- Industrial Goods & Service

- Machine Safety Market

Machine Safety Market Size, Share, and Growth Forecast 2026 - 2033

Machine Safety Market by Component (Presence Sensing Safety Sensors, Safety Interlock Switches, Safety Controllers/Modules/Relays, Programmable Safety Applications, Emergency Stop Controls, Two-Hand Safety Controls), Implementation Type (Individual Components, Embedded Components), by Application, End-user, Regional Analysis, 2026 - 2033

Machine Safety Market Size and Trend Analysis

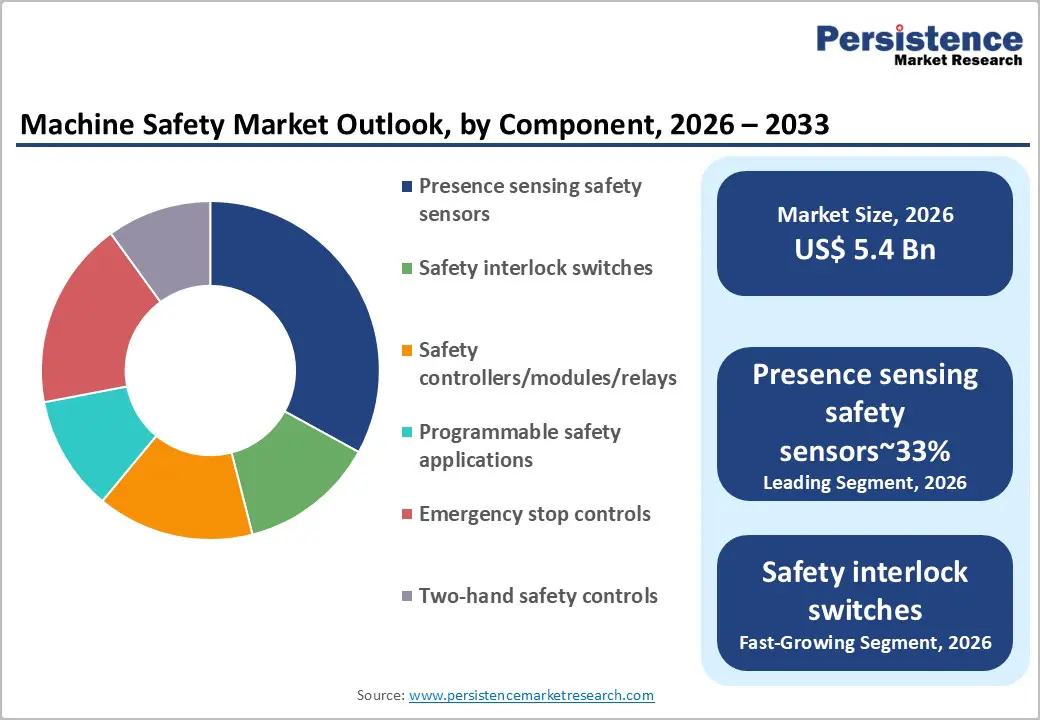

The global machine safety market size is likely to be valued at US$ 5.4 Billion in 2026 and is expected to reach US$ 8.0 Billion by 2033, growing at a CAGR of 5.7% during the forecast period from 2026 to 2033.

This sustained growth trajectory is principally driven by the simultaneous acceleration of industrial automation, stringent mandatory compliance with workplace safety standards such as ISO 13849 and IEC 62061, and a sharp global increase in human-robot collaboration deployments across automotive, semiconductor, and food processing industries.

