- Advanced Materials

- Mulch Film Market

Mulch Film Market Size, Share, and Growth Forecast, 2026 - 2033

Mulch Film Market by Product Type (Conventional (LDPE, LLDPE, HDPE, EVA), Biodegradable Mulch Films (PBAT, PLA, Starch-based blends - TPS, PLA/Starch, PHA/Starch)), Function (Light-blocking Films, Light-transmitting Films.), Application (Agriculture (Cereals & Grains, Oilseeds & Pulses, Fiber Crops), Horticulture (Fruits & Vegetables, Roots & Tubers, Floriculture & Ornamentals)), Regional Analysis for 2026 - 2033

Mulch Film Market Size and Trends Analysis

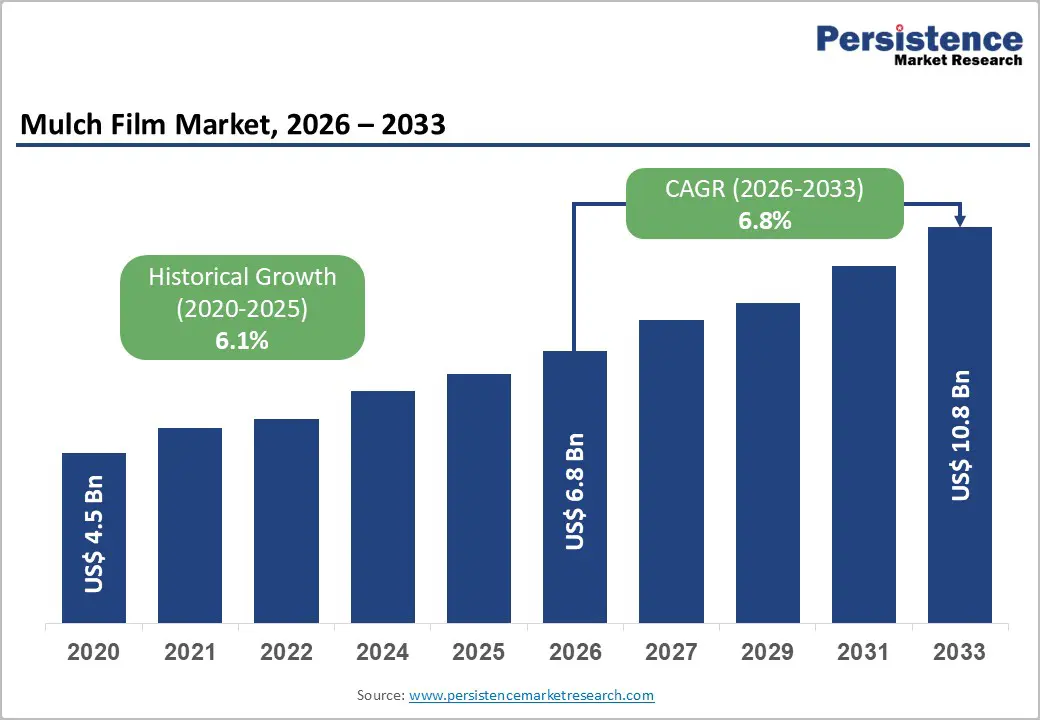

The global mulch film market size was valued at US$6.8 billion in 2026 and is projected to reach US$10.8 billion by 2033, growing at a CAGR of 6.8% between 2026 and 2033.

The market demonstrated strong historical momentum, reflecting consistent demand from the global agriculture and horticulture sectors. Primary growth catalysts include widespread adoption of precision agriculture techniques, regulatory mandates against conventional plastic use, and the accelerating transition toward biodegradable film alternatives.

