- Medical Devices

- Microsurgery Robot Market

Microsurgery Robot Market Size, Share, Trends, Growth, and Regional Forecast, 2026 to 2033

Microsurgery Robot Market by Product (Robotic Systems, Instruments & Accessories, and Software & Services), Application (Urology, Otology, Ophthalmology, Neurosurgery, and Others) End-user (Hospitals, Specialty Clinics, and Ambulatory Surgery Centers), and Regional Analysis from 2026 to 2033

Microsurgery Robot Market Share and Trends Analysis

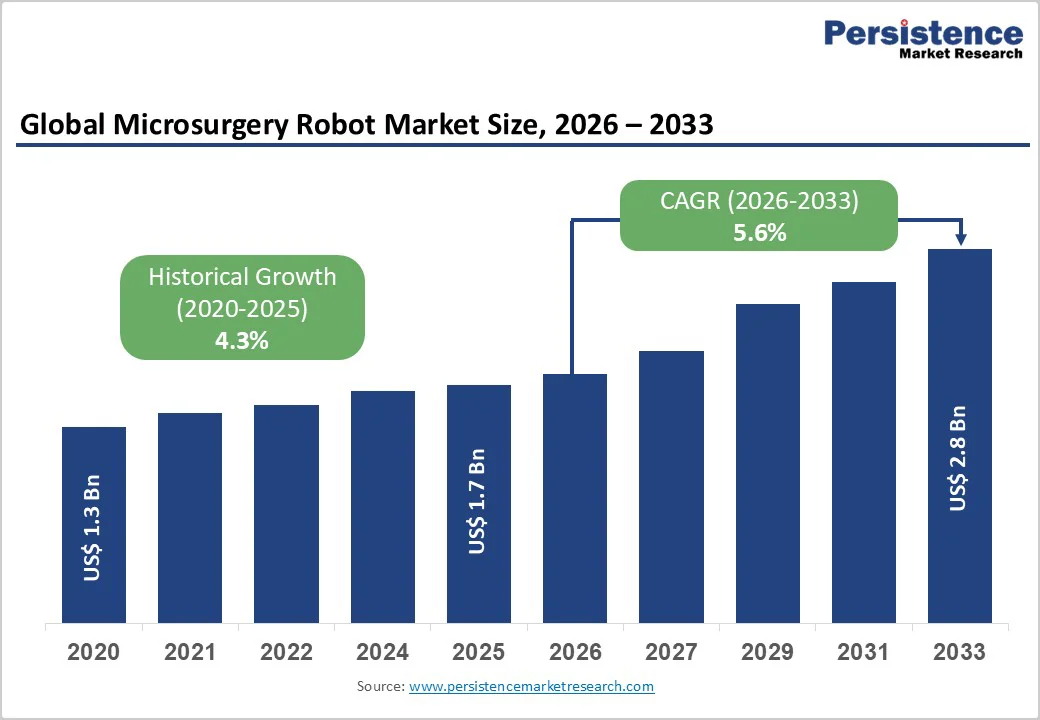

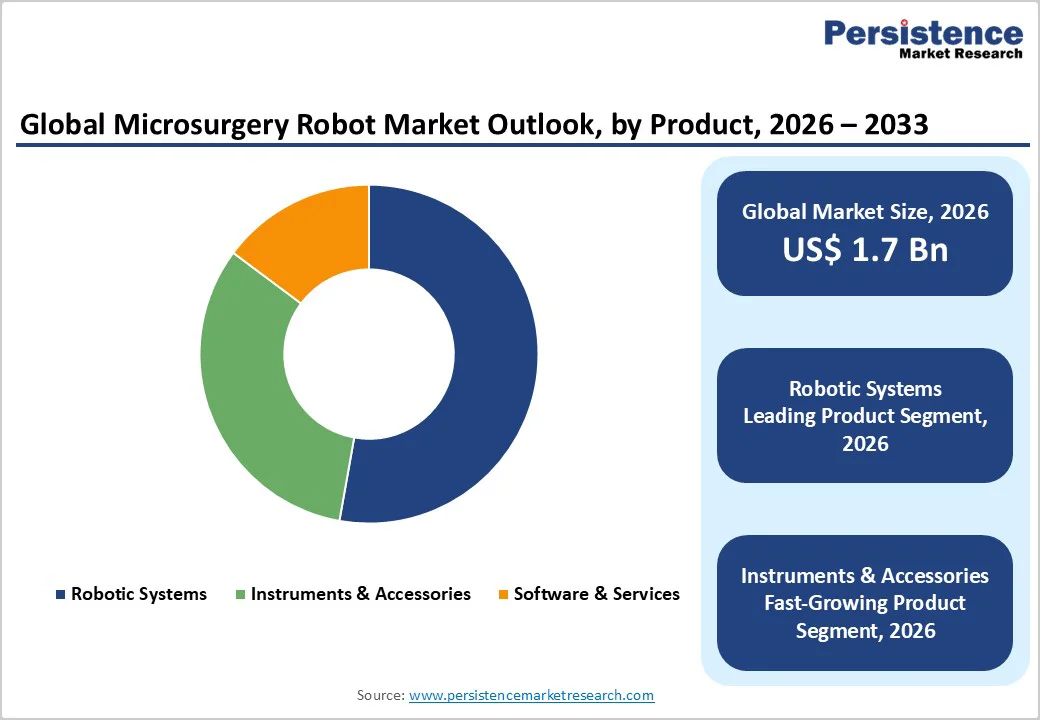

The global microsurgery robot market size is estimated to grow from US$ 1.7 billion in 2026 and projected to reach US$ 2.8 billion by 2033 growing at a CAGR of 5.6% during the forecast period from 2026 to 2033.

Global demand for microsurgery robots is rising rapidly, driven by the growing preference for minimally invasive, high-precision surgical procedures, increasing awareness of improved patient outcomes, and expanding adoption of robotic platforms across neurosurgery, ophthalmology, ENT, and microvascular reconstruction.

Hospitals and specialty centers are increasingly integrating microsurgical robots to achieve enhanced dexterity, tremor elimination, and superior maneuverability in delicate anatomical environments. Rising investments in tertiary-care infrastructure, expansion of surgeon training programs, and proliferation of robotics centers of excellence are accelerating adoption worldwide.