Key Market Highlights

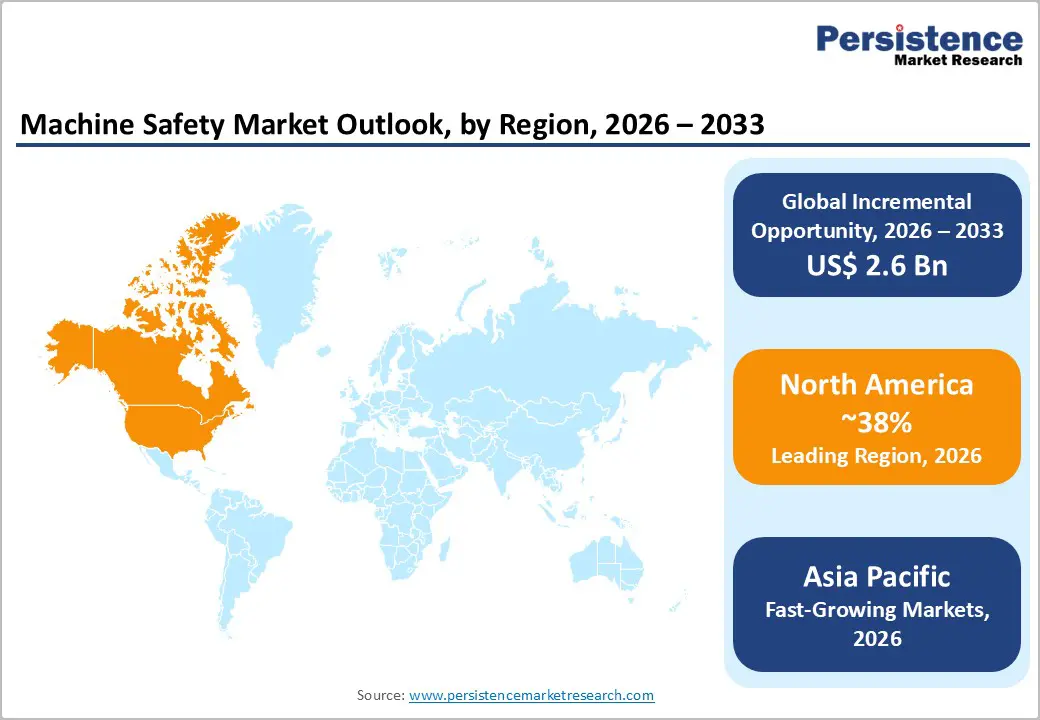

- Leading Region: North America leads the global Machine Safety Market holding 38% share, driven by OSHA's mandatory machine guarding standards, a large industrial automation base recording over 220,000 manufacturing injuries annually per BLS data, and a strong innovation ecosystem anchored by Rockwell Automation and Honeywell International.

- Fastest-Growing Region: Asia Pacific is the fastest-growing regional market with rising CAGR of 6.9%, propelled by China's annual industrial robot installations exceeding 270,000 units per IFR, India's PLI-driven manufacturing expansion, and tightening GB-standard safety compliance mandates across the region's vast electronics and automotive manufacturing base.

- Leading Segment: Presence sensing safety sensors dominate the component segment with approximately 33% market share, underpinned by mandatory Performance Level (PL)-rated detection requirements under ISO 13849-1:2023 for robotic cells, automated assembly lines, and collaborative robot deployments globally.

- Fastest-Growing Segment: The Robotics application segment is the fastest-growing category, accelerated by the IFR-reported global robot stock exceeding 3.9 million operational units and stringent ISO 10218-1 and ISO/TS 15066 compliance requirements for safety system integration in human-robot collaborative environments.

- Key Opportunity: The most significant market opportunity lies in IIoT-connected Safety-as-a-Service platforms, enabling real-time remote safety monitoring and predictive maintenance for industrial machinery, with semiconductor fabs funded by the US$ 52 Billion CHIPS and Science Act representing a premium, high-specification demand frontier.

| Key Insights | Details |

|---|---|

| Machine Safety Market Size (2026E) | US$ 5.4 Billion |

| Market Value Forecast (2033F) | US$ 8.0 Billion |

| Projected Growth CAGR (2026 - 2033) | 5.7% |

| Historical Market Growth (2020 - 2025) | 4.6% |

Market Dynamics

Drivers - Growing Workplace Safety Regulations and Compliance Mandates

The growing enforcement of workplace safety regulations across major industrial economies is driving strong adoption of certified machine safety solutions. Regulatory authorities worldwide are implementing strict standards that require manufacturers and plant operators to integrate advanced safety systems into industrial machinery. In the United States, the Occupational Safety and Health Administration (OSHA) enforces machine guarding standards under 29 CFR 1910.212, ensuring that workplaces follow strict safety practices to protect workers from hazardous equipment.

