- Renewable Energy

- Biofuel Powered Machinery Market

Biofuel Powered Machinery Market Size, Share, and Growth Forecast, 2026 - 2033

Biofuel Powered Machinery Market by Fuel Type (Biodiesel, Bioethanol, Biogas, Others), End User (Agriculture, Construction, Industrial, Others), and Regional Analysis for 2026 - 2033

Biofuel Powered Machinery Market Size and Trends Analysis

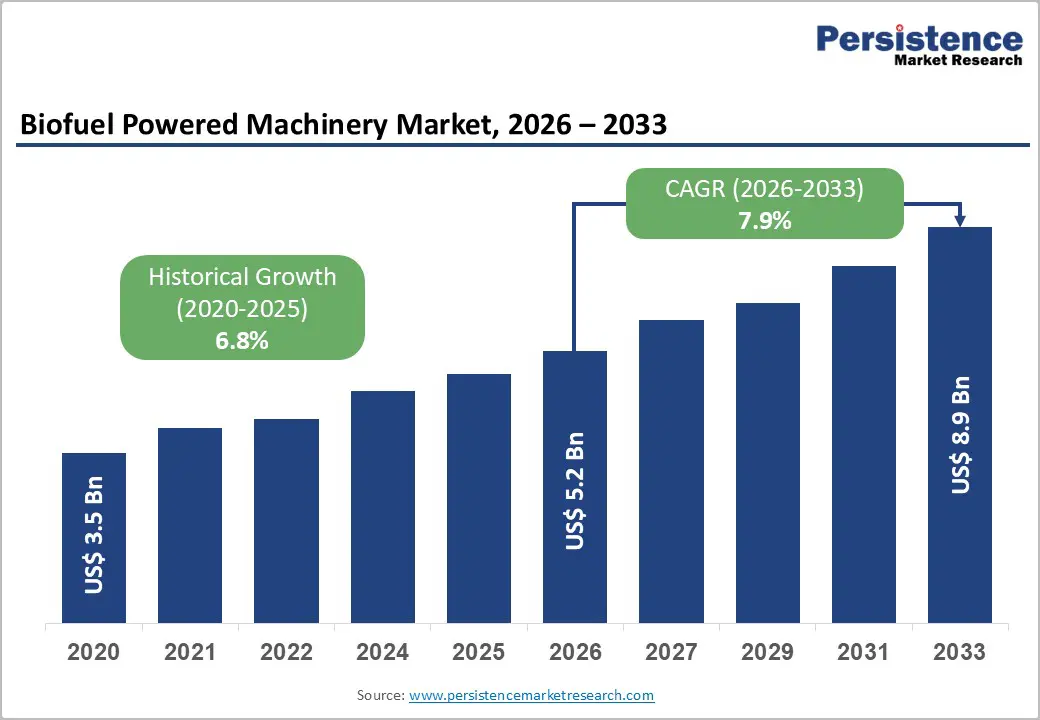

The global biofuel powered machinery market size is supposed to be valued at US$ 5.2 billion in 2026 and is projected to reach US$ 8.9 billion by 2033, growing at a CAGR of 7.9% between 2026 and 2033.

This robust expansion is primarily driven by escalating global mandates to reduce carbon emissions across agriculture and construction sectors, combined with strong policy support for renewable energy adoption.

The European Union’s Renewable Energy Directive III (RED III) mandates a minimum of 42.5% renewable energy in the EU’s total energy consumption by 2030, compelling machinery OEMs and fleet operators to accelerate their transition toward biofuel-powered equipment. Simultaneously, declining biofuel production costs, expanding feedstock availability, and growing awareness of lifecycle emission benefits are reinforcing the commercial viability of biofuel-compatible machinery across key global markets.