Key Industry Highlights:

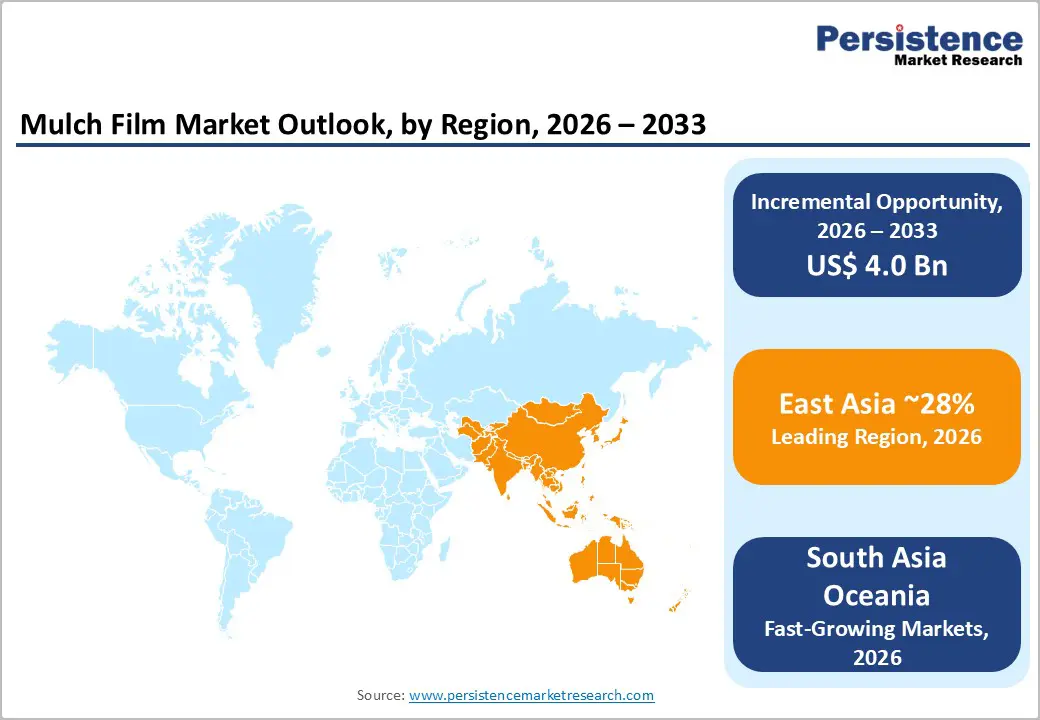

- Regional Leadership: East Asia is likely to account for 32% share in 2026, driven by China’s extensive adoption of conventional and biodegradable mulch films across cotton, maize, and vegetable cultivation.

- Fast-growing Region: North America accounts for 22% share, supported by high-value horticulture, speciality crop production, and adoption of nutrient-enhanced and functional biodegradable films.