The European Union Machinery Directive (2006/42/EC) is transitioning toward the updated EU Machinery Regulation (EU) 2023/1230, which will come into full effect in January 2027 and requires comprehensive functional safety assessments for machinery sold within the region. Additionally, the international safety standard ISO 13849-1:2023, maintained by ISO/TC 199, is used by more than 89% of machine builders as their primary framework for designing functional safety systems. Failure to comply with these regulations can result in legal penalties, operational disruptions, and reputational damage. As a result, manufacturers are increasingly investing in safety sensors, emergency stop systems, safety controllers, and programmable safety technologies across various manufacturing industries.

Rapid Adoption of Industrial Automation and Collaborative Robotics

The rapid expansion of industrial automation worldwide is significantly increasing the demand for advanced machine safety systems. As industries adopt automated production processes and robotics to improve efficiency and productivity, the need for reliable safety mechanisms becomes critical. Collaborative robots, or cobots, are particularly driving this demand because they are designed to operate in close proximity to human workers. Unlike traditional robots that operate behind protective barriers, cobots require advanced safety systems such as presence-sensing sensors, safety scanners, and force-limiting devices to ensure safe interaction between humans and machines.

According to the International Federation of Robotics (IFR), global industrial robot installations reached a record 553,052 units in 2023, with collaborative robot applications accounting for a growing share of deployments. Compliance with IEC 62061:2021, which defines functional safety requirements for safety-related control systems, is mandatory for cobot integrators. As industries such as automotive, electronics, and logistics continue to accelerate automation investments, the demand for reliable machine safety solutions is expected to grow steadily through 2033.

Restraints - High Initial Investment and Integration Complexity

One of the major challenges limiting wider adoption of machine safety systems is the high upfront investment required to implement certified safety solutions. Many manufacturers, particularly small and medium-sized enterprises, find it difficult to allocate the significant capital needed to install advanced safety technologies. Establishing a fully compliant machine safety framework typically involves deploying Safety Integrity Level (SIL)-rated controllers, redundant sensors, emergency stop devices, and programmable safety applications, all of which contribute to higher initial costs.

In addition to financial constraints, system integration can be complex, particularly in older industrial facilities where legacy machinery was not originally designed to meet modern safety standards. Retrofitting these machines to comply with updated regulations such as ISO 13849-1:2023 and IEC 62061:2021 often requires extensive engineering work, additional components, and specialized expertise. These technical challenges can delay safety implementation projects and increase operational costs. As a result, some manufacturers postpone upgrades despite regulatory pressure, which slows the overall pace of machine safety adoption across certain industrial sectors.

Shortage of Qualified Functional Safety Engineers

Another significant factor restricting the growth of the machine safety market is the global shortage of skilled functional safety engineers. Designing, implementing, and maintaining compliant safety systems requires highly specialized technical expertise in areas such as hazard analysis, risk assessment, performance level calculation, and safety lifecycle management. Engineers must also be familiar with complex international safety standards including IEC 61508, ISO 13849, and IEC 62061.

The number of professionals with certified expertise in these areas remains limited. Certification bodies such as TÜV Rheinland and TÜV SÜD have reported that the demand for Functional Safety Engineer (FSE) qualifications continues to exceed the rate at which trained professionals enter the workforce. This talent gap increases project timelines and raises consulting and engineering costs for companies attempting to deploy safety solutions. Additionally, the shortage of experienced professionals can slow the validation and approval processes required to ensure compliance. As industries continue to automate operations, the limited availability of skilled safety engineers may become a growing constraint on market expansion.

Opportunities - Expansion of Safety-as-a-Service and IIoT-Connected Safety Platforms

The evolution of machine safety systems toward cloud-connected platforms and service-based business models is creating significant growth opportunities for industry participants. With the advancement of Industrial Internet of Things (IIoT) technologies, manufacturers can now connect safety devices to centralized monitoring systems that enable real-time tracking of machine health and safety performance. These platforms allow operators to receive predictive maintenance alerts, monitor device diagnostics remotely, and perform automatic firmware updates for safety controllers and sensors.

The companies are gradually shifting from traditional one-time equipment sales to recurring service-based revenue models known as Safety-as-a-Service. Leading industrial automation providers such as Pilz GmbH and Rockwell Automation have introduced cloud-enabled safety diagnostic platforms that integrate with OPC UA communication protocols, enabling continuous compliance monitoring. This approach helps organizations maintain safety standards while reducing long-term maintenance costs. As Industry 4.0 adoption accelerates across automotive, semiconductor, and food processing industries, connected safety platforms are expected to grow faster than conventional hardware solutions, offering high-margin revenue opportunities for technology providers.

