- Renewable Energy

- Grey Hydrogen Market

Grey Hydrogen Market Size, Share, and Growth Forecast 2026 - 2033

Grey Hydrogen Market by Production Technology (Steam Methane Reforming (SMR), Coal Gasification, Partial Oxidation of Hydrocarbons, Others), by Feedstock (Natural Gas, Coal, Oil, Petroleum Coke), Industry (Petroleum Refining, Fertilizers, Methanol Production, Chemicals & Petrochemicals, Steel & Metallurgy, Power Generation, Others), and Regional Analysis, 2026-2033

Grey Hydrogen Market Size and Trend Analysis

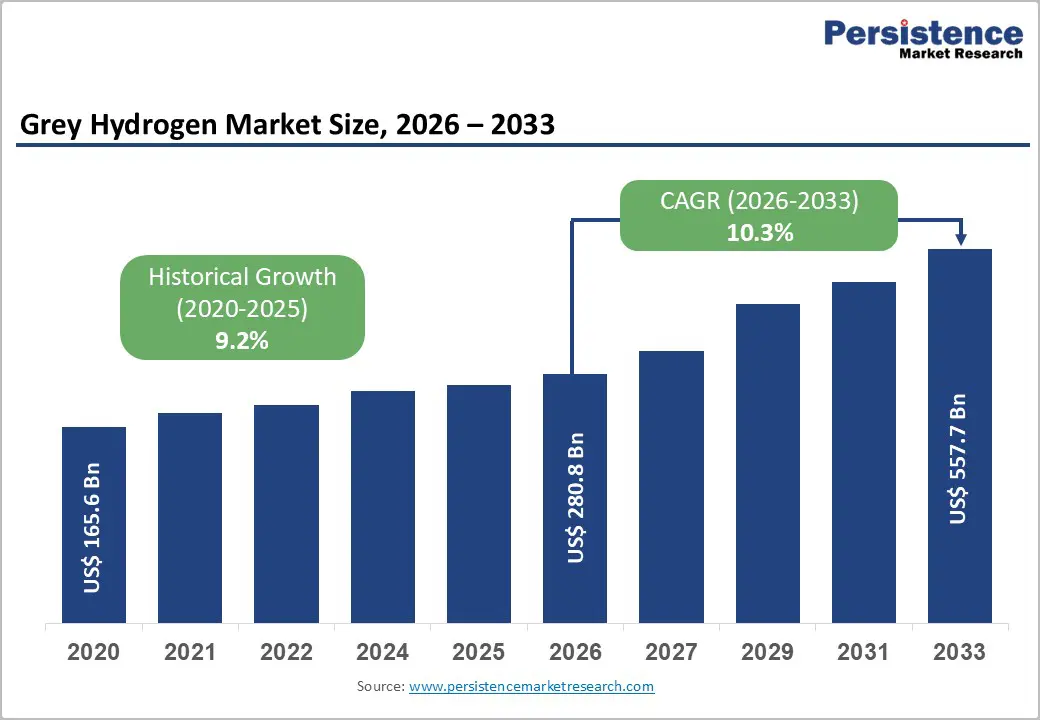

The global grey hydrogen market size is expected to be valued at US$ 280.8 billion in 2026 and projected to reach US$ 557.7 billion by 2033, growing at a CAGR of 10.3% between 2026 and 2033. Growth is driven by sustained demand from refining, fertilizers, and chemical industries, where hydrogen remains indispensable for core processes.

Large-scale ammonia production exceeding 180 million tons annually and extensive refining operations requiring continuous hydrogen for hydro treating underpin market stability. Despite decarbonization pressures, grey hydrogen maintains dominance due to cost efficiency, established infrastructure, and reliable supply, ensuring its critical role in supporting global industrial output.