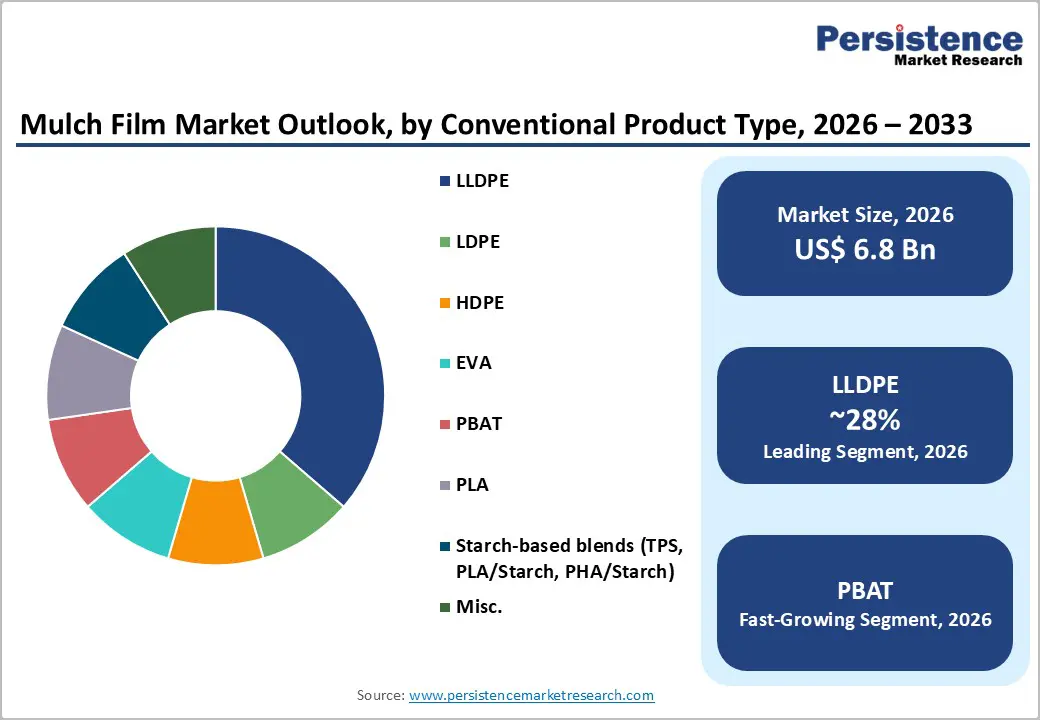

- Leading Product: Conventional Films Dominate: LLDPE mulch films remain the largest material segment with 28% share, offering flexibility, puncture resistance, and UV stabilisation for large-scale cereal, grain, and oilseed farming.

- Fast-growing Product: Biodegradable Films on the Rise: PBAT-based films are the fastest-growing segment, valued for mechanical strength, in-soil biodegradability, and compatibility with sustainable agriculture practices.

- Agriculture Applications Lead: The agriculture segment accounts for 55% revenue, with cereals and grains as the largest sub-segment, while fruits and vegetables are the fastest-growing due to high-intensity use in premium crops.

- Innovation and Sustainability Driving Adoption: Developments like Bumigro’s Microbe Edible Mulch Film and Sinopec’s PBST pilot expand opportunities by enhancing soil health, conserving water, and eliminating microplastic residues.

| Global Market Attributes | Key Insights |

|---|---|

| Mulch Film Market Size (2026E) | US$ 6.8 Bn |

| Market Value Forecast (2033F) | US$ 10.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.1% |

Market Dynamics

Growth Drivers

Global Food Security Imperative and Agricultural Intensification

The fundamental need to feed a rapidly expanding global population while managing finite arable land resources is a defining structural driver for the Mulch Film Market. Mulch films address this challenge directly by enhancing soil moisture retention, regulating soil temperature, suppressing weed competition, and accelerating crop maturity cycles, collectively contributing to yield improvements of 20% to 50% in field conditions, depending on crop type and agro-climatic zone.

India's domestic agrochemical market, valued at US$7.82 billion in FY24, underlines the scale of agricultural intensification underway in key emerging markets. In the United States, food and beverage manufacturing accounted for 16.8% of total U.S. manufacturing sales in 2021, reflecting the deep integration of agricultural inputs into economic output. The herbicide segment in India recorded a CAGR of around 10% between FY21 and FY24, underscoring the broader trend toward chemical and material-based crop management solutions. Mulch films operate in concert with these inputs, reducing pesticide requirements while protecting soil microbiomes, a dual benefit that resonates across both developed and developing agricultural markets.

Regulatory Pressure Against Conventional Plastic Films and the Shift Toward Sustainable Agriculture

Tightening environmental regulations governing single-use and agricultural plastics are compelling farmers, cooperatives, and agribusinesses to reassess their reliance on conventional polyethylene mulch films. The European Union's pesticide consumption reached a recorded low of approximately 292,000 tonnes in 2023, the lowest level since 2011, reflecting the impact of stricter environmental and safety regulations on agricultural practices.