Growing Safety Requirements in Semiconductor and Electronics Manufacturing

The rapid expansion of global semiconductor manufacturing is creating strong demand for advanced machine safety technologies. Governments around the world are investing heavily in domestic semiconductor production through large-scale policy initiatives and financial incentives. In the United States, the CHIPS and Science Act of 2022 allocated more than US$52 billion to strengthen domestic semiconductor manufacturing capacity. Similarly, the European Union’s Chips Act aims to double Europe’s share of global semiconductor production to 20%.

Semiconductor fabrication facilities use highly sophisticated equipment such as extreme ultraviolet lithography machines, robotic wafer handling systems, and high-voltage processing tools. These technologies require advanced safety architectures that meet SIL 2 and SIL 3 functional safety requirements defined by IEC 62061. In addition, semiconductor manufacturing environments demand cleanroom-compatible and highly precise safety components. This creates opportunities for suppliers capable of providing miniaturized safety sensors, advanced programmable safety controllers, and integrated safety validation services tailored specifically for high-precision semiconductor production environments.

Category-wise Analysis

Component Insights

Presence-sensing safety sensors represent the largest component segment within the Machine Safety Market, accounting for approximately 33% of total market revenue. These sensors include technologies such as safety light curtains, laser scanners, safety mats, and proximity detection sensors that act as the primary detection layer within a machine safety architecture. Their main function is to monitor hazardous machine zones and detect human presence in order to prevent potential accidents. According to ISO 13849-1:2023 standards, safety sensors must meet specific Performance Level (PL) ratings, with PL d and PL e devices commonly required for most industrial safety applications.

The growing deployment of collaborative robots and automated guided vehicles in industries such as automotive manufacturing, electronics production, and logistics operations is significantly increasing demand for advanced presence-sensing technologies. These systems help ensure safe interaction between workers and automated machinery. Leading technology providers including KEYENCE Corporation, SICK AG, and Omron Corporation continue to invest in innovations such as faster response times, compact sensor designs, and IIoT connectivity, strengthening the dominant position of this segment.

Implementation Type Insights

The individual components segment dominates the implementation type category in the machine safety market, accounting for nearly 65% of total market revenue. Individual safety components include standalone devices such as safety sensors, emergency stop switches, safety relays, and interlock switches that can be installed separately within industrial systems. Manufacturers prefer these modular solutions because they offer flexibility, lower installation costs, and easier integration into existing machinery. In many industrial facilities, especially those operating older equipment, replacing entire safety systems can be expensive and disruptive.

Individual components allow companies to upgrade specific safety elements without redesigning the entire machine architecture. This modular approach also helps organizations meet evolving safety regulations such as ISO 13849 and IEC 62061 through incremental improvements. The large global installed base of conventional machinery across industries such as automotive manufacturing, metal processing, and packaging continues to support demand for discrete safety devices. Additionally, validating performance levels for individual safety components is generally simpler compared to complex embedded safety systems.

Application Insights

The robotics application segment holds the largest share within the machine safety market, accounting for approximately 28% of total application revenue. Robotic systems require comprehensive safety architectures because they operate in close proximity to workers and involve high-speed mechanical movements. Industrial robotic cells typically integrate multiple layers of safety technology including safety scanners, light curtains, access door interlocks, programmable safety controllers, and torque monitoring systems. These solutions ensure compliance with international safety standards such as ISO 10218-1, which defines safety requirements for industrial robots, and ISO/TS 15066, which focuses specifically on collaborative robot safety.

According to the International Federation of Robotics, the global operational stock of industrial robots exceeded 3.9 million units by the end of 2022, and installations continue to increase across various industries. Each robotic installation requires dedicated safety infrastructure to protect workers and maintain regulatory compliance. Industries such as automotive manufacturing, electronics production, and semiconductor fabrication, where robot density is highest, remain the primary drivers of demand for robotics safety solutions.

End-user Insights

The automotive sector represents the largest end-use segment in the Machine Safety Market, accounting for approximately 26% of total industry demand. Automotive manufacturing facilities are among the most automated industrial environments in the world, incorporating thousands of robotic systems for welding, assembly, painting, and material handling operations. These highly automated production lines require advanced machine safety architectures to protect workers and maintain operational reliability.