Key Industry Highlights:

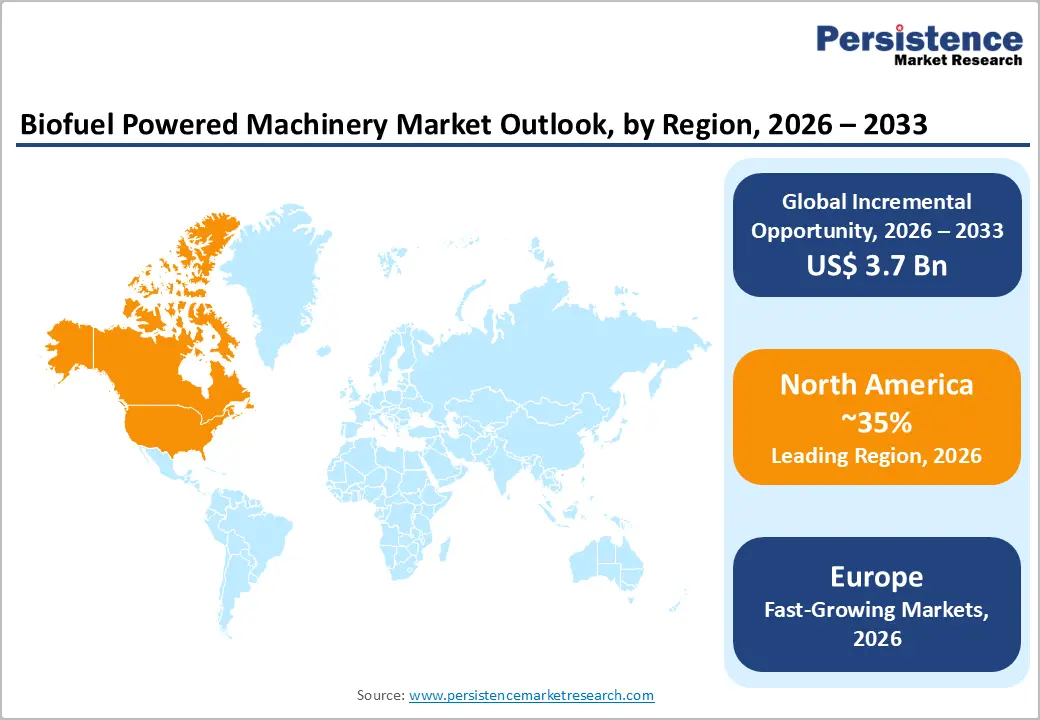

- Leading Region: North America leads the global biofuel-powered machinery market, driven by the U.S. Renewable Fuel Standard (RFS), robust OEM presence from John Deere and CNH Industrial N.V., and well-established biofuel production and distribution infrastructure supporting large-scale fleet adoption across agricultural and construction sectors.

- Fastest Growing Region: Asia Pacific is the fastest-growing regional market, propelled by India’s 20% ethanol blending target, China’s E10 mandate, and Indonesia’s B35 biodiesel program, collectively generating unprecedented demand for biofuel-compatible agricultural and construction machinery.