Key Industry Highlights

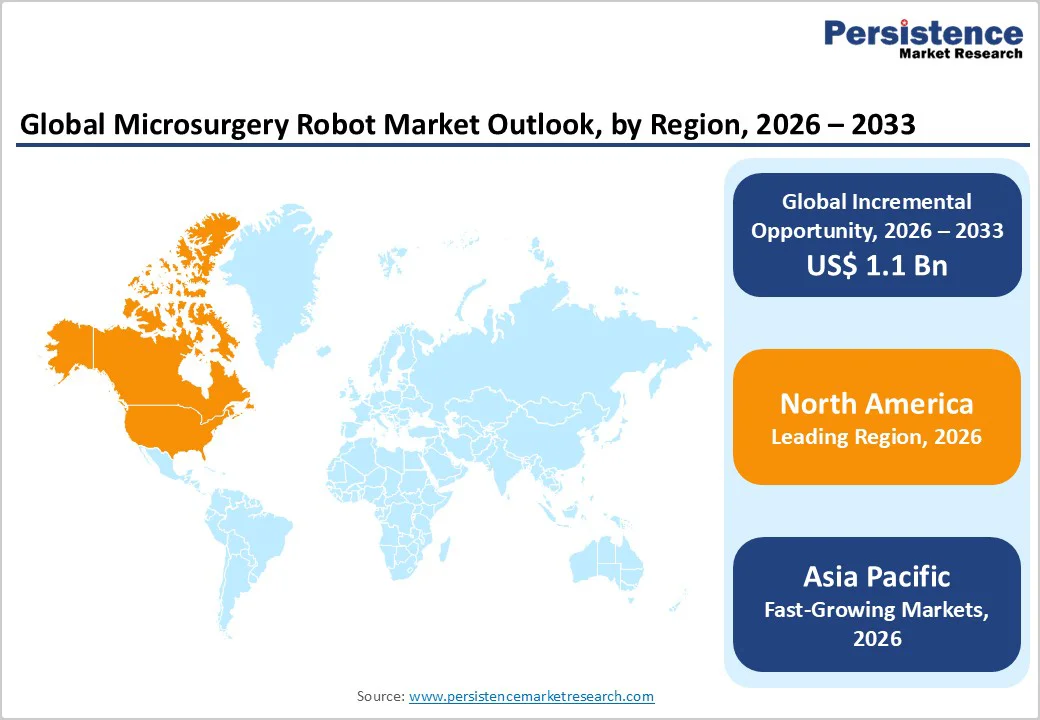

- Leading Region: North America holds the largest share at 47.3%, supported by advanced surgical infrastructure, strong clinical adoption of robotic microsurgery, high healthcare expenditure, and early access to FDA-cleared robotic systems.

- Fastest-Growing Region: Asia Pacific is expanding the fastest due to a large surgical patient pool, rapid modernization of hospitals, increasing medical tourism, and growing investments in robotic-assisted specialty surgery.

- Leading Product Segment: Robotic systems dominate the market due to their extensive use in neurosurgery, ophthalmology, and microvascular reconstruction, offering unmatched precision and improved surgical ergonomics.

- Fastest-Growing Product Segment: Instruments & accessories grow rapidly as recurring demand rises with increasing procedure volumes, frequent component replacement, and broader clinical utilization of microsurgical robots.

- Leading Application Segment: Neurosurgery remains the top application, driven by high adoption of robots for tumor resection, micro-dissection, aneurysm repair, and skull-base procedures requiring extreme precision.

- Fastest-Growing Application Segment: Ophthalmology is scaling quickly as robotic-assisted retinal and corneal microsurgeries gain traction, offering enhanced accuracy, reduced tremor, and better visual outcomes for delicate ocular procedures.

| Key Insights | Details |

|---|---|

| Microsurgery Robot Market Size (2026E) | US$ 1.7 Bn |

| Market Value Forecast (2033F) | US$ 2.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

Market Dynamics

Driver - Rising Burden of Complex Diseases and Advancements in Surgical Precision Technologies

The growing global incidence of chronic and degenerative disorders such as neurological diseases, vascular abnormalities, diabetic retinopathy, and various cancers continues to elevate the need for highly precise microsurgical interventions.

For instance, according to the American Academy of Neurology, the global burden of brain disorders is projected to reach 4.9 billion cases by 2050, highlighting the growing need for advanced neurosurgical solutions such as microsurgery robots to improve precision and patient outcomes As disease complexity increases, traditional manual techniques often fall short in delivering the accuracy and consistency required for delicate structures like microvascular networks, retinal tissues, and peripheral nerves.

This has accelerated the adoption of microsurgery robots in hospitals and specialty centers seeking to minimize surgical errors, reduce complication rates, shorten recovery times, and improve long-term patient outcomes. Health systems are also investing heavily in robotics to handle the rising caseload of minimally invasive procedures while optimizing surgeon performance and reducing fatigue.

The technological advancements in imaging, AI, and haptic-control technologies are driving the growth of microsurgical robotics. High-resolution 3D visualisation, enhanced depth perception, and digital magnification allow surgeons to operate confidently within micrometer-scale anatomical spaces.

AI-assisted movement guidance aids in trajectory planning and stabilizes micro-instrument actions, while robotic tremor filtration eliminates human hand instability. Additionally, next-generation force-feedback haptics simulate tactile sensation, improving safety during tissue manipulation.

These integrated innovations significantly expand procedural capabilities across neurosurgery, ophthalmology, reconstructive surgery, and supermicrosurgery, positioning robotics as a core technology for the next era of precision medicine.