The transition toward electric vehicle manufacturing has further increased safety requirements across automotive plants. EV battery production involves high-voltage equipment, specialized robotic systems, and precision assembly machinery that require advanced safety controllers and monitoring systems compliant with SIL 2 standards defined by IEC 62061. Major automotive manufacturers including Volkswagen Group, Toyota Motor Corporation, and General Motors implement strict internal safety frameworks that often exceed regulatory requirements. As electric vehicle production continues to expand globally, with the International Energy Agency projecting EV sales to exceed 20 million units annually by 2030, automotive facilities will remain a key driver of machine safety investments.

Regional Insights

North America Machine Safety Market Trends

The United States remains the foundation of the North American machine safety market, supported by a well-established regulatory framework enforced by Occupational Safety and Health Administration (OSHA). Mandatory machine guarding standards under OSHA regulations 29 CFR 1910.217 and 29 CFR 1910.212, along with a strong base of industrial automation in automotive, aerospace, and food processing industries, continue to drive steady demand for machine safety solutions. According to the U.S. Bureau of Labor Statistics (BLS), the manufacturing sector reported nearly 220,000 workplace injuries in 2024, reinforcing the need for certified safety systems across industrial facilities.

The National Institute for Occupational Safety and Health (NIOSH) and OSHA also promote best-practice guidelines for robotic safety, encouraging organizations to adopt advanced safety systems. Canada is steadily increasing machine safety investments, especially within its automotive supply chains concentrated in Ontario. The expanding semiconductor manufacturing ecosystem supported by the CHIPS and Science Act in the United States is also creating strong demand for high-specification safety systems in new fabrication plants. In addition, innovation leadership from companies such as Rockwell Automation and Honeywell International strengthens the regional ecosystem for safety integration, software development, and regulatory standard participation.

Europe Machine Safety Market Trends

Europe operates within one of the world’s most stringent regulatory environments for machine safety, supported by the EU Machinery Regulation (EU) 2023/1230, which will fully replace the Machinery Directive 2006/42/EC by January 2027. Germany, as the region’s leading manufacturing hub, represents the largest consumer of machine safety technologies. Its globally recognized automotive industry, driven by companies such as Volkswagen, BMW, and Mercedes-Benz, continues to invest heavily in advanced safety controllers and sensor systems compliant with DIN EN ISO 13849 standards. At the same time, France and Spain are accelerating their smart factory transformation through national Industry 4.0 initiatives, which is increasing the deployment of integrated safety solutions across manufacturing facilities.

The United Kingdom, despite its exit from the European Union, continues to maintain regulatory alignment with EN ISO 13849 and BS EN IEC 62061 standards through domestic adoption. Furthermore, the European Agency for Safety and Health at Work (EU-OSHA) regularly issues workplace safety directives that require industries to conduct periodic machine safety reassessments. Harmonized safety regulations across the European Economic Area also simplify cross-border trade for safety solution providers while enabling large-scale deployment of standardized safety components.

Asia Pacific Machine Safety Market Trends

The Asia Pacific region represents the fastest-growing market for machine safety worldwide, supported by rapid industrial automation expansion in China, advanced robotics development in Japan, and manufacturing modernization initiatives in India. China continues to dominate global industrial robot adoption, with annual installations exceeding 270,000 units according to the International Federation of Robotics. The country is also strengthening workplace safety regulations through updated GB national standards aligned with ISO 13849, encouraging the adoption of certified safety components across its vast manufacturing ecosystem.

Japan maintains a strong leadership position in safety technology manufacturing, with globally recognized companies such as KEYENCE Corporation, Omron Corporation, and IDEC Corporation producing advanced safety systems while also supporting high domestic demand from automotive, electronics, and precision machinery sectors. Meanwhile, India’s industrial safety landscape is evolving through regulatory frameworks such as the Factories Act and growing industrial robot adoption under the Production-Linked Incentive Scheme (PLI). In addition, rapidly expanding manufacturing bases in Vietnam, Thailand, and Malaysia are creating strong growth opportunities for machine safety suppliers seeking regional expansion through 2033.

Competitive Landscape

The global Machine Safety Market demonstrates a moderately consolidated competitive structure, where a limited number of multinational industrial automation companies hold a significant share of overall revenue. Major industry leaders include Siemens, Rockwell Automation, ABB, Schneider Electric, and Omron Corporation, all of which maintain strong global positions through extensive product portfolios and integrated automation capabilities. These companies offer comprehensive machine safety solutions covering controllers, sensors, emergency systems, and safety software, allowing them to provide end-to-end safety integration for industrial environments.