In parallel, the EU Commission and AIMPLAS initiated formal assessments in July 2024 to evaluate the inclusion of soil-biodegradable mulch films under the EU Fertilising Products Regulation, with certified films demonstrating effective in-soil biodegradation and agronomic performance comparable to conventional plastics. Novamont's Mater-Bi mulch film was certified under the EU Fertiliser Regulation 2019/1009 as an inorganic soil improver in November 2025, recognising its full biodegradability and zero microplastic residue profile. These regulatory milestones directly stimulate substitution demand in the Mulch Film Market by establishing formal certification pathways and creating commercially viable routes for the adoption of biodegradable products.

Technological Advancement in Biodegradable and Functional Film Materials

Material science innovation is fundamentally broadening the performance and cost competitiveness of next-generation mulch films, unlocking applications previously limited to conventional polyethylene. PBAT-based formulations now deliver mechanical durability comparable to LLDPE films while offering certified in-soil biodegradation within 90 to 180 days under standard agricultural conditions. BASF's ecovio M2351, a certified soil-biodegradable PBAT-based mulch film, demonstrated measurable improvements in tomato cultivation enabling farmers to plough films directly into soil post-harvest while reducing plastic residues, improving weed control, conserving water, and supporting crop quality.

In February 2026, Bumigro's Microbe Edible Mulch Film was recognised as a Top 10 New Product at the World Ag Expo, introducing a biodegradable, microbe-powered architecture that enhances soil health and eliminates microplastic residues. Additionally, Sinopec's successful pilot of fully biodegradable PBST mulch films in Xinjiang cotton fields in November 2025 demonstrated moisture and heat retention performance equivalent to traditional PE films. These technological milestones directly expand the addressable opportunity for the Mulch Film Market by enabling farmers to achieve productivity targets without compromising environmental compliance.

Market Restraining Factors

High Cost of Biodegradable Films Relative to Conventional Alternatives

PBAT and PLA-based films carry raw material costs substantially above those of LLDPE or LDPE, limiting adoption primarily to high-value horticultural crops where the economics of yield improvement can justify the incremental investment. In smallholder-dominated agricultural economies, which collectively account for a substantial share of global mulch film demand in South and Southeast Asia, price sensitivity remains a critical adoption barrier. Although advances in polymer compounding and production scale are gradually narrowing this cost differential, the gap remains wide enough to constrain market penetration in commodity crop applications, dampening the pace of technology transition and creating a dual-track market dynamic

Environmental and Disposal Challenges Associated with Conventional PE Films

Despite their cost advantages, conventional polyethylene mulch films, including LDPE, LLDPE, and HDPE variants, present significant end-of-life management challenges that are increasingly attracting regulatory scrutiny. PE films degrade into microplastic particles that infiltrate soil profiles, disrupt nutrient cycling, harm soil organisms, and potentially enter the food chain through crop uptake. Post-harvest film retrieval in large-scale cereal and grain cultivation is labour-intensive and often incomplete, leading to soil contamination that compounds across successive growing seasons. European Union member states have recorded measurable soil microplastic contamination from accumulated film residues, triggering policy discussions on mandatory biodegradability requirements. These environmental liabilities create reputational and compliance risks for conventional film producers, constraining their long-term market positioning even as they retain dominant volume share in the near term.

Key Market Opportunities

Government-Led Biodegradable Agriculture Programs and Regulatory Certification Frameworks

The formalisation of regulatory certification frameworks for biodegradable mulch films across major agricultural economies represents a transformative structural opportunity for the Mulch Film Market. As governments move beyond voluntary sustainability commitments toward binding regulatory frameworks, certified biodegradable films stand to benefit from preferential procurement, subsidy support, and expanded market access.

The EU's Fertilising Products Regulation provides a concrete precedent: Novamont's Mater-Bi certification as an inorganic soil improver under this regulation in November 2025 establishes a replicable compliance pathway for other manufacturers. In India, the food processing sector attracted US$ 13.4 Billion in FDI inflows between 2000 and June 2025, and large-scale government initiatives including 41 Mega Food Parks and extensive cold-chain expansion are systematically elevating the role of precision agricultural inputs.