Key Industry Highlights:

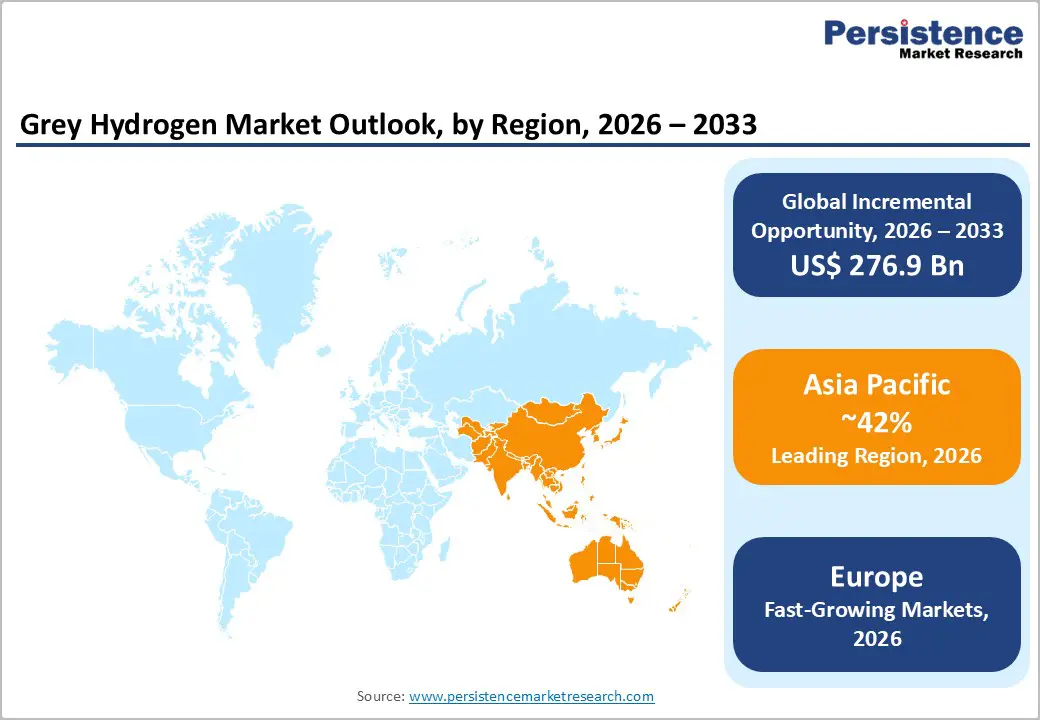

- Leading Region: Asia Pacific dominates with 42% share in 2025, driven by large-scale industrial production across China and India.

- Fastest-Growing Region: Europe leads with a 8.5% CAGR, supported by energy transition policies.

- Leading Production Technology: Steam Methane Reforming (SMR) leads with a 65% share, owing to cost efficiency and established infrastructure.

- Leading End-Use Industry: Fertilizers hold a 45% share, driven by strong global ammonia demand.

- Key Market Opportunity: Partial Oxidation (POX) presents strong potential in heavy industries due to feedstock flexibility and suitability for complex operations.

Market Dynamics

Drivers - Rising Industrial Demand from Fertilizer and Refining Sectors Driving Market Expansion

Fertilizer production drives grey hydrogen growth as ammonia synthesis consumes the majority of output. United Nations projections indicate that the global population will reach 9.7 billion by 2050, increasing fertilizer demand by nearly 50% to ensure food security. FAO data indicate that ammonia production requires about 175 kg of hydrogen per ton, which is supported by the current global capacity of about 185 million tons.

Refining activities further strengthen demand, with the International Energy Agency (IEA) reporting nearly 50 million tons of hydrogen consumption annually for desulfurization. Stricter fuel standards, such as IMO 2020, significantly increase hydrogen usage in hydroprocessing, reinforcing grey hydrogen’s indispensable role in maintaining fuel quality and ensuring compliance across global refining operations.

Expanding Steel and Chemical Industries Supporting Hydrogen Consumption

The steel industry’s gradual transition toward hydrogen-based reduction technologies is sustaining grey hydrogen demand, particularly in coal-dependent regions. According to the World Steel Association, global crude steel production reached 1.88 billion tons in 2023, with Asia accounting for approximately 72%, underscoring strong regional demand for hydrogen-intensive processes across industrial value chains.

In the chemicals sector, methanol production continues to rely heavily on grey hydrogen for synthesis. The European Chemical Industry Council (Cefic) projects chemical demand to rise by nearly 50% by 2050, driven by plastics and industrial applications. Combined with low production costs of $1-2 per kg (U.S. DOE), abundant feedstocks support scalable growth in developing economies.

