- Pharmaceuticals

- Pharmaceutical Sterility Testing Market

Pharmaceutical Sterility Testing Market Size, Share, and Growth Forecast 2026 - 2033

Pharmaceutical Sterility Testing Market by Product Type (Kits and Reagents, Instruments), Test Type (Sterility Testing, Bioburden Testing), Sample (Pharmaceuticals, Medical Devices), End-user (Compounding Pharmacies), and Regional Analysis, 2026 - 2033

Pharmaceutical Sterility Testing Market Size and Trends Analysis

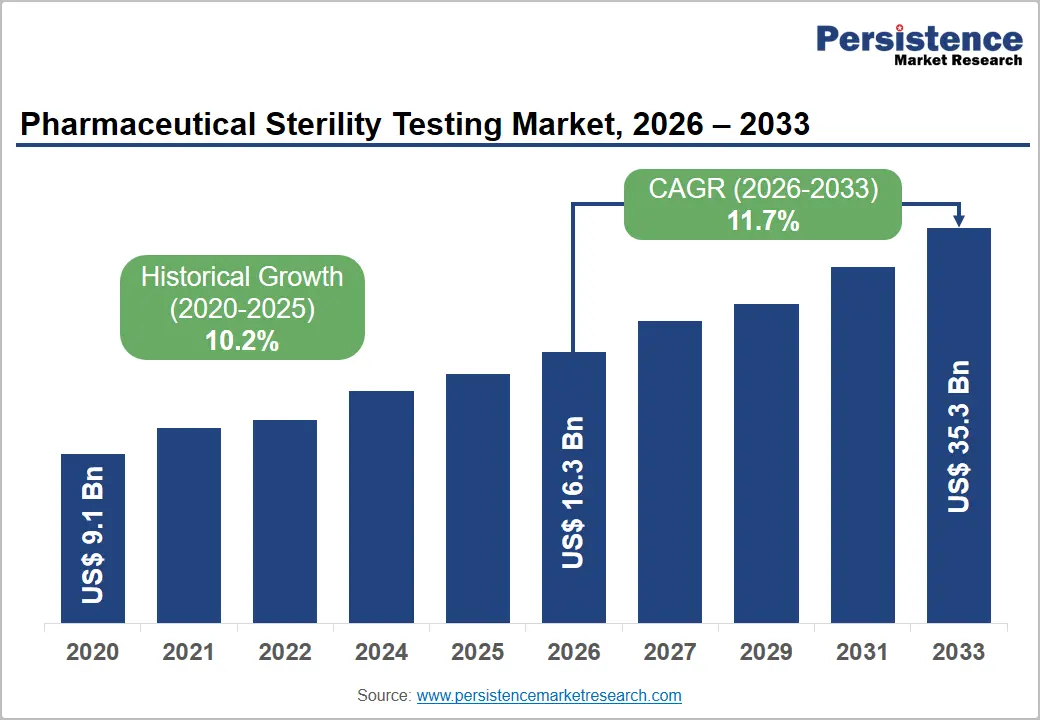

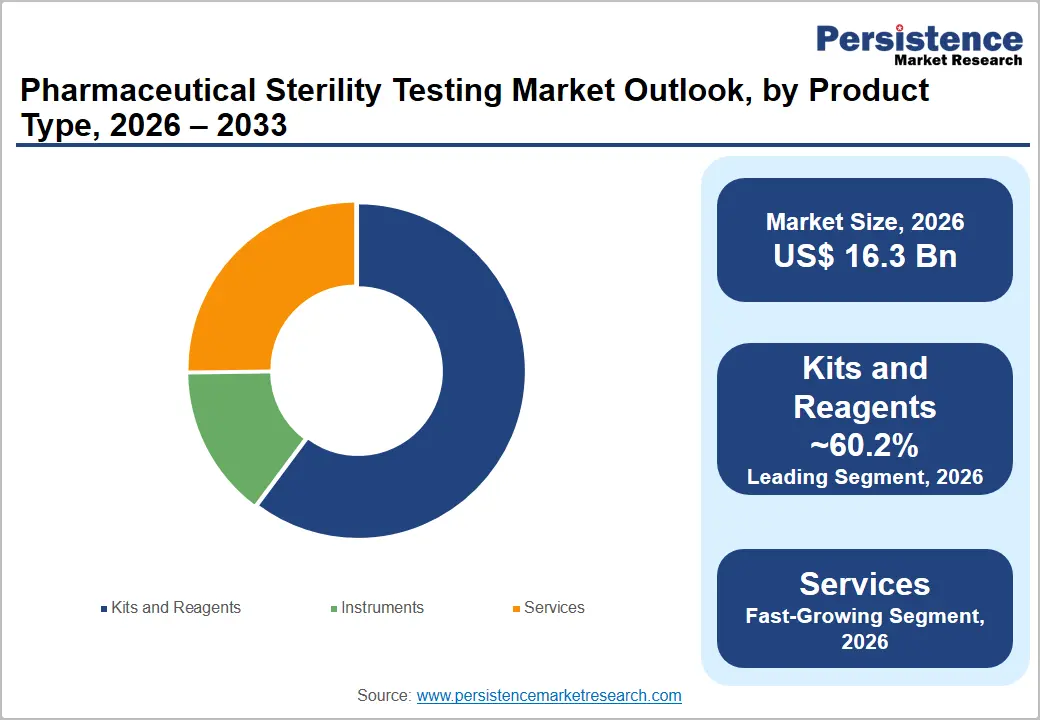

The global pharmaceutical sterility testing market size is likely to be valued at US$16.3 billion in 2026 and is estimated to reach US$35.3 billion by 2033, growing at a CAGR of 11.7% during the forecast period from 2026 to 2033, driven by rising approval and production of biologics and injectable drugs that require strict sterility validation. Surging adoption of rapid microbiological testing methods to reduce batch release timelines is also predicted to drive growth.

