- Agrochemicals

- Fungicides Market

Fungicides Market Size, Share, and Growth Forecast 2026 - 2033

Fungicides Market by Product Type (Benzimidazoles, Triazoles, Strobilurins, Chloronitriles, Dithiocarbamates, Phenylamides, Bio-fungicides, Others), by Source (Synthetic Fungicides, Bio-based Fungicides), by Application Method (Foliar Spray, Soil Treatment, Seed Treatment, Drip Application, Post-Harvest Application), by End-Use, by Regional Analysis, 2026 - 2033

Fungicides Market Size and Trend Analysis

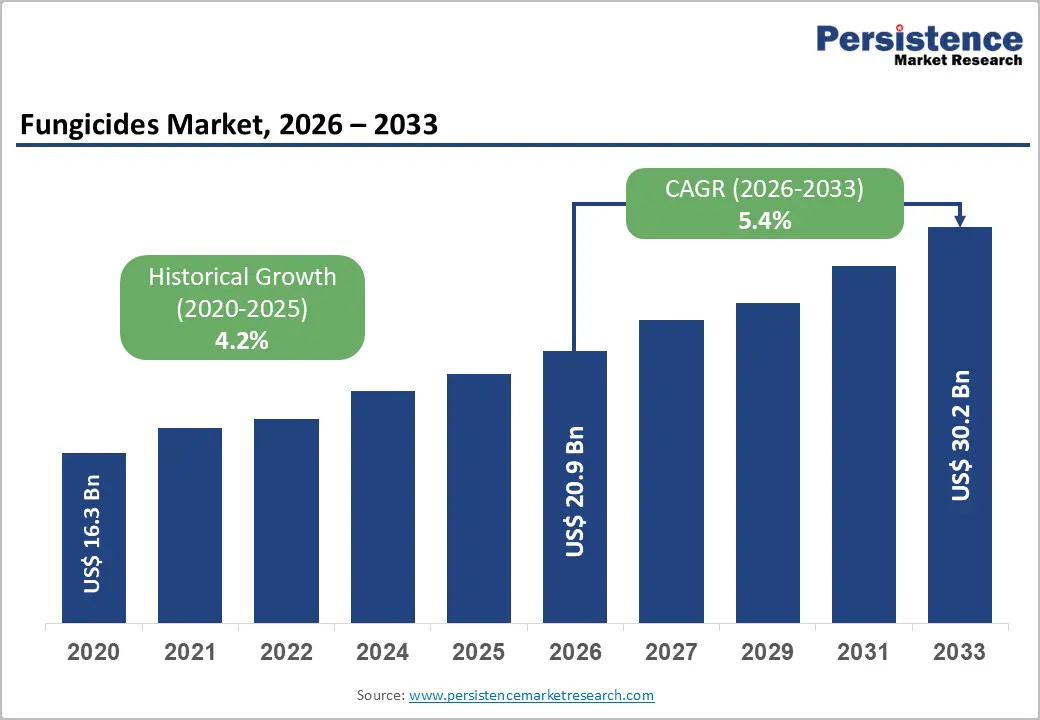

The global fungicides market size is likely to be valued at US$ 20.9 billion in 2026 and is projected to reach US$ 30.2 billion by 2033, growing at a CAGR of 5.4% between 2026 and 2033.

The impact of fungal diseases on global crop production, and innovations in fungicide formulations, such as novel modes of action from manufacturers addresses resistance issues and promote sustainable farming, further bolstering market expansion.

Key Industry Highlights:

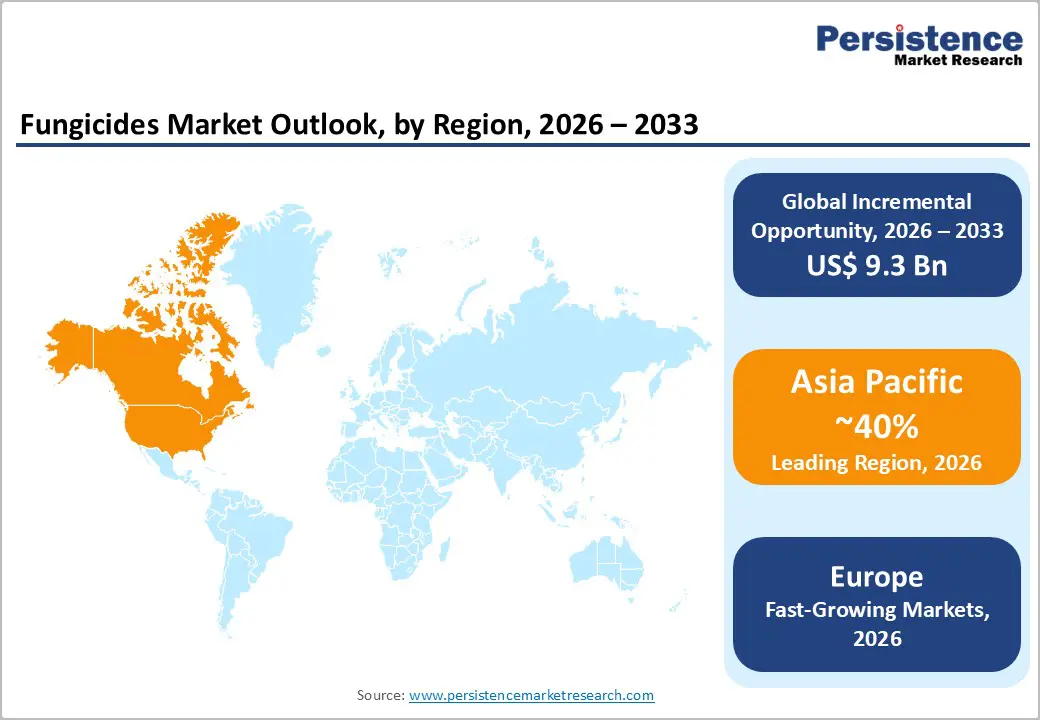

- Leading Region: Asia-Pacific is the dominant region in the global fungicides market, with a 40% share, driven by extensive agricultural land in China and India, where fungal diseases threaten yields of staple crops essential for feeding billions.

- Fastest-Growing Region: Europe is the fastest-growing region in the fungicides market, projected to grow at a CAGR of 5.9% over the forecast period, driven by stringent regulations, sustainability policies, and advanced farming practices in key countries such as Germany, France, the U.K., and Spain.

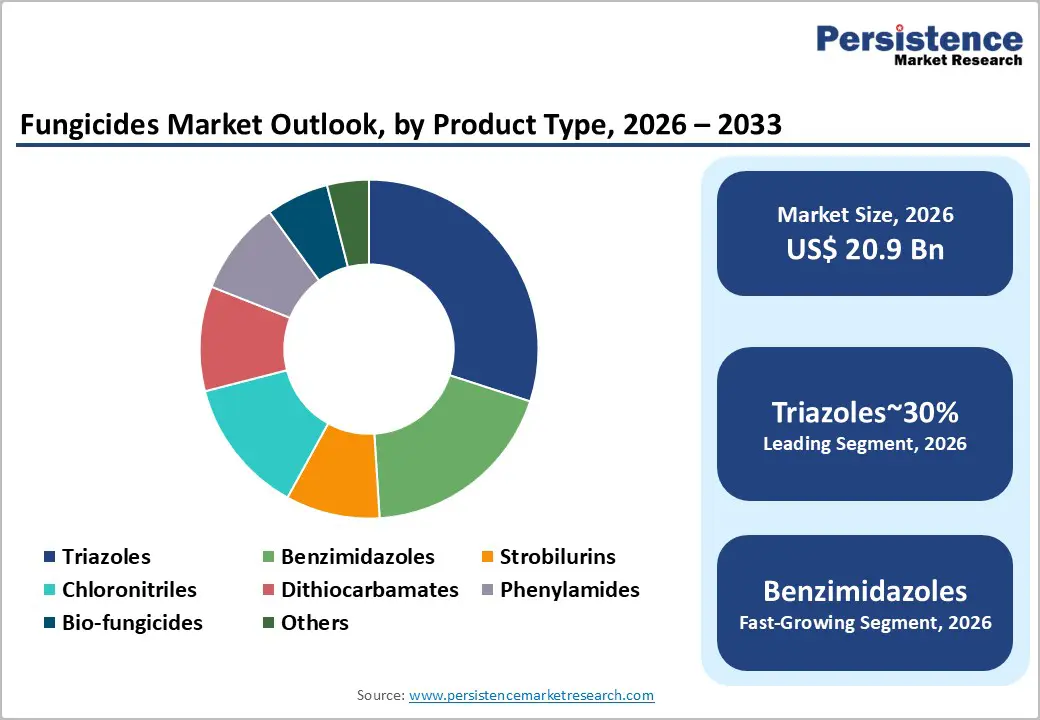

- LeadingSegment: Triazoles dominate as the leading segment by Product Type, holding 30% share due to their systemic efficacy against rust and mildew in cereals, as per global usage trends.