Restraints - High Costs and Integration Challenges Limiting Adoption

Microsurgical robotic platforms require significant capital investment, involving high-priced hardware, precision-engineered optics, and sophisticated control consoles. In addition to the upfront acquisition cost, ongoing expenses for software upgrades, instrument replacements, maintenance contracts, and training programs further increase the total cost of ownership.

For mid-sized hospitals and specialty clinics with limited budgets, these financial barriers can be prohibitive, delaying adoption despite the clear clinical benefits of robotic assistance. Smaller facilities may also struggle to justify the return on investment due to lower surgical volumes, making the cost-to-benefit ratio less attractive compared to larger tertiary-care centers or academic institutions.

This financial burden can slow the penetration of advanced microsurgical robotics in emerging markets and non-urban regions, where capital constraints and resource limitations are more pronounced.

Moreover, integration challenges pose additional hurdles for new adopters. Microsurgery robots must be compatible with existing imaging systems, intraoperative navigation tools, and surgical microscopes. Operating room layouts often require modification to accommodate the robotic arms, consoles, and supporting hardware, while sterilization protocols must be adapted for delicate robotic instruments.

These operational complexities demand careful planning, technical expertise, and collaboration between hospital administrators, surgical teams, and device manufacturers. Failure to address integration effectively can result in workflow inefficiencies, underutilization of expensive systems, and delays in achieving optimal clinical outcomes.

Opportunity - AI-Integrated Autonomous Assistance Systems & Strategic Partnerships

AI-driven motion guidance, automated suturing algorithms, and real-time tissue recognition are redefining the capabilities of next-generation microsurgery platforms. These intelligent systems enable unprecedented precision, reduced procedure times, and enhanced safety, especially in delicate interventions.

Expansion into ophthalmic and supermicrosurgery applications such as retinal vein cannulation, nerve repair, and lymphatic reconstruction presents high-value commercialization opportunities. By integrating machine learning and predictive analytics, these platforms can assist surgeons in navigating complex anatomical structures, minimizing human error, and improving patient outcomes, making them a critical driver of growth in the microsurgery robot market.

Strategic collaborations between hospitals, startups, and device manufacturers further accelerate innovation and adoption. Joint R&D initiatives focused on specialized micro-tools, modular robotic arms, and surgeon-friendly consoles enhance the functionality and usability of these systems.

Partnerships also facilitate clinical validation, regulatory approvals, and faster market penetration. By combining cutting-edge AI capabilities with collaborative development, stakeholders can create versatile, scalable solutions that address the rising global demand for minimally invasive and precision microsurgical procedures, ultimately driving both clinical impact and commercial success.

Category-wise Analysis

By Product Insights

The robotic systems segment is projected to dominate the global microsurgery robot market in 2026, accounting for a significant revenue share of 52.8%. This dominance is driven by the growing adoption of microsurgical robotic platforms capable of providing motion scaling, tremor elimination, enhanced dexterity, and superior visualization during complex procedures.

Surgeons increasingly prefer robotic systems for delicate interventions in neurosurgery, ophthalmology, ENT, and microvascular reconstruction due to their ability to perform precise suturing, micro-anastomosis, and tissue manipulation with minimal trauma. Rising demand for minimally invasive workflows, reduced complication rates, and improved functional outcomes further supports adoption.

In addition, ongoing innovations such as miniaturized robotic arms, microscope-integrated systems, and AI-enabled control software-combined with expanding hands-on training and simulation programs-are accelerating global deployment of advanced microsurgical robotic platforms.

By Application Insights

The neurosurgery segment is expected to dominate the global microsurgery robot market in 2026 with a revenue share of 30.7%. Neurosurgeons are increasingly adopting robotic platforms to enhance precision in tumor resections, micro-dissections, aneurysm clipping, and skull-base procedures where millimeter-level accuracy is critical.

