- Specialty & Fine Chemicals

- Phase-transfer Catalyst Market

Phase-transfer Catalyst Market Size, Share, and Growth Forecast, 2026 - 2033

Phase-transfer Catalyst Market by Product Type (Quaternary Ammonium Salts, Ammonium Salts, Others), End-use Industry (Pharmaceuticals, Agrochemicals, Others), Application, and Regional Analysis for 2026 - 2033

Phase-Transfer Catalyst Market Size and Trends Analysis

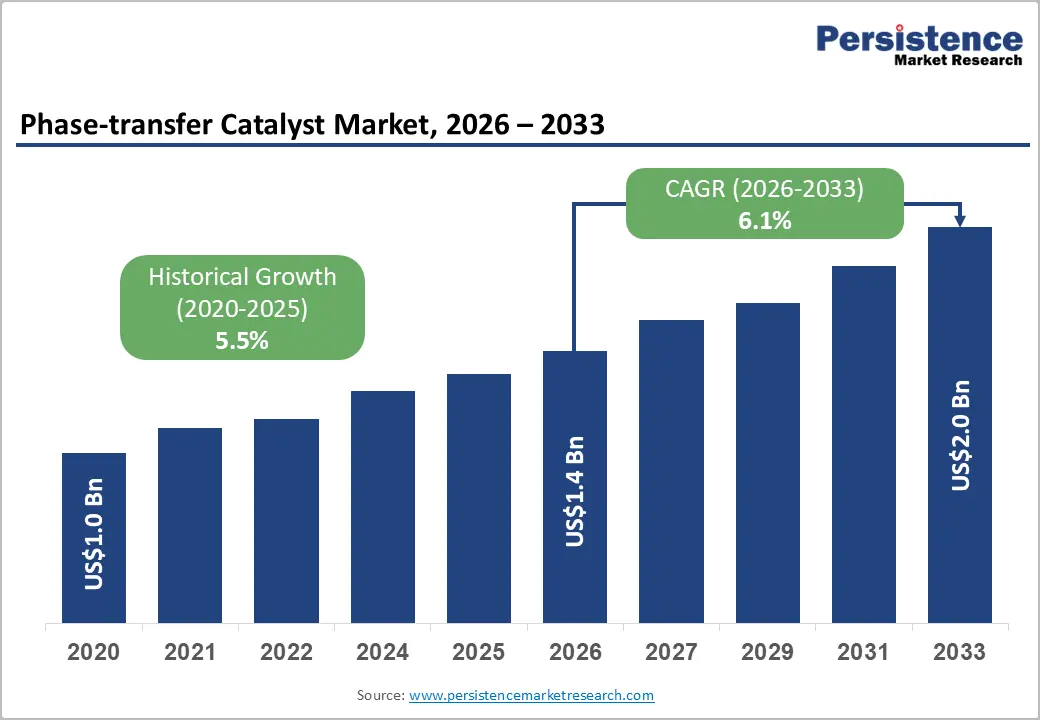

The global phase-transfer catalyst market size is likely to be valued at US$1.4 billion in 2026 and is expected to reach US$2.0 billion by 2033, growing at a CAGR of 6.1% during the forecast period from 2026 to 2033, driven by increasing demand for efficient reaction processes, rising emphasis on sustainable chemical manufacturing, and expanding use of catalysts that improve reaction selectivity while reducing operational complexity.

As manufacturers pursue higher yields, lower waste generation, and improved process economics, phase-transfer catalysts continue to gain strategic importance across industrial chemical value chains.