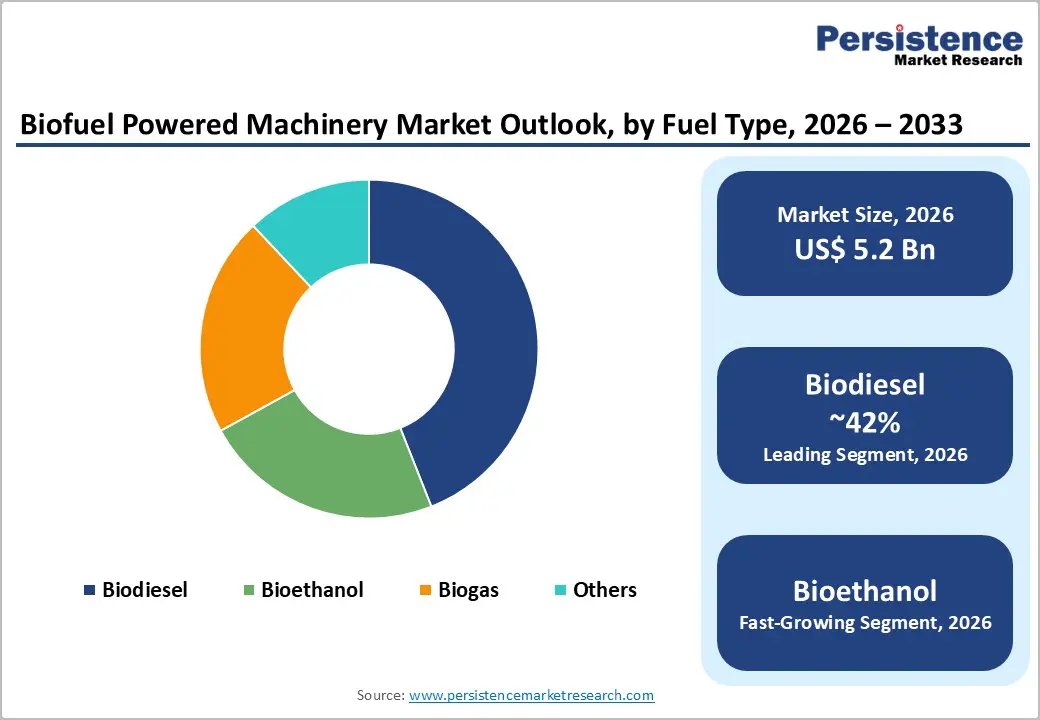

- Dominant Segment: Biodiesel holds the leading position in the Fuel Type category with approximately 42% market share in 2025, driven by broad regulatory support and seamless compatibility with existing diesel engine infrastructure across agriculture and construction sectors globally.

- Fastest Growing Segment: Biogas is the fastest-growing fuel type segment, supported by rising government investment in anaerobic digestion infrastructure and growing incentives for biomethane use in off-road machinery applications, particularly in Europe and the Asia Pacific.

- Key Opportunity: The construction sector’s decarbonization imperative, amplified by green procurement mandates under the U.S. Bipartisan Infrastructure Law and the EU Taxonomy Regulation, presents a major growth opportunity for manufacturers of biofuel-powered and heavy alternative-fuel equipment globally.

| Key Insights | Details |

|---|---|

| Biofuel-Powered Machinery Market Size (2026E) | US$ 5.2 Bn |

| Market Value Forecast (2033F) | US$ 8.9 Bn |

| Projected Growth CAGR (2026 - 2033) | 7.9% |

| Historical Market Growth (2020 - 2025) | 6.8% |

Market Dynamics

Key Growth Drivers

Stringent Government Emission Regulations and Biofuel Mandates

Governments across the globe are enforcing increasingly stringent emission standards compelling key industries to transition toward alternative fuel equipment and low-carbon machinery solutions. The U.S. Environmental Protection Agency (EPA) administers the Renewable Fuel Standard (RFS) program, which mandates progressively increasing volumes of renewable fuels including biodiesel and cellulosic ethanol in transportation and off-road applications, directly driving demand for biodiesel-powered engines and ethanol fuel machinery.

The European Union’s Fit for 55 legislative package targets a 55% reduction in greenhouse gas emissions by 2030, compelling equipment manufacturers to accelerate investments in biofuel compatibility. According to the International Energy Agency (IEA), the agriculture and construction sectors together account for approximately 15% of global energy-related CO2 emissions. These coordinated regulatory frameworks create a sustained demand environment for biofuel-powered equipment, driving long-term market expansion across all major geographies.

Rising Feedstock Availability and Declining Biofuel Production Costs

The economics of biofuel production have improved substantially over the past decade, making renewable fuel machinery increasingly cost-competitive with conventional diesel alternatives. According to the International Renewable Energy Agency (IRENA), the cost of producing biodiesel from vegetable oils declined by approximately 30% between 2010 and 2023, driven by process optimization and scale-up investments in facilities. Global biodiesel production reached approximately 47 billion liters in 2023, per data from the U.S. Energy Information Administration (EIA), reflecting growing feedstock supply from soybean, rapeseed, and waste cooking oil streams.

In Brazil and the United States, abundant ethanol feedstocks, sugarcane and corn, respectively, have enabled large-scale deployment of ethanol fuel machinery in agricultural and construction operations. These favorable cost and supply dynamics are collectively reducing the total cost of ownership for biofuel machinery operators, broadening commercial uptake and accelerating global market adoption.

Market Restraining Factors

High Initial Equipment Costs and Retrofitting Challenges

A significant barrier to the widespread adoption of biofuel-powered machinery is the elevated upfront capital expenditure required for purpose-built or retrofitted biofuel-compatible equipment. Biofuel-compatible engines require specialized materials and fuel system seals that are resistant to fuel acidity, increasing manufacturing costs by an estimated 10-20% compared to conventional diesel engines, per industry engineering assessments.

SAE International has documented that retrofitting existing fleet machinery to handle high-blend biofuels such as B20 or B100 can cost operators between US$ 3,000 and US$ 15,000 per unit, representing a prohibitive financial burden for small and medium-scale operators in agriculture and construction. This cost barrier constrains adoption, particularly in price-sensitive emerging markets where operators prioritize short-term payback periods.