Key Industry Highlights

- Leading Product Type: Kits and reagents, approximately 60.2% share in 2026, as they provide pre-validated components that ensure compliance with pharmacopeia guidelines and reduce testing variability.

- Dominant Test Type: Bioburden testing, with a nearly 43.6% share in 2026, as it enables early detection of microbial contamination during production.

- Latest Product: In September 2025, Nelson Laboratories launched RapidCert, a rapid Biological Indicator (BI) sterility testing service. The new solution combines traditional biological indicators with rapid microbiological methods and reduces incubation time to 48 hours, compared with seven days required under conventional methods.

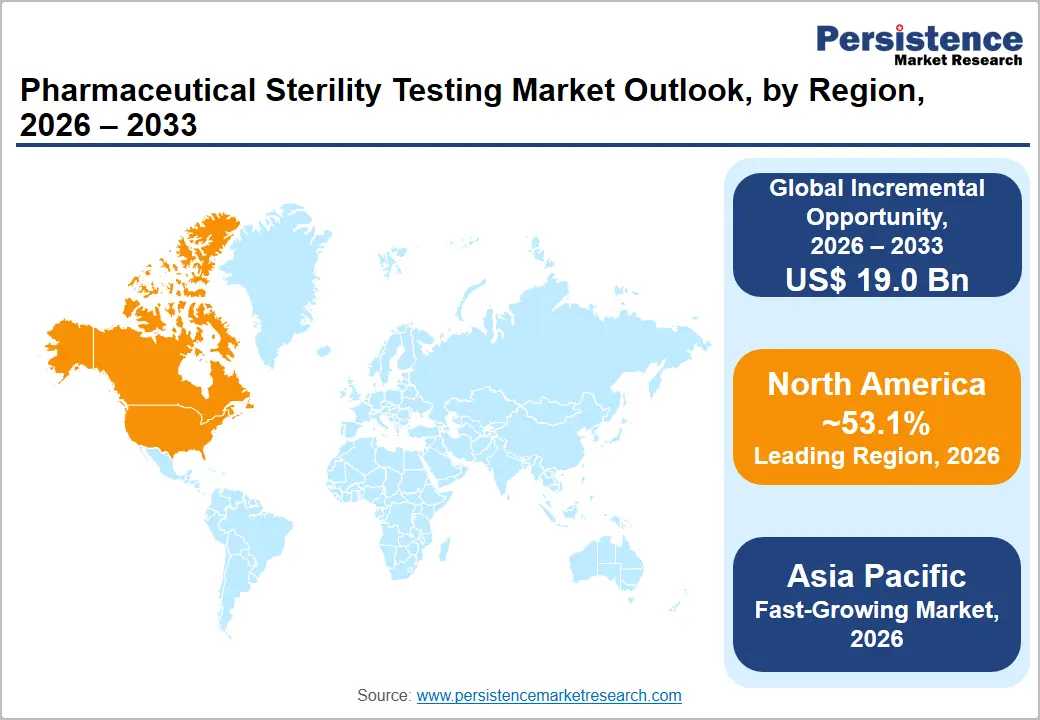

- Leading Region: North America, with about a 53.1% share in 2026, owing to strict regulatory enforcement by the U.S. FDA.

