- Renewable Energy

- Concentrated Solar Power Market

Concentrated Solar Power Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Concentrated Solar Power Market by Technology (Parabolic Trough Systems, Power Tower / Central Receiver Systems, Linear Fresnel Reflector Systems, Dish Stirling Systems), Capacity (Below 50 MW, 50-150 MW, Above 150 MW), Application (Utility-Scale Power Generation, Industrial Process Heat, Desalination, Enhanced Oil Recovery, Others), and Region Analysis for 2026 to 2033

Concentrated Solar Power Market Share and Trends Analysis

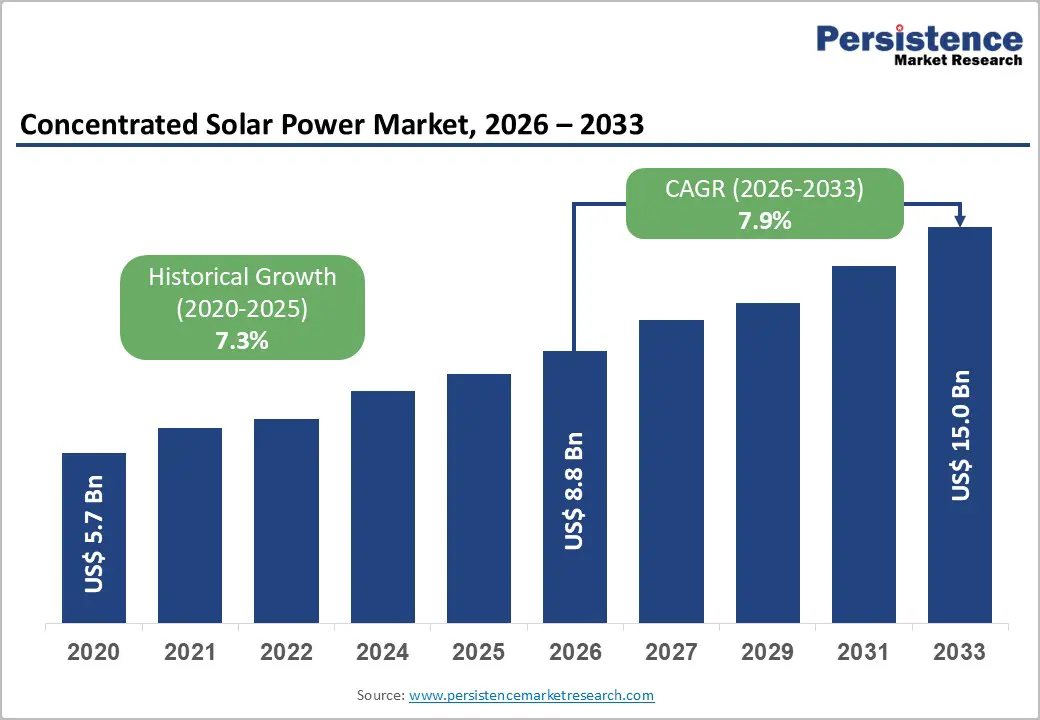

The global concentrated solar power market size is anticipated to reach US$ 8.8 billion in 2026 and US$ 15.0 billion by 2033, growing at a CAGR of 7.9% between 2026 and 2033.

Government-backed renewable energy targets, thermal energy storage integration, and expanding CSP deployment in solar-rich MENA, Asian, and North American markets are the primary growth catalysts. CSP's unique dispatchability advantage, enabled by molten salt thermal storage, differentiates it from photovoltaic systems in utility-scale baseload applications. Growing interest in CSP-powered desalination and industrial process heat further broadens the addressable application base through 2033.

Key Industry Highlights:

- Leading Technology: Parabolic Trough dominates with a 72.4% technology share; Power Tower/Central Receiver is the fastest-growing technology at a 13.5% CAGR, driven by supercritical CO2 cycles and TES advances.

- Leading Capacity: Above 150 MW capacity segment leads at 46.4% share and grows fast at 8.4% CAGR, anchored by MENA and Asian national utility-scale CSP procurement tenders.