Key Industry Highlights:

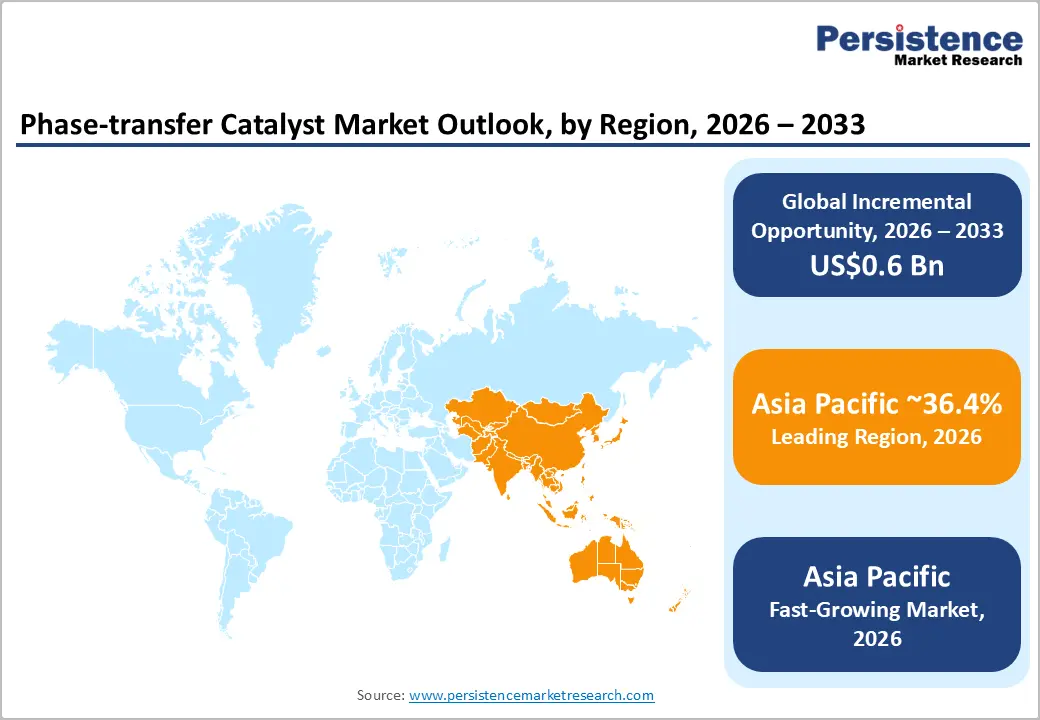

- Leading Region: Asia Pacific is anticipated to account for 36.4% of market share in 2026, driven by strong pharmaceutical manufacturing, expanding agrochemical production, and cost-competitive chemical processing industries.

- Fastest-growing Region: Asia Pacific is projected to register the highest growth rate through 2033, supported by increasing investments in China, India, and ASEAN countries, along with expanding specialty chemical and pharmaceutical production capacities.