AIMPLAS's development of compostable mulch films through the AGRO+ Project, enabling used films to be converted into high-quality compost, further demonstrates the policy-industry alignment that can accelerate adoption. These developments collectively indicate that regulatory recognition is transitioning from an emerging prospect to an established commercial reality for biodegradable film producers.

Nutrient-Enhanced and Multifunctional Film Innovations Addressing Unmet Crop Needs

Conventional mulch films deliver value primarily through physical protection, moisture retention, weed suppression, and thermal regulation. The development of nutrient-enhanced and biologically functional films represents a significant product evolution that can unlock premium pricing and expand addressable applications within the Mulch Film Market.

Lehigh University, with USDA backing and international research partners, is developing biodegradable nutrient-enhanced mulch films that deliver essential crop nutrients while naturally degrading in soil, offering simultaneous input consolidation and waste reduction benefits. Central South University of Forestry and Technology in China developed a bamboo-based biodegradable liquid slow-release mulch film for selenium-enriched crops in July 2025, providing soil moisture retention, heat regulation, and improved soil structure in a single application. BioBag World Australia introduced its BioAgri mulch film made from Mater-Bi in 2026, providing a cost-effective, microplastic-free solution for Australian growers. These functional innovations are transforming mulch films from commodity inputs to value-added agronomic solutions, a positioning shift that supports margin improvement for manufacturers and opens new segments in precision farming and speciality crop production.

Food Processing Sector Expansion Driving Demand for High-Quality Horticultural Produce

The structural expansion of formal food processing industries across Asia and the Americas is creating intensified demand for standardised, high-quality horticultural raw materials a demand that mulch film adoption directly enables. As food processors require consistent produce quality, growers are incentivised to adopt inputs, including mulch films, that enhance crop uniformity, reduce surface contamination, and extend shelf life.

India's food processing sector contributed 8.8 per cent of manufacturing GVA and 8.4 percent of agricultural GVA in 2024, was valued at Rs. 30.5 lakh crore (US$354.5 billion), and is projected to reach Rs. 45.8 lakh crore (US$ 535 Billion) by FY26. In the United States, food and beverage manufacturing accounted for 15% of manufacturing value added in 2021, with over 42,700 establishments operating nationally, creating a geographically distributed network of quality-sensitive procurement.

The EU accommodation and food services sector employed approximately 10.9 million people in 2022 and generated €280.7 Billion in value added, reflecting robust food sector activity that indirectly supports grower adoption of productivity-enhancing inputs. The Mulch Film Market is well-positioned to capture incremental demand from this channel as food supply chain traceability and quality standards tighten globally.

Category-wise Analysis

Product Type Insights

Conventional mulch films constitute the dominant product type in the global market, accounting for 68% of overall product type revenue in 2026. Within this segment, LLDPE leads with a 28% share of the conventional category, making it the single largest material sub-segment across the entire product type classification. LLDPE's dominance is attributable to its superior balance of mechanical flexibility, puncture resistance, and UV stabilisation capability, properties that make it the material of choice for large-scale cereal, grain, and oilseed cultivation. Its established manufacturing infrastructure, broad supplier base, and predictable cost profile further reinforce its position.

The conventional segment also encompasses LDPE, HDPE, and EVA variants, each serving specialised applications where specific optical, thermal, or physical properties are required. Despite environmental pressures, the sheer scale of conventional cereal and grain agriculture globally sustains a high volume offtake for LLDPE-based products, and the segment is expected to retain the majority share through the forecast period even as biodegradable alternatives gain ground.