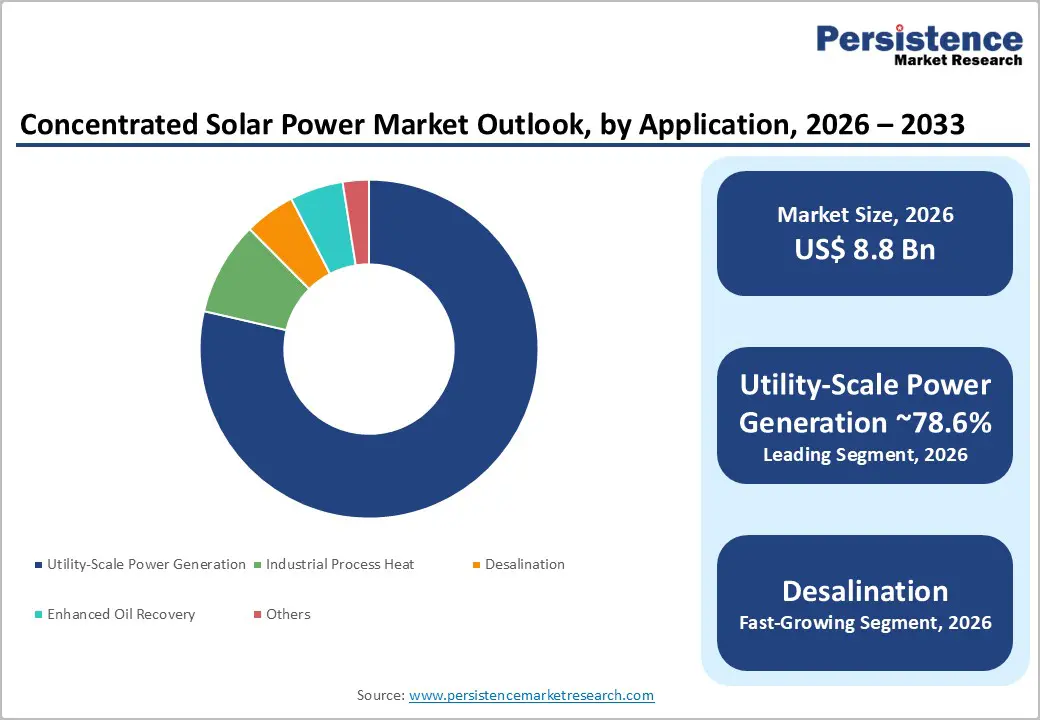

- Leading Application: Utility-Scale Power Generation leads application at 78.6% share; Desalination is projected a fast-growth at 12.7% CAGR, validated by EU-funded CSP-desalination demonstration projects in MENA.

