- Industrial Goods & Service

- High Density Racks Market

High Density Racks Market Size, Share, and Growth Forecast, 2026 - 2033

High Density Racks Market by Cooling Compatibility (Air-Cooled, Liquid-Cooled, Hybrid-Ready), End-user (Hyperscale Data Centers, Colocation Providers, Enterprise IT, Government and Defense, Edge & Telecom), and Regional Analysis 2026 - 2033

High Density Racks Market Share and Trends Analysis

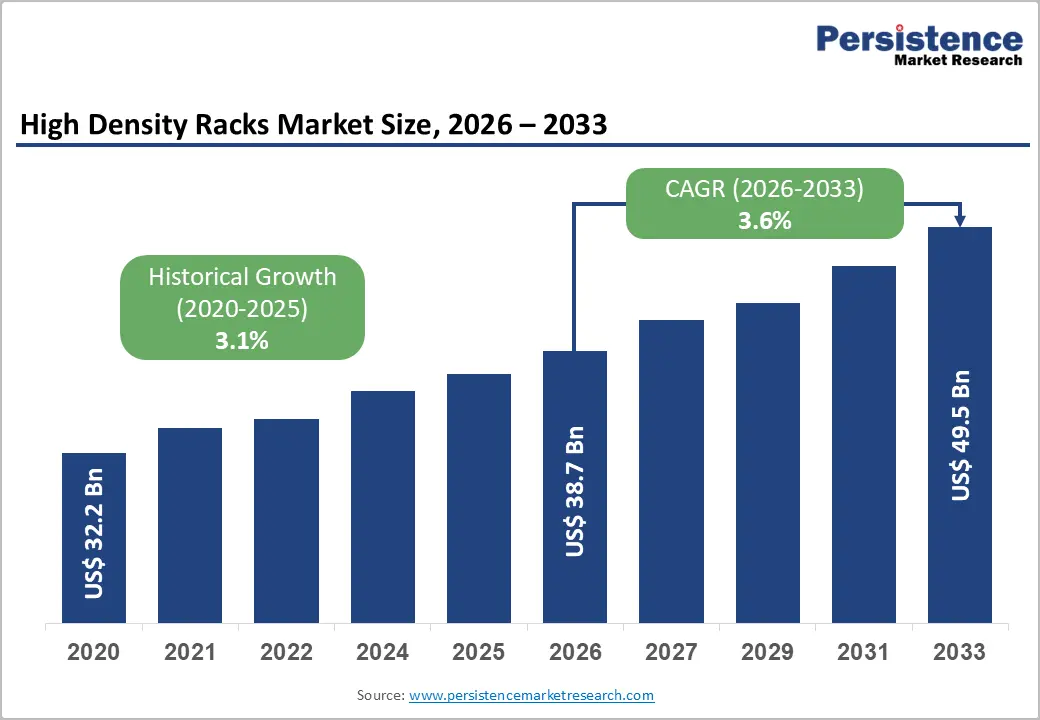

The global high density racks market is likely to be valued at US$38.7 billion in 2026 and is anticipated to reach US$49.5 billion by 2033, growing at a CAGR of 3.6% during the forecast period from 2026 to 2033, driven by the rapid rise in AI workloads, which continue to increase rack power densities year after year.

Expanding data center capacity to support intensive computing requirements is further fueling demand, with procurement accelerating among hyperscale operators as well as edge facilities. Additionally, the swift rollout of artificial intelligence infrastructure is creating the need for advanced cooling systems and efficient power distribution within server racks. As a result, demand is strengthening for robust, structurally reinforced enclosures capable of supporting higher equipment loads.

Key Industry Highlights:

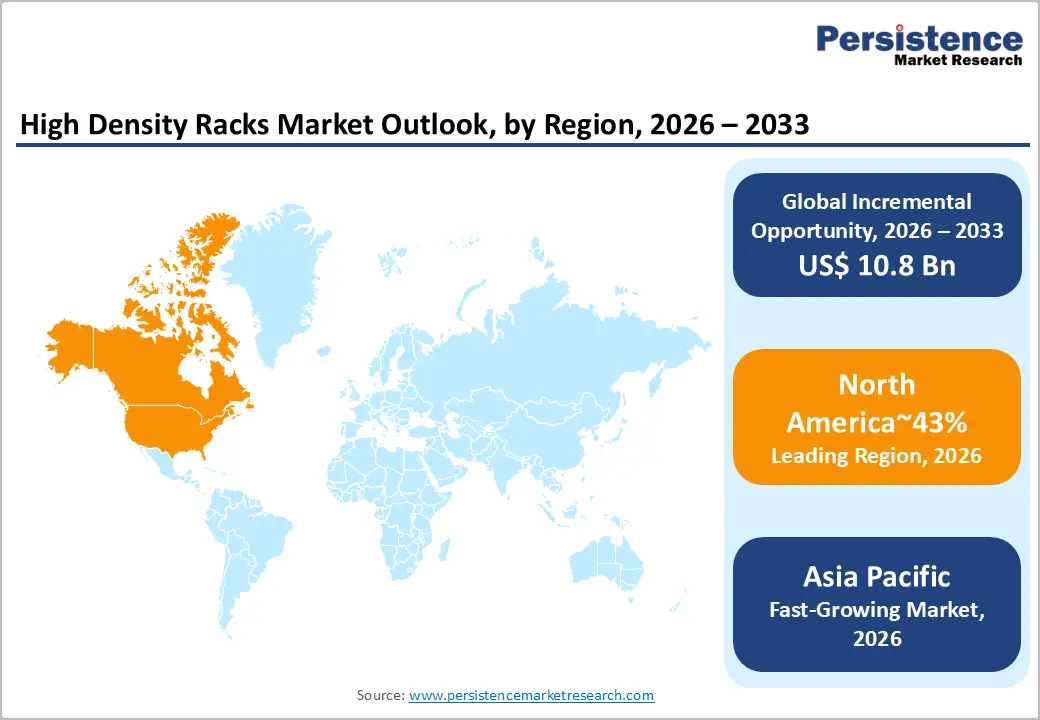

- Leading Region: North America is estimated to lead the market, with approximately 43% share in 2026, driven by a high concentration of hyperscale facilities and early adoption of generative artificial intelligence technologies.

- Fastest-growing Region: Asia Pacific is projected to be the fastest-growing region, driven by accelerating digital transformation and massive investments in modular data centers across emerging economies.

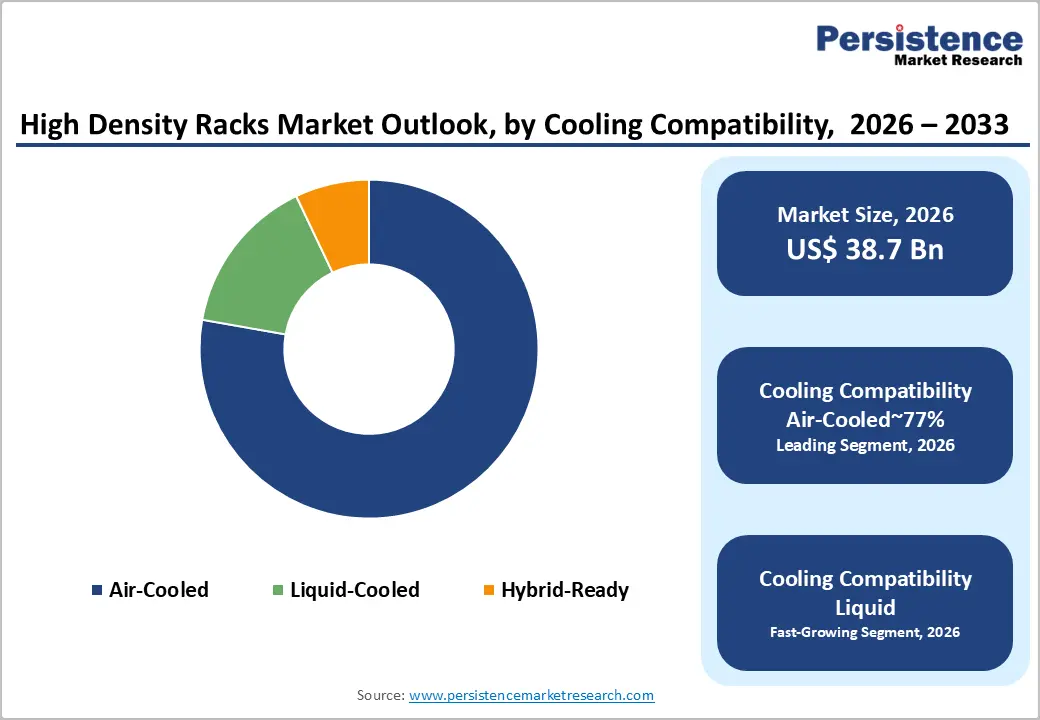

- Leading Cooling Compatibility: Air-cooled is expected to lead, accounting for approximately 77% share in 2026, through established presence in existing data center ecosystems, cost-effective compatibility for legacy facilities, and widespread availability of air-handling equipment.