- Fast-growing Region: Asia Pacific, backed by the increasing shift of global pharmaceutical manufacturing to India and China.

DRO Analysis

Driver - Biologics Approvals to Create a Large Testing-Obligated Product Base

Every injectable biologic, including monoclonal antibodies (mAbs), biosimilars, and Advanced Therapy Medicinal Products (ATMPs), must pass sterility testing before it can be released for patient use. This regulatory obligation means the testing market extends directly in proportion to the pipeline. According to a peer-reviewed analysis published in Biomedicines (2025), biologics accounted for 32% of all U.S. Food and Drug Administration (FDA) drug approvals in 2024, with 13 mAbs approved, the highest number since 2015.

By mid-2025, six additional biologics had already received approval, indicating the pace will be sustained. As each product is formulated as a sterile injectable, every approval adds a permanent sterility testing requirement to the manufacturer's routine Quality Control (QC) workflow. It is anticipated to propel demand across the testing lifecycle of each drug.

Updated Manufacturing Rules to Push Quality Control Work to Contract Labs

The revised European Union (EU) Good Manufacturing Practice (GMP) Annex 1, which became fully effective in August 2023, significantly raised the bar for sterile product manufacturing. The updated regulation, which extended from 16 to 58 pages, now mandates a documented Contamination Control Strategy (CCS) covering the entire facility, including any outsourced steps.

It also explicitly requires that Contract Development and Manufacturing Organizations (CDMOs) and contract laboratories holding sterility testing responsibilities be included within the CCS scope and that quality agreements define data-sharing and batch-release access. Hence, small-scale manufacturers who lack the cleanroom infrastructure or isolator capacity to comply in-house are increasingly directing sterility testing to specialist contract labs equipped to meet the new requirements.

Restraint - High Setup Cost of Isolator-Based Testing Infrastructure

Pharmaceutical manufacturers face increasing pressure to implement isolator technology for sterility testing, driven by the strong recommendations outlined in EU GMP Annex 1 and the superior contamination control isolators provide compared to conventional laminar airflow hoods. However, the substantial upfront investment, operational expenses, and ongoing maintenance requirements associated with isolator systems remain significant challenges, particularly for small and mid-sized manufacturers, thereby constraining broader market adoption.

Validating an isolator requires extensive documentation, engineering qualification runs, and dedicated QA oversight, a process that can span several months before the system is cleared for routine use. Hence, multiple small-scale manufacturers are unable to independently meet the isolator requirement, compelling them either to delay compliance or depend entirely on outsourced testing partners. Until modular and low-cost isolator designs become more accessible, this capital barrier will likely continue to restrict adoption across the market’s small participants.

Opportunity - Fast Detection Technology to Replace Traditional 14-Day Testing Window

The conventional sterility test under United States Pharmacopeia (USP) general chapter <71> requires a 14-day incubation period. This makes it one of the slowest steps in pharmaceutical batch release. The delay is augmenting the adoption of Rapid Microbiological Methods (RMMs). In March 2025, Nelson Labs, a Sotera Health company and global testing organization with over 900 laboratory tests across 12 facilities, announced rapid sterility testing services at sites in the U.S. and Germany.

It aims to cut incubation from 14 days to six using bioluminescence technology while remaining USP-compliant. In October 2025, Lonza acquired Redberry SAS to integrate its Red One solid-phase cytometry (SPC) platform for rapid sterility and bioburden testing. It explicitly cited that the technology would lower compliance costs and support biologics as well as cell and gene therapy production. These transactions showcase rising commercial confidence in RMMs as a production-ready alternative.

Short-Lived Cell and Gene Therapies to Demand Purpose-Built Sterility Frameworks

Cell and gene therapies present a testing problem that conventional sterility methods cannot solve. Their shelf lives are often shorter than the 14-day incubation window required by standard compendial tests. This means a product could expire before its sterility is confirmed. On 1 August 2025, the U.S. Pharmacopeia (USP) introduced chapter <72>, the first official USP chapter permitting respiration-based rapid microbiological methods for short-shelf-life products such as cell and gene therapies.

It does not require the extensive alternative method validation previously needed under USP <1223>. This places the validation burden for rapid methods on par with the established standard. As of December 2023, 33 cell and gene therapies had been approved by the FDA, with thousands more in clinical development. It is creating an expanding pool of products that will require sterility testing frameworks specifically built for short-shelf-life release.

