- Pharmaceuticals

- Sarcopenia Treatment Market

Sarcopenia Treatment Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Sarcopenia Treatment Market by Treatment (Protein Supplements, Vitamin B12 Supplements, Vitamin D & Calcium Supplements, Others), Route of Administration (Oral, Parenteral, Enteral), Distribution Channel (Hospital Pharmacies, Drug Stores & Retail Pharmacies, Online Pharmacies), and Regional Analysis from 2026 - 2033

Sarcopenia Treatment Market Share and Trends Analysis

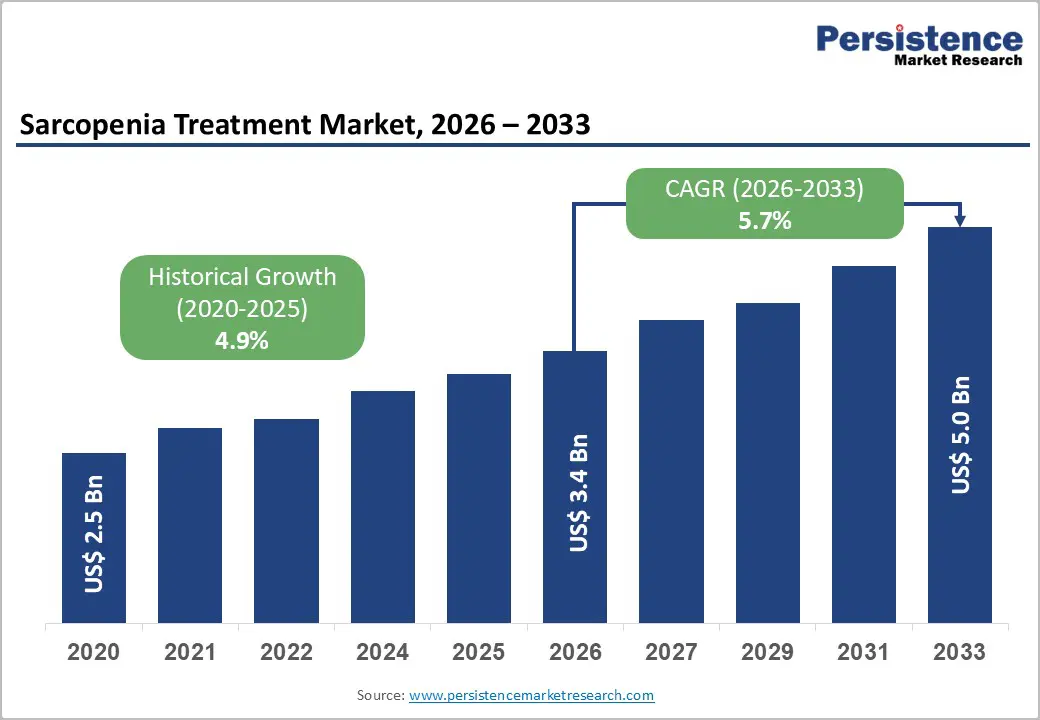

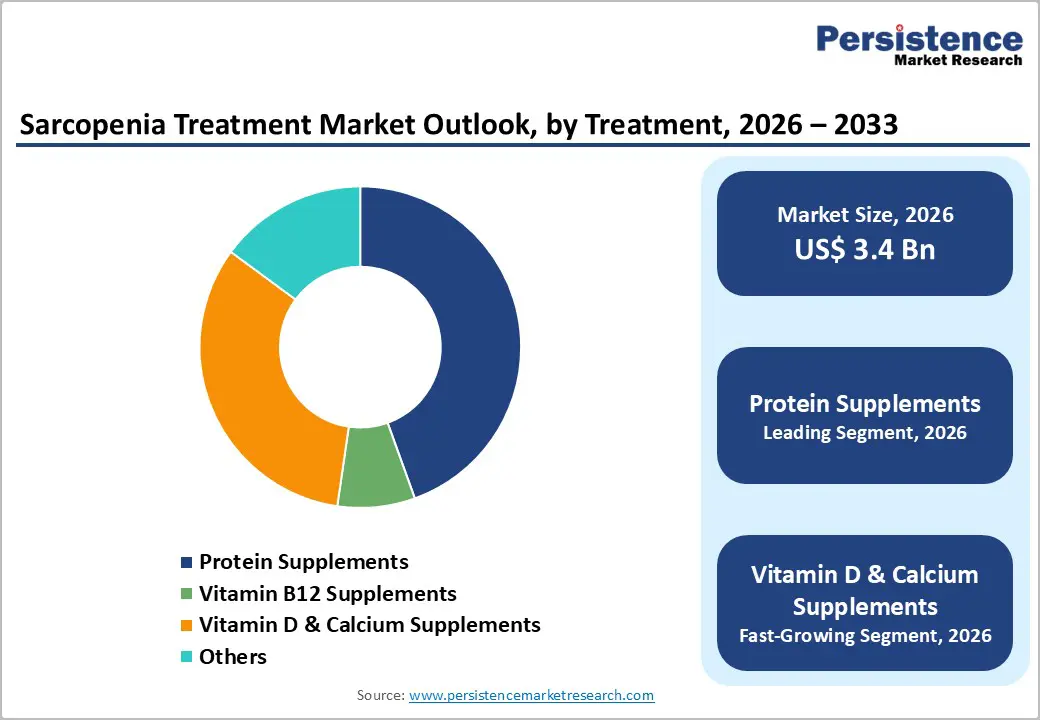

The global sarcopenia treatment market is estimated to grow from US$ 3.4 billion in 2026 to US$ 5.0 billion by 2033. The market is projected to grow at a CAGR of 5.7% from 2026 to 2033.

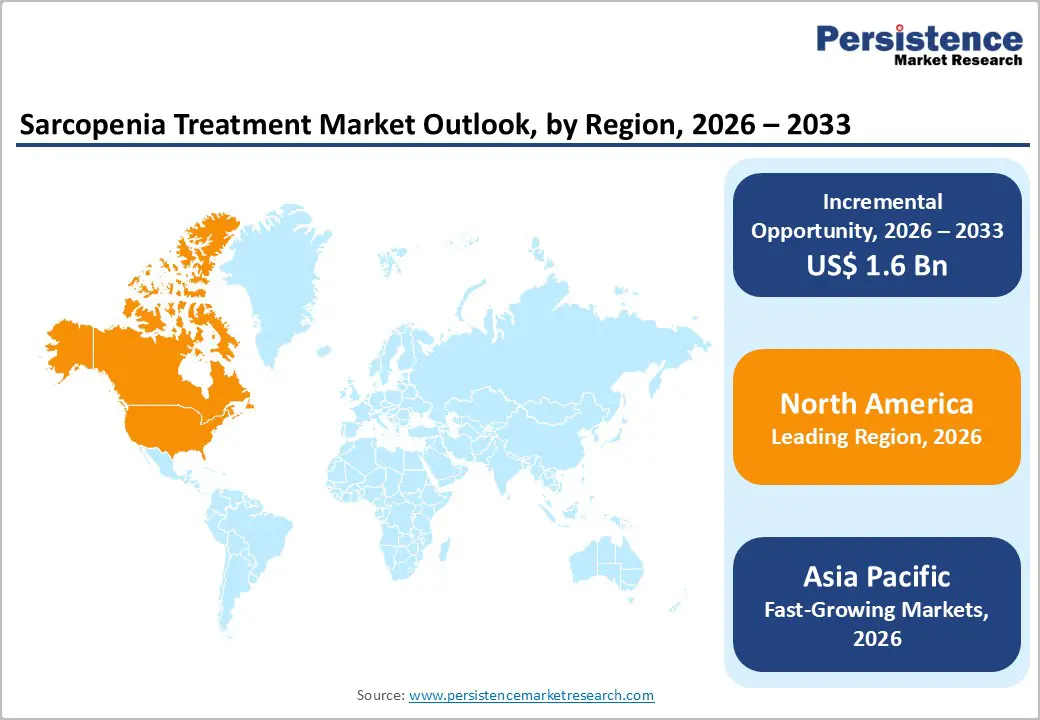

The sarcopenia treatment market is growing steadily, driven by population aging, rising prevalence of muscle loss disorders, and increasing awareness of preventive nutrition and therapies. North America leads due to strong clinical research, advanced healthcare infrastructure, and high supplement adoption. Asia-Pacific shows rapid growth, supported by expanding elderly populations, improving healthcare access, and growing nutrition awareness.

Key Industry Highlights:

- Dominant Segment: Nutritional supplements dominate the sarcopenia treatment market in 2025, led by protein supplements and vitamin D & calcium formulations, driven by their preventive role, ease of administration, and widespread use in elderly populations.

- Dominant Region: North America leads the market in 2025, supported by strong clinical awareness, high adoption of medical nutrition, and advanced geriatric care infrastructure. Asia-Pacific is the fastest-growing region due to rapid population aging, improving diagnosis, and rising affordability of supplements.

- Market Drivers: Growth is driven by global population aging, increasing prevalence of age-related muscle loss, higher awareness of sarcopenia as a clinical condition, emphasis on preventive healthcare, and integration of nutrition into elderly care protocols.