PBAT polybutylene adipate terephthalate is the fastest-growing material segment within the Mulch Film Market, driven by its unique combination of flexibility, mechanical strength, and certified in-soil biodegradability. Unlike PLA, which can be brittle at low temperatures, PBAT offers physical handling properties closely analogous to conventional PE films, reducing the learning curve for farmers transitioning from traditional materials. Sinopec's November 2025 pilot of fully biodegradable PBST mulch film in Xinjiang cotton fields demonstrated effective degradation alongside moisture and heat retention comparable to traditional PE films a critical validation milestone for PBAT-class materials in large-scale commercial agriculture.

Application Insights

The agriculture segment is the dominant application category, accounting for 55% of total application revenue in 2026. Within this segment, Cereals and Grains command a 22% share of the agriculture application, making it the highest-volume end-use sub-category in the entire Mulch Film Market. Mulch films deployed in cereal and grain production deliver measurable benefits through moisture conservation in semi-arid cultivation zones, soil temperature stabilisation during early germination phases, and reduction of interrow weed competition collectively contributing to yield stability and input efficiency at scale.

Key consuming states in India for agrochemicals include Maharashtra, Goa, Andhra Pradesh, Telangana, and Madhya Pradesh, where intensive cereal and oilseed agriculture underpins consistently high mulch film demand. The agriculture segment also encompasses Oilseeds and Pulses, Fibre Crops, and miscellaneous field crops, each with distinct mulch film specifications and adoption rates driven by crop economics and agronomic practices.

Fruits and vegetables are the fastest-growing sub-segment, fueled by the global consumer shift toward fresh produce consumption, the expansion of controlled environment agriculture, and the premium pricing that quality-differentiated fruits and vegetables command in formal retail channels. Mulch film usage in this segment is characterised by high intensity, with multiple film applications per season in row crop production of strawberries, tomatoes, peppers, cucumbers, and soft fruits...

Regional Insights and Trends

North America Mulch Film Market Trends

North America accounts for 22% of the global Mulch Film Market revenue in 2026, representing a substantial and technologically sophisticated regional market. The United States anchors demand, driven by a well-capitalised commercial agriculture sector with strong adoption of precision farming inputs. U.S. food and beverage manufacturing comprised 16.8% of total manufacturing sales in 2021, with over 42,700 establishments distributed across California, Texas, and New York states, also characterised by high-intensity horticultural and speciality crop production, where mulch film utilisation is highest.

The regulatory environment in North America is evolving toward greater sustainability accountability: the USDA's active funding of Lehigh University's biodegradable nutrient-enhanced mulch film research signals growing federal interest in transitioning agricultural film use toward environmentally compliant alternatives. Innovation-led differentiation is a defining characteristic of North American competitive dynamics, with multinational chemical companies leveraging R&D capabilities to introduce high-performance functional films.

The integration of mulch films into broader precision agriculture ecosystems including soil sensors, drip irrigation, and GPS-guided application equipment, further elevates their strategic value in this region.

East Asia Mulch Film Market Trends

East Asia is the largest regional contributor to the Global Mulch Film Market, accounting for 32% of global revenue in 2026, with China serving as the dominant country market. China's agricultural policy framework has historically been among the most supportive globally for plastic film adoption in field crops, with mulch film use across cotton, maize, and vegetable cultivation deeply embedded in northern and northwestern farming systems.

Growing environmental concern over plastic residue accumulation has prompted significant policy reorientation: China's government has actively mandated degradable film pilot programs, with Sinopec's November 2025 successful pilot of fully biodegradable PBST mulch film in Xinjiang cotton fields representing a landmark commercial validation of this national direction. Central South University of Forestry and Technology developed a bamboo-based biodegradable liquid slow-release mulch film in July 2025, supported by national research priorities around selenium-enriched crop production and sustainable agriculture. Japan and South Korea contribute to regional demand through high-value horticultural and protected cultivation applications, where premium functional films with controlled optical and thermal properties command significant market share.