Restraints - Intensifying Carbon Regulations and Emissions Costs Limiting Market Growth

Stringent environmental regulations and carbon pricing mechanisms are significantly restraining the expansion of grey hydrogen. The European Union Emissions Trading System (ETS) imposes carbon costs of €80-100 per ton of CO2, heavily impacting Steam Methane Reforming (SMR), which emits 9-12 kg CO2 per kg of hydrogen produced. IEA analysis indicates potential penalties of $1-2 per kg by 2030 under net-zero pathways, reducing cost competitiveness.

Additionally, China’s expanding carbon market, now covering the steel sector and nearly 40% of emissions, is increasing operational costs by 20-30% for unabated hydrogen processes. These regulatory pressures are accelerating the transition toward low-carbon alternatives, discouraging new investments in grey hydrogen infrastructure and limiting long-term market expansion potential.

Feedstock Price Volatility Increasing Production Cost Uncertainty

Grey hydrogen production is highly sensitive to fluctuations in feedstock prices, particularly natural gas and coal. Sharp increases, such as the 150% surge in natural gas prices in 2022 reported by the BP Statistical Review, have pushed SMR production costs to approximately $2-3 per kg, significantly affecting profitability and operational stability for producers.

Similarly, coal supply disruptions in key exporting regions, such as Australia, have affected the economics of coal gasification. According to World Bank projections, continued volatility in energy markets through 2030 is expected to further strain margins. Limited effectiveness of long-term hedging strategies adds uncertainty, discouraging large-scale capacity expansions and investment planning.

Opportunities - Advancing Partial Oxidation Technologies: Unlocking Flexible Hydrogen Production Pathways

Partial Oxidation (POX) is gaining traction as a strategic opportunity due to its ability to process diverse feedstocks such as oil and petroleum coke, particularly in steel and heavy industries. Support from initiatives such as the U.S. Department of Energy’s over $1 billion in funding for hydrogen hubs is accelerating the adoption of transitional hydrogen technologies. The IEA estimates POX could capture 15-20% market share by 2030.

Pilot projects by major industry players demonstrate yields up to 20% higher when processing heavier feedstocks, thereby enhancing efficiency and enabling cost optimization. This makes POX highly suitable for retrofitting existing facilities, especially in the Asia Pacific, where industrial infrastructure and feedstock diversity support scalable deployment, positioning the technology as a key enabler in the evolving grey hydrogen landscape.

Emerging Economy Policies and Industrialization Driving Hydrogen Demand Growth

Government-led initiatives in emerging economies are creating strong growth opportunities for grey hydrogen, particularly during the transition toward cleaner energy systems. India’s National Hydrogen Mission targets production of 5 million tons by 2030, with grey hydrogen expected to dominate initial supply due to cost advantages, as outlined by the Ministry of New and Renewable Energy.

Additionally, Indonesia is investing nearly $10 billion in coal gasification projects to strengthen domestic hydrogen and chemical output. Rapid industrialization across ASEAN nations is expected to drive growth exceeding 10% CAGR, positioning grey hydrogen as a critical bridge solution that supports economic expansion while enabling the gradual integration of low-carbon hydrogen technologies.

Category-wise Analysis

Production Technology Insights

Steam Methane Reforming (SMR) dominates the grey hydrogen market, accounting for approximately 65% of the market share in 2025 due to its technological maturity and well-established natural gas infrastructure. According to the International Energy Agency, SMRs account for nearly 75% of global hydrogen production, supported by cost advantages of around $1/kg in the U.S., driven by shale gas availability. Its scalability, with plants capable of producing over 10,000 tons per day, further reinforces its leadership position.

Partial Oxidation (POX) is emerging as the fastest-growing production technology, driven by its flexibility in processing heavier feedstocks like oil and petroleum coke. Increasing adoption in industrial retrofits and integration with complex refining and steel operations is accelerating its growth, particularly in regions with diverse feedstock availability and expanding heavy industrial infrastructure.