Their competitive advantage is further strengthened through internationally recognized functional safety certifications such as TÜV, CE, and UL. To expand their market presence, leading companies are focusing on strategies such as cross-selling safety products within existing automation platforms, acquiring specialized safety technology firms, and investing in advanced digital safety platforms. Emerging business models are also gaining traction, including subscription-based safety services, remote compliance validation, and AI-enabled risk assessment tools, which allow vendors to strengthen long-term customer relationships beyond traditional hardware sales.

Key Developments:

- In January 2025: Rockwell Automation expanded its GuardLogix 5580 safety controller portfolio, improving EtherNet/IP connectivity and safety response performance for modern automation environments. The controllers support integrated safety and standard control within a single platform, helping manufacturers simplify machine architecture while ensuring compliance with functional safety standards.

- In March 2024: Siemens launched the SIRIUS 3SK2 modular safety relay series designed to support smart factory environments. The system includes embedded diagnostics and IO-Link connectivity, allowing real-time monitoring of safety devices, improving predictive maintenance capabilities, and helping manufacturers align safety infrastructure with evolving Industry 4.0 production systems.

- In September 2023: SICK AG expanded its microScan3 safety laser scanner family with new outdoor-capable variants for automated guided vehicles and autonomous mobile robots. These scanners enhance navigation safety and obstacle detection in logistics environments, supporting the rapid growth of warehouse automation and autonomous material-handling systems.

Companies Covered in Machine Safety Market

- Schneider Electric

- Rockwell Automation

- Siemens

- KEYENCE CORPORATION

- Emerson Electric Co.

- Omron Corporation

- SICK AG

- ABB

- Honeywell International

- IDEC Corporation

- ISE Controls

- Mitsubishi Electric

- OmniSource Corporation

- Pilz GmbH & Co. KG

- Banner Engineering Corp.

- Schmersal Group

- HIMA Paul Hildebrandt GmbH

- Fortress Interlocks

Frequently Asked Questions

The global Machine Safety Market is estimated at US$ 5.4 Billion in 2026 and is projected to reach US$ 8.0 Billion by 2033, expanding at a CAGR of 5.7% over the forecast period. The market recorded a historical CAGR of 4.6% between 2020 and 2025, reflecting consistent growth aligned with industrial automation expansion.

The foremost demand drivers are mandatory regulatory compliance with standards such as ISO 13849, IEC 62061, and OSHA 29 CFR 1910.212, combined with the rapid global expansion of industrial automation and collaborative robotics. The U.S. BLS recorded 220,000 manufacturing workplace injuries in 2024, sustaining powerful organizational and regulatory imperatives to invest in certified machine safety systems.

Presence sensing safety sensors lead the component segment with an estimated 33% market share. Their role as the mandatory hazard-detection layer in all certified machine safety architectures, supported by Performance Level (PL) requirements under ISO 13849-1:2023, makes them the most universally deployed safety component across robotics, assembly, and packaging applications globally.

North America holds the leading regional position, driven by OSHA's comprehensive machine safety regulatory framework, a large base of automated industrial facilities, and the presence of globally significant market participants including Rockwell Automation and Honeywell International. The U.S. also benefits from the CHIPS and Science Act-funded semiconductor fab expansion generating premium-specification safety system demand.

The most compelling opportunity lies in IIoT-connected Safety-as-a-Service platforms that enable real-time remote monitoring, predictive diagnostics, and continuous compliance management for industrial safety devices. The US$ 52 Billion CHIPS and Science Act and the EU Chips Act targeting 20% global chip production share are creating high-value, SIL 2/3-rated safety system demand in new semiconductor fabrication facilities.

Leading companies in the global Machine Safety Market include Siemens, Rockwell Automation, Schneider Electric, ABB, Honeywell International, KEYENCE CORPORATION, Omron Corporation, SICK AG, Emerson Electric Co., Mitsubishi Electric, IDEC Corporation, Pilz GmbH & Co. KG, Banner Engineering Corp., Schmersal Group, and HIMA Paul Hildebrandt GmbH, among other regional specialists and system integrators.