Category-wise Analysis

Product Type Insights

Kits and reagents are predicted to lead with a share of approximately 60.2% in 2026, as sterility testing must follow strict pharmacopeia standards such as USP <71> and EU GMP Annex 1. Pre-validated kits reduce human errors and variations between labs. This is important in regulated environments where even minor deviations can lead to batch rejection. For example, the U.S. Pharmacopeia clearly defines the use of standardized media and reagents for sterility testing, which pushes companies to adopt ready-to-use kits instead of preparing media in-house.

Services are estimated to be the fastest-growing segment over the forecast period. This is due to the fact that pharmaceutical companies are now outsourcing sterility testing to specialized contract labs to avoid maintaining costly cleanroom environments and trained microbiology teams. Sterility testing requires controlled environments such as ISO Class 5 cleanrooms, which are expensive to build and maintain. According to the U.S. Food and Drug Administration (FDA), aseptic testing environments must meet strict contamination control standards, making in-house setups resource-intensive.

Test Type Insights

The bioburden testing segment is anticipated to dominate with a share of nearly 43.6% in 2026 as it helps manufacturers monitor microbial load before sterilization. Unlike sterility testing, which is performed at the end, bioburden testing provides early insights into contamination risks during production. This complies with modern quality approaches such as Quality by Design (QbD), promoted by the International Council for Harmonization.

The sterility testing segment is expected to remain in the second position in 2026, as it is legally required before releasing sterile pharmaceutical products such as injectables, ophthalmics, and biologics. Regulatory agencies do not allow product release without confirming the absence of viable microorganisms. The European Medicines Agency mandates sterility testing as part of batch release under EU GMP guidelines, making it unavoidable for manufacturers.

Regional Insights

North America Pharmaceutical Sterility Testing Market Trends

North America is predicted to dominate in 2026 with a share of approximately 53.1%, as sterility testing is tightly enforced by regulators. The U.S. Food and Drug Administration (FDA) requires sterility assurance for every batch of sterile drugs. This creates consistent demand across pharmaceutical and biotech companies. The region also has a high number of biologics and injectable drug approvals, which require extensive sterility testing. Another key factor is the presence of advanced testing infrastructure.

The U.S. has a large network of GMP-certified labs and contract testing providers. In 2025, Charles River Laboratories expanded its microbial testing capacity in North America to support rising demand from cell and gene therapy developers.

U.S. Pharmaceutical Sterility Testing Market Trends

A share of nearly 55.4% is expected to be held by the U.S. in 2026, owing to its leadership in advanced therapies. Cell and gene therapies require fast sterility testing methods, which is propelling the adoption of rapid microbiological technologies. According to the U.S. FDA, more than 20 cell and gene therapies were approved or under priority review in recent years, increasing demand for specialized sterility testing. The country is also investing in alternative methods. The FDA supports rapid sterility testing under its emerging technology program. This encourages companies to adopt quick and automated solutions.

Asia Pacific Pharmaceutical Sterility Testing Market Trends

Asia Pacific is anticipated to be the fastest-growing region in 2026 with a share of nearly 26.9%, as global pharmaceutical manufacturing is shifting to this region. China and India offer low production costs and large-scale manufacturing capacity. This increases the demand for sterility testing to meet export standards. Governments are also strengthening regulatory frameworks. For example, the National Medical Products Administration has updated GMP guidelines to comply more closely with global standards, which increases testing requirements. This regulatory compliance is pushing companies to invest more in sterility testing capabilities.

China Pharmaceutical Sterility Testing Market Trends

China will likely lead in Asia Pacific in 2026 with a share of around 41.5%, backed by its fast-expanding biologics sector. The country has seen a rise in domestic monoclonal antibody and vaccine production. These products require strict sterility assurance. In recent years, the National Medical Products Administration introduced reforms to speed up drug approvals while maintaining quality standards, increasing testing demand. Another factor is investment in local testing infrastructure. Local companies are building in-house GMP labs and partnering with global testing firms. This improves testing capacity and supports market growth.

India Pharmaceutical Sterility Testing Market Trends

In 2026, India is projected to account for a share of approximately 22.8%, as it is one of the largest producers of generic drugs and vaccines. Sterility testing is important for export-oriented manufacturing. The Central Drugs Standard Control Organization enforces sterility testing for injectable drugs under Indian Pharmacopeia standards. The country also gained attention during COVID-19 vaccine production. Domestic manufacturers extended sterile manufacturing facilities. This created long-term demand for sterility testing.