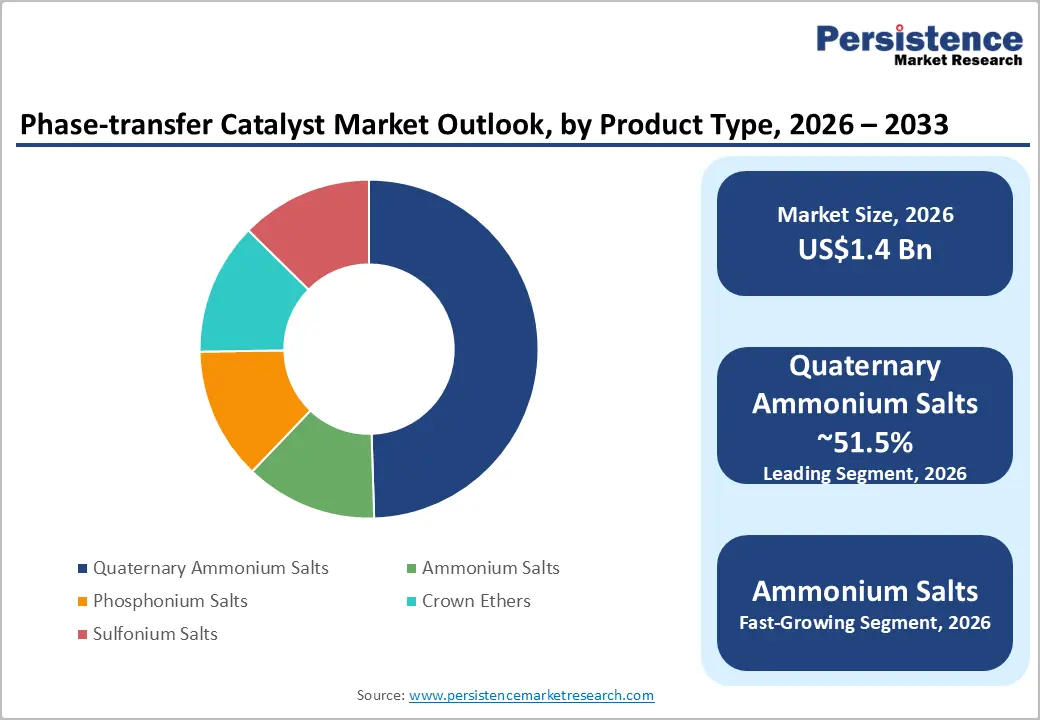

- Dominant Product Type: Quaternary ammonium salts are anticipated to hold 51.5% of market revenue in 2026, owing to their extensive use in pharmaceutical synthesis, agrochemical manufacturing, and specialty chemical applications.

- Leading End-use Industry: Pharmaceuticals are anticipated to account for 33.2% of market revenue in 2026, supported by growing API production, increasing drug development activities, and the rising adoption of advanced manufacturing technologies.

DRO Analysis

Driver - Expanding Pharmaceutical Manufacturing and API Production

The pharmaceutical industry remains the most significant demand generator for phase-transfer catalysts. These catalysts play a critical role in active pharmaceutical ingredient (API) synthesis by facilitating reactions between immiscible phases, improving reaction efficiency, enhancing selectivity, and reducing processing costs. Growing investments in pharmaceutical innovation, increasing generic drug production, and expanding contract development and manufacturing activities continue to strengthen the catalyst demand.

Modern pharmaceutical manufacturers are increasingly focused on process intensification strategies that improve production yields while reducing solvent consumption and waste generation. Phase-transfer catalysts support these objectives by enabling milder reaction conditions and shortening reaction cycles. The continued expansion of global pharmaceutical production, particularly in North America, Europe, India, and China, is expected to sustain long-term demand for high-purity quaternary ammonium and phosphonium catalysts. As regulatory agencies encourage advanced manufacturing technologies, catalyst adoption is expected to increase throughout pharmaceutical supply chains.

Rising Agrochemical Production and Crop Protection Requirements

Growing global food demand and increasing pressure to improve agricultural productivity are driving expansion within the agrochemical industry. Crop losses caused by insects, weeds, and plant diseases continue to create demand for effective crop protection products, resulting in increased production of herbicides, fungicides, and insecticides. Phase-transfer catalysts are widely utilized during the synthesis of agrochemical active ingredients and intermediates because they improve reaction efficiency and reduce processing complexity.

Manufacturers are also seeking cleaner and more sustainable production methods to comply with environmental regulations while maintaining profitability. Phase-transfer catalysts help achieve these objectives by enabling higher conversion rates and minimizing by-product formation. Rapid growth in agricultural production across Asia-Pacific, Latin America, and parts of Africa is generating new opportunities for agrochemical manufacturers, which in turn supports increasing consumption of catalyst technologies. The segment remains one of the strongest growth contributors to overall market expansion.

Restraint - Regulatory Compliance and Product Qualification Challenges

Despite favorable demand fundamentals, the market faces challenges associated with stringent regulatory requirements and extensive product qualification procedures. Pharmaceutical and agrochemical manufacturers require comprehensive documentation regarding catalyst purity, impurity profiles, environmental impact, and production consistency. Meeting these requirements increases development costs and extends commercialization timelines for catalyst suppliers.

Environmental regulations governing chemical manufacturing are becoming increasingly stringent, particularly in developed economies. Compliance with evolving safety standards, waste management requirements, and sustainability initiatives requires substantial investment in quality systems and process controls. Smaller manufacturers often face difficulties competing with established suppliers that possess extensive regulatory expertise and validated manufacturing infrastructure. Consequently, market entry barriers remain relatively high, limiting the pace of new supplier participation and increasing operational complexity across the value chain.