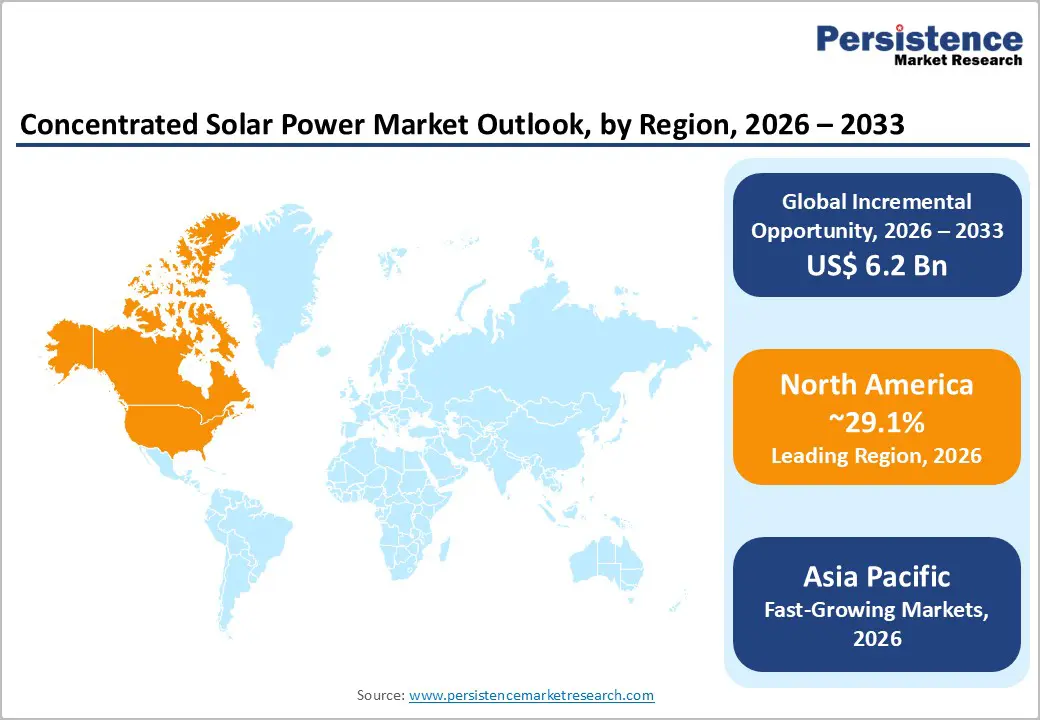

- Regional Leadership: North America leads with a 29.1% share (2025); Asia Pacific is the fastest-growing region at a 10.0% CAGR, driven by China's 5 GW CSP target and India's solar mission mandates.

- Opportunity: Key 2024 - 2025 strategic developments include ACWA Power's 300 MW Saudi CSP-storage project, Sener's supercritical CO2 partnership, and Vast Solar's modular Power Tower commercialization.

Market Dynamics Analysis

Drivers - National Renewable Energy Targets and Government Policy Incentives

Governments across solar-rich regions are embedding CSP into long-term clean energy strategies, creating policy-backed demand pipelines of multi-gigawatt scale. The International Energy Agency (IEA) projects that global installed CSP capacity must grow from 7.2 GW in 2023 to over 230 GW by 2050 to align with net-zero scenarios, implying an investment requirement exceeding US$ 300 Bn in the forecast period. Saudi Arabia's National Renewable Energy Program targets 2.7 GW of CSP capacity by 2030 under Vision 2030, while the UAE's 950 MW Mohammed bin Rashid Al Maktoum Solar Park Phase IV directly incorporates parabolic trough and central tower CSP systems.

In the United States, the Inflation Reduction Act (IRA) of 2022 extended Investment Tax Credits (ITCs) of up to 30% for qualifying solar thermal projects, thereby improving the financial viability of CSP projects. Morocco's 580 MW Noor Solar Complex and South Africa's Redstone and KaXu projects exemplify how sovereign energy policy drives utility-scale CSP commitments. These regulatory and financial frameworks are translating directly into confirmed capacity pipelines, providing CSP equipment and EPC contractors with multi-year revenue visibility essential for large capital deployment decisions.

Thermal Energy Storage Integration and Grid Dispatchability Advantage

CSP's ability to integrate molten salt thermal energy storage (TES) systems, enabling 8-16+ hours of dispatchable electricity generation independent of real-time solar irradiation, is its most strategically differentiated feature over variable renewable technologies, including solar PV and wind. As power grid operators globally confront the "duck curve" challenge of renewable over-generation during daylight hours and peak evening demand, dispatchable CSP with TES is attracting premium offtake pricing in power purchase agreements (PPAs).

The U.S. Department of Energy's SunShot Initiative targets CSP with storage costs at US$ 0.05/kWh by 2030, reinforcing technology investments in advanced molten-salt storage, supercritical CO2 cycles, and particle-based heat-transfer systems. Chile, Spain, and Israel have commissioned CSP-plus-storage plants exceeding 100 MW, demonstrating commercial-scale bankability. Grid operators in emerging markets with high solar DNI (Direct Normal Irradiance) resources, including India, Morocco, and Chile, are increasingly specifying CSP with TES in national tender frameworks, creating structured procurement pathways for integrated CSP-storage system providers.