Robotic systems offer controlled instrument articulation, steadier micro-movements, and improved navigation in confined anatomical spaces, significantly improving surgical safety and patient outcomes. Rising prevalence of neurodegenerative conditions, increasing number of complex cranial and spinal procedures, and growing preference for minimally invasive neurosurgical approaches are fueling market leadership.

Adoption is further supported by integration of robotics with surgical microscopes, neuronavigation systems, and intraoperative imaging modalities, enabling more predictable results and reducing surgeon fatigue during lengthy procedures.

By End-user Insights

The hospitals segment is projected to dominate the global microsurgery robot market in 2026, capturing a revenue share of 54.6%. Hospitals particularly tertiary-care centers and academic institutions are the primary adopters of microsurgical robotics due to their ability to invest in high-cost technologies, manage complex case loads, and support multidisciplinary surgical teams.

Increasing utilization of robotics across neurosurgery, ophthalmology, ENT, and reconstructive surgery is strengthening hospital-based demand. High patient footfall, access to skilled surgeons, and availability of robust imaging and navigation systems further enable seamless integration of microsurgical robots into operating rooms.

Moreover, hospitals benefit from structured training programs, research collaborations, and participation in clinical trials that drive early adoption. Growing focus on improving precision, reducing surgical complications, and enhancing patient recovery timelines continues to position hospitals as the leading end-user segment globally.

Region-wise Insights

North America Microsurgery Robot Market Trends

North America is expected to maintain global dominance in the microsurgery robot market with market share value of 47.3%, supported by its advanced healthcare infrastructure, strong innovation ecosystem, and high adoption of precision-driven surgical technologies. The U.S. leads the region due to frequent FDA approvals, strong presence of robotic-surgery pioneers, and extensive collaborations between hospitals, universities, and device manufacturers.

Major academic medical centers actively pilot microsurgical robotic platforms for neurosurgery, ophthalmology, and reconstructive procedures, further accelerating commercialization. Rising demand for improved surgical accuracy, reduced tremors, and faster postoperative recovery continues to drive capital investments by large hospital networks.

The region also benefits from strong reimbursement pathways for complex microsurgical interventions and increasing surgeon preference for robot-assisted visualization and dexterity. Growing investments in OR integration, digital surgery platforms, simulation-based training, and AI-powered guidance systems are expanding clinical applications.

Additionally, rising patient awareness of minimally invasive alternatives and the growing number of centers of excellence in robotic microsurgery strengthen North America’s long-term leadership in the global market.

Europe Microsurgery Robot Market Trends

The Europe shows steady and mature adoption of microsurgery robotic platforms, supported by strong clinical research, well-established hospital networks, and a high focus on minimally invasive surgical standards. Countries such as Germany, the U.K., France, Italy, Switzerland, and the Nordic region lead deployment, backed by early clinical validation studies and structured surgeon training pathways.

The region is characterized by active integration of robotic systems into ophthalmic microsurgery, microvascular reconstruction, ENT, and neurosurgical workflows, driven by the need for enhanced dexterity and improved patient outcomes.

Europe’s favorable regulatory environment, emphasis on clinical safety, and wide involvement of research universities create a supportive landscape for evaluating and adopting next-generation systems. Growing demand for advanced imaging-guided interventions, microscope-integrated robotics, and AI-assisted precision tools further strengthens adoption.

Regional manufacturers continue to innovate in micro-actuation, force-feedback capabilities, and miniaturized robotic arms. Government initiatives supporting digital transformation, combined with rising geriatric populations requiring delicate surgical care, continue to boost Europe’s overall market growth.

Asia Pacific Microsurgery Robot Market Trends

Asia Pacific is projected to be the fastest-growing region for microsurgery robots with a CAGR of 7.6%, driven by rising healthcare expenditure, strong medical tourism, and rapid modernization of surgical infrastructure. Countries such as China, Japan, South Korea, Singapore, and India are expanding robotic-assisted programs across neurosurgery, ophthalmology, ENT, and reconstructive specialties.