- Fastest Growing Segment: Bio-based fungicides represent the fastest-growing segment by source with a CAGR of 6.3%, propelled by regulatory shifts towards sustainability and organic farming expansions worldwide.

- Key opportunity lies in precision technologies for bio-fungicides, enabling targeted applications that reduce environmental impact while boosting yields in high-value horticulture.

| Key Insights | Details |

|---|---|

| Fungicides Market Size (2026E) | US$ 20.9 Bn |

| Market Value Forecast (2033F) | US$ 30.2 Bn |

| Projected Growth CAGR (2026 - 2033) | 5.4% |

| Historical Market Growth (2020 - 2025) | 4.2% |

Market Dynamics

Driver - Growing Crop Infections and Rising Global Food Demand are Driving Increased Reliance on Fungicides

The rising incidence of fungal diseases across global agriculture continues to be a major driver of growth for the fungicide market, as farmers face increasing threats to crop productivity and food security. Climate variability, high humidity, and intensive farming practices are increasing crop vulnerability to diseases such as rust, blight, and mildew, which significantly reduce yields. According to the FAO, fungal pathogens cause more than $220 billion in crop losses annually, placing pressure on farmers to adopt effective fungicide strategies.

As the global population is projected to reach 9.7 billion by 2050, maintaining stable food supplies will likely become essential, increasing demand for preventive and curative fungicide products. Regulatory bodies such as the JMPR evaluated 37 pesticides in 2024, reinforcing the importance of residue-safe fungicides that support global trade. With fungicides accounting for 22% of global pesticide use, market momentum remains strong amid rising disease pressures.

Sustainable and Innovative Fungicide Technologies are Boosting Market Growth through Improved Efficacy and Reduced Environmental Impact

Technological advances in sustainable fungicide solutions are significantly contributing to the global fungicide market by addressing environmental concerns and improving product performance. Newer active ingredients with novel modes of action offer improved control over resistant fungal strains such as Asian Soybean Rust without harming surrounding ecosystems. These innovations support modern farming needs and comply with increasingly strict environmental regulations.

FAO data indicate that fungicide applications have increased by 54% since the 1990s, attributable to precision-focused formulations that reduce unnecessary use. In addition, biologically integrated fungicides are gaining acceptance in IPM systems as consumers prefer residue-free produce. Regulatory bodies like the EPA continue to encourage the adoption of low-impact products. As a result, sustainable technologies are creating long-term growth potential by enhancing efficacy, reducing environmental risks, and helping farmers manage resistance more effectively.

Restraint - Tightening Global Regulations on Chemical Usage are Restricting Synthetic Fungicide Adoption and Slowing Market Expansion

Stringent environmental and health regulations have become a major restraint on the global fungicide market, as regulatory agencies impose stricter controls on synthetic formulations to minimize ecological risks. The U.S. Environmental Protection Agency (EPA) has introduced strict guidelines under its 2025 Insecticide Strategy, which extend to fungicides to limit spray drift and chemical runoff, affecting nearly 75% of active ingredients in certain cases. These evolving requirements increase compliance and production costs for manufacturers, slowing approvals for new formulations.

The European Food Safety Authority (EFSA) reduced tolerance levels for 47 fungicide active ingredients in 2024, thereby affecting market penetration across Europe. Concerns regarding pollinator health and biodiversity loss, as highlighted in FAO assessments, add further pressure on producers and farmers to shift toward environmentally friendly solutions. These regulatory challenges disrupt supply chains, increase product prices, and constrain the growth rate of the synthetic fungicides segment in key regions.

Increasing Fungal Resistance to Traditional Fungicides is Weakening Product Effectiveness and Raising Treatment Costs

The growing problem of fungal resistance to conventional fungicides poses a critical challenge to market expansion, as reduced product effectiveness increases operational costs for farmers. Overuse and repeated application of older fungicide classes have accelerated the development of resistance in common pathogens, particularly those causing diseases such as powdery mildew. FAO analysis indicates that nearly 30% of traditional fungicide groups have lost substantial efficacy due to mutation-driven resistance, resulting in continued yield losses despite treatment.

In high-intensity farming regions, resistance issues have contributed to a 20% decline in treatment success rates over the past decade. To counter this, regulatory authorities, such as the EPA, require detailed resistance-management plans before approving new products, thereby increasing development timelines. These challenges force farmers to rotate multiple fungicides, increasing costs and operational complexity, while manufacturers face reduced confidence and investment returns in older chemical categories.