- Leading End-user: Hyperscale data centers are projected to dominate for the massive scale of cloud infrastructure investments and continuous expansion of hyperscale facilities, with approximately 53% share in 2026.

- Competitive Environment: Market participants are focusing on integrated liquid cooling and power management solutions. Leading vendors are expanding manufacturing capacities in regional hubs to reduce lead times for hyperscale clients.

DRO Analysis

Driver - Artificial Intelligence Integration

Rapid adoption of generative artificial intelligence models drives extreme server rack power densities exceeding conventional infrastructure thresholds. Modern graphics processing units require power levels surpassing thirty kilowatts per cabinet, rendering traditional air-cooled systems operationally insufficient. This structural shift compels data center operators to transition toward liquid cooling architectures capable of managing concentrated thermal loads. Increasing computational intensity across enterprise workloads further accelerates demand for high-efficiency thermal management systems within advanced data environments.

Enterprise deployments expand through Vertiv with Liebert XDU Coolant Distribution Unit supporting high-performance computing clusters within existing facilities. These systems enable precise thermal regulation while maintaining energy efficiency under sustained processing loads. Integration of advanced power and cooling management frameworks enhances rack-level performance across dense computing environments. Growing reliance on such specialized infrastructure reinforces broader market acceleration driven by artificial intelligence adoption.

Edge Computing Expansion

Latency-sensitive applications across autonomous driving and industrial automation accelerate demand for localized data processing infrastructure. Compact high-density racks enable powerful computing within space-constrained regional environments supporting real-time analytics. Telecommunication providers deploy these systems within 5G base stations to reduce latency and enhance processing efficiency. This decentralized architecture strengthens modular infrastructure adoption across suburban and distributed network ecosystems.

Local deployments expand through Schneider Electric with EcoStruxure Data Center Solutions, enabling rapid installation across varied environmental conditions. Pre-configured modular systems reduce deployment timelines while maintaining operational consistency for edge nodes. Integrated monitoring software ensures uptime and performance stability across critical decentralized networks. Increasing reliance on modular designs reinforces vendor positioning within localized infrastructure and edge computing ecosystems.

Restraint - Thermal Management Complexity

Excessive heat generation in high-density computing environments creates major operational constraints for legacy data centers. Cooling high-performance chips exceeding seven hundred watts requires advanced liquid-to-chip heat exchange systems. Air-based cooling architectures cannot effectively dissipate such thermal loads, limiting the deployment of next-generation hardware. This mismatch between infrastructure capability and processing demand slows modernization across aging facilities.

Retrofitting complexity intensifies with Rittal through RiMatrix Next Generation, requiring extensive plumbing integration for liquid cooling loops. Facility upgrades demand significant capital investment and structural redesign across existing data center layouts. Medium-sized enterprises face cost barriers that delay the adoption of high-density computing systems. These infrastructure constraints persist as a key restraint on rapid migration toward advanced hardware environments.

Capital Expenditure Intensity

High-density data center construction demands substantial upfront capital compared with conventional server room deployments. Advanced liquid-cooled racks and specialized power distribution systems command premium pricing due to complex engineering requirements. Elevated interest rate environments further increase financing costs, making total ownership burdens difficult for smaller providers. This financial pressure limits competitive entry and slows infrastructure upgrades outside hyperscale environments.

Procurement constraints intensify with Panduit through FlexFusion Cabinets, offering modular benefits but maintaining high acquisition costs. Regional enterprises often defer upgrades and extend the lifecycle of legacy hardware to manage budget limitations. Capital sensitivity influences purchasing decisions, prioritizing cost control over performance enhancements. These constraints collectively slow the adoption of premium rack systems across secondary and mid-tier industrial sectors.

Opportunity - Liquid Cooling Adoption

Transition toward liquid cooling technologies creates a major revenue opportunity for advanced data center infrastructure providers. Traditional air cooling reaches physical limits as AI workloads demand higher thermal dissipation efficiency. Water-based systems become essential for managing dense GPU clusters and maintaining operational stability. Bloomberg indicates liquid cooling could reach 20% of data centers by 2030, highlighting a large replacement cycle for legacy air-cooled systems.