Opportunity - Manufacturing Expansion across Asia Pacific

Asia Pacific represents the most attractive growth opportunity for phase-transfer catalyst manufacturers. The region accounts for approximately 36.4% of market revenue and continues to benefit from large-scale investments in pharmaceutical production, agrochemical manufacturing, and specialty chemical processing. Countries such as China and India have emerged as major global production hubs due to favorable manufacturing economics, skilled labor availability, and expanding domestic demand.

Growing localization strategies among chemical producers are creating opportunities for catalyst suppliers to establish regional production facilities and strengthen supply chain resilience. Reduced logistics costs, shorter delivery times, and improved customer responsiveness are encouraging further investment in regional manufacturing capabilities. As pharmaceutical and chemical production capacities continue expanding throughout Asia Pacific, catalyst demand is expected to grow at a faster pace than in mature markets.

Development of Sustainable and High-Performance Catalyst Technologies

Sustainability has become a key purchasing criterion for chemical manufacturers worldwide. As companies pursue lower environmental footprints and improved process efficiencies, demand is increasing for advanced catalyst systems that support greener manufacturing practices. Recyclable catalysts, immobilized catalyst technologies, and high-selectivity formulations are gaining attention because they reduce waste generation and simplify downstream purification processes.

Innovation in catalyst design is creating opportunities for suppliers to differentiate through performance improvements rather than price competition. Customers increasingly seek solutions that lower energy consumption, improve reaction yields, and support regulatory compliance objectives. Manufacturers capable of developing environmentally responsible catalyst technologies are expected to benefit from stronger customer relationships, higher margins, and expanding opportunities within regulated end-use industries.

Category-wise Analysis

Product Type Insights

Quaternary ammonium salts are anticipated to account for 51.5% of the market share in 2026. Their dominance is driven by broad applicability in pharmaceutical synthesis, agrochemical production, and specialty chemical manufacturing. Widely used catalysts such as tetrabutylammonium bromide (TBAB) and benzyltriethylammonium chloride (BTEAC) facilitate alkylation, nucleophilic substitution, and oxidation reactions by efficiently transferring reactive species between aqueous and organic phases. Their established commercial availability, cost-effectiveness, and reliable performance continue to support widespread adoption across industrial processes.

Ammonium salts are projected to be the fastest-growing product type, supported by rising demand for efficient reaction systems in pharmaceutical intermediates, crop-protection chemicals, and specialty chemicals. For example, ammonium-based catalysts are increasingly utilized in the synthesis of herbicides and active pharmaceutical ingredients where improved yields and lower waste generation are priorities. Phosphonium salts remain important in high-temperature reactions requiring superior thermal stability, while crown ethers and sulfonium salts serve specialized applications in fine chemicals and advanced organic synthesis.

End-Use Industry Insights

Pharmaceuticals are anticipated to account for 33.2% of market revenue in 2026. The segment's dominance stems from the extensive use of phase-transfer catalysts in API synthesis, drug intermediates, and complex organic reactions. Catalysts such as TBAB are commonly employed in the production of cardiovascular, anti-infective, and specialty therapeutic compounds. Rising healthcare expenditure, expanding generic drug manufacturing, and increasing adoption of advanced pharmaceutical production technologies continue to strengthen demand for high-purity catalyst systems.

Agrochemicals are expected to be the fastest-growing end-use industry throughout the forecast period. Growing demand for herbicides, fungicides, and insecticides is driving catalyst consumption in crop-protection chemical synthesis. For example, phase-transfer catalysts are widely used in the production of glyphosate intermediates and various pyrethroid-based insecticides, helping improve reaction efficiency and product yields. Strong agricultural output growth across China, India, Brazil, and Southeast Asia is expected to support sustained expansion. Specialty chemicals remain a significant secondary market, while petrochemicals, food and beverage processing, and cosmetics provide additional growth opportunities.