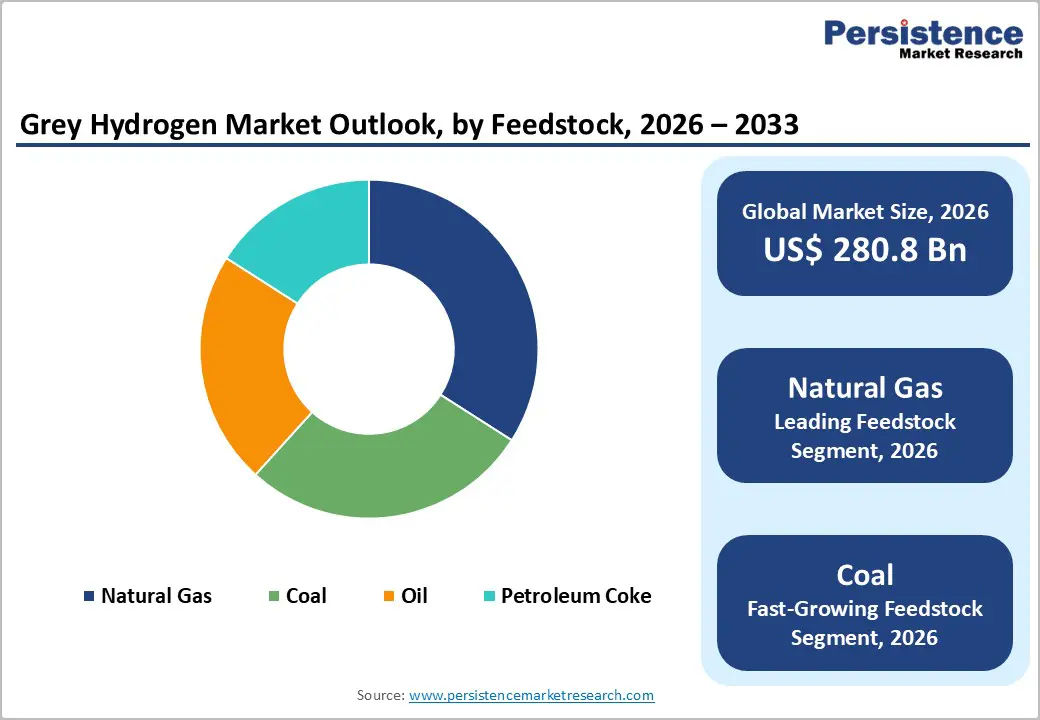

Feedstock Insights

Natural gas leads the grey hydrogen market with an estimated 55% share in 2025, driven by its widespread availability and cost efficiency. The U.S. Energy Information Administration notes that nearly 70% of hydrogen production relies on natural gas, supported by strong supply levels, such as over 600 billion cubic meters of output in the U.S. Additionally, the World Bank highlights a cost advantage of nearly 30% over coal-based production, reinforcing natural gas's dominance.

Coal is emerging as the fastest-growing feedstock, particularly in regions with abundant reserves and limited access to natural gas infrastructure. Expanding coal gasification projects in Asia are supporting increased adoption, enabling countries to leverage domestic resources for hydrogen production while meeting rising industrial demand across chemicals, fertilizers, and steel sectors.

Industry Insights

Fertilizers dominate the grey hydrogen market, holding approximately 45% of the market share in 2025, as ammonia production remains the largest consumer of hydrogen. The Food and Agriculture Organization reports global ammonia capacity at around 185 million tons, requiring substantial hydrogen input for synthesis. Rising global food demand, as projected by the United Nations, continues to strengthen fertilizer production, ensuring sustained dominance of this segment.

Steel & metallurgy is emerging as the fastest-growing end-use industry, driven by increasing adoption of hydrogen-based processes in iron and steel production. Industrial decarbonization efforts and advancements in hydrogen utilization are encouraging steel manufacturers to integrate hydrogen into production cycles, particularly in regions with strong industrial growth and evolving environmental regulations.

Regional Insights

North America Grey Hydrogen Market Trends and Insights

North America holds a significant share of the grey hydrogen market, accounting for approximately 28% in 2025, driven primarily by the United States’ strong refining base and abundant shale gas resources. The U.S. produces nearly 10 million tons of hydrogen annually, according to the EIA, supporting large-scale refining and petrochemical operations. Policy support through the Inflation Reduction Act and Department of Energy hydrogen hub initiatives, particularly in Texas, further strengthens infrastructure and production capabilities.