Dell Technologies with PowerEdge XE9680 Rack Integration supports high-density AI environments through built-in fluid handling systems. These platforms enable direct-to-chip cooling while optimizing rack-level efficiency and performance consistency. Early hyperscaler adoption validates the commercial scalability and operational reliability of liquid cooling infrastructures. Expanding deployment of such systems strengthens overall valuation across the high-density data center equipment ecosystem.

Sustainable Power Solutions

Rising regulatory pressure on data center emissions drives adoption of energy-efficient rack architectures. Vendors integrating intelligent power monitoring and high-efficiency distribution systems gain measurable operational advantages. Corporate sustainability mandates push procurement toward infrastructure, reducing Power Usage Effectiveness across large-scale facilities. This shift accelerates demand for rack designs optimizing both electrical efficiency and thermal management within high-density computing environments.

Environmentally focused operators expand investments through Cisco with Nexus 9000 Series Rack Kits supporting optimized airflow and reduced cooling energy requirements. These configurations lower reliance on high-power fans and chillers across intensive workloads. Alignment with green energy standards enhances eligibility for contracts with multinational technology firms prioritizing carbon reduction targets.

Category-wise Analysis

Cooling Compatibility Insights

Air-Cooled systems are expected to dominate, accounting for approximately 77% share in 2026, supported by their established presence in existing data center ecosystems. These systems remain the standard for enterprise IT halls and smaller colocation suites where power densities do not yet exceed 20 kW per rack. Most legacy facilities utilize raised-floor air distribution or hot-aisle containment, making air-cooled racks the most cost-effective and compatible option for routine infrastructure refreshes.

Vendors sustain this dominance by offering optimized airflow designs such as Rittal’s RiLineX platform, which improves cooling efficiency within traditional frameworks. Despite the rise of liquid cooling, the widespread availability of air-handling equipment, and the lower capital requirements of air-cooled enclosures, anchor their leading market position.

Liquid-cooled solutions are anticipated to be the fastest-growing segment, driven by the thermal demands of high-performance AI accelerators and massive GPU clusters. As processor TDPs surpass 700 watts, traditional air systems become physically incapable of removing heat efficiently, necessitating direct-to-chip or immersion cooling architectures. Cloud service providers and research institutions are increasingly adopting these systems to maximize compute density while reducing cooling energy consumption. The integration of cooling manifolds directly into the racking structure simplifies the deployment of these advanced thermal management solutions for hyperscale operators.

End-user Insights

Hyperscale data centers are expected to lead, accounting for approximately 53% share in 2026, underpinned by the massive scale of cloud infrastructure investments globally. These organizations operate vast campuses that require highly standardized, high-density racking units to maximize server count per square foot of white space. Their transition toward AI-centric hardware deployments necessitates enclosures that can support power loads exceeding 50 kW per cabinet.

Manufacturers cater to this demand through innovative solutions such as Vertiv’s PowerIT rack PDU, which provides the granular power control required for such massive deployments. The continuous expansion of hyperscale facilities in major data hubs ensures a steady procurement volume for specialized high-performance racks. This user group remains the primary anchor for large-format, liquid-ready enclosure systems.

Edge & telecom providers are anticipated to be the fastest growing segment, driven by the deployment of 5G networks and the proliferation of low-latency digital services. These users require compact, high-density enclosures that can be installed in constrained urban environments or remote industrial sites while maintaining server performance. The shift toward decentralized compute is supported by products such as Eaton’s, which offer pre-built, ruggedized infrastructure for rapid edge deployment.

As telecommunications firms upgrade their base stations to host AI-driven analytics at the network edge, the demand for dense, managed racks in small form factors is accelerating. These specialized enclosures provide the necessary environmental protection and cooling for high-performance hardware outside of traditional data center halls.

Regional Analysis

North America High Density Racks Market Trends

North America is expected to remain the leading regional market, accounting for approximately 43% share in 2026, supported by hyperscale infrastructure concentration and advanced digital ecosystem maturity. Demand is anticipated to be driven by artificial intelligence workloads requiring dense compute environments and high-capacity thermal management architectures across enterprise and cloud deployments.

U.S. High Density Racks Market Trends

The U.S. is expected to dominate, driven by the rapid transformation of hyperscale facilities into AI-focused compute environments. Extremely low data center vacancy rates accelerate the adoption of ultra-high-density rack configurations within constrained spaces. Vertiv Holdings Co expands domestic manufacturing to address supply constraints for power and cooling systems.

Canada High Density Racks Market Trends

Canada is anticipated to lead regional growth, supported by access to renewable energy and favorable climatic conditions. Lower cooling requirements enhance operational efficiency for high-density data center deployments across key regions. Schneider Electric collaborates with local firms to deploy modular high-density data center solutions.

