar street lighting systems have become a practical and cost-effective option for governments and private organizations, reinforcing their commercial dominance across both public infrastructure projects and private installations worldwide.

By Component Insights

By component category, the solar panel segment leads market revenue, accounting for approximately 38% of the total component share. Solar panels act as the primary energy-generation units in solar street lighting systems and directly influence overall system efficiency, power output, and operational reliability. Continuous technological advancements have significantly improved panel performance. Innovations such as monocrystalline PERC (Passivated Emitter and Rear Cell) and bifacial solar panel technologies enable higher energy conversion rates, allowing greater power generation even from compact panel sizes typically used in pole-mounted street lighting systems.

According to the International Renewable Energy Agency (IRENA), solar photovoltaic efficiency has steadily improved over the past decade while manufacturing costs have declined significantly. This combination has reinforced the solar panel’s position as the most critical cost and performance driver in solar street lighting systems. Additionally, the increasing adoption of high-wattage panels for urban and commercial installations, along with deeper OEM integration by lighting manufacturers, continues to strengthen the solar panel segment’s revenue leadership.

By Power Capacity Insights

The 40 W - 100 W power capacity range is the dominant segment in the market, accounting for approximately 42% of total market revenue. This capacity range offers an ideal balance between lighting performance, energy efficiency, and system affordability, making it the most widely adopted specification for various public lighting applications. Systems in this range are commonly used for municipal road lighting, residential streets, commercial parking areas, and institutional campuses.

One of the key advantages of this capacity segment is its compatibility with a wide variety of pole heights, mounting structures, and battery configurations, allowing flexible deployment across different infrastructure environments. Urban planners and municipal authorities across Asia Pacific and Europe frequently specify 40 W - 100 W solar street lighting systems for primary and secondary roads, as they effectively meet illumination standards and safety requirements. This power range also complies with established lighting guidelines set by organizations such as the Illuminating Engineering Society (IES) and the European Committee for Standardization (CEN), further supporting its strong market preference.

By Installation Type Insights

By installation category, new installations represent the dominant segment, accounting for approximately 64% of the total market share. Rapid urbanization, expanding infrastructure development, and increasing investments in public lighting projects across emerging economies are driving a strong pipeline of new solar street lighting deployments. Countries such as India, China, Nigeria, and Brazil are witnessing large-scale development of new roads, residential areas, and public infrastructure, creating significant demand for new lighting installations.

Government-led smart city programs and rural electrification initiatives, particularly in the Asia Pacific region, are also encouraging the adoption of solar lighting solutions in newly developed areas. In many cases, solar street lights are being installed as the primary lighting solution rather than replacing conventional grid-based systems. Additionally, international funding from institutions such as the World Bank and the Asian Development Bank (ADB) for infrastructure development across South Asia, Africa, and Southeast Asia continues to support solar street lighting projects, helping maintain the strong growth and dominance of the new installation segment.

By End-user Insights

The Municipal/Government segment is the leading end-user category, accounting for approximately 45% of total market demand. Public sector organizations and local governments remain the largest and most consistent buyers of solar street lighting systems, primarily driven by the need to provide energy-efficient, reliable, and cost-effective public lighting infrastructure. Government initiatives aimed at reducing electricity consumption, lowering long-term operational costs, and achieving carbon reduction and sustainability targets are strongly encouraging the adoption of solar lighting solutions. Large-scale procurement programs and aggregated purchasing models are further accelerating deployments.

In India, Energy Efficiency Services Limited (EESL) has facilitated large-volume installations across multiple urban local bodies through centralized procurement frameworks. Similarly, in the United States, the Department of Energy (DOE) actively promotes the transition to LED and solar-powered street lighting systems among municipal utilities. These initiatives, combined with growing environmental regulations and public safety priorities, continue to strengthen government leadership in global solar street lighting adoption.

Regional Insights

North America Solar Street Lighting Trends

The United States leads the North America Solar Street Lighting market, supported by a combination of federal clean energy incentives, state renewable portfolio standards, and large-scale municipal infrastructure modernization initiatives. The Bipartisan Infrastructure Law (BIL) of 2021 allocated more than US$ 7.5 billion for clean energy and public infrastructure projects, including targeted funding for energy-efficient street lighting upgrades. Several states, including California, New York, and Texas, have integrated solar street lighting into their broader net-zero and sustainability roadmaps, creating steady demand for these systems.

The New York State Public Service Commission’s approval of solar net-metering credits for municipal street lighting accounts has lowered financial barriers for city and town governments. Canada is emerging as an important secondary market, especially in remote northern and Indigenous communities where extending traditional power grids is expensive. Programs led by Natural Resources Canada (NRCan) are supporting renewable energy projects in remote areas, promoting off-grid solar lighting solutions. Furthermore, post-pandemic infrastructure recovery spending and growing interest in resilient, low-maintenance public lighting systems are strengthening demand across both urban and rural Canadian markets, supporting steady regional growth.

Europe Solar Street Lighting Trends

Europe represents a mature yet steadily expanding Solar Street Lighting market, with Germany, France, Spain, and the United Kingdom leading in deployment and technology innovation. The European Union’s Fit for 55 legislative package, which aims to reduce greenhouse gas emissions by at least 55%, is creating strong policy momentum for replacing conventional public lighting with solar-powered alternatives. In addition, the EU Energy Efficiency Directive requires measurable improvements in public sector energy performance, encouraging both new solar installations and retrofit programs across municipal lighting networks.