Restraints - Land and Water Resource Intensity Creating Site Development Constraints

Large-scale CSP facilities require significant contiguous land areas, typically 4-8 km² per 100 MW installed, and significant water volumes for wet-cooling operations, creating site development constraints particularly in arid, high-DNI locations where land tenure, water rights, and environmental permitting are complex. Projects in MENA, India, and the American Southwest have encountered permitting delays extending 18-36 months, slowing the pace of capacity addition against contracted delivery timelines. Dry-cooling alternatives reduce water dependency but impose efficiency penalties of 3-10%, affecting project economics and competitive positioning relative to photovoltaic alternatives.

Competition from Rapidly Declining Utility-Scale Solar PV and Battery Storage

CSP faces structural competitive pressure from utility-scale solar PV, whose levelized cost of electricity (LCOE) has declined approximately 90% since 2010 (International Renewable Energy Agency, 2023), increasingly paired with lithium-ion battery storage. As battery storage costs fall below US$ 150/kWh at project scale, PV-plus-battery systems are encroaching on CSP's dispatchability advantage for sub-8-hour storage durations. This competitive dynamic is narrowing CSP's addressable market toward long-duration storage and high-temperature industrial heat applications, compressing the commercial pipeline for shorter-duration utility projects and demanding continuous cost reductions in CSP technology.

Opportunities - CSP-Powered Desalination for Water-Scarce Regions

Water scarcity and energy security frequently converge in the same high-DNI geographies, particularly across MENA, Sub-Saharan Africa, coastal India, and the American Southwest, creating a structurally compelling opportunity for integrated CSP-desalination systems. The DESOLINATION EU-funded project demonstrated a 200 kW CSP air Brayton cycle power tower successfully driving advanced desalination systems at King Saud University in 2024, validating the technology at demonstration scale.

The World Resources Institute identifies 17 nations as facing "extremely high" water stress, a majority of which possess the high solar irradiation levels necessary for CSP operation. With global desalination capacity needing to triple by 2050 (World Bank), CSP-desalination hybrid systems address both power and water supply simultaneously, a compelling value proposition for governments facing dual resource scarcity. The addressable market for CSP-powered desalination is estimated to reach US$ 1.5-2.0 Bn by 2030 across MENA and South Asian coastal deployment zones.

Industrial Process Heat and Enhanced Oil Recovery Applications

The industrial sector accounts for approximately one-third of global final energy consumption, with process heat requirements between 150°C and 400°C, a temperature range well within the operational capacity of parabolic trough and linear Fresnel CSP collectors. Industries including chemicals, food processing, textiles, and mining present significant addressable demand for solar thermal process heat, particularly as carbon-pricing mechanisms raise the cost of fossil-fuel-fired industrial heat in Europe and emerging markets.

The Enhanced Oil Recovery (EOR) application, where CSP-generated steam is injected into oil reservoirs to improve crude extraction efficiency, is gaining commercial traction in California, Oman, and Saudi Arabia. Chevron's Coalinga CSP-EOR project in California demonstrated 29 MW of solar-steam generation, and ADNOC has explored scalable CSP-EOR deployment within its oilfield operations. As carbon-emission regulations tighten on fossil fuel extraction, CSP-EOR offers operators a pathway to decarbonize steam production while maintaining extraction volumes, with an estimated US$ 400-600 Mn near-term addressable market.

Category-wise Analysis

Technology Insights

Parabolic trough systems lead the technology segment with a 72.4% share in 2026. Its leadership reflects decades of commercial deployment history, proven bankability in international PPA frameworks, and an established global supply chain for receivers, mirrors, and heat transfer fluids. The 580 MW Noor-I/II/III complex in Morocco, U.S. Mojave Solar Project, and multiple Indian CSP installations are all parabolic trough-based, demonstrating cross-regional OEM and EPC maturity.

While power tower systems are gaining share through higher operating temperatures and superior storage integration, Parabolic trough's entrenched OEM relationships and risk-adjusted bankability metrics ensure sustained leadership through the medium term.