Feedstock Availability Volatility and Food-vs-Fuel Tensions

Biofuel feedstock supply chains remain vulnerable to agricultural commodity price volatility, creating a structural restraint on market expansion. The Food and Agriculture Organization (FAO) of the United Nations has highlighted persistent tensions between diverting key crops, including corn, soy, and sugarcane, toward biofuel production and global food supply security imperatives.

During the 2021-2022 global commodity price shock, prices for key biofuel feedstock crops surged by over 40%, directly undermining the cost competitiveness of biofuel machinery operations. Such volatility introduces significant procurement risk for fleet operators considering long-term biofuel adoption, particularly in developing economies where food security concerns outweigh large-scale first-generation biofuel mandates.

Biofuel-Powered Machinery Market Trends and Opportunities

Agricultural Sector Mechanization Growth and Biofuel Policy Alignment

The global agriculture sector represents one of the most compelling near-term growth frontiers for biofuel-powered equipment, particularly across rapidly mechanizing economies in Asia and Africa. According to the Food and Agriculture Organization (FAO), tractor demand in South Asia and Sub-Saharan Africa is projected to grow at over 5% annually through 2030, driven by intensifying agricultural mechanization and rising farm incomes.

In India, the government’s Sub-Mission on Agricultural Mechanization (SMAM) scheme has subsidized over 1.5 million farm machinery units to date, while the National Biofuel Policy 2018 targets 20% ethanol blending by 2025, directly incentivizing adoption of ethanol-compatible tractors and harvesters. Brazil’s RenovaBio program further accelerates the adoption of ethanol-fueled machinery in commercial agriculture, leveraging the world’s most cost-competitive sugarcane-based ethanol industry. OEMs investing in B20 and B100-compatible agricultural equipment are uniquely positioned to capture this structural demand surge.

Construction Sector Decarbonization and Green Procurement Mandates

The global construction industry faces mounting pressure to decarbonize its heavy equipment fleet, creating a high-value growth opportunity for manufacturers of biofuel- and alternative-fuel-powered equipment. The United Nations Environment Program (UNEP) estimates that construction accounts for approximately 38% of global CO2 emissions when including materials production and operations. Major economies are embedding sustainability requirements in public infrastructure procurement frameworks.

The U.S. Bipartisan Infrastructure Law allocates over US$ 1.2 trillion in infrastructure spending with progressive sustainability clauses, while the UK’s Net Zero Strategy mandates low-emission machinery on public-sector construction projects. Caterpillar Inc., Volvo Construction Equipment, and Komatsu Ltd. have each validated their construction machinery portfolios for biofuel blends including HVO100 and B20, indicating a structural pivot in heavy equipment markets toward cleaner fuel solutions over the forecast period.

Category-wise Analysis

Fuel Type Insights

Biodiesel dominates the biofuel powered machinery market by fuel type, accounting for approximately 42% of total revenue share in 2026. Its leading position stems from high compatibility with existing diesel engine infrastructure, which significantly lowers conversion barriers for fleet operators. B20 (20% biodiesel blend) and B100 (pure biodiesel) formulations are certified for use across a broad range of off-road machinery by leading OEMs, including John Deere, CNH Industrial N.V., and AGCO Corporation.

According to the U.S. Energy Information Administration (EIA), biodiesel consumption in the U.S. off-road sector alone exceeded 1.8 billion gallons in 2023, underscoring the fuel’s deep commercial penetration. Biodiesel’s superior lubricity reduces particulate emissions, and compatibility with existing fuel distribution networks makes biodiesel-powered engines the preferred choice for agriculture and construction operations globally. The increasing utilization of advanced feedstocks, including used cooking oil and animal fats is further enhancing the environmental credentials and cost profile of biodiesel, reinforcing its dominant segment position.

End-user Insights

The agriculture segment leads the biofuel powered machinery market by end user, accounting for approximately 38% of total revenue share in 2025. This dominance reflects the sector’s intensive reliance on off-road diesel-powered machinery including tractors, combine harvesters, planters, sprayers, and irrigation equipment and the deliberate alignment of biofuel blending mandates with agricultural policy objectives in key markets. Brazil, the United States, and India have specifically designed their biofuel programs to incentivize fuel transitions within the agricultural sector.