- Market Opportunity: Key opportunities include development of clinically validated muscle-targeted nutraceuticals, combination nutrition-therapy approaches, expansion of prescription-grade supplements, digital monitoring of muscle health, and growth in emerging markets with large aging populations.

| Key Insights | Details |

|---|---|

|

Global Sarcopenia Treatment Market Size (2026E) |

US$ 3.4 Bn |

|

Market Value Forecast (2033F) |

US$ 5.0 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.9% |

Market Dynamics

Driver - Rising clinical awareness and recognition of sarcopenia as a diagnosable condition

Rising clinical awareness and recognition of sarcopenia as a diagnosable condition significantly drive the sarcopenia treatment market. Sarcopenia, defined as age-related loss of skeletal muscle mass and strength, now affects an estimated 10% of adults over age 60 worldwide, with prevalence increasing to 11–50% among those aged 80 and older. This broader epidemiological understanding has been shaped by the adoption of standardized diagnostic criteria such as those from the European and Asian Working Groups, enabling clinicians to identify the condition more reliably and consistently in clinical practice.

Improved recognition of sarcopenia’s impact on health outcomes has further heightened clinical interest and market growth. Research shows sarcopenia’s prevalence varies by setting, with up to 51% of older adults in nursing homes affected and 23–24% in hospitalized elderly, underscoring its clinical burden. As healthcare systems prioritize aging-related conditions, clinicians increasingly screen for muscle mass, strength, and performance, translating into greater demand for interventions and supportive therapies. Government and academic emphasis on preventive approaches reinforces this trend, expanding diagnostic utilization and integrating sarcopenia into standard geriatric assessment protocols.

Restraints - Limited availability of approved pharmacological therapies specifically for sarcopenia

A major restraint in the sarcopenia treatment market is the limited availability of approved pharmacological therapies specifically for sarcopenia. According to clinical literature and regulatory data, there are currently no medications approved by the United States Food and Drug Administration (FDA) or European Medicines Agency (EMA) for the treatment of sarcopenia, despite its recognition as a disease with an ICD-10 code (M62.84) since 2016. This means that drug development has not yet yielded a therapy formally indicated for sarcopenia, and clinical practice relies heavily on non-drug interventions such as resistance exercise and nutritional support.

The absence of approved drugs directly targeting sarcopenia constrains market expansion and therapeutic innovation. While researchers have investigated various candidate agents-such as anabolic hormones, selective androgen receptor modulators (SARMs), and growth factors—none have received regulatory approval due to inconsistent efficacy and safety concerns in clinical trials. For example, selective androgen receptor modulators have shown limited success in improving muscle mass without clear functional benefits, and development efforts have been discontinued or remain in early stages. This regulatory gap restricts pharmaceutical investment, limits standardized treatment protocols, and sustains reliance on exercise and nutrition rather than pharmacotherapy for sarcopenia management.

Opportunity - Development of targeted, prescription-grade nutraceuticals for muscle health

The development of targeted, prescription-grade nutraceuticals for muscle health represents a significant opportunity in the sarcopenia treatment market. Evidence indicates that tailored nutritional interventions, especially protein-based multinutrient therapies, can improve muscle strength and function in older adults with sarcopenia. A recent systematic review of randomized trials showed that protein-based nutritional supplementation significantly improved handgrip strength and gait speed in older adults with sarcopenia compared with control groups. These results support the role of scientifically formulated nutraceuticals as adjuncts to exercise and clinical care for sarcopenia management, validating investment in targeted, clinically tested products.

Clinical and epidemiological data further justify this opportunity: comprehensive meta-analyses involving thousands of elderly participants demonstrate that nutritional supplementation, particularly with high-quality protein sources and multinutrient compositions, yields measurable benefits in muscle mass, muscle strength, and physical performance. For example, protein supplementation was associated with significant improvements in skeletal muscle mass index and handgrip strength among elderly adults, and higher dietary protein intake correlates with reduced sarcopenia risk in large population studies. These findings, grounded in clinical research and public health observations, create a strong foundation for prescription-grade nutraceutical development targeted at sarcopenia.

Category-wise Analysis

By Treatment Insights

Protein supplements dominate with 44.5% share of the global market in 2025, because adequate protein intake is essential for maintaining muscle mass and strength, particularly in older adults. Aging leads to reduced muscle protein synthesis, contributing to sarcopenia, which affects up to 50% of adults over 80 and increases frailty, fall risk, and hospitalization. Studies indicate that older adults require higher protein intake (1.0–1.2 g/kg/day or more) than standard recommendations to preserve muscle health. Protein supplements-such as whey, milk, and amino-acid enriched products-provide a convenient, concentrated source of essential amino acids, supporting muscle protein synthesis. Their effectiveness in improving muscle mass, strength, and functional performance explains their dominant share in the sarcopenia treatment market.