Market Opportunity

Rising Demand for Eco-Friendly Farming is Creating Strong Growth Opportunities for Bio-Based Fungicides

The growing adoption of bio-based fungicides represents a major market opportunity, driven by regulatory support and shifting consumer preferences toward safer and eco-friendly agricultural inputs. Governments across major farming economies are promoting integrated pest management systems that incorporate biological agents due to their low toxicity and minimal environmental residues. The EU’s Farm to Fork Strategy aims to reduce pesticide use by 50% by 2030, accelerating demand for bio-fungicides. Innovations enable high-performing, residue-safe crop solutions for rapidly expanding organic markets in Asia and Latin America, where organic farming is growing at 12% annually.

Bio-based fungicides also offer premium pricing advantages for horticulture and greenhouse crops. With the FAO emphasizing sustainable crop protection, the segment presents strong growth opportunities for companies seeking to diversify portfolios and meet rising global demand for environmentally responsible solutions.

Precision Agriculture Tools are Driving Efficient, Targeted Fungicide Use and Opening New Market Opportunities

Precision agriculture technologies are creating strong growth prospects for the global fungicides market by enabling targeted, efficient application methods that reduce waste and operating costs. The use of drones, smart sensors, and AI-driven disease detection helps farmers apply fungicides exactly where needed, lowering total application volumes by nearly 30% while maintaining crop yields, as highlighted in FAO sustainability reports. In North America, USDA-supported initiatives encourage the adoption of such tools to combat fungal outbreaks in crops like soybeans, corn, and wheat.

These solutions also support compliance with EPA guidelines for minimizing drift and improving environmental safety. Precision-enabled fungicide applications enhance the performance of widely used molecules such as tebuconazole, particularly in regions dealing with resistance challenges. As commercial farms increasingly adopt digital agriculture systems, opportunities expand for companies offering integrated fungicide and precision-application technology packages that improve efficiency and long-term profitability.

Category-wise Analysis

By Product Type Insights

Triazoles dominate the By Product Type category of the global fungicides market, holding around 30% market share due to their strong, broad-spectrum performance against major fungal diseases. Key products such as tebuconazole and propiconazole inhibit ergosterol biosynthesis, providing both preventive and curative protection for crops such as cereals, fruits, and vegetables. Their flexible use across multiple application methods and relatively low risk of resistance strengthen their market leadership. Supported by FAO adoption trends and JMPR safety evaluations, triazoles remain a preferred and globally compliant class of fungicides.

By Source Insights

Synthetic fungicides account for nearly 75% of the market, driven by their proven reliability, rapid action, and suitability for large-scale farming. Popular classes like strobilurins offer strong control against diseases such as blight, supporting global yield protection needs. FAO data showing that fungicides account for 22% of overall pesticide use highlight the continued importance of synthetic pesticides. Their widespread availability, stable supply chains, and established regulatory approvals, particularly from the EPA, support their continued dominance, even as the industry shifts toward more environmentally friendly formulations.

By Application Insights

Foliar Spray holds the leading position, accounting for about 60% of global fungicide use, due to its direct and efficient delivery to plant surfaces. This method is particularly effective for managing foliar diseases, such as powdery mildew, in crops such as grapes and vegetables. USDA findings emphasize the role of USDA in IPM programs in achieving strong coverage without soil contamination. With the growing adoption of precision tools, including drones, foliar spraying remains essential for both commercial and horticultural farming.

By End-user Insights

Agricultural use dominates, accounting for 80% share, driven by the need to protect large-scale crop production from serious fungal threats. Fungicides play a critical role in preventing the 20% yield losses reported by the FAO for grains and oilseeds. Both synthetic and bio-based products support farmers in maintaining consistent output and ensuring food security. Strong EPA regulatory guidelines for residue management further reinforce demand, as growers prioritize effective, scalable solutions suited for extensive farmlands.

Regional Insights

North America Fungicides Market Trends

North America continues to experience strong growth in the fungicides market, driven by sophisticated agricultural systems, heavy investment in modern farming technologies, and strict regulatory oversight. The U.S. remains the leading market, with the EPA’s 2025 strategies emphasizing improved management of drift and chemical runoff. These regulations encourage the adoption of advanced fungicide products, such as BASF’s Zorina, which received approval for soybeans and helps reduce white mold losses estimated at more than 26 million bushels annually.