Europe High Density Racks Market Trends

Europe is expected to remain a mature and structurally stable market, with demand anchored in stringent energy efficiency regulations and data governance frameworks. Enterprise adoption is anticipated to prioritize rack architectures delivering optimized power usage effectiveness under evolving sustainability compliance mandates. Replacement cycles are likely to dominate demand, driven by modernization of legacy financial and industrial data center environments.

Germany High Density Racks Market Trends

Germany is expected to dominate, driven by the Frankfurt data hub serving as a central European connectivity gateway. Regulatory mandates under energy efficiency laws enforce the adoption of heat reuse systems within data center operations. Rittal GmbH & Co. KG introduces advanced rack architectures aligned with high-density computing requirements.

U.K. High Density Racks Market Trends

The U.K. is anticipated to lead, supported by a high concentration of financial institutions and AI-driven enterprises. Space constraints and elevated land costs accelerate the adoption of vertically optimized high-density rack configurations. Eaton Corporation strengthens cooling infrastructure through the acquisition of advanced thermal solution providers.

Asia Pacific High Density Racks Market Trends

Asia Pacific is expected to register the fastest growth trajectory, approximating a significant global share, driven by rapid digital transformation and sovereign cloud infrastructure expansion. Demand is anticipated to accelerate due to exponential data generation from mobile ecosystems and enterprise digitization initiatives across emerging economies.

China High Density Racks Market Trends

China is expected to dominate, supported by national initiatives optimizing data distribution and high-performance computing capabilities. Strong patent activity in advanced computing technologies reinforces domestic demand for high-density rack systems. Inspur Group and Huawei Technologies integrate immersion cooling with rack architectures to enhance thermal efficiency.

India High Density Racks Market Trends

Market growth in India is supported by large-scale digitalization programs and an expanding data consumption base. Shift toward hyperscale artificial intelligence clusters strengthens demand for advanced high-density infrastructure. Schneider Electric expands local manufacturing capabilities for liquid cooling systems to support domestic deployments.

Competitive Landscape

The global high density racks market reflects a consolidated structure, with leading infrastructure vendors shaping procurement through integrated hardware and power ecosystems. Cisco strengthens enterprise positioning via Nexus 9000 rack-integrated solutions, combining networking and physical infrastructure. Vertiv Group Corp. advances power delivery standards through high-density rack systems optimized for AI workloads. Schneider Electric drives innovation via EcoStruxure-enabled racks supporting AI-ready deployments. Huawei Technologies expands high-density platforms targeting cost-performance optimization, while Rittal GmbH focuses on OCP-aligned designs and thermal management precision.

Key Industry Developments:

- In March 2026, ‘Vertiv’ announced a massive expansion of manufacturing capacity across North America and Mexico to meet rising AI infrastructure demand. This expansion includes two new facilities in South Carolina and a 45% capacity increase in Mexicali, enabling Vertiv to scale the production of integrated power modules and high-density rack systems with 7x regional capacity.

- In February 2026, Schneider Electric launched a dedicated Motivair liquid cooling solutions factory in India to accelerate high-density AI infrastructure. This facility focuses on manufacturing advanced cooling units essential for managing the thermal loads of ultra-high-density AI racks, strengthening Schneider’s local supply chain for the APAC region.

Companies Covered in High Density Racks Market

- Schneider Electric

- Vertiv

- Cisco

- Hewlett-Packard Enterprise

- Dell Technologies

- Eaton

- Rittal

- Legrand

- Huawei Technologies

- Panduit

- Delta Electronics

- IBM

- Fujitsu

- Chatsworth Products

- Belden

- Black Box

Frequently Asked Questions

The global high density racks market is projected to be valued at US$38.7 billion in 2026 and is expected to reach US$49.5 billion by 2033.

Excessive heat generation in high-density computing environments requires advanced liquid-to-chip heat exchange systems, and air-based cooling cannot effectively dissipate thermal loads from chips exceeding 700 watts, limiting deployment of next-generation hardware in legacy facilities.

The high density racks market is forecast to grow at a CAGR of 3.6% from 2026 to 2033.

North America is expected to lead with approximately 43% share in 2026, driven by hyperscale infrastructure concentration and AI workload adoption.

Key players include Schneider Electric, Vertiv Group Corp., Eaton Corporation, Rittal GmbH & Co. KG, Cisco Systems, Hewlett Packard Enterprise, Dell Technologies, Panduit, Legrand, and Huawei Technologies.