By Route of Administration Insights

Oral administration dominates the sarcopenia treatment market because it aligns with the primary modalities used to address muscle loss-nutritional supplements and dietary protein-which are most effectively delivered through the oral route. Older adults often receive protein, vitamin D, calcium, and multinutrient supplements orally, enabling direct absorption of nutrients essential for maintaining muscle mass and function. Research shows that oral protein supplementation significantly improves muscle strength and physical performance in sarcopenic individuals, with studies linking higher dietary protein intake to better preservation of muscle mass in aging populations. Oral delivery also offers convenience, high patient compliance, and cost-effectiveness compared with invasive alternatives. These practical and clinical advantages explain the oral route’s dominant share in sarcopenia treatment.

Regional Insights

North America Sarcopenia Treatment Market Trends

North America dominates the sarcopenia treatment market with 38.1% share in 2025, because of its large aging population and advanced healthcare infrastructure, which together support early diagnosis and intervention. In 2024, the region accounted for around 39–43% of the global market share, with the United States representing the majority of that share due to established clinical practices and strong adoption of nutritional and therapeutic strategies for muscle health.

Additionally, sarcopenia prevalence and awareness among healthcare professionals in North America drive treatment uptake. Studies show a notable prevalence of reduced muscle strength among older U.S. adults aged 60 and over, contributing to clinical focus on muscle loss management, which increases demand for supplements and therapeutic options.

Europe Sarcopenia Treatment Market Trends

Europe is a key region in the sarcopenia treatment market due to its rapidly aging population and strong healthcare infrastructure. The current prevalence of sarcopenia in older adults ranges from 11–20%, and this number is projected to rise by over 60% by 2045, increasing demand for interventions to maintain muscle mass and function. Countries such as Germany, France, and the United Kingdom integrate geriatric care and preventive assessments into primary healthcare, supporting early diagnosis and treatment uptake. This combination of demographic pressure and well-established healthcare systems makes Europe a significant market for nutritional supplements and therapeutic solutions targeting sarcopenia.

Asia-Pacific Sarcopenia Treatment Market Trends

Asia Pacific is the fastest-growing region in the sarcopenia treatment market due to its rapidly aging population and increasing awareness of age-related muscle loss. The number of people aged over 60 in the region is projected to nearly triple to 1.3 billion by 2050, with China alone having over 200 million adults aged 65 and older, driving demand for nutritional and therapeutic interventions. Governments are expanding geriatric healthcare programs, early diagnosis initiatives, and preventive strategies, while sarcopenia prevalence in older adults is around 16.5%, highlighting the clinical burden. These demographic and healthcare factors collectively accelerate treatment adoption, making the Asia Pacific a high-growth market.

Competitive Landscape

Leading sarcopenia treatment providers focus on protein-based supplements, vitamin D formulations, and prescription-grade nutraceuticals. By improving muscle mass, strength, and functional performance, enhancing treatment adherence, and integrating preventive care with healthcare systems, they support early intervention, promote healthy aging, and drive adoption, fueling growth in the global sarcopenia treatment market.

Key Industry Developments:

- In January 2025, A novel androgen receptor agonist was granted fast-track designation for the treatment of sarcopenia in patients with cirrhosis. The designation, provided by regulatory authorities, aimed to expedite the development and review of the therapy due to its potential to address the significant unmet medical need of muscle wasting in liver disease.

Companies Covered in Sarcopenia Treatment Market

- Nestlé Health Science

- Abbott Laboratories

- Sanofi S.A.

- Novartis AG

- Eli Lilly and Company

- Amgen Inc.

- Pfizer Inc.

- Regeneron Pharmaceuticals, Inc.

- MyoPax GmbH

- Biophytis

- Epirium Bio

- BPGbio, Inc.

- Lipocine

- Others

Frequently Asked Questions

The global sarcopenia treatment market is projected to be valued at US$ 3.4 Bn in 2026.

Aging population, rising sarcopenia prevalence, protein supplements, vitamin D, clinical awareness, preventive care, exercise, nutrition, healthcare access.

The global sarcopenia treatment market is poised to witness a CAGR of 5.7% between 2026 and 2033.

Targeted nutraceuticals, combination therapies, digital muscle monitoring, emerging markets, prescription-grade supplements, preventive healthcare, and geriatric care expansion.

Nestlé Health Science, Abbott Laboratories, Sanofi S.A., Novartis AG, Eli Lilly and Company, Amgen Inc.