Regional Insights

North America Phase-transfer Catalyst Market Trends

North America remains one of the most technologically advanced markets for phase-transfer catalysts, supported by a strong pharmaceutical ecosystem, sophisticated specialty chemical manufacturing, and continuous investment in process innovation. The region benefits from stringent quality standards and regulatory oversight, encouraging the adoption of high-performance catalyst systems that improve reaction efficiency, product consistency, and sustainability. Demand is primarily concentrated in pharmaceutical production, biotechnology applications, and specialty chemical synthesis, where manufacturers prioritize process optimization and regulatory compliance.

U.S. Phase-transfer Catalyst Market Trends

The U.S. is the dominant market within North America, accounting for the majority of regional demand. Its leadership is supported by a large pharmaceutical industry, advanced contract manufacturing sector, and extensive R&D infrastructure. Phase-transfer catalysts are widely utilized in API synthesis, drug intermediates, and specialty chemical production, where high-purity catalysts are required to meet strict quality standards. Growing investments in continuous manufacturing technologies, biotechnology development, and sustainable chemical processes continue to drive catalyst adoption across the country.

Canada Phase-transfer Catalyst Market Trends

Canada represents a smaller but steadily growing market, supported by investments in pharmaceutical manufacturing, life sciences research, and specialty chemicals. Government initiatives aimed at strengthening domestic pharmaceutical production and improving healthcare supply-chain resilience are creating opportunities for catalyst suppliers. Demand is primarily concentrated in pharmaceutical synthesis and research-driven specialty chemical applications.

North America remains one of the most profitable regional markets, characterized by strong innovation capabilities, premium product demand, and increasing adoption of advanced catalyst technologies.

Europe Phase-transfer Catalyst Market Trends

Europe is a mature yet highly attractive market for phase-transfer catalysts, supported by advanced chemical manufacturing capabilities, a strong pharmaceutical sector, and stringent environmental regulations. Sustainability initiatives across the region are encouraging manufacturers to adopt catalyst technologies that improve reaction efficiency, reduce waste generation, and lower environmental impact. Demand remains concentrated in high-value pharmaceutical and specialty chemical applications where product quality and regulatory compliance are critical.

Germany Phase-transfer Catalyst Market Trends

Germany is the largest market in Europe, benefiting from one of the world's most advanced chemical and pharmaceutical industries. The country's strong industrial base, extensive R&D activities, and leadership in specialty chemicals support significant demand for phase-transfer catalysts. German manufacturers increasingly focus on sustainable production technologies and process efficiency improvements, driving adoption of advanced catalyst systems.

U.K. Phase-transfer Catalyst Market Trends

The U.K. remains an important market due to its strong pharmaceutical research ecosystem and expanding biotechnology sector. Demand is driven by drug development activities, contract manufacturing services, and investments in innovative chemical synthesis technologies. Pharmaceutical companies continue to seek catalyst solutions that enhance process performance while maintaining regulatory compliance.

France Phase-transfer Catalyst Market Trends

France contributes significantly to regional demand through its pharmaceutical manufacturing and specialty chemical industries. Increasing emphasis on green chemistry and sustainable industrial production is encouraging broader adoption of efficient catalyst technologies. Investments in life sciences and advanced materials further support market growth.

Spain Phase-transfer Catalyst Market Trends

Spain is emerging as a growing market within Southern Europe, supported by expanding pharmaceutical production and specialty chemical manufacturing activities. The country is increasingly attracting industrial investment aimed at improving production capabilities and export competitiveness, creating additional opportunities for catalyst suppliers.

Europe's focus on sustainability, innovation, and regulatory excellence ensures continued demand for premium phase-transfer catalyst products despite moderate overall growth rates.

Asia Pacific Phase-transfer Catalyst Market Trends

Asia Pacific is anticipated to account for 36.4% of the market share in 2026, making it both the largest and fastest-growing regional market. The region's leadership is supported by extensive pharmaceutical manufacturing, rapidly expanding agrochemical production, competitive manufacturing costs, and growing specialty chemical industries. Increasing industrialization, favorable government policies, and expanding export activities continue to strengthen market growth across key economies.