Brazil’s RenovaBio program has driven large-scale adoption of bioethanol-powered farm machinery, backed by the world’s most cost-competitive sugarcane ethanol supply chain. The U.S. Department of Agriculture (USDA) has reported that over 60% of farm fuel consumption in corn belt states involves some form of biofuel blend. This strong policy-market alignment, combined with high machinery density in major agricultural economies, firmly cements agriculture as the leading end-user segment in the global biofuel-powered machinery market.

Regional Insights and Trends

North America Biofuel Powered Machinery Trends

The United States holds the dominant position in the North American biofuel-powered equipment landscape, underpinned by the Renewable Fuel Standard (RFS) program administered by the U.S. Environmental Protection Agency (EPA). The RFS mandates increasing volumes of renewable fuels including biodiesel and cellulosic ethanol in non-road fuel applications, directly stimulating new machinery purchases and fleet upgrades.

John Deere and CNH Industrial N.V. have significantly expanded their biofuel-compatible product portfolios, with multiple tractor, combine harvester, and sprayer models certified for B20 and higher biodiesel blends. The U.S. also operates one of the world’s most mature biofuel production and distribution infrastructures, reducing operational barriers for fleet operators.

Canada is emerging as a growing market, following the enactment of the Clean Fuel Regulations (CFR) in 2022, which mandate lifecycle carbon intensity reductions across fuel supply chains, indirectly stimulating the adoption of alternative fuel equipment in agriculture and forestry. The North American market as a whole benefits from a robust OEM presence, abundant feedstock supply, and strong policy continuity, collectively providing a favorable growth environment for biofuel-powered equipment manufacturers throughout the 2026 - 2033 forecast period.

Europe Biofuel Powered Machinery Trends

Europe is one of the most regulatory-active regions in the global biofuel-powered machinery market, driven by the European Union’s Renewable Energy Directive III (RED III) and the overarching European Green Deal, which targets climate neutrality by 2050. Germany is the largest single-country market in Europe, supported by a mature biodiesel production base — producing approximately 3.5 million tonnes in 2023 according to the European Biodiesel Board (EBB). France advances its bioethanol agenda through the E10 petrol mandate, while Spain and the United Kingdom are investing in second-generation advanced biofuel technologies and infrastructure.

The EU’s Fit for 55 package is compelling OEMs including Komatsu Ltd. and JCB to accelerate biofuel compatibility certifications for off-road equipment. Stage V emission norms for non-road mobile machinery (NRMM) are further incentivizing manufacturers to develop and offer renewable fuel machinery solutions across agricultural and construction segments. Western Europe’s well-developed biofuel distribution network reduces operational barriers, making it one of the world’s most favorable environments for large-scale fleet adoption of biofuel-powered equipment.

Asia Pacific Biofuel Powered Machinery Trends

Asia Pacific represents the fastest-growing regional market for biofuel-powered machinery, fueled by rapid agricultural mechanization, large-scale urban infrastructure expansion, and expansive government-led biofuel mandates. China has extended its E10 ethanol blending mandate across multiple provinces, while its vast agricultural sector continues to generate strong demand for biogas and biodiesel-compatible farm equipment. Japan’s Basic Hydrogen Strategy and the national decarbonization roadmap are opening investment avenues for advanced biofuel machinery in construction and industrial applications.

India represents a particularly high-growth market opportunity, with the National Biofuel Policy 2018 targeting 20% ethanol blending by 2025 and active policy support for biodiesel adoption in tractors and transport machinery. In Southeast Asia, Indonesia enforces a B35 biodiesel mandate among the world’s most ambitious while Malaysia operates a B20 mandate, both leveraging abundant palm oil feedstocks and generating substantial demand for compatible plantation and construction machinery. Kubota Corporation and AGCO Corporation are among the leading OEMs capitalizing on Asia Pacific’s rapidly expanding biofuel machinery market across the forecast period.

Competitive Landscape

The global biofuel-powered machinery market exhibits a moderately consolidated competitive structure, with a handful of multinational OEMs - led by John Deere, CNH Industrial N.V., AGCO Corporation, Caterpillar Inc., and Volvo Construction Equipment - collectively commanding a dominant revenue share. These incumbents leverage extensive dealer networks, strong brand equity, and deep R&D capabilities to maintain competitive advantage.