Europe Pharmaceutical Sterility Testing Market Trends

Europe will likely see decent growth in the forecast period, with a share of nearly 12.7% in 2026, owing to strong regulatory systems and rising biosimilar production. The European Medicines Agency mandates strict sterility testing under EU GMP Annex 1, which ensures consistent demand across countries. The region is also a leader in biosimilars. These products require similar sterility assurance as original biologics. As more biosimilars are developed, the demand for sterility testing continues to rise. This creates stable and long-term growth rather than sudden spikes.

Germany Pharmaceutical Sterility Testing Market Trends

Germany will likely register a substantial share of approximately 37.6% in 2026, as it has a well-established pharmaceutical manufacturing base and advanced laboratory infrastructure. Companies in Germany are early adopters of automated and rapid sterility testing technologies. For example, Sartorius AG has been extending its microbiology solutions portfolio, including tools for sterility and bioburden testing. This shows the country’s focus on innovation and high-quality production standards.

U.K. Pharmaceutical Sterility Testing Market Trends

A share of around 19.2% is predicted to be held by the U.K. in 2026, spurred by its superior clinical research network. The Medicines and Healthcare products Regulatory Agency maintains strict quality standards for sterile products, ensuring continued testing demand. The country is also active in advanced therapy research. Several clinical trials for cell and gene therapies are conducted in the U.K., which increases the demand for rapid and reliable sterility testing. This positions the country for stable growth rather than quick expansion.

Competitive Landscape

The global pharmaceutical sterility testing market is moderately fragmented with the presence of large multinational testing providers, specialized microbiology laboratories, rapid microbiological technology developers, and contract testing organizations. Companies such as STERIS plc, Charles River Laboratories, Sartorius AG, Thermo Fisher Scientific, SGS SA, Nelson Laboratories, and Rapid Micro Biosystems are investing heavily in automation, digital microbiology, and rapid microbial detection technologies. They aim to reduce product-release timelines for pharmaceutical and biopharmaceutical manufacturers.

A key competitive trend is the race to support the fast-growing cell and gene therapy sector, where conventional sterility testing timelines are often impractical. Another area of competition is outsourced testing services. Pharmaceutical companies now prefer specialized laboratories rather than maintaining extensive in-house sterility testing infrastructure. Hence, Nelson Labs, SGS, Charles River Laboratories, Pace Analytical, and Solvias continue expanding laboratory capacity and regulatory-compliant testing services.

Key Industry Developments:

- In April 2026, Sapho Bio announced that it had secured US$5 million in funding and completed USP <1223> validation for its rapid sterility testing platform. The company stated that its RNA-based assay can detect viable bacterial and fungal contamination in approximately 20 hours, offering a significant reduction compared with the traditional 14-day sterility testing process.

- In October 2025, Recipharm inaugurated new parenteral development and sterility laboratories at its Bengaluru, India facility. The company reported that the investment would strengthen its sterile pharmaceutical development and testing capabilities while supporting clients with regulatory-compliant sterility and analytical testing services.

- In September 2025, FUJIFILM Wako Pure Chemical Corporation launched the RiboNAT Rapid Sterility Test for cell therapy applications. The kit was developed to overcome the limitations of conventional 14-day sterility testing and provide rapid microbial detection for cell therapies that often require administration within a few days of production.

Companies Covered in Pharmaceutical Sterility Testing Market

- Pacific Biolabs

- Steris Plc

- Boston Analytical

- Nelson Laboratories, LLC (Sotera Health)

- Sartorius AG

- SOLVIAS AG

- SGS SA

- Labcorp

- Pace Analytical

- Charles River Laboratories

- Thermo Fisher Scientific, Inc.

- Rapid Micro Biosystems

- Almac Group

- Labor LS SE & Co. KG

Frequently Asked Questions

The global pharmaceutical sterility testing market is projected to be valued at US$16.3 billion in 2026.

The pharmaceutical sterility testing market is expected to reach US$35.3 billion by 2033.

Key market trends include the shift toward rapid microbiological methods and the launch of integrated testing platforms to reduce turnaround time.

Kits and reagents are expected to be the leading product type with a share of nearly 60.2% in 2026.

The pharmaceutical sterility testing market is expected to grow at a CAGR of 11.7% from 2026 to 2033.

Pacific Biolabs, Steris Plc, and Boston Analytical are a few key market players.