Increasing availability of cost-effective robotic platforms, combined with the entry of regional manufacturers, is improving affordability and widening access for mid-sized hospitals and specialty clinics. Government-supported digital health initiatives, rising investments in tertiary-care facilities, and partnerships with global OEMs for training and technology transfer are boosting adoption.

Growing demand for precise, minimally invasive procedures especially for retinal, auditory, and microvascular conditions is fueling clinical uptake.

Surgeons across Asia Pacific are increasingly participating in international fellowships and adopting robotic systems to enhance surgical accuracy, reduce fatigue, and improve patient recovery times. Strengthening private healthcare networks, rising medical tourism for complex microsurgeries, and expanding robotics centers of excellence continue to drive robust market growth across the region.

Competitive Landscape

The global microsurgery robot market is highly competitive, with strong participation from companies such as Medtronic, meerecompany Inc., Microsure, Siemens Healthineers, Smith + Nephew, and Stryker. These players leverage advanced robotic microsurgical platforms, high-precision motion-scaling technologies, and extensive hospital partnerships to strengthen their global presence.

Rising demand for tremor-elimination systems, enhanced microvascular precision, and minimally invasive procedures is accelerating deployment across neurosurgery, ophthalmology, ENT, and reconstructive surgery centers.

Manufacturers are increasingly focusing on AI-enabled motion control, augmented-reality-assisted visualization, and miniaturized multi-arm platforms tailored for delicate tissue manipulation.

Strategic priorities include expanding application portfolios, improving real-time force-feedback and safety systems, strengthening surgeon training and simulation programs, and forming collaborations with clinical research institutes to validate new indications and support long-term market growth.

Key Industry Developments:

- In December 2025, Medtronic announced that the U.S. Food and Drug Administration (FDA) cleared the Hugo™ robotic-assisted surgery (RAS) system for urologic procedures. This clearance introduces a versatile robotic platform to U.S. surgeons and health systems, enabling the expansion of soft-tissue robotic surgery programs and broader access to minimally invasive care.

- In October 2025, MMI, a robotics company focused on advancing treatment options and enhancing outcomes for patients with complex conditions, announced the successful completion of the first neurosurgical cases in a clinical trial of the Symani® Surgical System, sponsored by the Jacobs Institute.

- In October 2025, Johnson & Johnson MedTech announced advancements in its robotic systems through physical artificial intelligence (AI) technologies, which create simulated environments to accelerate product innovation, optimize clinical workflows, and enhance training for clinical teams.

- In May 2024, Sony Group Corporation announced the development of a microsurgery assistance robot featuring automatic surgical instrument exchange and precision control. The prototype is scheduled for unveiling at Sony’s booth during the 2024 IEEE International Conference on Robotics and Automation (ICRA 2024) in Yokohama,

Companies Covered in Microsurgery Robot Market

- Medtronic

- meerecompany Inc.

- Microsure

- Siemens Healthineers

- Smith + Nephew

- Stryker

- Zimmer Biomet

- Asensus Surgical US, Inc.

- avateramedical GmbH

- CMR Surgical Ltd.

- Distalmotion SA

- Intuitive Surgical Operations, Inc.

- Johnson & Johnson

- Medical Microinstruments, Inc.

- Others

Frequently Asked Questions

The global microsurgery robot market is projected at US$ 1.7 billion in 2026.

Rising demand for high-precision minimally invasive procedures, increasing burden of complex neurosurgical and ophthalmic conditions, and rapid advances in robotic dexterity, imaging, and tele-operation technologies are driving the global microsurgery robot market.

The global microsurgery robot market is poised to witness a CAGR of 5.6% between 2026 and 2033.

Expansion into ophthalmology and microvascular reconstruction, development of compact cost-efficient robotic platforms, and growing adoption in specialty clinics and emerging markets are creating opportunities in the market.

Medtronic, meerecompany Inc., Microsure, Siemens Healthineers, Smith + Nephew, and Stryker are some of the key players in the microsurgery robot market.