Canada complements regional growth through its oil sands operations, where hydrogen is essential for upgrading processes. Expanding gasification projects in Alberta are enhancing production capacity, while integration with industrial applications ensures continued demand. The region’s mature energy ecosystem and policy-backed transition strategies position it as a stable and influential contributor to the global grey hydrogen market.

Europe Grey Hydrogen Market Trends and Insights

Europe’s grey hydrogen market is characterized by strong industrial demand and a structured transition toward low-carbon alternatives. The market is projected to grow at a CAGR of around 8.5% between 2026 and 2033, supported by continued consumption in the refining and steel sectors. Germany alone consumes nearly 2 million tons of hydrogen annually in steel production, with companies like Thyssenkrupp driving demand across heavy industries.

The European Union’s hydrogen strategy targeting 20 million tons of hydrogen supply further supports market activity, while countries such as France and Spain expand refining operations through major players like TotalEnergies. Although policies like the Carbon Border Adjustment Mechanism (CBAM) increase pressure on emissions-intensive production, grey hydrogen remains a transitional solution, sustaining industrial operations.

Asia Pacific Grey Hydrogen Market Trends and Insights

Asia Pacific dominates the global grey hydrogen market, with an estimated 42% share in 2025, driven by large-scale industrialization and the extensive use of coal and natural gas as feedstocks. China leads the region, producing approximately 25 million tons of hydrogen annually, largely via coal-based processes, according to the National Energy Administration. Strong demand from refining, chemicals, and fertilizers further reinforces regional dominance.

India is also expanding its hydrogen capacity, targeting 5 million tons of production through SMR under national initiatives. Meanwhile, Japan and ASEAN countries are witnessing rising demand from the manufacturing and industrial sectors. Indonesia’s focus on petroleum coke-based gasification highlights feedstock diversification, supporting regional growth and strengthening the Asia Pacific’s position as the global hub for grey hydrogen production and consumption.

Competitive Landscape

The grey hydrogen market is characterized by a highly consolidated structure, dominated by large integrated producers operating captive production units aligned with refining and chemical facilities. Competitive advantage is driven by economies of scale, access to reliable feedstock supply, and the ability to operate large-scale Steam Methane Reforming (SMR) infrastructure efficiently. Continuous investments in process optimization and operational efficiency further strengthen market positioning.

Strategic focus is shifting toward enhancing production efficiency while preparing for the energy transition. Players are increasingly integrating hybrid production models that combine conventional grey hydrogen with lower-carbon alternatives, improving flexibility. Innovation in reforming technologies and feedstock diversification are emerging as key differentiators, enabling long-term competitiveness.

Key Developments:

- In March 2025, Air Products and Chemicals Inc. launched a $4.5 billion Steam Methane Reforming (SMR) facility in Saudi Arabia, adding over 1.5 million tons of hydrogen production capacity annually, strengthening large-scale supply for refining and industrial applications.

- In July 2024, Linde plc expanded its Texas-based hydrogen plant, significantly boosting supply to nearby refining and petrochemical industries while enhancing regional production efficiency through advanced SMR technology and integrated infrastructure support systems.

- In January 2025, Sinopec commissioned a major coal gasification project in China, increasing hydrogen output by around 2 million tons annually to support fertilizer production, thereby reinforcing its position as a large-scale industrial hydrogen supplier.

Companies Covered in Grey Hydrogen Market

- Air Liquide

- Linde plc

- Air Products and Chemicals Inc.

- ExxonMobil Corporation

- Shell plc

- BP plc

- TotalEnergies SE

- Sinopec

- China National Petroleum Corporation

- Chevron Corporation

- Indian Oil Corporation Limited

- Reliance Industries Limited

- Messer Group GmbH

- Iwatani Corporation

- Mitsubishi Heavy Industries Ltd.

Frequently Asked Questions

US$ 280.8 billion, driven by strong demand from the refining and fertilizers industries.

Fertilizers dominate with 45% share, as hydrogen remains essential for ammonia production supporting global food demand.

Asia Pacific leads with 42% share, driven by large-scale production in China and India.

Partial Oxidation (POX) technology offers growth potential in steel and refining due to feedstock flexibility.

Major companies include Air Products and Chemicals Inc., Linde plc, Shell plc, and Sinopec.