Key differentiators include biofuel blend compatibility certifications, fuel efficiency performance, after-sales support breadth, and total cost of ownership propositions. Market leaders are increasingly forming strategic partnerships with biofuel producers and investing in engine technologies capable of handling higher biodiesel and bioethanol blend ratios. Emerging trends include OEM-agronomist collaborations, telematics for real-time fuel monitoring, and modular powertrain architectures supporting multi-fuel flexibility.

Key Industry Developments

- In April, 2026, Optimus Technologies, Inc. and Sunoil Biodiesel B.V. announced a strategic commercial partnership aimed at accelerating the adoption of 100% biodiesel (B100) among heavy-duty vehicle fleets in the Netherlands. This collaboration represents Optimus’ official entry into the European market and introduces a scalable deployment model that integrates its advanced fuel system technology with a consistent supply of sustainable, waste-derived biodiesel.

- In January 2025, Volvo Construction Equipment announced that its entire Stage V-compliant machine range is now certified for operation on HVO100 (hydrotreated vegetable oil), delivering up to 90% lifecycle CO2 reduction versus conventional diesel, significantly advancing biofuel adoption across the construction machinery segment.

- In March 2024, John Deere unveiled its next-generation PowerTech™ engine series capable of operating on biodiesel blends up to B100 without hardware modification, reinforcing the company’s industry leadership in biofuel-compatible agricultural machinery across global markets.

- In September 2023, Kubota Corporation launched a new range of biogas-compatible compact tractors targeting the Southeast Asian market, with pilot deployments initiated in Indonesia and Thailand under local government biofuel incentive and subsidy programs.

Companies Covered in Biofuel Powered Machinery Market

- John Deere

- CNH Industrial N.V.

- AGCO Corporation

- Caterpillar Inc.

- Volvo Construction Equipment

- Komatsu Ltd.

- JCB

- Kubota Corporation

- MAN Energy Solutions

- Doosan Infracore

- Yanmar Holdings Co., Ltd.

- Deutz AG

- CLAAS KGaA mbH

- Mahindra & Mahindra Ltd.

Frequently Asked Questions

The global Biofuel Powered Machinery market is valued at US$ 5.2 Bn in 2026 and is projected to reach US$ 8.9 Bn by 2033, growing at a CAGR of 7.9% during 2026 - 2033. Historically, the market registered a CAGR of 6.8% between 2020 and 2025, driven by rising biofuel mandates and regulatory push for carbon-neutral machinery across agriculture and construction sectors worldwide.

Key demand drivers include stringent government emission regulations such as the U.S. Renewable Fuel Standard (RFS) and the EU’s Renewable Energy Directive III (RED III), rapid growth in global biofuel production reaching approximately 47 billion liters in 2023 per the U.S. Energy Information Administration (EIA) declining biofuel production costs per IRENA data, and mounting mandates to decarbonize fleet operations in agriculture and construction across key global economies.

Biodiesel is the dominant fuel type segment, accounting for approximately 42% of total market share in 2025. Its leadership is underpinned by strong regulatory backing, seamless compatibility with existing diesel engine platforms, and widespread OEM certification including from John Deere and CNH Industrial N.V. for B20 and B100 formulations across agricultural and construction machinery applications globally.

North America is the leading regional market, anchored by the U.S. Renewable Fuel Standard (RFS) program, a well-established biofuel production and distribution infrastructure, and the presence of dominant global OEMs including John Deere and Caterpillar Inc. The region’s robust regulatory clarity, abundant feedstock supply, and widespread commercial fleet adoption of biodiesel-powered engines and ethanol fuel machinery collectively reinforce its market leadership position.

Key opportunities include the construction sector’s decarbonization imperative, driven by green procurement mandates under the U.S. Bipartisan Infrastructure Law and the EU Taxonomy Regulation, and the rapid agricultural mechanization across Asia Pacific particularly in India and Southeast Asia generating strong near-term demand for B20 and B100-compatible farm machinery and heavy construction equipment from leading global OEMs.

Leading companies operating in the global Biofuel Powered Machinery market include John Deere, CNH Industrial N.V., AGCO Corporation, Caterpillar Inc., Volvo Construction Equipment, Komatsu Ltd., JCB, Kubota Corporation, MAN Energy Solutions, and Doosan Infracore, among other regional and specialty machinery manufacturers contributing to global market revenues.