The region’s strong focus on integrated pest management supports the use of digital scouting tools, precision spraying, and sustainable formulations. USDA initiatives further promote bio-based alternatives that align with climate goals and reduce chemical dependency. Amid increasing pressures from unpredictable weather and climate-driven disease outbreaks, growers in North America continue to adopt innovative solutions to improve productivity while minimizing environmental impacts.

Europe Fungicides Market Trends

Europe is the fastest-growing region in the fungicides market, which is heavily shaped by stringent regulatory frameworks, sustainability policies, and advanced farming practices across major economies such as Germany, France, the U.K., and Spain. The European Food Safety Authority (EFSA) tightened residue limits for 47 fungicide active ingredients in 2024, prompting manufacturers and farmers to adopt low-residue and environmentally friendly formulations. This shift has supported the adoption of products, used widely to manage cereal diseases in humid European climates where resistance is a growing concern.

The region’s strong emphasis on green agriculture, supported by the EU Farm to Fork Strategy, promotes the rapid integration of bio-fungicides in viticulture, horticulture, and organic farming. Countries such as France and Spain benefit from harmonized trade regulations and large cultivated areas, ensuring consistent demand. Europe’s balanced approach to innovation, regulation, and sustainability maintains stable market growth despite rising environmental constraints.

Asia Pacific Fungicides Market Trends

The Asia-Pacific region is experiencing rapid growth in the fungicide market, driven by large-scale agricultural production, diverse climatic conditions, and increasing demand for food output. China leads the region in fungicide consumption for crops such as rice, where triazoles are widely used to manage sheath blight, supported by government subsidies and strong domestic manufacturing capabilities.

India is also a major market, benefiting millions of smallholder farmers facing varying disease pressures. Countries across ASEAN offer competitive manufacturing environments, making the region a global supply hub for fungicide production. Japan, known for its advanced agricultural technologies, focuses on high-precision applications for fruits and specialty crops. FAO data showing a 121% increase in herbicide and fungicide use highlight the region’s increasing reliance on crop protection measures to meet growing population needs and food-security challenges.

Competitive Landscape

The global fungicides market displays a consolidated structure, dominated by multinational corporations controlling a significant supply through extensive R&D and global distribution networks. Leaders employ strategies such as mergers and pipeline expansions to counter resistance, with BASF and Syngenta investing in novel actives for sustainable growth. Key differentiators include mode-of-action diversity and IPM compatibility, while emerging models emphasize digital integration for precision delivery, fostering innovation amid regulatory pressures.

Key Developments:

- In October 2025, BASF secured U.S. Environmental Protection Agency approval for Zorina fungicide, combining Endura and Revysol, to help U.S. soybean growers recover more than 26.1 million bushels lost to white mold in 2024.

- In June 2025, BASF initiated registration for Adapzo Active, a novel HDAC-inhibitor fungicide targeting Asian Soybean Rust in South America, offering enhanced resistance-management capability.

- In October 2024, Syngenta launched its technologies ADEPIDYN and TYMIRIUM across several markets, delivering broad-spectrum protection against both fungal and nematode threats for rice and vegetables.

Companies Covered in Fungicides Market

- Nufarm Ltd.

- FMC Corporation

- DuPont

- BASF Agricultural Solutions

- Cheminova A/S

- Bayer CropScience

- Syngenta AG

- Dow AgroSciences

- Lanxess AG

- Monsanto

- Adama Agricultural Solutions

- Simonis B.V.

- E.I. du Pont de Nemours & Company

- Chemtura Corporation

- Corteva Agriscience

- UPL Limited

Frequently Asked Questions

The global fungicides market is expected to reach US$ 30.2 Bn by 2033, reflecting steady growth from US$ 20.9 Bn in 2026 at a 5.4% CAGR, driven by crop protection needs.

Rising fungal disease incidence due to climate change and population growth fuels demand, with FAO noting $220 billion annual losses, necessitating advanced protection for food security.

Triazoles lead by type with 30% share, valued for broad-spectrum control of rust and blight in cereals, supported by systemic efficacy and low resistance rates.

Asia Pacific is dominant accounting for the largest share due to vast farmlands in China and India, where fungicide use addresses disease pressures in rice and wheat production.

Innovation in bio-based and precision fungicides offers key opportunities, aligning with EPA regulations to reduce drift and promote sustainable IPM in horticulture.

Key players include Syngenta AG, BASF Agricultural Solutions, and Bayer CropScience, leading through R&D in novel actives like ADEPIDYN® for resistance management.