China Phase-transfer Catalyst Market Trends

China is the largest market in Asia Pacific and a major global producer of pharmaceutical intermediates, active ingredients, agrochemicals, and specialty chemicals. The country's vast manufacturing infrastructure, integrated supply chains, and large domestic market create significant demand for phase-transfer catalysts. Investments in higher-value specialty chemicals and sustainable manufacturing technologies are further supporting market expansion.

India Phase-transfer Catalyst Market Trends

India has emerged as one of the fastest-growing markets due to its strong position in generic pharmaceuticals, contract manufacturing, and specialty chemical production. The country's expanding pharmaceutical exports, growing agrochemical sector, and increasing investment in chemical manufacturing capacity continue to drive catalyst consumption. Rising emphasis on process efficiency and global quality standards is accelerating adoption of advanced catalyst technologies.

Japan Phase-transfer Catalyst Market Trends

Japan remains an important high-value market characterized by advanced chemical manufacturing and innovation-driven applications. Demand is concentrated in pharmaceutical synthesis, electronics chemicals, and high-performance specialty materials. Japanese manufacturers prioritize precision, product quality, and technological innovation, creating opportunities for premium catalyst solutions.

Competitive Landscape

The global phase-transfer catalyst market is fragmented to moderately fragmented, with a combination of multinational chemical companies and regional specialty manufacturers competing across different application segments. Market competition is primarily based on product quality, catalyst performance, regulatory compliance, technical expertise, and supply reliability. Established suppliers benefit from extensive customer relationships and validated manufacturing capabilities, while smaller participants focus on niche applications and customized solutions. The competitive environment encourages continuous innovation and process improvement, particularly within pharmaceutical and specialty chemical applications.

Leading market participants are focusing on product innovation, sustainable catalyst development, regional manufacturing expansion, and customer-specific technical support. Companies increasingly emphasize high-performance formulations, operational efficiency improvements, and localized supply networks. Strategic investments in research and development remain critical for maintaining competitive differentiation and addressing evolving customer requirements across regulated industries.

Key Industry Developments:

- In August 2025, Evonik Industries AG inaugurated a world-scale alkoxides production facility on Jurong Island, Singapore, with an annual capacity of 100,000 metric tons, aiming to strengthen its catalyst supply network across Asia and enhance responsiveness to growing demand from pharmaceutical, biodiesel, and specialty chemical industries.

Companies Covered in Phase-transfer Catalyst Market

- Merck KGaA

- Solvay SA

- Evonik Industries AG

- BASF SE

- Clariant AG

- SACHEM Inc.

- Tatva Chintan Pharma Chem Ltd.

- Dishman Carbogen Amcis Ltd.

- Nippon Chemical Industrial Co., Ltd.

- Cayman Chemical Company

- Kente Catalysts Inc.

- Central Drug House (CDH)

- Pacific Organics Pvt. Ltd.

- PAT Impex India

- Otto Chemie Pvt. Ltd.

- Tokyo Chemical Industry Co., Ltd. (TCI)

Frequently Asked Questions

The global phase-transfer catalyst market is anticipated to be valued at US$1.4 billion in 2026.

The global phase-transfer catalyst market is expected to reach US$2.0 billion by 2033.

Key market trends include increasing adoption of green chemistry practices, rising pharmaceutical and agrochemical production, growing demand for high-selectivity catalysts, expansion of chemical manufacturing in Asia Pacific, and the development of recyclable and sustainable catalyst technologies.

Quaternary ammonium salts are the leading product type segment, accounting for approximately 51.5% of market revenue due to their broad applicability in pharmaceutical, agrochemical, and specialty chemical synthesis.

The market is projected to expand at a CAGR of 6.1% between 2026 and 2033.

Major companies include Merck KGaA, Solvay SA, Evonik Industries AG, BASF SE, and Clariant AG.