Europe Mulch Film Market Trends

Europe accounts for 18% of the Global Mulch Film Market in 2026, characterised by a high-regulatory, sustainability-driven market environment that is increasingly shaping product standards globally. EU pesticide consumption reached a low of approximately 292,000 tonnes in 2023, reflecting sustained pressure on agricultural chemical use that indirectly benefits mulch films as a mechanical alternative to herbicides for weed management. France, Spain, Germany, and Italy collectively account for 52% of the EU's utilised agricultural area and 49 percent of arable land, making them the primary European demand centres for mulch films.

The EU's formal assessment of soil-biodegradable mulch films under the Fertilising Products Regulation, initiated in July 2024 by the EU Commission through AIMPLAS, is a pivotal regulatory development that could redefine product standards across the continent. Novamont's Mater-Bi mulch film received AIAB organic farming certification as early as February 2020, and its subsequent EU Fertiliser Regulation 2019 per 1009 certification in November 2025 illustrates the maturation of the European biodegradable film regulatory pathway.

Competitive Landscape

The global mulch film market is moderately fragmented, with competition spread across multinational chemical giants and regional specialists. Leading players such as BASF SE, Berry Global Inc., and The Dow Chemical Company dominate through extensive R&D, advanced polymer technology, and global distribution networks, offering high-performance and biodegradable mulch films. European firms like RKW Group, Novamont S.p.A., and Armando Alvarez Group focus on sustainable and premium solutions, particularly in horticulture, while other notable players, such as AEP Industries Inc. and BioBag International AS compete regionally with niche offerings.

Market dynamics are increasingly driven by the rising demand for eco-friendly and biodegradable films, prompting innovation and strategic collaborations. Despite this, no single player fully dominates, keeping the market competitive yet open to new entrants.

Key Industry Developments

- February 25, 2026, Bumigro’s Microbe Edible Mulch Film was named a Top 10 New Product Winner at the 2026 World Ag Expo, highlighting the company’s leadership in sustainable agricultural innovation by introducing a biodegradable, microbe-powered mulch film that enhances soil health, reduces labour costs, and eliminates microplastic residues.

- November 6, 2025, Novamont’s Mater-Bi mulch film was certified under EU Fertiliser Regulation 2019/1009 as an inorganic soil improver, recognising its biodegradability, zero microplastic residue, and soil health benefits, positioning it as a sustainable solution for weed control while complying with environmental and soil protection standards.

- November 14, 2025, Sinopec successfully piloted its fully biodegradable PBST mulch film in Xinjiang cotton fields, demonstrating effective degradation, moisture and heat retention, and crop yield comparable to traditional PE films, offering a sustainable solution to residual plastic pollution while supporting green agriculture.

Companies Covered in Mulch Film Market

- BASF SE

- Kingfa Sci & Tech Co Ltd

- BioBag International AS

- Yibiyuan Water-Saving Equipment Technology Co., Ltd.

- Polystar Plastics Ltd

- Armando Alvarez

- Novamont S.p.A.

- Berry Global Inc.

- Napco National

- Tilak Polypack

- Intergro, Inc.

- Shalimar Group

- Solplast

- GEROVIT

- Plastitech

Frequently Asked Questions

The global mulch film market is projected to be valued at US$ 6.8 Bn in 2026.

The conventional segment is expected to account for approximately 68% of the Global Mulch Film Market by Product Type in 2026.

The mulch film market is expected to witness a CAGR of 6.8% from 2026 to 2033.

Global Mulch Film Market growth is driven by the global food security imperative and agricultural intensification, regulatory pressure against conventional plastics, and technological advancements in biodegradable and functional film materials.

Key market opportunities in the global Mulch Film Market include government-led biodegradable agriculture programs and regulatory certifications, nutrient-enhanced and multifunctional film innovations, and the expansion of the food processing sector, driving demand for high-quality horticultural produce.

Key players in the Mulch Film Market include BASF SE, Berry Global Inc., The Dow Chemical Company,RKW Group, Novamont S.p.A., and Armando Alvarez Group.