Power tower / central receiver systems are the fastest-growing technology at a remarkable CAGR of 13.5% through 2033. Their superior solar-to-electric efficiency (up to 21.8% per independent studies), compatibility with supercritical CO2 cycles, and ability to reach temperatures exceeding 565°C for next-generation molten salt storage are driving accelerated OEM investment and project specification.

Capacity Insights

Plants with a capacity above 150 MW lead the segment with a 46.4% share in 2026. Utility-scale procurement frameworks across MENA, India, South Africa, and the U.S. favor large-scale CSP plants due to their superior economies of scale in land use, EPC costs, grid connection infrastructure, and TES system efficiency. Projects exceeding 150 MW, including Morocco's Noor III (150 MW), Dubai's MBR Phase IV (700 MW combined), and Chile's Cerro Dominador (110 MW), anchor the global installed base and confirmed pipeline.

The Below 50 MW segment addresses distributed industrial and desalination applications, while the 50-150 MW range serves smaller national program tenders. Above 150 MW dominance is expected to strengthen through 2033.

Above 150 MW is also the fastest-growing capacity segment at 8.4% CAGR through 2033. The scale of national renewable energy tenders, particularly in Saudi Arabia, India, and Australia, structurally favors gigawatt-scale CSP project pipelines, with individual plants consistently exceeding the 150 MW threshold.

Application Analysis

Utility-Scale Power Generation leads the application segment with a commanding 78.6% market share in 2026. CSP's primary value proposition as a dispatchable, large-scale renewable power generation technology fundamentally anchors it to utility procurement frameworks, sovereign energy targets, and long-term PPA structures. Its thermal storage capability enables evening and overnight power generation, critical for baseload grid stability that PV alone cannot deliver.

Industrial Process Heat and EOR serve important niche roles but remain constrained by site-specific requirements and limited OEM project pipelines relative to utility-scale. Utility generation dominance will persist through 2033, reinforced by MENA and South Asian sovereign energy commitments.

Desalination (Water Treatment) is the fastest-growing application at a CAGR of 12.7% through 2033. MENA region water scarcity urgency, CSP-desalination technology validation at King Saud University, and EU-funded demonstration projects are collectively driving interest in commercial-scale deployment for this high-potential niche application segment.

Regional Market Insights

North America Concentrated Solar Power Market Share

North America holds the leading regional position with 29.1% share of the global CSP Market in 2025, anchored by the United States' extensive installed CSP base, the world's largest, exceeding 1.7 GW, concentrated in California, Arizona, and Nevada with solar resources among the highest Direct Normal Irradiance (DNI) zones globally. The Inflation Reduction Act's 30% ITC for solar thermal projects, combined with the U.S. DOE's Concentrating Solar-Thermal Power initiative targeting US$ 0.05/kWh by 2030, sustains a strong technology investment and project development ecosystem.

Canada is exploring CSP-thermal hybrid applications in northern industrial zones. The U.S. hosts leading CSP technology innovators and EPC contractors, reinforcing North America's technology leadership position.

North America's growth is driven by grid integration of dispatchable renewables, IRA financial incentives, and growing CSP-EOR applications within California and Southwestern U.S. fossil fuel operations targeting emission reduction mandates.

Europe Concentrated Solar Power Market Insights

Europe holds a 23.9% share of the global CSP market in 2025 and is growing at a steady 6.1% CAGR through 2033, driven by Spain's position as the world's second-largest CSP market with over 2.3 GW installed, home to the Andasol and Gemasolar projects that pioneered commercial molten salt storage. Germany invests in CSP technology research and component manufacturing, while France and Spain drive deployment through EU renewable energy integration frameworks.

The EU's REPowerEU plan targets 600 GW of renewable capacity by 2030, with CSP qualifying for dispatch-priority classification under grid stability criteria. The DESOLINATION project partners, operating across multiple EU member states, exemplify Europe's R&D investment in CSP-desalination convergence.