The United Kingdom has shown a strong commitment to sustainable and smart street lighting infrastructure, with local authorities such as Oxfordshire County Council investing in connected solar lighting systems. Spain’s high solar irradiance and ambitious renewable energy goals have made it one of Europe’s fastest-growing markets for solar lighting adoption. Meanwhile, Germany and France are increasing investments in integrating solar street lights with smart city platforms, using IoT-based monitoring systems to improve energy management and streamline maintenance across large urban lighting networks.

Asia Pacific Solar Street Lighting Trends

Asia Pacific is both the largest and the fastest-growing regional market for Solar Street Lighting, driven primarily by strong demand from China, India, and countries across the ASEAN region. China dominates the global market in terms of both manufacturing capacity and domestic deployment. Provincial governments, particularly in regions such as Guangdong, are offering LED subsidies and launching large-scale smart city pilot programs, which are increasing procurement of solar street lighting systems.

The country also hosts the world’s highest number of smart city pilot projects, sustaining strong demand for integrated and intelligent solar lighting solutions in urban and peri-urban areas. India represents another major growth engine, supported by initiatives from the Ministry of New and Renewable Energy (MNRE) and large-scale deployment programs under the PM-Kusum scheme and EESL contracts. Projects such as Signify’s solar lighting initiative across 43 villages on Majuli Island in Assam demonstrate scalable models for rural electrification. At the same time, Vietnam, Indonesia, and the Philippines are accelerating adoption through renewable energy policies and international development funding.

Competitive Landscape

The global Solar Street Lighting market is moderately fragmented, with both large multinational lighting companies and specialized regional manufacturers competing across product innovation, technology integration, and geographic reach. Major players such as Signify maintain strong market positions due to their global distribution networks, well-established brand recognition under the Philips portfolio, and continuous investment in research and development. In 2024, the company allocated approximately 4.34% of its total revenue to R&D activities, supporting innovation in advanced lighting solutions.

Leading companies differentiate themselves through smart IoT integration, modular all-in-one lighting systems, and proprietary wireless energy management platforms. At the same time, mid-sized and regional manufacturers, particularly in China and India, focus on competitive pricing and customized solutions tailored to local market requirements. New commercial models are also shaping the competitive landscape, including Solar-as-a-Service (SaaS) and Energy Service Company (ESCO) arrangements. These models reduce upfront investment costs for municipalities and accelerate project implementation, enabling faster adoption across both developed and developing regions.

Key Market Developments

- In October 2025: Signify expanded its professional solar lighting portfolio with the launch of SunStay Pro gen2 and SunStay Pro gen2 mini. These integrated solar streetlights feature motion-sensing technology, hybrid charging capability, and an aluminum housing made from 80% recycled material, designed for campuses, bike paths, and pedestrian areas.

- In May 2023: Signify partnered with Evangelical Social Action Forum to deploy 100 solar streetlights across 43 villages on Majuli Island in Assam, India. The project improved night-time safety and sustainable energy access, benefiting more than 32,000 residents under the company’s rural electrification initiative.

Companies Covered in Solar Street Lighting Market

- Anhui Longvolt Energy

- Bridgelux

- Covimed

- Dragons Breath Solar

- Exide Industries

- Greenshine New Energy

- Leadsun

- Omegasolar

- Sepco

- Signify

- Sokoyo Solar Lighting

- Sunna Design

- Solar Lighting International

- Solux

- Sunmaster

- Shenzhen Spark Co. Ltd.

- Urja Global Ltd.

- Su-Kam Power Systems

- Kingshine Solar Lighting

- Fonroche Éclairage

Frequently Asked Questions

The global Solar Street Lighting market is estimated to be valued at US$ 5.9 Billion in 2026 and is projected to grow to US$ 9.9 Billion by 2033, advancing at a CAGR of 7.6% during the forecast period, supported by government clean energy mandates and declining solar and battery technology costs.

The primary drivers include accelerating government renewable energy policies from institutions such as the MNRE, U.S. DOE, and the European Commission, the sustained decline in solar PV and lithium battery costs , with IRENA documenting over a 90% module cost reduction since 2010 , and the growing global imperative for off-grid public lighting infrastructure.

Standalone Solar Street Lights hold the leading product type position with approximately 35% market share. Their grid-independent design, zero cabling requirements, and suitability for remote and underserved electrification programs , supported by government schemes in India, Africa, and Southeast Asia , make them the most widely deployed solar street lighting configuration globally.

Asia Pacific leads the global Solar Street Lighting market, anchored by large-scale government procurement in China and India, the region's dominant manufacturing ecosystem, and a rapidly growing smart city project pipeline. China's record of smart city pilot programs and India's national solar lighting schemes collectively drive the region's market leadership.

Off-grid rural electrification across South Asia and Sub-Saharan Africa constitutes the largest near-term opportunity. With approximately 770 million people globally lacking electricity access per the IEA, combined with World Bank and ADB financing and national subsidy programs from governments such as India's MNRE, this segment is positioned to generate substantial procurement demand through 2033.

The global Solar Street Lighting market is served by leading players including Signify, Leadsun, Anhui Longvolt Energy, Greenshine New Energy, Exide Industries, Sokoyo Solar Lighting, Sunna Design, Sepco, Bridgelux, Solar Lighting International, Solux, Sunmaster, Omegasolar, Dragons Breath Solar, and Covimed, among others.