The market growth scenario in Europe is characterized by Spain's CSP fleet expansion, EU carbon border adjustment mechanisms incentivizing dispatchable renewables, and growing cross-border CSP power import agreements with North African producers under Euro-Mediterranean energy partnerships.

Asia Pacific Concentrated Solar Power Market Insights

Asia Pacific is the fastest-growing CSP region at 10.0% CAGR through 2033, driven by China's ambitious CSP capacity targets, reaching 5 GW by 2030 under the National Energy Administration's solar thermal power development plan, and India's National Solar Mission targeting 10 GW of CSP capacity under thermal storage mandates. China commissioned the Qinghai Delingha 50 MW tower CSP project and multiple Gansu province parabolic trough plants, establishing the region's manufacturing and engineering competency.

Australia is developing the Aurora CSP project, and ASEAN markets, particularly Thailand and Vietnam, are formulating CSP feasibility frameworks. Rapid electricity demand growth, high solar DNI zones, and government industrial policy support define the investment thesis.

Asia Pacific's manufacturing scale advantages for mirrors, receivers, and steel structures, combined with government infrastructure financing programs targeting 2030 renewable energy commitments, make it the most strategically dynamic CSP growth market through 2033.

Competitive Landscape

The global CSP Market is moderately fragmented, with the five largest players, Abengoa Solar, BrightSource Energy, ACWA Power, SolarReserve (technology), and Sener Group, collectively accounting for approximately 42% of global installed project capacity in 2025. Regional EPC specialists and national energy companies hold the remaining share. Market leaders differentiate through proprietary thermal storage configurations, proven plant operational data, and established sovereign PPA track records that de-risk project financing for institutional lenders.

Technology differentiation in Power Tower and TES systems, geographic expansion into MENA and Asia Pacific markets, and strategic co-development of CSP-desalination and CSP-industrial heat projects define the dominant competitive themes. Players investing in supercritical CO2 cycle integration and AI-driven heliostat optimization are building next-generation cost competitiveness for post-2026 project pipelines.

Strategic Developments

- In October 2024, the DESOLINATION EU project partners conducted a formal site evaluation of the 200 kW CSP Power Tower at King Saud University, validating integrated solar-thermal desalination technology combining Brayton cycle power and advanced water treatment systems for MENA commercialization.

- In January 2025, ACWA Power reached financial close for a 300 MW solar project in Saudi Arabia under the PIF’s renewable energy program, supporting Vision 2030, with integrated storage capabilities aimed at enhancing grid stability and meeting rising industrial power demand.

- In March 2024, Sener Group and a Spanish utility co-announced a technical partnership targeting supercritical CO2 cycle integration with existing parabolic trough CSP plants in Spain, aiming to improve thermal-to-electric conversion efficiency by 8-12% versus conventional steam Rankine configurations.

Companies Covered in Concentrated Solar Power Market

- Abengoa Solar S.A.

- ACWA Power

- BrightSource Energy

- Sener Group

- SolarPACES/DLR

- Siemens Energy AG

- General Electric (GE Vernova)

- Enel Green Power

- TSK Group

- Aalborg CSP

- WorleyParsons (Worley)

- Cobra Group (ACS Group)

- SunCan (China Datang Corporation)

- Themax Limited, Vast Solar

Frequently Asked Questions

The concentrated solar power market is valued at US$ 8.8 Bn in 2026, projected to reach US$ 15.0 Bn by 2033.

Government renewable energy mandates, CSP's unique thermal storage dispatchability advantage, and expanding applications in desalination and industrial process heat are the primary growth drivers.

The market is projected to grow at a CAGR of 7.9% from 2026 to 2033.

CSP-desalination integration in water-scarce MENA and South Asian markets and industrial process heat decarbonization represent the most commercially actionable near-term growth opportunities.

Abengoa Solar, ACWA Power, BrightSource Energy, Sener Group, Siemens Energy, Enel Green Power, TSK Group, Aalborg CSP, and Vast Solar are the leading global market participants.